|

市場調查報告書

商品編碼

1645103

亞太增壓壓縮機:市場佔有率分析、產業趨勢與成長預測(2025-2030 年)Asia-Pacific Booster Compressor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

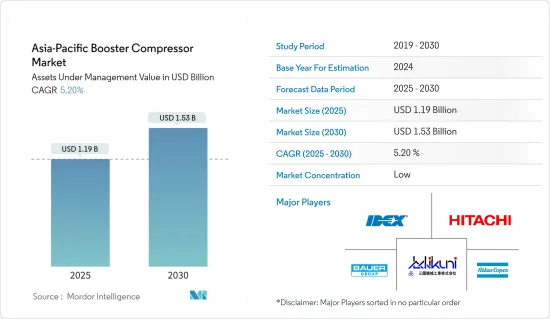

亞太地區增壓壓縮機市場規模(基於管理資產)預計將從 2025 年的 11.9 億美元成長到 2030 年的 15.3 億美元,預測期內(2025-2030 年)的複合年成長率為 5.2%。

關鍵亮點

- 從中期來看,各種因素都在推動增壓壓縮機市場的成長,包括全部區域工業計劃數量的增加以及各種應用對天然氣的需求不斷增加。

- 另一方面,由於使用現有的壓縮系統來避免新安裝的高昂支出,該技術的高安裝成本也可能抑制市場成長。

- 預計從煤炭發電廠到天然氣發電廠的快速轉變以及車輛中天然氣使用的增加將為主要企業提供有利可圖的成長機會,以在未來幾年維持其市場地位。

- 由於能源消耗的增加,預計中國將在預測期內佔據市場主導地位。

亞太地區增壓壓縮機市場趨勢

預計石油和天然氣產業將主導市場

- 增壓壓縮機用於石油和天然氣價值鏈的許多應用,涵蓋從上游、下游到中游的所有環節。在天然氣管道傳輸系統的中游段,採用此技術的比例最大。目前,世界正趨向於增加天然氣消費以滿足能源需求,加速天然氣輸送網路的成長。

- 2023 年亞太地區天然氣消費量將達到 905 億立方英尺/天 (bcf/d),比 2016 年成長 34%。這一成長主要是由於工業、商業和住宅領域擴大轉向更清潔的能源產出方法。為了平衡供需狀況,全國各地正在鋪設多條天然氣管道。

- 澳洲擁有遍布全國的管道網路。該國的天然氣管道容量遠超過石油管線。 2023年,天然氣輸送管將超過4.2萬公里,以高壓方式將天然氣從生產基地高效輸送到大、小城市的郊區。

- 該國非常熱衷於開發新的管道以支援現有的基礎設施並進一步發展天然氣出口能力和能力。例如,2023年8月,APA集團位於西澳大利亞的新北部金礦區互聯互通(NGI)管道正式開通。這條長達580公里的地下管道將把丹皮爾市與班伯里天然氣管道和金礦區天然氣管道連接起來,為現有和新的天然氣產區和天然氣儲存基礎設施提供更好的通道,特別是珀斯盆地。

- 馬來西亞擁有亞洲最大的天然氣管道網路之一,天然氣發行系統(NGDS)總長約2,468公里,可滿足該國國內的天然氣需求。該國管道公司正在不斷實施新計劃。

- 2023 年 8 月,工業氣體公司空氣產品公司表示將在檳城峇六拜自由工業區和峇都交灣工業建設、擁有和營運兩家氮氣工廠。該公司計劃進一步擴大這兩個地區的管道網路。此次對額外產能和基礎設施的策略性投資旨在加強該公司在馬來西亞北部的主導地位及其滿足市場需求的能力。

- 預計這些發展將推動亞太地區增壓壓縮機市場的未來成長。

中國可望主導市場

- 中國的高都市化正在不斷增加能源消耗,從而帶來發電工程和新的燃料供應運輸系統的增加。天然氣是中國最受歡迎的發電能源之一。

- 根據BP世界能源統計報告,2023年該國以天然氣為基礎的發電量約為297.8TWh。政府對更清潔的電力來源實施了嚴格的監管,刺激了未來幾年大量天然氣發電廠計劃。

- 中國是世界上最大的天然氣進口國,正在尋求減少燃煤發電廠的發電量,從而增加對天然氣的需求以滿足其能源需求。例如,2023年10月,GE Vernova的天然氣發電業務與哈爾濱電氣宣布,國投旗下吉能(舟山)燃氣發電公司已訂單兩台GE 9HA.02燃氣渦輪機的訂單,將用於中國浙江省舟山群島的一座新的聯合循環發電廠。

- 中國是亞太地區最大的原油和天然氣生產國,2023年約佔該地區原油和天然氣總產量的57.6%和33.8%。預計2023年原油產量為419.8萬桶/日,與前一年同期比較成長2.1%,較2020年成長7.6%。

- 截至 2023 年 1 月,中國在建天然氣管道約 17,800 公里(價值約 219 億美元),印度在建天然氣管道 14,300 公里(價值約 207 億美元),這一距離可繞地球四分之三以上。

- 增壓壓縮機市場也受到中國為滿足該國日益成長的天然氣需求而規劃的新天然氣輸送管道的推動。 2022 年 10 月,中國國家發展和改革委員會 (NDRC)核准建造一條連接四川省(中國西南部)天然氣田和湖北省(中國中部)的天然氣管道,輸送能力為每年 200 億立方英尺。建設工程預計於 2022 年 12 月開工,並於 2024年終完工。該計劃由中國管道集團西南管道公司開發。

- 這些新興市場的發展很可能帶動中國增壓壓縮機市場的未來成長。

亞太地區增壓壓縮機產業概況

亞太地區增壓壓縮機市場呈現細分化。市場的主要企業包括 IDEX India Private Ltd、日立、Bauer Kompressoren、Mikuni Kikai Kogyo 和阿特拉斯·科普柯有限公司。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究範圍

- 市場定義

- 調查前提

第 2 章執行摘要

第3章調查方法

第4章 市場概況

- 介紹

- 2029 年市場規模與需求預測(十億美元)

- 最新趨勢和發展

- 政府法規和政策

- 市場動態

- 驅動程式

- 工業計劃成長

- 各種用途對天然氣的需求不斷增加

- 限制因素

- 安裝成本高

- 驅動程式

- 供應鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 投資分析

第5章 市場區隔

- 冷卻類型

- 空氣冷卻

- 水冷

- 最終用戶

- 石油和天然氣

- 化學

- 發電

- 其他

- 地區

- 中國

- 印度

- 印尼

- 馬來西亞

- 泰國

- 越南

- 其他亞太地區

第6章 競爭格局

- 併購、合資、合作與協議

- 主要企業策略

- 公司簡介

- IDEX India Private Ltd

- Hitachi Ltd

- Bauer Kompressoren

- Mikuni Kikai Kogyo Co. Ltd

- Atlas Copco Ltd

- Haskel International, Inc.

- Kirloskar Pneumatic Co. Ltd

- General Electric Company

- Ingersoll-Rand PLC

- Aircomp Enterprise

- 市場排名分析

- 其他知名公司名單

第7章 市場機會與未來趨勢

- 從燃煤發電廠轉向燃氣發電廠

- 汽車汽油使用量增加

簡介目錄

Product Code: 50002214

The Asia-Pacific Booster Compressor Market size in terms of assets under management value is expected to grow from USD 1.19 billion in 2025 to USD 1.53 billion by 2030, at a CAGR of 5.2% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, various factors, such as the growth in industrial projects across the region and the escalating natural gas demand for various applications, are driving the growth of the booster compressor market.

- On the other hand, since the technology involves high installation costs, the use of existing compression systems to avoid the high expenditure on new installations could constrain market growth.

- Nevertheless, there is a rapid transition from coal to gas power stations, as well as a rise in the use of gas in motor vehicles, which is expected to provide lucrative growth opportunities for key players to maintain their position in the market in the coming years.

- China is expected to dominate the market during the forecast period due to the increase in energy consumption.

Asia-Pacific Booster Compressor Market Trends

The Oil and Gas Segment is Expected to Dominate the Market

- Booster compressors are used in a number of applications in the oil and gas value chain, covering all the sectors from upstream and downstream to the midstream. The maximum deployment was observed in the midstream segment in the gas pipeline transit systems. The world is currently drifting toward high natural gas consumption for energy requirements, upscaling the growth of gas transmission networks.

- The natural gas consumption in Asia-Pacific in 2023 was recorded as 90.5 billion cubic feet per day (bcf/day), an increase of 34% compared to 2016. The growth was primarily due to the increased inclination toward cleaner methods of energy generation in the industrial, commercial, and residential sectors. Many cross-country and national gas pipelines are being laid down to balance the supply-demand scenario.

- Australia has an extensive pipeline network all over the country. The country's gas pipeline capacity dominates the landscape relative to oil pipelines. The country has more than 42,000 km of natural gas transmission pipelines in 2023 that efficiently transported gas under high pressure from where it is produced to the outskirts of cities both large and small.

- The country is very keen on developing new pipelines to support its existing infrastructure and further develop its gas exporting capacity and capability. For instance, in August 2023, The APA Group's new Northern Goldfields Interconnect (NGI) pipeline in Western Australia was officially opened. The 580-kilometer buried pipeline connects Dampier City to the Bunbury Natural Gas Pipeline and the Goldfields Gas Pipeline, providing better access to existing and new natural gas production regions and gas storage infrastructure, especially in the Perth Basin.

- Malaysia has one of the most extensive natural gas pipeline networks in Asia, totaling about 2,468 km for the Natural Gas Distribution System (NGDS) to meet the domestic demand for gas in Malaysia. The pipeline companies in the country are constantly executing new projects.

- In August 2023, Air Products, an industrial gas company, announced that it would build, own, and operate two nitrogen plants in Penang's Bayan Lepas Free Industrial Zone and Batu Kawan Industrial Park. The company is expected to extend its pipeline network further in both areas. This strategic investment in additional capacity and infrastructure was intended to strengthen the company's leading position in Northern Malaysia and its capability to meet market needs.

- Developments like these are expected to boost the growth of the Asia-Pacific booster compressor market in the future.

China is Expected to Dominate the Market

- A high urbanization rate in China has led to an escalation of energy consumption, which has led to a rise in power generation projects and new fuel supply transit systems. Natural gas is one of the most prevalent power generation sources in China.

- According to the BP Statistical Review of World Energy, the country's natural gas-based power generation was around 297.8 TWh in 2023. The government laid down stringent regulations for cleaner power generation sources, spurring numerous gas-based power plant projects for the coming years.

- China is the largest importer of natural gas globally, and as the nation tries to reduce electricity generation through coal-fired power plants, the demand for natural gas is increasing to meet the energy requirements. For example, in October 2023, GE Vernova's Gas Power business and Harbin Electric announced that the SDIC (State Development & Investment Corp. Ltd) Jineng (Zhoushan) Gas Power Generation Co. Ltd ordered two GE 9HA.02 gas turbines for a new combined cycle power plant in the Zhoushan archipelago in Zhejiang Province, China.

- China is the largest crude oil and natural gas producer in the Asia-Pacific region; it accounted for around 57.6% and 33.8% of the total production of crude oil and natural gas, respectively, in the region in 2023. In 2023, 4198 thousand barrels per day of crude oil were produced, an increase of 2.1% over the previous year and an increase of 7.6% over 2020.

- As of January 2023, nearly 17,800 kilometers of gas pipelines were under construction in China, worth around USD 21.9 billion, and 14,300 km in India, worth around USD 20.7 billion, a distance circling over three-quarters of Earth.

- The booster compressor market is also driven by the country's new gas transmission pipeline plans to meet the growing natural gas demand in China. In October 2022, the Chinese National Development and Reform Commission (NDRC) approved the construction of a 20 billion cubic feet/year natural gas pipeline connecting gas fields in Sichuan province (southwestern China) to Hubei province (central China). Construction was expected to begin in December 2022, and the project is expected to be completed by the end of 2024. The project was developed by PipeChina's Southwest Pipeline Company.

- Such developments are likely to lead to the growth of the Chinese market for booster compressors in the future.

Asia-Pacific Booster Compressor Industry Overview

The Asia-Pacific booster compressor market is fragmented. Some of the key players in the market include IDEX India Private Ltd, Hitachi Ltd, Bauer Kompressoren, Mikuni Kikai Kogyo Co. Ltd, and Atlas Copco Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Growth in Industrial Projects

- 4.5.1.2 Escalating Natural Gas Demand for Various Applications

- 4.5.2 Restraints

- 4.5.2.1 High Installation Costs

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Cooling Type

- 5.1.1 Air-cooled

- 5.1.2 Water-cooled

- 5.2 End User

- 5.2.1 Oil and Gas

- 5.2.2 Chemical

- 5.2.3 Power Generation

- 5.2.4 Other End Users

- 5.3 Geography

- 5.3.1 China

- 5.3.2 India

- 5.3.3 Indonesia

- 5.3.4 Malaysia

- 5.3.5 Thailand

- 5.3.6 Vietnam

- 5.3.7 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 IDEX India Private Ltd

- 6.3.2 Hitachi Ltd

- 6.3.3 Bauer Kompressoren

- 6.3.4 Mikuni Kikai Kogyo Co. Ltd

- 6.3.5 Atlas Copco Ltd

- 6.3.6 Haskel International, Inc.

- 6.3.7 Kirloskar Pneumatic Co. Ltd

- 6.3.8 General Electric Company

- 6.3.9 Ingersoll-Rand PLC

- 6.3.10 Aircomp Enterprise

- 6.4 Market Ranking Analysis

- 6.5 List of Other Prominent Companies

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Transition from coal to gas power stations

- 7.2 Rise in the use of gas in motor vehicles

02-2729-4219

+886-2-2729-4219

增壓壓縮機市場:依冷氣類型、壓縮階段、最終用戶、地區

增壓壓縮機市場:依冷氣類型、壓縮階段、最終用戶、地區 增壓壓縮機市場規模、佔有率和成長分析(按製冷類型、壓縮級、壓力等級、應用和地區)- 產業預測 2025-2032

增壓壓縮機市場規模、佔有率和成長分析(按製冷類型、壓縮級、壓力等級、應用和地區)- 產業預測 2025-2032 中東和非洲增壓壓縮機 -市場佔有率分析、行業趨勢、統計數據、成長預測(2025-2030 年)

中東和非洲增壓壓縮機 -市場佔有率分析、行業趨勢、統計數據、成長預測(2025-2030 年) 高壓增壓器的全球市場:產業分析,規模,佔有率,成長,趨勢,預測(2024年~2031年)

高壓增壓器的全球市場:產業分析,規模,佔有率,成長,趨勢,預測(2024年~2031年) 增壓壓縮機市場:按冷卻類型、壓縮級和最終用戶分類 - 2025-2030 年全球預測

增壓壓縮機市場:按冷卻類型、壓縮級和最終用戶分類 - 2025-2030 年全球預測 增壓壓縮機市場,按冷卻類型、壓縮級、壓力、最終用戶、國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測

增壓壓縮機市場,按冷卻類型、壓縮級、壓力、最終用戶、國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測 2024-2032 年按冷卻類型、壓縮級、電源、最終用戶和地區分類的增壓壓縮機市場報告

2024-2032 年按冷卻類型、壓縮級、電源、最終用戶和地區分類的增壓壓縮機市場報告 全球增壓壓縮機市場:趨勢、預測、競爭分析(~2030 年)

全球增壓壓縮機市場:趨勢、預測、競爭分析(~2030 年)![氣動增壓系統市場:趨勢、機會與競爭分析 [2023-2028]](/sample/img/cover/42/1341965.png) 氣動增壓系統市場:趨勢、機會與競爭分析 [2023-2028]

氣動增壓系統市場:趨勢、機會與競爭分析 [2023-2028]