|

市場調查報告書

商品編碼

1644867

空調設備:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Air Conditioning Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

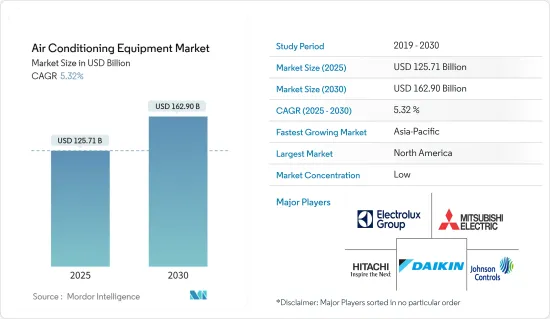

空調設備市場規模預計在 2025 年為 1,257.1 億美元,預計到 2030 年將達到 1,629 億美元,預測期內(2025-2030 年)的複合年成長率為 5.32%。

空調的工作原理是從空間中吸收熱量,排放室外,並冷卻室內的空氣。然後,冷卻的空氣會透過通風系統在整個建築物內循環。作為 HVAC 系統的重要組成部分,空調對於維持舒適的生活溫度至關重要。

通常稱為「分離式系統」的空調由室外機中的冷凝器和室內機中的蒸發器組成。除濕的工作原理是將室內暖空氣移到冷蒸發器上,使空氣凝結並釋放水分。分離式系統的特點是室內機和室外機是分開的,但也有整合室外機的「套裝」系統。

主要亮點

- 建築業的成長預計將增加住宅、商業和工業領域對空調設備的需求。住宅、商業和工業領域的建築支出增加以及建築許可激增。值得注意的是,在聯邦政府對基礎設施大量投資的推動下,美國建築業預計將進一步成長。這一積極趨勢不僅限於公共計劃,私人商業建築也正在蓬勃發展。

- 特別是在開發中國家,快速的都市化和經濟擴張推動了住宅和商業建築的激增,從而增加了對空調系統的需求。隨著收入的增加,越來越多的家庭和企業能夠投資和安裝空調設備。

- 氣候變遷導致全球氣溫上升,導致世界各地熱浪的頻率和強度增加。因此,對空調系統的需求正在激增。這種需求在歷史上冷氣需求較低的地區尤其明顯。

- 空調在美國家庭中比在歐洲家庭中更為普及。這一趨勢很大程度上是由美國某些地區的氣候需求所推動的。

- 例如,潮濕的南部和乾燥的西南部歷來需要冷卻解決方案。國際能源總署指出,美國西南部中暑警告數量增加,凸顯了情勢的嚴重性。此外,美國中南部以其高濕度而聞名,這意味著空調非常普遍。相反,以混合濕潤氣候和年降水量超過 20 英吋為特徵的中西部地區的空調使用量也顯著增加。

- 受俄烏衝突和經濟放緩影響,空調市場面臨重大波動。通貨膨脹和利率上升抑制了消費者支出,減少了需求並阻礙了市場成長。此外,美國貿易緊張局勢加劇了全球供應鏈的中斷,對兩國的空調設備製造商產生了重大影響。

空調設備市場趨勢

分離式系統可望大幅成長

- 分離式空調由室外機和室內機組成。在單分體系統中,室內機和室外機透過銅管連接。多分體系統允許將客戶選擇的最多五個室內機組連接到一個室外機組。多分體空調適用於多房間、大房間和各種氣候區。另一個主要優點是室外機佔地面積小,易於安裝。

- 兩家公司聯手推出節能、氣候友善的分離式空調。例如,LG電子在其2024年產品系列中宣布推出一系列針對印度市場的空調。這些設備擁有先進的技術,並優先考慮能源效率和使用者舒適度。 LG 2024 AC 系列配備了 Energy Manager,這是一項可最佳化能源使用並確保最佳冷卻效果的技術。

- 此外,美的全易系列R290機組的推出也標誌著一個轉捩點。 Midia 的可攜式R290空調已在歐洲銷售一段時間了。世界上最常用的冷凍設備是分離式空調,安裝在外牆上。 Midia 的 R290 分離式空調預計將顛覆歐洲市場,並引發歐洲大陸減少能源使用和溫室氣體排放的變化。

- 此外,2024年4月,三星電子新加坡今天推出了最新的WindFree空調系列。此次產品的推出標誌著三星家電產品線的擴展,旨在改善住宅的生活方式。此系列具有舒適冷卻、節能和注重聯網生活等特色。

- 此外,LG電子表示,2023年其空調產量約1,203萬台。這些產品是在韓國、印度、中國和泰國的工廠生產的。

預計北美將佔據較大的市場佔有率

- 北美空調設備市場是一個強勁且充滿活力的產業,受快速都市化、技術進步、氣候變遷和極端天氣事件等因素所驅動。

- 由於全球暖化和氣候變遷導致美國都市區以及西南部和南部陽光地帶的氣溫上升,這些地區各種空調系統的使用增加。美國某些地區,例如潮濕的南部和沙漠化的西南部,對空調的需求早已成為現實。

- 國際能源總署指出,美國西南部高溫警告數量增加,凸顯人類福祉面臨的嚴峻局勢。此外,美國南部和中部濕度較高,因此使用空調的情況很普遍。相反,中西部地區屬於混合濕潤氣候,每年降水量超過 20 英吋。預計這些因素將推動該國對空調的需求。

- 此外,根據美國能源部 (DOE) 的數據,高達 75% 的美國家庭都擁有空調。這些機組消耗了全國總發電量的約 6%,每年為屋主帶來約 290 億美元的損失。

- 結果,每年約有 1.17 億噸二氧化碳排放到大氣中。隨著人們越來越努力地轉向更節能的空調和實施其他策略以保持舒適的室內溫度,以及減少用於製冷的能源使用,市場潛力預計會增加。

空調產業概況

空調設備產業競爭激烈,國內外企業都積極參與。國際參與者正在透過與當地參與者的合作擴大在該國的業務。隨著市場預計擴大並提供更多機會,預計將有更多參與者進入市場。所研究的市場的主要企業包括三菱電機和江森自控。這些主要企業正在採用各種成長策略,如併購、新產品發布、業務擴張、合資和夥伴關係,以鞏固其在該市場的地位。

- 2024 年 3 月,三菱電機特靈 HVAC美國有限責任公司 (METUS) 宣布推出 Premier 壁掛式室內機 (MSZ-GS/MSY-GS)。同時,Premier MSZ-GS 室內機相容於單區和多區熱泵室外機,包括單區和多區超級加熱逆變器 (H2i) 機。 MSY-GS 是一款單區空調,適用於不需要暖氣的氣候。

- 2024 年 2 月:DAIKIN INDUSTRIES透過專注於關鍵要素來增強空調。冷媒由全球暖化潛勢較低的R32改為HFC-32,更重視環保與節能。此外空調的基本性能也得到了提升。大金的一項重要舉措是,將於 2024 年 11 月推出大樓用多功能空調。該系列擁有業界領先的能源效率,這對於減少您的環境影響和營運負擔至關重要。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 產業價值鏈分析

- 評估影響市場的宏觀經濟因素

第5章 市場動態

- 市場促進因素

- 更換現有設備以提高性能

- 政府支持法規,包括透過稅額扣抵計劃獎勵節能

- 市場挑戰

- 依賴宏觀經濟經濟狀況

第6章 市場細分

- 按類型

- 分離系統(管道式和無管道式)

- 可變冷媒流量 (VRF)

- 空氣調節機

- 冷卻器

- 風機盤管

- 室內套餐和屋頂

- 其他類型

- 按最終用戶產業

- 住宅

- 商業

- 產業

- 按地區

- 北美洲

- 亞洲

- 澳洲和紐西蘭

- 歐洲

- 拉丁美洲

- 中東和非洲

第7章 競爭格局

- 公司簡介

- Daikin Industries Ltd

- Hitachi Ltd

- Electrolux AB Corporation

- Mitsubishi Electric Corporation

- Johnson Controls

- Haier Group

- Carrier Corporate

- Panasonic Corporation

- Alfa Laval AB

- Lennox International Inc.

第8章投資分析

第9章:市場的未來

The Air Conditioning Equipment Market size is estimated at USD 125.71 billion in 2025, and is expected to reach USD 162.90 billion by 2030, at a CAGR of 5.32% during the forecast period (2025-2030).

An air conditioner extracts heat from a space and expells it outside, cooling indoor air. This cooled air is then circulated throughout a building via ventilation. Air conditioners are crucial in maintaining comfortable living temperatures as a pivotal HVAC system component.

Commonly referred to as "split systems," air conditioners consist of an outdoor unit, the condenser, and an indoor unit, the evaporator. Dehumidification occurs as warm indoor air moves over the cold evaporator, causing the air to condense and shed moisture, akin to how condensation forms on chilled glass. While split systems feature distinct indoor and outdoor units, there's also a "packaged" system where elements are integrated into a single outdoor unit.

Key Highlights

- The growing construction sector is expected to boost the demand for AC equipment in the residential, commercial, and industrial sectors. The increasing construction spending and a surge in building permits across residential, commercial, and industrial sectors. Notably, the US construction sector is set for further growth, supported by significant federal investments in infrastructure. This positive trend isn't limited to public projects; private commercial construction is also gaining momentum.

- Rapid urbanization and economic expansion, especially in developing nations, are fueling a surge in residential and commercial construction, driving the demand for air conditioning systems. With increasing incomes, a growing number of households and businesses can now invest in and deploy air conditioning units.

- The escalation of global temperatures due to climate change has heightened the frequency and intensity of heatwaves worldwide. Consequently, there has been a surge in the demand for air conditioning systems. This demand is particularly pronounced in regions that historically had lower cooling needs.

- Air conditioning is significantly more prevalent in American households than in European ones. This trend is largely attributed to the climatic demands of specific US regions.

- For instance, the humid South and arid Southwest have historically necessitated cooling solutions. Highlighting the severity of the situation, the IEA has noted a rise in heat alerts in the Southwestern United States, underscoring the health risks. Moreover, central and southern US regions, known for their high humidity, exhibit a higher prevalence of air conditioning. Conversely, the Midwest, characterized by a mixed-humid climate and annual precipitation exceeding 20 inches, also sees a notable uptake in air conditioner usage.

- The air conditioning equipment market faced substantial disruptions due to the Russia-Ukraine conflict and an economic slowdown. Rising inflation and interest rates curbed consumer spending, dampening demand and stalling market growth. Additionally, the trade tensions between the United States and China exacerbated global supply chain disruptions, significantly affecting AC manufacturers in both nations.

Air Conditioning Equipment Market Trends

Split System is Expected to Register Significant Growth

- A split air conditioner consists of an outdoor unit and an indoor unit. In single-split systems, an interior and outdoor unit are connected by copper pipe. In multi-split systems, up to five indoor units of customer choice can be connected to one outside unit. The multi-split is appropriate for many rooms or large rooms and various climatic zones. The outdoor unit's small footprint and easy installation are major benefits.

- The firms are collaborating to provide energy-efficient and climatic-friendly split air conditioners. For instance, in its 2024 product lineup, LG Electronics introduced a series of air conditioners tailored for the Indian market. These units boast advanced technology, prioritizing energy efficiency and user comfort. LG's 2024 AC range has the Energy Manager, a technology that optimizes energy usage and guarantees top-notch cooling.

- Furthermore, introducing Midea's All Easy Series R290 units is a tipping point. Midea's portable R290 air conditioners have been available in Europe for some time. The most often used appliances for cooling spaces globally are split air conditioners mounted on an exterior wall. The R290 split air conditioners from Midea are expected to disrupt the European market and spark a change that will lower the continent's energy use and greenhouse gas emissions.

- Furthermore, in April 2024, Samsung Electronics Singapore unveiled its newest WindFree Air Conditioner series today. This launch marks an expansion of Samsung's lineup of home appliances aimed at enhancing homeowners' lifestyles. The series boasts features like comfort cooling, energy-saving capabilities, and a focus on connected living.

- In addition, according to LG Electronics, in 2023, it produced approximately 12.03 million air conditioners. These units were manufactured across facilities in South Korea, India, China, and Thailand.

North America is Expected to Hold Significant Market Share

- The air conditioning equipment market in North America is a robust and dynamic industry driven by factors such as rapid urbanization, technological advancements, climate change, and extreme weather.

- The rise in temperature in American cities and the sunbelt regions of Southwestern and southern America, caused by global warming and climate change, has led to greater use of different air conditioning systems in these areas. The necessity of cool air in specific US regions, like the humid South and the desert Southwest, has been a longstanding reality.

- The IEA has noted a rise in heat alerts in the Southwestern United States, underscoring the difficult conditions for human well-being. Additionally, the use of air conditioning is more common in the southern and central regions of the United States because of the higher levels of humidity found in those areas. Conversely, the Midwest encounters a mixed-humid climate with an annual rainfall exceeding 20 inches. These factors are expected to propel the demand for air conditioners in the country.

- Furthermore, according to the Department of Energy (DOE), a substantial 75% of US households own air conditioning units. These units consume roughly 6% of the nation's total electricity production, leading to an annual cost of approximately USD 29 billion for homeowners.

- As a result, approximately 117 million metric tons of carbon dioxide are emitted into the atmosphere annually. The growing initiatives to shift towards more energy-efficient air conditioners and implement other strategies to maintain comfortable indoor temperatures, as well as the goal of reducing energy usage for cooling purposes, are expected to enhance the market's potential.

Air Conditioning Equipment Industry Overview

The air conditioning equipment landscape is highly competitive, with several local and international players active. International participants operate in the country through partnerships with regional players. With the market expected to broaden and yield more opportunities, more players are expected to enter. The key players in the market studied include Mitsubishi Electric and Johnson Controls, among others. These major players have adopted various growth strategies, such as mergers and acquisitions, new product launches, expansions, joint ventures, partnerships, and others, to strengthen their position in this market.

- March 2024: Mitsubishi Electric Trane HVAC US LLC (METUS) announced the introduction of Premier Wall-mounted Indoor Units (MSZ-GS/MSY-GS). At the same time, Premier MSZ-GS Indoor Units are compatible with single-zone and multi-zone heat pump outdoor units, including single- and multi-zone Hyper-Heating INVERTER (H2i) units. The MSY-GS is a single-zone, cooling-only air conditioner for climates with unnecessary heating.

- February 2024: Daikin Industries Ltd enhanced its air conditioners by focusing on critical elements. This includes shifting to HFC-32, an R32 refrigerant with low global warming potential, emphasizing its eco-friendliness and energy efficiency. Additionally, Daikin has bolstered the fundamental performance of its air conditioning units. In a significant move, Daikin is set to launch the VRV 7 multi-air conditioner series for buildings in November 2024. This series boasts the industry's top energy efficiency and is pivotal in lessening environmental footprints and operational burdens.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Replacement of Existing Equipment With Better Performing Ones

- 5.1.2 Supportive Government Regulations Including Incentives for Saving Energy Through Tax Credit Programs

- 5.2 Market Challenges

- 5.2.1 Dependence on Macro-economic Conditions

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Split System (Ducted and Ductless)

- 6.1.2 Variable Refrigerant Flow (VRF)

- 6.1.3 Air Handling Units

- 6.1.4 Chillers

- 6.1.5 Fan Coils

- 6.1.6 Indoor Packaged and Roof Tops

- 6.1.7 Other Types

- 6.2 By End-user Industry

- 6.2.1 Residential

- 6.2.2 Commercial

- 6.2.3 Industrial

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Asia

- 6.3.3 Australia and New Zealand

- 6.3.4 Europe

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Daikin Industries Ltd

- 7.1.2 Hitachi Ltd

- 7.1.3 Electrolux AB Corporation

- 7.1.4 Mitsubishi Electric Corporation

- 7.1.5 Johnson Controls

- 7.1.6 Haier Group

- 7.1.7 Carrier Corporate

- 7.1.8 Panasonic Corporation

- 7.1.9 Alfa Laval AB

- 7.1.10 Lennox International Inc.

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

氟泵空調市場:按類型、容量、技術、應用、最終用途和分銷管道分類,全球預測,2026-2032年

氟泵空調市場:按類型、容量、技術、應用、最終用途和分銷管道分類,全球預測,2026-2032年 住宅風管設計軟體市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、模組及功能分類

住宅風管設計軟體市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、模組及功能分類 日本空調市場規模、佔有率、趨勢和預測:按產品、應用和地區分類,2026-2034年

日本空調市場規模、佔有率、趨勢和預測:按產品、應用和地區分類,2026-2034年 2026年全球空調設備市場報告

2026年全球空調設備市場報告 住宅空調市場-全球產業規模、佔有率、趨勢、機會及預測(依產品類型、通路、地區及競爭格局分類,2021-2031年)交流太陽能空調市場按類型、技術、功率輸出、銷售管道和最終用戶分類-2026-2032年全球預測全球儲能貨櫃空調市場:依技術、儲能技術、冷氣、應用及銷售管道分類,2026-2032年預測商用中央空調市場按產品類型、建築類型、安裝類型、容量範圍和最終用戶分類 - 全球預測(2026-2032 年)商用太陽能空調市場按產品類型、安裝類型、容量範圍、應用、最終用戶和分銷管道分類-2026年至2032年全球預測

住宅空調市場-全球產業規模、佔有率、趨勢、機會及預測(依產品類型、通路、地區及競爭格局分類,2021-2031年)交流太陽能空調市場按類型、技術、功率輸出、銷售管道和最終用戶分類-2026-2032年全球預測全球儲能貨櫃空調市場:依技術、儲能技術、冷氣、應用及銷售管道分類,2026-2032年預測商用中央空調市場按產品類型、建築類型、安裝類型、容量範圍和最終用戶分類 - 全球預測(2026-2032 年)商用太陽能空調市場按產品類型、安裝類型、容量範圍、應用、最終用戶和分銷管道分類-2026年至2032年全球預測 全球空調市場(2025 年)

全球空調市場(2025 年)