|

市場調查報告書

商品編碼

1644511

圍籬:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Fencing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

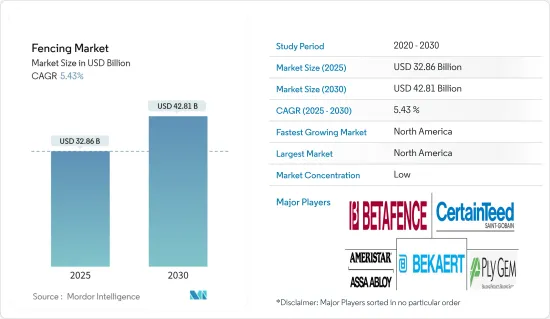

圍籬市場規模預計在 2025 年為 328.6 億美元,預計到 2030 年將達到 428.1 億美元,預測期內(2025-2030 年)的複合年成長率為 5.43%。

主要亮點

- 商業和住宅建築計劃的激增刺激了對圍欄的需求,推動了製造業的進步和技術創新,以滿足對可靠、持久的圍欄系統日益成長的需求。特別是,全球住宅領域的新建和改建項目正在增加,這成為全球圍欄市場的主要推動力。

- 製造公司不斷努力改進其產品以滿足客戶需求,從而促進該地區的市場成長。在北美和歐洲,人們非常重視保護寵物和資產,並加強了對竊盜和各種犯罪活動的防範。此外,歐洲各地對重建和維修計劃的需求也大幅增加。政府的支持優先考慮具有成本效益的解決方案,導致人們對塑膠圍欄的偏好日益增加。

- 亞太地區擁有中國和印度等新興市場,正在吸引投資者的興趣。然而,該地區繼續面臨貿易爭端和經濟放緩,國內需求疲軟,特別是中國和印度,導致包括製造業在內的一系列行業的投資和生產減少。

- 軍事組織經常使用電圍欄來阻止國際邊界附近的入侵。值得注意的是,中國軍隊在與印度有爭議的邊界的拉達克地區使用了帶刺鐵絲網,而俄羅斯軍隊則在中俄邊境安裝了防護電圍欄。人們對國家安全的擔憂日益加劇,預計將推動市場成長,因為電圍欄不僅可以阻止未經授權的進入,還可以防止野生動物進入農場,從而大大提高農場的安全性。然而,需要定期檢查以確保最佳性能,而電圍欄的高維護成本是市場擴張的障礙。為了應對這些挑戰並降低高昂的固定成本,人們正在探索無人道口圍欄等替代解決方案。

- 圍籬市場依用途分為三類:工業、農業和住宅。由於可支配收入的增加和家庭對安全和隱私的日益重視,住宅建設和改造正在推動住宅行業的擴張。此外,人們對有特色的圍欄的需求也日益增加,以增強住宅的美觀。由於需要保護農場、作物和牲畜免受野生動物和盜竊的侵害,農業部門預計將經歷快速成長。農業圍籬需求的增加是由於農業侵占案例的增加,導致圍籬需要根據客戶要求客製化,並使用高品質的原料。

圍籬市場的趨勢

北美圍籬市場創下最高成長率

- 北美住宅安全和安保領域的消費者需求顯著增加,推動了成長。同時,該地區越來越重視住宅,住宅建築計劃正在激增,預計未來幾年市場將進一步擴大。特別是農業領域對木柵欄的日益成長的偏好對於推動北美木柵欄市場至關重要。

- 日益成長的消費趨勢進一步推動了需求的激增,尤其是富裕和年輕的群體,他們正在尋找創新的圍欄解決方案。同時,不同收入水平的消費者都被木柵欄所吸引,因為它能保護隱私和安全。在北美市場,本土廠商佔據主導地位,其次是國內外廠商。領先的製造商優先考慮技術和設計創新以保持領先地位。

- 在北美,參與者也積極進行併購以擴大市場,國際參與者將注意力轉向當地競爭對手。雖然北美主要製造商主要透過線上平台直接向最終用戶銷售,但木柵欄的銷售主要透過線下管道進行,利用經銷商和零售商的影響。

房地產建設增加推動市場

- 預計隱私將成為 2023 年的一個大問題,將有更多客戶選擇板上板圍欄。設計使用垂直堆疊的木板來遮擋花園和房屋的視線,以防止窺探。與板條牆類似,柵欄圍欄由長而扁平的木板堆疊在一起製成,以形成木板牆。除了保護隱私之外,這種圍欄再次變得流行起來,因為它曾經在農村以外很少見到。 2023 年,越來越多的住宅希望用經濟高效、環保的圍欄材料來更新他們的圍欄。隨著永續性變得越來越重要,竹子、生物複合材料和天然灌木/樹籬屏障的需求預計將會增加。

- 中產階級的崛起正在幫助擊劍業務擴大。根據歐盟委員會預測,到2030年新興中產階級的數量將達到55億人。不斷成長的中產階級人口中約有87%是亞裔。住宅建設的增加和建築竣工的復甦正在推動圍欄行業的成長。由於業務增加和建築業投資增加,房地產市場的成長也推動了全球圍籬市場的擴張。定期檢查對於確保最佳性能是必要的,但由於與傳統電圍欄升級相關的改造和維護成本高,因此很難實施。高昂的維護成本是電圍欄發展的一個阻礙。農民正在轉向其他解決方案,例如無人機,以抵消在跨國界設置障礙所產生的高昂固定成本,而這可能會限制市場的擴張。

- 都市化進程的加速對圍籬市場的成長貢獻巨大。都市化是一個術語,描述的是人們從農村大規模遷移到人口密度較高的都市區。都市化將增加住宅和非住宅需求,推動圍籬市場向前發展。中階的擴張正在推動圍欄產業的發展。因此,預計未來圍欄行業的成長將受到都市化進程加快的推動。

圍籬行業概況

圍欄市場比較分散,由多家參與者組成。新建築計劃中住宅圍欄的成長是為參與者創造新機會的關鍵促進因素。主要參與者包括 CertainTeed、PLY Gem、Bekaert、BetaFence、Ameristar Perimeter Security 等。主要製造商之間為擴大市場而建立的策略夥伴關係和協議越來越多,推動著全球圍欄市場的成長。產業參與企業正在採用各種策略,例如新產品開發、夥伴關係、併購、協議和聯盟,以實現圍欄市場的成長。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 調查前提條件

- 研究範圍

第2章調查方法

- 分析方法

- 研究階段

第3章執行摘要

第4章 市場洞察

- 當前市場狀況

- 科技趨勢

- 供應鏈/價值鏈分析洞察

- 政府監管

- 深入了解圍籬所使用的材料

- COVID-19 市場影響

第5章 市場動態

- 驅動程式

- 政府對高速公路、機場和鐵路等基礎設施計劃的投資通常需要設置圍欄以確保安全。

- 圍欄技術的進步,例如整合監控和警報系統的智慧圍欄系統,正在吸引尋求增強安全解決方案的客戶。

- 限制因素

- 原物料價格上漲

- 低價產品競爭加劇

- 機會

- 對美觀圍欄解決方案的需求不斷增加

- 環保圍籬材料越來越受歡迎

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者/購買者的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭強度

第6章 市場細分

- 按類型

- 木柵欄

- 金屬柵欄

- 其他類型

- 按最終用戶

- 住宅

- 農業

- 軍事和國防

- 政府

- 石油和化工

- 礦業

- 能源和電力

- 倉庫

- 其他最終用戶

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 拉丁美洲

- 巴西

- 哥倫比亞

- 阿根廷

- 其他拉丁美洲國家

- 歐洲

- 德國

- 英國

- 法國

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太地區

- 中東和非洲

- 沙烏地阿拉伯

- 埃及

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

- 北美洲

第7章 競爭格局

- 市場集中度概覽

- 公司簡介

- CertainTeed

- PLY Gem

- Bekaert

- BetaFence

- Ameristar Perimeter Security

- Long Fence

- Gregory Industries

- A1 Fence Products

- Specrail

- Jerith

第 8 章:未來趨勢

第 9 章 附錄

- 宏觀經濟指標(按行業分類的GDP)

- 主要生產、消費、出口和進口統計數據

The Fencing Market size is estimated at USD 32.86 billion in 2025, and is expected to reach USD 42.81 billion by 2030, at a CAGR of 5.43% during the forecast period (2025-2030).

Key Highlights

- The surge in commercial and residential construction projects is fueling the need for fencing, prompting advancements and innovations in manufacturing to meet the rising demand for dependable and long-lasting fencing systems. Notably, the residential sector is experiencing an uptick in new builds and remodeling activities worldwide, serving as a primary catalyst for the global fencing market.

- Manufacturing firms continually strive to enhance their products to align with customer requirements, contributing to regional market growth. In North America and Europe, there's a notable emphasis on safeguarding pets and assets, bolstering protection against theft and various forms of criminal activity. Moreover, there's a considerable demand for renovation and retrofit projects throughout Europe. Government-backed initiatives prioritize cost-efficient solutions, leading to an increased preference for plastic fences.

- Asia-Pacific presents promising prospects for the fencing market, given its inclusion of rapidly developing nations like China and India, attracting considerable investor interest. However, trade disputes and economic deceleration persist in the region, particularly in China and India, where subdued domestic demand has led to reductions in investments and production across various sectors, including manufacturing.

- Military organizations often employ electric fencing to deter intrusions near international borders. Notably, China's military utilizes spiked electric wires in the Ladakh region along the disputed border with India, while the Russian military has installed electric fencing along the China-Russia border for protection. The growing focus on national security is expected to drive market growth, as electric fencing not only deters unauthorized human entry but also prevents wildlife encroachment, significantly enhancing farm safety. However, the market expansion is hindered by the substantial maintenance costs associated with electric fencing, which require regular inspections for optimal performance. Alternative solutions, such as unmanned crossings, are being explored to address these challenges and mitigate high fixed costs.

- The fencing market is segmented into three categories based on applications: industrial, agricultural, and residential. Residential construction and remodeling activities are driving the expansion of the residential segment, supported by rising disposable incomes and the increasing importance households place on security and privacy. Furthermore, there is a growing demand for distinctive fences to enhance the aesthetic appeal of residential properties. In the agricultural sector, rapid growth is anticipated due to the need to protect farms, crops, and livestock from wildlife and theft. This increased demand for agricultural fencing is driven by rising instances of agricultural intrusions, leading to the customization of fences according to customer specifications and the use of high-quality raw materials.

Fencing Market Trends

The Fencing Market in North America is Witnessing the Highest Growth Rate

- North America's residential safety and security sector is witnessing a notable uptick in consumer demand, driving its growth. Simultaneously, the region's emphasis on enhanced home aesthetics and a surge in residential construction projects are poised to bolster the market in the coming years. Notably, the agricultural sector's increasing preference for wood fencing is pivotal in propelling the North American wood fencing market.

- This surge in demand is further fueled by a rising trend among consumers, particularly the affluent and younger demographics, who seek innovative fencing solutions. On the other hand, consumers with varying income levels are gravitating towards wood fencing for privacy and security. Local manufacturers hold the lion's share in the North American market, with national and international players following suit. To stay ahead, industry leaders are prioritizing technological and design innovations.

- In North America, players are also actively pursuing M&A acquisitions to expand their market reach, while international players are eyeing local competitors. While major manufacturers in North America primarily sell directly to end-users through online platforms, wood fencing sales predominantly occur through offline channels, leveraging the influence of distributors and retailers.

Increasing Real Estate Construction Driving the Market

- In 2023, as privacy was predicted to be a major issue, more customers chose board-on-board fences. This design uses vertically overlapping boards to block the view of a yard or house and keep off prying eyes. Similar to a slatwall, a stockade fence is made of long, flat wooden planks that are placed one on top of the other to form a plank wall. In addition to privacy concerns, this type of fencing is once again becoming popular because it was so uncommon to see it outside of rural areas. In 2023, more homeowners wanted to update their fences using cost-effective, eco-friendly fencing materials. As sustainability became more important, bamboo, biocomposite materials, and natural shrub/hedge barriers were expected to witness an increase in demand.

- The rise of the middle class is helping the expansion of the fencing business. According to the European Commission, by 2030, there are likely to be 5.5 billion members of the emerging middle class. Around 87% of the growing middle-class population will be Asian. Rising home building and a rebound in building completions are driving the growth of the fencing sector. The expansion of the global fencing market is also being fueled by growth in the estate market, brought on by a rise in firms and greater investment in the construction sector. Regular inspections are necessary to ensure optimal performance, but they are challenging to carry out due to the high cost of improvements and maintenance associated with upgrading conventional electric fences. Hefty maintenance expenses hamper its growth. Farmers are seeking other solutions, like unmanned drones, to offset the high fixed costs linked with the necessity to deploy barriers over international boundaries, which may stifle market expansion.

- Rising urbanization is considerably contributing to the growth of the fence market. Urbanization is the term used to describe the widespread movement of people from rural to urban areas, which leads to higher human population densities in urban areas. Urbanization is increasing the demand for both residential and non-residential structures, which will advance the fence market. The expansion of the middle class is helping the fencing industry. Consequently, future fencing industry growth is anticipated to be fueled by rising urbanization.

Fencing Industry Overview

The fencing market is fragmented and consists of many players. The growth of residential fencing in new construction projects is a significant driver of new opportunities for the players. The major players are CertainTeed, PLY Gem, Bekaert, BetaFence, Ameristar Perimeter Security, and many more. Growing strategic partnerships and agreements among key manufacturers for market expansion are boosting the growth of the global fencing market. The industry participants have adopted various strategies, such as new product developments, partnerships, mergers and acquisitions, agreements, and collaborations, to achieve growth in the fencing market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Technological Trends

- 4.3 Insights on Supply Chain/Value Chain Analysis

- 4.4 Government Regulations

- 4.5 Insights on Materials Used for Fencing

- 4.6 Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Drivers

- 5.1.1 Government Investments in Infrastructure Projects, Such as Highways, Airports, and Railways, Often Require Fencing for Safety and Security

- 5.1.2 Advancements in Fencing Technologies, Such as Smart Fencing Systems With Integrated Surveillance and Alarm Systems, are Attracting Customers Looking for Enhanced Security Solutions

- 5.2 Restraints

- 5.2.1 Soaring Prices of Raw Material

- 5.2.2 Increasing Competition from Low-cost Products

- 5.3 Opportunities

- 5.3.1 Increasing Demand for Aesthetically Pleasing Fencing Solutions

- 5.3.2 Increasing Popularity of Eco-friendly Fencing Materials

- 5.4 Industry Attractiveness - Porter's Five Forces Analysis

- 5.4.1 Bargaining Power of Suppliers

- 5.4.2 Bargaining Power of Consumers / Buyers

- 5.4.3 Threat of New Entrants

- 5.4.4 Threat of Substitute Products

- 5.4.5 Intensity of Competitive Rivalry

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Wood Fencing

- 6.1.2 Metal Fencing

- 6.1.3 Other Types

- 6.2 By End User

- 6.2.1 Residential

- 6.2.2 Agricultural

- 6.2.3 Military and Defense

- 6.2.4 Government

- 6.2.5 Petroleum and Chemicals

- 6.2.6 Mining

- 6.2.7 Energy and Power

- 6.2.8 Warehouse

- 6.2.9 Other End Users

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.1.3 Mexico

- 6.3.2 Latin America

- 6.3.2.1 Brazil

- 6.3.2.2 Colombia

- 6.3.2.3 Argentina

- 6.3.2.4 Rest of Latin America

- 6.3.3 Europe

- 6.3.3.1 Germany

- 6.3.3.2 United Kingdom

- 6.3.3.3 France

- 6.3.3.4 Russia

- 6.3.3.5 Rest of Europe

- 6.3.4 Asia-Pacific

- 6.3.4.1 China

- 6.3.4.2 Japan

- 6.3.4.3 India

- 6.3.4.4 South Korea

- 6.3.4.5 Rest of Asia-Pacific

- 6.3.5 Middle East and Africa

- 6.3.5.1 Saudi Arabia

- 6.3.5.2 Egypt

- 6.3.5.3 South Africa

- 6.3.5.4 United Arab Emirates

- 6.3.5.5 Rest of Middle East and Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Market Concentration Overview

- 7.2 Company Profiles

- 7.2.1 CertainTeed

- 7.2.2 PLY Gem

- 7.2.3 Bekaert

- 7.2.4 BetaFence

- 7.2.5 Ameristar Perimeter Security

- 7.2.6 Long Fence

- 7.2.7 Gregory Industries

- 7.2.8 A1 Fence Products

- 7.2.9 Specrail

- 7.2.10 Jerith*

8 FUTURE TRENDS

9 APPENDIX

- 9.1 Marcroeconomic Indicators (GDP breakdown by sector)

- 9.2 Key Production, Consumption, Exports & Import Statistics

2025年3D虛擬圍籬全球市場報告

2025年3D虛擬圍籬全球市場報告 圍欄市場:按類型、應用和地區

圍欄市場:按類型、應用和地區 車輛護欄柵欄門市場,按產品類型、按應用、按材料、按控制系統、按國家和地區 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率和預測2025 年全球圍籬市場報告

車輛護欄柵欄門市場,按產品類型、按應用、按材料、按控制系統、按國家和地區 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率和預測2025 年全球圍籬市場報告 全球鋼鐵柵欄及柵欄零件市場擊劍市場 - 全球產業規模、佔有率、趨勢、機會和預測(按類型、最終用戶、地區和競爭分類,2019-2029 年)2024 年深水養殖網箱全球市場報告2024 年漁網和水產養殖網箱全球市場報告

全球鋼鐵柵欄及柵欄零件市場擊劍市場 - 全球產業規模、佔有率、趨勢、機會和預測(按類型、最終用戶、地區和競爭分類,2019-2029 年)2024 年深水養殖網箱全球市場報告2024 年漁網和水產養殖網箱全球市場報告 車輛自動道閘市場:現況分析及未來預測(2024-2032)鋼板網市場報告:趨勢、預測和競爭分析(至 2030 年)

車輛自動道閘市場:現況分析及未來預測(2024-2032)鋼板網市場報告:趨勢、預測和競爭分析(至 2030 年)