|

市場調查報告書

商品編碼

1644496

歐洲彈性辦公室:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Europe Flexible Office - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

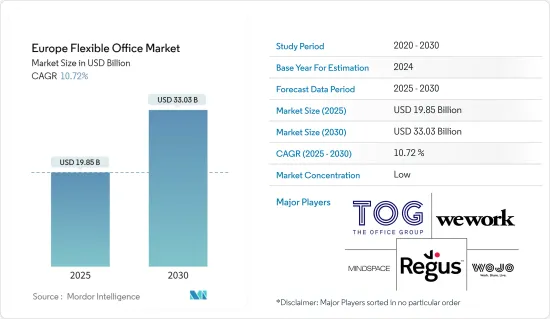

預計2025年歐洲彈性辦公市場規模為198.5億美元,到2030年預計將達到330.3億美元,預測期內(2025-2030年)的複合年成長率為10.72%。

主要亮點

- 2023 年第一季,歐洲彈性辦公空間將佔辦公空間總使用量的 4%,低於 2019 年的尖峰時段8% 和 2022 年第一季的 7%。排名榜首的是倫敦金融城,佔 13%,其次是布拉格(佔 8%)和阿姆斯特丹(佔 6%)。美國大城市也出現了類似的模式,彈性辦公室的使用率從 2019 年的 7% 下降到 2023 年的 1.5%。這一趨勢與全球變化相吻合,小型企業正在進入市場並將其業務擴展到大城市以外的地區。

- 中小企業的崛起是歐洲所有主要城市都出現的趨勢,新的工作方式與地點和產業無關。這些趨勢正在推動歐洲彈性辦公市場的發展。該地區的新興企業數量預計將推動市場成長。

- 數位系統日益成長的重要性以及執行密集型工作的需求導致員工對獨立工作的渴望激增,無論是在辦公室還是在他們選擇的任何地方。

- 這使得歐洲公司有機會透過更好地利用辦公空間、減少員工出行時間並提高員工滿意度來提高工作效率和生產力。預計這將在預測期內促進靈活辦公市場的成長。

- 雖然對靈活辦公室的需求持續成長,但採用這種模式仍面臨一些障礙。人們普遍關心的是更開放的環境中的資訊安全、保密性和隱私問題。這導致主要企業擔心其對行銷的潛在影響,尤其是可能會削弱自己的品牌。然而,這些擔憂被企業可能需要在投資組合中增加更多靈活空間的風險所抵消。這是由於勞動力市場正在發展,許多雇主難以留住和吸引高技能工人。

歐洲彈性辦公市場的趨勢

共享辦公空間需求不斷成長

租戶對靈活辦公空間和房東安裝的辦公空間越來越感興趣。此舉是為了因應裝修和資金籌措成本的上升,以及開發完工的延遲。選擇這些空間將有助於減輕這些風險並為您的租戶提供靈活性和便利性。此外,關鍵位置優質彈性辦公空間的稀缺性導致業主對配套空間的需求增加,一些中心報告稱其已滿租。

傳統上,小型租戶更喜歡 5,000 平方英尺以下的辦公空間,但我們看到 5,000 至 10,000 平方英尺辦公空間的交易明顯增加。

2022 年,倫敦金融城 10,000 平方英尺以下業主自配空間的交易量將翻倍。 2022 年,房東提供的空間佔倫敦金融城所有 10,000 平方英尺以下辦公室租賃交易的 42%,較 2021 年的 21% 大幅成長。

此外,對於由業主提供軟服務的全面管理空間的需求也日益成長。預計規模較小的租戶將繼續青睞健身空間,尤其是隨著包含軟服務的「套裝保險契約」變得越來越普遍。

英國佔市場主導地位

管理合約在英國越來越受歡迎,到 2023 年上半年將佔交易的 43%,而 2019 年僅為 9%。目前,英國有 14 家服務式辦公室營運商正在積極尋求超過 20,000 平方英尺的空間,其中 93% 的人傾向於管理合約模式。

受新興企業、辦公室租賃需求飆升以及靈活工作空間出現的推動,倫敦的辦公空間市場正在迅速擴張。

中小企業的快速成長是全國性的趨勢,新的工作方式超越了地點和產業的界限。

這些動態正在推動倫敦靈活的辦公市場,蓬勃發展的Start-Ups公司刺激了該地區的進一步擴張。

倫敦辦公大樓市場受到幾個關鍵因素的影響。這些顯著的趨勢包括竣工數量激增、租賃期限縮短、靈活工作空間領域的強勁成長、以及由於持續關注品質而導致的優質辦公空間供應過剩。

2023 年的最新研究強調,倫敦對彈性辦公空間的需求日益成長。隨著越來越多的企業希望重返辦公室,靈活的工作安排為現場辦公和遠距辦公都帶來了好處。

需求的增加將導致彈性辦公供應的減少和相關成本的增加。例如,2022 年,彈性工作空間中永久辦公桌的租金每季增加 3.4%,達到每月 690 英鎊(867.19 美元)。

歐洲彈性辦公產業概況

歐洲彈性辦公市場較為分散,彈性辦公空間市場參與者眾多。此外,隨著對休閒辦公環境的需求不斷成長,許多公司正在進入市場。歐洲靈活辦公市場中的公司正在採取多項成長和擴大策略以獲得競爭優勢。主要參與者包括 The Office Group、WeWork、WOJO、Regus Group、Mindspace 等。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 調查前提條件

- 研究範圍

第2章調查方法

- 分析方法

- 研究階段

第3章執行摘要

第4章 市場動態與洞察

- 當前市場狀況

- 科技趨勢

- 產業價值鏈分析

- 政府法規和舉措

- 辦公室租金洞察

- 辦公空間規劃洞察

- COVID-19 對市場的影響

第5章 市場動態

- 驅動程式

- 遠距工作熱潮推動市場

- 新興企業和小型企業的崛起

- 限制因素

- 提供類似服務的供應商增加將影響市場

- 影響市場的經濟不確定性與監管因素

- 機會

- 有潛力拓展尚未開發的市場

- 對遠距工作者和自由工作者日益成長的需求也推動了市場的發展。

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者/購買者的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭強度

第6章 市場細分

- 按類型

- 私人辦公室

- 共享辦公空間

- 虛擬辦公室

- 按最終用戶

- 資訊科技/通訊

- 媒體與娛樂

- 零售和消費品

- 按地區

- 德國

- 英國

- 法國

- 其他歐洲國家

第7章 競爭格局

- 公司簡介

- The Office Group

- WeWork

- WOJO

- Regus Group

- Mindspace

- KNOTEL

- Ordnung ApS

- Matrikel1

- Green desk

- DBH Business Services

- 其他公司

第 8 章:市場的未來

第 9 章 附錄

第10章 免責聲明

The Europe Flexible Office Market size is estimated at USD 19.85 billion in 2025, and is expected to reach USD 33.03 billion by 2030, at a CAGR of 10.72% during the forecast period (2025-2030).

Key Highlights

- In Q1 2023, flex office take-up in Europe constituted 4% of the total office take-up, marking a decline from its peak of 8% in 2019 and the 7% recorded in Q1 2022. Leading the pack, London City accounted for 13% of the take-up, with Prague at 8% and Amsterdam at 6%. A similar pattern emerged in major US cities, with flex office take-up dwindling from 7% in 2019 to 1.5% in 2023. This trend aligns with a global shift, where smaller operators enter the market and expand their footprint beyond major cities.

- The increase in small and medium-sized businesses is a trend observed across all major cities of Europe, while new working practices are neither location nor sector-specific. These trends have fueled the flexible office market in Europe. The number of startups in the region is expected to boost the market's growth.

- The growing significance of digital systems and the need for completing knowledge-intensive tasks has transformed into a surging desire among employees to work from the office or from any desired location in an independent way.

- This has offered firms in Europe a chance to utilize the office space more proficiently, reduce the traveling hours of employees, and increase employee satisfaction, thereby boosting their work efficiency and productivity. This will help the flexible office market grow during the forecast period.

- Although the demand for flexible office space continues to grow, some obstacles stand in the way of the adoption of this model. Commonly raised concerns include the issues of information security, confidentiality, and privacy in a more open environment. This leads to the companies worrying about the potential impact on their marketing, especially because it could weaken their brands. However, such concerns are outweighed by the risk that companies may need more flexible space in their portfolios. This is due to the developments in the labor market, with many employers worrying about either keeping or attracting the most highly skilled workers.

Europe Flexible Office Market Trends

Increasing Demand for Coworking Spaces

Occupiers are increasingly showing interest in both flexible office spaces and those fitted by landlords. This trend responds to the escalating costs of fit-outs and financing and delays in development completions. Opting for these spaces helps mitigate these risks and offers occupiers enhanced flexibility and convenience. Also, the scarcity of prime flexible office spaces in key locations further fuels the demand for landlord-fitted spaces, with some centers reporting full occupancy rates.

Traditionally, smaller tenants have preferred fitted office spaces, with most deals for spaces under 5,000 sq. ft. However, there has been a noticeable increase in the number of fitted office space deals, ranging from 5,000 to 10,000 sq. ft. This trend is particularly pronounced in the City of London market.

In 2022, the City of London doubled transaction volumes for landlord-fitted spaces below 10,000 sq. ft. Landlord-fitted spaces constituted 42% of all office leasing transactions below 10,000 sq. ft in the City of London in 2022, a significant jump from the 21% seen in 2021.

Additionally, there is a rising demand for fully managed spaces where landlords offer soft services. It is anticipated that smaller tenants will continue to prefer fitted spaces, particularly as 'package deals' that include soft services gain traction.

The United Kingdom Dominates the Market

Management agreements are gaining popularity in the United Kingdom, and they accounted for 43% of deals by H1 2023, a significant jump from just 9% in 2019. Currently, 14 serviced office operators in the United Kingdom are actively searching for spaces exceeding 20,000 sq. ft, and an overwhelming 93% prefer the management agreement model.

London's office space market is rapidly expanding, fueled by its thriving start-ups and IT sectors, surging office lease demands, and the emergence of flexible workspaces.

This surge in small and medium-sized businesses is a nationwide trend, while new work practices transcend location and sector boundaries.

These dynamics drive the flexible office market in London, as the region's burgeoning start-up scene is set to fuel its expansion further.

Several key factors are shaping London's office market. These include notable trends such as a surge in completions, shorter lease terms, robust growth in the flexible workspace segment, and an oversupply of prime office spaces due to a persistent preference for quality.

Recent studies from 2023 have highlighted an increasing demand for flexible office spaces in London. As businesses increasingly call for a return to the office, flexible work arrangements benefit both in-person and remote scheduling.

This heightened demand leads to a dwindling supply of flexible offices and a subsequent rise in costs. For instance, in 2022, the rental cost for a permanent desk in a flexible workspace saw a 3.4% quarterly increase, reaching GBP 690 per month (USD 867.19 per month).

Europe Flexible Office Industry Overview

The European flexible office market is fragmented, with many players existing in the flexible office spaces market. Also, many more companies are entering the market to meet the increasing demand for casual office environments. The European flexible office market companies are involved in several growth and expansion strategies to gain a competitive advantage. The major players include The Office Group, WeWork, WOJO, Regus Group, and Mindspace.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS AND DYNAMICS

- 4.1 Current Market Scenario

- 4.2 Technological Trends

- 4.3 Industry Value Chain Analysis

- 4.4 Government Regulations and Initiatives

- 4.5 Insights into Office Rents

- 4.6 Insights into Office Space Planning

- 4.7 Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Drivers

- 5.1.1 Booming remote work driving the market

- 5.1.2 Increasing number of start-ups and small businesses

- 5.2 Restraints

- 5.2.1 Growing number of providers offering similar services affecting the market

- 5.2.2 Economic uncertainities and regulatory factors affecting the market

- 5.3 Opportunities

- 5.3.1 The potential to expand into untapped markets

- 5.3.2 The evolving needs of remote workers and freeelancers are also driving the market

- 5.4 Industry Attractiveness - Porter's Five Forces Analysis

- 5.4.1 Bargaining Power of Suppliers

- 5.4.2 Bargaining Power of Consumers/Buyers

- 5.4.3 Threat of New Entrants

- 5.4.4 Threat of Substitute Products

- 5.4.5 Intensity of Competitive Rivalry

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Private Offices

- 6.1.2 Coworking Spaces

- 6.1.3 Virtual Offices

- 6.2 By End User

- 6.2.1 IT and Telecommunications

- 6.2.2 Media and Entertainment

- 6.2.3 Retail and Consumer Goods

- 6.3 By Geography

- 6.3.1 Germany

- 6.3.2 United Kingdom

- 6.3.3 France

- 6.3.4 Rest of Europe

7 COMPETITIVE LANDSCAPE

- 7.1 Overview (Market Concentration and Major Players)

- 7.2 Company Profiles

- 7.2.1 The Office Group

- 7.2.2 WeWork

- 7.2.3 WOJO

- 7.2.4 Regus Group

- 7.2.5 Mindspace

- 7.2.6 KNOTEL

- 7.2.7 Ordnung ApS

- 7.2.8 Matrikel1

- 7.2.9 Green desk

- 7.2.10 DBH Business Services*

- 7.3 Other companies