|

市場調查報告書

商品編碼

1644634

系統整合-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)System Integration - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

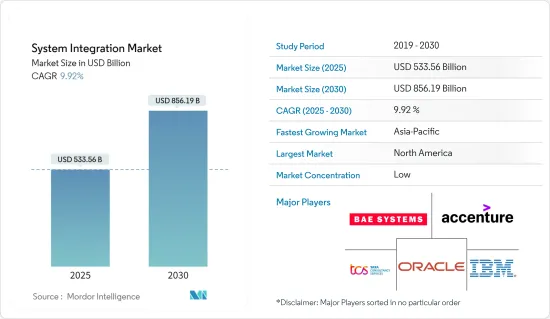

系統整合市場規模預計在 2025 年為 5,335.6 億美元,預計到 2030 年將達到 8,561.9 億美元,預測期內(2025-2030 年)的複合年成長率為 9.92%。

系統整合市場受到雲端技術的不斷發展和採用以及由於生產力提高和成本降低而導致的終端行業需求不斷成長的推動。

關鍵亮點

- 系統整合是將幾個單獨的子系統或子組件組合成一個更大的系統的過程,以便子系統可以協同工作。此外,系統整合將組織與第三方(包括客戶、供應商和股東)連結起來。

- 雲端運算的日益普及和中小型企業的快速成長正在推動全球系統整合市場向前發展。此外,對低成本、節能製造流程的需求也對系統整合市場的成長產生了積極影響。

- 此外,隨著對軟體即服務 (SaaS) 解決方案的需求不斷成長,雲端整合變得越來越流行。雲端整合工具為組織連接不同的系統創造了新的機會。雲端整合的優勢包括公共產業成本、無單點故障、可擴展性、地理獨立性以及缺乏硬體支持,所有這些都有助於人們接受和採用雲端整合解決方案和服務。因此,包括金融服務和軟體公司在內的各種各樣的企業都在使用雲端運算。

- 一些行業參與者正在與較小的雲端供應商合作,以增加他們的雲端使用量。例如,2022 年 4 月,Google與埃森哲、Confluent、Databricks、德勤、 推出 DB 等公司合作成立了資料雲聯盟,以使資料在不同業務系統、平台和環境中更具可攜性和可訪問性。聯盟成員將提供基礎設施、API 和整合支持,以確保跨多個平台和跨多個領域的產品的資料可攜性和可訪問性。為了幫助企業進行資料庫遷移,Google Cloud 與系統整合商和顧問公司合作,包括 TCS、Deloitte、Kyndryl、HCL、Wipro、Infosys、Cognizant 和 Capgemini。

- 系統整合透過整合不同的流程使組織能夠更智慧地運作。由於企業複雜性影響組織的競爭和獲利方式,公司開始意識到系統整合的重要性。系統整合技術為企業IT基礎設施提供集中的、整合的、經濟高效的解決方案。推動系統整合市場擴張的主要因素之一是資訊科技用戶的增加。美國勞工統計局預測,到 2031 年,電腦相關職業的就業人數將增加 15%。

- 然而,缺乏客戶知識和業務預算限制阻礙了系統整合產業的發展。此外,系統整合的高成本使得中小企業難以轉向系統整合,從而抑制了市場的成長。相反,邊緣運算、物聯網 (IoT) 和人工智慧整合等技術進步可能會為整個預測期內系統整合市場的擴張提供有利的前景。

系統整合市場趨勢

軟體/應用整合成長強勁

- 軟體整合是將不同類型的軟體子系統整合為單一統一的系統。軟體整合是必要的,原因有很多,例如建立資料倉儲,其中資料需要透過 ETL 流程移動,或整合各種資料庫或檔案式的系統。領先的企業正在轉向基於軟體即服務 (SaaS)雲端基礎的解決方案,以幫助他們輕鬆管理某些業務流程。

- 對自動化技術的需求不斷成長、雲端運算的採用以及不斷擴大的寬頻基礎設施是推動系統整合市場中軟體整合部分成長的關鍵因素。

- 系統整合使組織能夠存取並同時可視化資料,以便做出更好的決策。因此,雲端運算技術的採用、寬頻基礎設施的擴展以及企業對提高現有系統效率的需求不斷成長是推動全球整合軟體市場成長的關鍵因素。此外,消費者對虛擬的興趣日益濃厚也推動了產業的擴張。

- 2022 年 3 月,思科系統公司公佈了 Cisco Intersight 平台與公共雲端的新整合,以使 Kubernetes 叢集和虛擬機器可在多個雲端中觀察到。此外,思科也將推出 HyperFlex 超融合基礎設施,以增加邊緣運算並為用戶擴展混合雲端功能。這使組織能夠更快地交付用於雲端整合的基礎架構和應用程式。

- 2023 年 5 月,Sonata Software 也被選為拜耳新的雲端基礎的農業食品解決方案的系統整合合作夥伴。專門實施、規劃、協調、調度、測試和升級技術解決方案的公司被視為系統整合合作夥伴。我們從根本上控制複雜 IT 解決方案的生命週期,從部署到營運。

北美佔據主要市場佔有率

- 由於大型企業擴大採用雲端基礎的服務以及物聯網在工業自動化中的應用日益廣泛,北美佔據了最大的市場。隨著該地區的 BFSI 行業也採用現代技術,北美的系統整合市場具有巨大的成長潛力。為了實現這一目標,銀行正在努力確保滿足每位客戶的需求。

- 此外,企業可擴展性的提高以及巨量資料、雲端基礎的服務和軟體即服務(SaaS)等先進技術的普及,增加了北美各地組織的業務的複雜性。

- 因此,對分散式資訊技術 (IT) 解決方案(例如系統整合)的需求日益增加,以簡化不同的系統。此外,iPaaS(整合平台即服務)解決方案的整合將擴大運輸和石油天然氣行業的系統整合應用。它允許跨多個應用程式共用整合資源。

- 此外,2023 年 6 月,金融基礎設施和整合技術及整合平台即服務 (iPaaS) 供應商 PortX 將發布其 Integration Manager 產品 2.0 版本。這是一次重大更新,包含許多尖端功能,旨在提高對數位核心整合的控制並簡化業務流程。 Integration Manager 2.0 為金融機構提供的 API主導流程自動化最大限度地減少了內部員工的壓力,並列出了核心提供者未提供的廣泛解決方案。

- 此外,美國銀行聲稱,70% 的美國銀行客戶使用數位服務來滿足他們的金融需求。數位服務將幫助美國銀行擴大客戶群並保持市場競爭力。在預測期內,隨著組織轉向系統整合服務,該地區對系統整合服務的需求預計將會增加。

- 隨著各行各業尋求透過系統整合來提高生產力,該地區已經確定了一系列合作夥伴關係和合作關係。例如,2022年5月,紅帽宣布與通用汽車夥伴關係,擴大邊緣軟體定義汽車的開發,為電動車的普及奠定基礎。該夥伴關係將支援各種車載安全和非安全相關的應用,包括駕駛輔助程序、資訊娛樂、連接和車身控制。

系統整合行業概況

系統整合市場競爭激烈,許多日本國內及海外公司進入該市場。隨著市場預期擴大並提供更多機會,預計將有更多參與企業逐步進入市場。研究涉及的市場主要企業包括埃森哲、IBM 公司、威普羅有限公司等。這些參與企業正在採取各種成長策略,如併購、新產品發布、業務擴張、合資和夥伴關係,以加強在該市場的地位。

- 2022 年 4 月-布魯克公司宣布收購軟體和系統整合公司 Optimal Industrial Automation and Technologies。對 Optimal 的 Biopharma Tools 的收購增強了布魯克作為小分子、生技藥品和新型藥物模式製藥公司領先軟體和解決方案提供者的地位。

- 2022 年 2 月-Ansys 和 AWS 宣佈建立策略夥伴關係。該合作夥伴關係使得 ANSYS 產品能夠在 AWS 上部署,從而使模擬工作負載更易於訪問,並提供可擴展性和靈活性,以便從任何地方透過 Web 瀏覽器輕鬆存取軟體和儲存解決方案。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況

- 產業價值鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 購買者/消費者的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭強度

- COVID-19 市場影響評估

- 市場促進因素

- 雲端技術的進步與應用

- 提高生產力並降低 IT 管理成本

- 市場問題

- 系統整合高成本

第5章 市場區隔

- 按服務類型

- 基礎設施整合

- 軟體/應用整合

- 諮詢

- 按最終用戶產業

- 車

- 航太和國防

- 資訊科技和電訊

- BFSI

- 醫療

- 石油和天然氣

- 其他(能源、化工、採礦等)

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 法國

- 英國

- 亞洲

- 印度

- 中國

- 日本

- 澳洲和紐西蘭

- 拉丁美洲

- 中東和非洲

- 北美洲

第6章 競爭格局

- 公司簡介

- Accenture

- IBM Corporation

- Tata Consultancy Services Limited

- Oracle Corporation

- BAE systems

- Wipro Limited

- Cognizant

- Deloitte Touche Tohmatsu Limited

- Infosys Limited

- MDS Systems Integration(MDS SI)

第7章投資分析

第8章 市場機會與未來趨勢

The System Integration Market size is estimated at USD 533.56 billion in 2025, and is expected to reach USD 856.19 billion by 2030, at a CAGR of 9.92% during the forecast period (2025-2030).

The system integration market is driven by the ongoing advancement and adoption of cloud technologies and increased demand from end-use industries because of increased productivity and less cost.

Key Highlights

- System Integration refers to combining multiple individual subsystems or sub-components into one more extensive system, allowing the subsystems to function together. Furthermore, system integration connects the organization with third parties, including customers, suppliers, and shareholders.

- The growing usage of cloud computing and the rapid growth of small and medium-sized organizations (SMEs) are propelling the global system integration market forward. Furthermore, the desire for low-cost and energy-efficient manufacturing processes is favorably impacting the growth of the system integration market.

- Furthermore, Cloud Integration has grown in popularity as the demand for the Software as a Service (SaaS) solution continues to increase. Cloud integration tools have opened new opportunities for organizations to connect disparate systems. The advantages of cloud integration include utility-style costing, the absence of a single point of failure, scalability, geographical independence, and the lack of hardware support, all contributing to cloud integration solutions and services being accepted and implemented. As a result, various businesses, including financial services and Software companies, use cloud computing.

- Several industry participants are partnering with small cloud providers in order to increase cloud usage. For instance, In April 2022, Google launched a Data Cloud Alliance in partnership with Accenture, Confluent, Databricks, Deloitte, Mongo DB, etc., to make data more portable and accessible across disparate business systems, platforms, and environments. Members of the alliance will provide infrastructure, APIs, and integration support to ensure data portability and accessibility between multiple platforms and products across various domains. To help enterprises migrate their databases, Google Cloud has partnered with system integrators and consulting firms such as TCS, Deloitte, Kyndryl, HCL, Wipro, Infosys, Cognizant, and Capgemini.

- System integration allows more intelligent organizational operations by bringing together different processes. As enterprise complexity has an impact on an organization's capacity to compete and generate profit, businesses are beginning to recognize the significance of system integration. Technologies for system integration offer businesses centralized, integrated, and cost-effective solutions for their IT infrastructure. One of the major factors propelling the expansion of the system integration market is the rise in information technology users. The U.S. Bureau of Labor Statistics predicts that employment in computer-related occupations will rise by 15% by 2031.

- However, a lack of client knowledge and business budgetary restraints are impeding the growth of the system integration industry. Also, The high cost associated with system integration makes it difficult for small and medium enterprises to switch to system integration, restraining market growth. On the contrary, technological advancements such as the integration of edge computing, the internet of things (IoT), and artificial intelligence are likely to provide lucrative prospects for system integration market expansion throughout the forecast period.

System Integration Market Trends

Software/Application Integration to have a Significant Growth

- Software integration is bringing together various types of software sub-systems to create a single unified system. Software integration can be required for several reasons, including setting up a data warehouse where data needs to be moved through an ETL process and linking various databases and file-based systems. Major organizations use software-as-a-service (SaaS) cloud-based solutions, enabling them to manage particular business processes without a hassle.

- The increasing need for automation technologies, cloud computing usage, and expanding broadband infrastructure are some of the key factors driving the growth of the software integration segment in the system integration market.

- Due to system integration, organizations can access and visualize data simultaneously for better decision-making. As a result, the adoption of cloud computing technology, the growth of broadband infrastructure, and the rising demand from businesses to improve the efficiency of their current systems are some of the key factors driving the market growth of the global integration software market. Also boosting industry expansion is growing consumer interest in virtualization.

- In March 2022, Cisco Systems, Inc. revealed that its new Cisco Intersight platform integrations with public cloud integration would enable Kubernetes clusters and virtual machines to be observable across several clouds. In addition, Cisco HyperFlex Hyper-Converged Infrastructure was introduced to increase edge computing and expand users' hybrid cloud capabilities. This would allow the organization to offer infrastructure and apps for cloud integrations more quickly.

- Sonata Software was also chosen in May 2023 to serve as the system integration partner for Bayer's new cloud-based agri-food solution. A company that specializes in implementing, planning, coordinating, scheduling, testing, and upgrading technological solutions is considered a System Integration partner. It essentially controls the complex IT solution's deployment to operation lifecycle.

North America to Hold Major Market Share

- North America held the largest market as a result of the expanding use of cloud-based services by large enterprises and the expanding use of IoT in industrial automation. The BFSI sector of the region has also embraced modern technology, which has enormous growth potential for the North American system integration market. In order to accomplish this, banks are working very hard to ensure that they meet every customer's needs.

- Also, the rising scalability among businesses and the widespread adoption of advanced technologies, such as big data, cloud-based services, and Software-as-a-Service (SaaS), have increased the complexity of operations in different organizations in the North American region.

- Consequently, there is a rise in demand for distributed information technology (IT) solutions, such as system integration, for streamlining different systems. Additionally, integrating Integration Platform as a Service (iPaaS) solutions expands system integration applications in the transportation and oil and gas industries. It allows sharing of integrated resources across multiple applications.

- Moreover, In June 2023, PortX, a provider of financial infrastructure and integration technology that offers Integration-Platform-as-a-Service (iPaaS), will release version 2.0 of its Integration Manager product. This is a significant update that is jam-packed with cutting-edge features made to improve control over digital core integration and streamline business processes. The API-driven process automation offered by Integration Manager 2.0 to FIs minimizes the stress on internal staff and offers a wide range of solutions not offered by core providers.

- Also, 70% of Bank of America's clients use digital services for their financial needs, the bank claims. It can aid the bank in expanding its clientele and maintaining its competitiveness in the market. During the projected period, there will be an increase in the demand for system integration services in the region as a result of organizations switching to these services.

- The region is witnessing various partnerships and collaborations as industries look to switch to system integration to increase productivity. For instance, In May 2022, Red Hat announced a partnership with General Motors to expand the development of software-defined vehicles at the edge and lay the foundation for broader electric vehicle adoption. This partnership will support various in-vehicle safety and non-safety-related applications, including driver assistance programs, infotainment, connectivity, and body control.

System Integration Industry Overview

The system integration market is significantly competitive, with several local and international players operating. With the market expected to broaden and yield more opportunities, more players are expected to enter the market gradually. The key players in the market studied include Accenture, IBM Corporation, and Wipro Limited. These players have adopted various growth strategies, such as mergers and acquisitions, new product launches, expansions, joint ventures, partnerships, and others, to strengthen their position in this market.

- April 2022 - Bruker Corporation announced the acquisition of Optimal Industrial Automation and Technologies, a software and system integration company. The Optimal biopharma tools acquisition strengthens Bruker as a key software and solutions provider for small molecule, biologics, and new drug modalities pharma companies.

- February 2022 - Ansys and AWS announced a strategic partnership. The collaboration will enable the deployment of Ansys products on AWS - making simulation workloads more user-friendly while offering scalability and flexibility with easy access to software and storage solutions from anywhere with a web browser.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of the impact of COVID-19 on the Market

- 4.5 Market Drivers

- 4.5.1 Advancements and adoption of cloud-technologies

- 4.5.2 Benefits of increasing productivity while reducing IT Management cost

- 4.6 Market Challenges

- 4.6.1 High cost associated with system integration

5 MARKET SEGMENTATION

- 5.1 By Service Type

- 5.1.1 Infrastructure Integration

- 5.1.2 Software/Application Integration

- 5.1.3 Consulting

- 5.2 By End-user Industry

- 5.2.1 Automotive

- 5.2.2 Aerospace and Defense

- 5.2.3 IT and Telecom

- 5.2.4 BFSI

- 5.2.5 Healthcare

- 5.2.6 Oil and Gas

- 5.2.7 Others (Energy, Chemical, Mining etc.)

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 France

- 5.3.2.3 United Kingdom

- 5.3.3 Asia

- 5.3.3.1 India

- 5.3.3.2 China

- 5.3.3.3 Japan

- 5.3.4 Australia and New Zealand

- 5.3.5 Latin America

- 5.3.6 Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Accenture

- 6.1.2 IBM Corporation

- 6.1.3 Tata Consultancy Services Limited

- 6.1.4 Oracle Corporation

- 6.1.5 BAE systems

- 6.1.6 Wipro Limited

- 6.1.7 Cognizant

- 6.1.8 Deloitte Touche Tohmatsu Limited

- 6.1.9 Infosys Limited

- 6.1.10 MDS Systems Integration (MDS SI)

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

2025年全球整合系統市場報告

2025年全球整合系統市場報告 系統整合市場:按解決方案、公司規模、產業和地區分類整合系統市場 - 全球產業規模、佔有率、趨勢、機會和預測,細分、按產品、按服務、按最終用戶、按地區和競爭,2020-2030F

系統整合市場:按解決方案、公司規模、產業和地區分類整合系統市場 - 全球產業規模、佔有率、趨勢、機會和預測,細分、按產品、按服務、按最終用戶、按地區和競爭,2020-2030F 系統整合市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測系統整合市場 - 全球產業規模、佔有率、趨勢、機會和預測,按服務類型、企業規模、垂直產業、地區和競爭細分,2019-2029F系統整合市場規模、佔有率、按服務類型、公司規模、最終用途和地區分類的成長分析 - 產業預測,2024-2031 年

系統整合市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測系統整合市場 - 全球產業規模、佔有率、趨勢、機會和預測,按服務類型、企業規模、垂直產業、地區和競爭細分,2019-2029F系統整合市場規模、佔有率、按服務類型、公司規模、最終用途和地區分類的成長分析 - 產業預測,2024-2031 年 2024-2032 年按服務(基礎設施整合、應用程式整合、諮詢)、最終用途產業(BFSI、政府、製造、電信、零售、石油和天然氣、醫療保健等)和地區分類的系統整合市場報告整合系統市場、機會、成長動力、產業趨勢分析與預測,2024-2032

2024-2032 年按服務(基礎設施整合、應用程式整合、諮詢)、最終用途產業(BFSI、政府、製造、電信、零售、石油和天然氣、醫療保健等)和地區分類的系統整合市場報告整合系統市場、機會、成長動力、產業趨勢分析與預測,2024-2032 UC 2.0系統整合全球市場:2024-2028電信系統整合市場 - 按整合(硬體、設備、應用程式、資料)、按企業規模、按應用程式(網路管理、營運支援系統、業務支援系統、5G 服務)、按部署模型和預測 2024 - 2032 年

UC 2.0系統整合全球市場:2024-2028電信系統整合市場 - 按整合(硬體、設備、應用程式、資料)、按企業規模、按應用程式(網路管理、營運支援系統、業務支援系統、5G 服務)、按部署模型和預測 2024 - 2032 年