|

市場調查報告書

商品編碼

1645125

巨量資料即服務 (BDaaS):市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Big Data As A Service - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

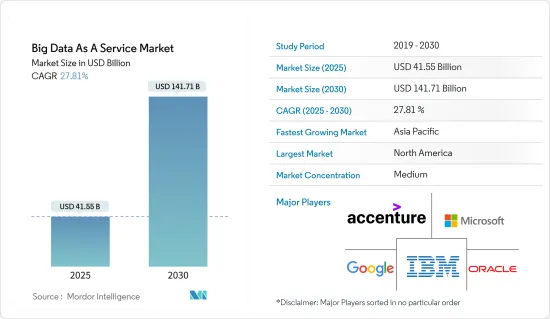

巨量資料即服務 (BDaaS) 市場規模預計在 2025 年為 415.5 億美元,預計到 2030 年將達到 1417.1 億美元,預測期內(2025-2030 年)的複合年成長率為 27.81%。

技術的進步導致了基於服務的解決方案的興起,從而產生了 SaaS(軟體即服務)、PaaS(平台即服務)和 DaaS(數據即服務)。巨量資料供應商將這些服務視為潛在的成長機會,因為它們可以帶來許多好處。隨著企業擴大採用資料主導的行銷策略、行動和混合環境以及全球交付網路,雲端處理變得無所不在。

主要亮點

- 雲端處理不斷發展,為各種規模和行業的企業提供了購買、使用和受益於雲端投資的新方式。在政府的支持下,開放資料技術正變得越來越普及,阿根廷的布宜諾斯艾利斯、秘魯的拉利伯塔德和巴西的聖保羅等城市都對提高政府透明度等措施表示歡迎。

- 阿布雷拉坦、美洲開發銀行 (IADB) 和拉丁美洲開放資料計劃 (ODI) 等組織正在共同合作,擴大整個拉丁美洲的開放資料努力,幫助減少腐敗、增強城市復原力、減少對婦女的暴力行為並改善醫療服務。

- 資料分析在企業中發揮著至關重要的作用,幫助他們組織、儲存和簡化龐大的資料集,幫助他們即時處理大量資料並提高決策能力。此外,巨量資料和商業分析的一個關鍵目標是幫助組織更了解目標受眾和客戶,從而加強本地行銷宣傳活動。

- 網路普及率的提高和技術的進步正在推動拉丁美洲巨量資料市場的蓬勃發展。透過社群網路所能產生的資料量正在迅速擴大,並且呈指數級成長。然而,由於缺乏對投資回報率的認可以及傳統公司面臨的營運挑戰,市場面臨限制。

- 此外,最近爆發的新冠疫情凸顯了不確定性對決策流程和市場的不利影響。目前的疫情後復甦為這段過渡時期提供了巨大機會。隨著市場參與企業及時收到有關情況的資訊,能源市場開始緩和。

BDaaS(巨量資料即服務)市場趨勢

私有雲端的普及推動了市場

- 私有雲端服務專為滿足組織需求而設計,通常透過私有網路或企業廣域網路而不是開放網際網路來源存取。這些服務使企業能夠建立指定安全性和服務等級協定要求的 IT 架構,實現雲端託管和內部部署應用程式之間的無縫整合。

- 透過私有雲端,基礎設施和服務都透過私有網路進行管理,並且軟體和硬體專用於客戶的組織。這可以確保資料不會放錯或遺失,並允許根據需求靈活地更改資源配置。

- 存取私有雲端環境更加安全,因為存取是透過受保護的私有網路線路而不是公共網際網路進行的。此外,私有雲端提供固定定價模式(而非計量收費) ,使企業能夠長期更有效地規劃成長與預算。

- 這些優勢對於工作量可預測、需要專業客製化、在受監管行業營運且必須遵守管治和安全標準的企業尤其有吸引力。金融和政府等行業更有可能採用私有雲端解決方案,因為專用基礎架構讓您完全控制資料和應用程式。

美國佔有最大的市場佔有率

- 在預測期內,美國將主導區域和全球巨量資料即服務 (BDaaS) 市場。這主要是因為市場上大多數主要供應商都位於美國,而且離散製造、銀行、流程製造、專業服務以及聯邦/中央政府等區域產業擴大採用巨量資料服務。

- 巨量資料最近在美國逐漸受到關注,但許多行業的許多公司尚未充分理解巨量資料。然而,採用巨量資料服務來提高內部效率的趨勢日益成長。事實上,最近的一項調查顯示,43% 的公司將簡化內部流程列為數位轉型的主要驅動力。

- 跨國公司英特爾就是美國公司中看到巨量資料巨大價值的著名例子。該公司利用巨量資料來加速晶片開發、識別製造缺陷並警告安全威脅。透過採用巨量資料,英特爾能夠使用預測分析來提高質量,同時節省約 3000 萬美元的品質保證成本。

- 預計製造業的成長速度也將快於整體經濟。根據製造商生產力和創新聯盟 (MAPI) 的數據,到 2022 年,產量預計將成長約 3.5%。此外,預計在預測期內,當地中小企業對 SaaS 的採用將不斷增加,從而擴大研究市場的範圍。

巨量資料即服務 (BDaaS) 產業概覽

巨量資料即服務 (BDaaS) 有可能透過提供差異化和附加價值服務的新機會來顛覆競爭。然而,開放原始碼工具的出現極大地擴展了巨量資料分析技術的功能,使得主要企業很難在不降低產品性能的情況下跟上競爭對手的步伐。這樣的環境可能會提高成本並降低產業盈利。為了保持競爭力,領先的巨量資料解決方案供應商正在收購新興企業並投資新技術來支援他們的整體產品。此外,由於技術進步為公司提供了永續的競爭優勢,市場正在見證多個聯盟和合併。

2023 年 5 月,IBM 宣布收購 Polar Security,並透露計劃將 Polar Security 的 DSPM 技術整合到其旗艦 Guardium 系列資料安全產品中。透過整合 Polar Security 的 DSPM 技術,IBM Security Guardium 現在可以為安全團隊提供一個資料安全平台,該平台涵蓋任何儲存(包括 SaaS、本地和公有雲端基礎架構)上的任何類型資料。

2022 年 11 月,Wipro 推出了 Wipro 資料 Intelligence Suite,這是一站式服務,旨在加速雲端現代化和資料收益。該套件旨在升級在 Amazon Web Services (AWS) 上運作的資料資產,其中包括資料儲存、管道、視覺化等。

2022 年 8 月,混合資料新興企業Cloudera 宣布發布 Cloudera Data Platform (CDP) One。 CDP One 是一款軟體即服務 (SaaS) 產品,可為任何類型的資料提供快速、簡單的自助分析和探索性資料科學。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 調查結果

- 調查前提

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 市場概況

- 市場促進因素與限制因素簡介

- 市場促進因素

- 增加雲端採用和資料生成

- 對內部效率的要求越來越高

- 私有雲端採用率不斷成長

- 市場限制

- 資料安全問題

- 價值鏈/供應鏈分析

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 購買者/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭強度

第5章 市場區隔

- 按部署

- 本地

- 雲

- 私人的

- 民眾

- 混合

- 按最終用戶

- 資訊科技/通訊

- 能源和電力

- BFSI

- 衛生保健

- 零售

- 製造業

- 其他最終用戶

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太地區

- 拉丁美洲

- 巴西

- 墨西哥

- 其他拉丁美洲國家

- 中東和非洲

- 北美洲

第6章 競爭格局

- 公司簡介

- IBM Corporation

- Microsoft Corporation

- Oracle Corporation

- SAP SE

- Hewlett-Packard Company

- SAS Institute Inc.

- Accenture PLC

- Information Builders Inc.

- Google LLC

- Amazon Web Services Inc.

- Alteryx Ltd

- Wipro Ltd

- Opera Solutions LLC

- Guavus Inc.

第7章 市場投資

第8章 市場機會與未來趨勢

The Big Data As A Service Market size is estimated at USD 41.55 billion in 2025, and is expected to reach USD 141.71 billion by 2030, at a CAGR of 27.81% during the forecast period (2025-2030).

Advancements in technology have led to the rise of service-based solutions, which have given birth to Software as a Service (SaaS), Platform as a Service (PaaS), and Data as a Service (DaaS). Big data vendors have identified these as potential growth opportunities due to the benefits these services offer. As businesses increasingly adopt data-driven marketing strategies, mobile and hybrid working environments, and worldwide supply networks, cloud computing is becoming more ubiquitous.

Key Highlights

- Cloud computing continues to evolve, providing businesses of all sizes and industries with new ways to purchase, utilize, and benefit from their cloud investments. With the support of governments, open data technology is gaining traction, and cities like Buenos Aires in Argentina, La Libertad in Peru, and Sao Paolo in Brazil are welcoming initiatives such as government transparency.

- Organizations such as Abrelatam, the Inter-American Development Bank (IADB), and Latin America Open Data Initiative (ODI) are working together to scale open data initiatives across Latin America, helping to reduce corruption, increase the resilience of cities, decrease violence against women, and improve the delivery of healthcare services.

- Data Analytics plays a key role in the enterprise, enabling them to deal with large amounts of data within real time and improve their decision making capabilities by allowing them to organise, store, and simplify vast datasets. Additionally, a key goal of big data and business analytics is to assist organizations in strengthening their regional marketing campaigns by assisting them in better understanding their target audiences and customers.

- Increasing Internet penetration has expanded, and increasing technological progress has led to Latin America's booming market for big data. The rapid expansion and exponential increase in the amount of data that can be generated through social networks. However, the market faces restraints through the Relative lack of Awareness of ROI and operational challenges for Legacy Enterprises.

- In addition, the adverse impact of uncertainty on decision making processes and markets has recently become evident from an outbreak of a COVID-19 pandemic. There are significant opportunities in the current post-pandemic recovery in this transition. Energy markets had started to ease up when the market participants received timely information about the situation.

Big Data as a Service Market Trends

Growing Adoption of Private Cloud is Driving the Market

- Private cloud services are specifically designed to cater to an organization's needs and are generally accessed through a private network or corporate WAN rather than an open Internet source. These services allow organizations to establish their IT architectures by specifying their requirements for security and service-level agreements and enable seamless integration between cloud-hosted applications and in-house applications.

- In a private cloud, both infrastructure and services are maintained on a private network, and software and hardware are exclusively dedicated to the client organization. This ensures that data is not misplaced or lost and provides the flexibility to modify resource configuration in response to demand.

- Because a private cloud environment is accessed using private and protected network lines rather than the public internet, cloud access is more secure. Furthermore, private clouds offer a set pricing model, as opposed to a pay-as-you-go method, enabling organizations to plan expansion and budget more efficiently in the long run.

- These advantages are particularly appealing to enterprises that can predict their workloads, require specialized customization, operate in regulated sectors, and must comply with governance and security standards. Since the dedicated infrastructure provides complete control over data and applications, industries such as finance and government are more likely to adopt a private cloud solution.

United States Occupied the Largest Share In the Market

- The United States is poised to dominate the regional and global big data as a service market over the forecast period. This is largely because most major vendors in the market are based in the United States, and the adoption of big data services is widespread in regional sectors such as discrete manufacturing, banking, process manufacturing, professional services, and federal/central government.

- Although big data has recently gained attention in the US, it is still not fully understood by many businesses across different sectors. However, there is a growing trend in adopting big data services to enhance internal efficiency. In fact, 43% of companies in a recent survey identified internal process efficiency as the primary driving force behind their digital transformation.

- One notable example of a US-based company that has found significant value in big data is Intel, a multinational corporation. The company uses big data to speed up chip development, identify manufacturing glitches, and warn about security threats. By adopting big data, Intel has enabled predictive analysis and saved approximately USD 30 million on its quality assurance spend, while still improving quality.

- The manufacturing sector is also expected to grow faster than the general economy. According to the Manufacturers Alliance for Productivity and Innovation (MAPI), production is projected to increase by around 3.5% until 2022. Additionally, the rising adoption of SaaS among local SMEs is anticipated to expand the studied market scope over the forecast period.

Big Data as a Service Industry Overview

Big data services have the potential to disrupt competition by providing new opportunities for differentiation and value-added services and semi-conslidated. However, the availability of open-source tools has led to a significant expansion of capabilities in Big Data analytics technology, making it challenging for companies to keep up with rivals without giving away too much product performance. This environment can escalate costs and erode industry profitability. To stay competitive, major Big Data solution providers are acquiring or investing in startups and new technologies that support their overall product offerings. The market is also witnessing multiple partnerships and mergers as technological advancements bring sustainable competitive advantages to companies.

In May 2023, IBM has announced it has acquired Polar Security, and plans to integrate Polar Security's DSPM technology within its Guardium family of leading data security products. With the integration of Polar Security's DSPM technology, IBM Security Guardium will provide security teams with a data security platform that covers all types of data across all storage locations, SaaS, on premises and in public cloud infrastructure.

In November 2022, Wipro Ltd. launched the Wipro Data Intelligence Suite, a one-stop shop for accelerating cloud modernization and data monetization. The suite is designed to upgrade data estates, including data stores, pipelines, and visualizations, that run on Amazon Web Services (AWS).

In August 2022, Cloudera, a hybrid data startup, announced the release of Cloudera Data Platform (CDP) One. CDP One is a software-as-a-service (SaaS) product that provides quick and simple self-service analytics and exploratory data science on any type of data.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Introduction to Market Drivers and Restraints

- 4.3 Market Drivers

- 4.3.1 Increasing Cloud Adoption And Rise In The Data Volume Generated

- 4.3.2 Increasing Demand For Improving Organization's Internal Efficiency

- 4.3.3 Growing Adoption of Private Cloud

- 4.4 Market Restraints

- 4.4.1 Data Security Concerns

- 4.5 Value Chain / Supply Chain Analysis

- 4.6 Industry Attractiveness - Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Deployment

- 5.1.1 On-premise

- 5.1.2 Cloud

- 5.1.2.1 Private

- 5.1.2.2 Public

- 5.1.2.3 Hybrid

- 5.2 By End User

- 5.2.1 IT and Telecommunication

- 5.2.2 Energy and Power

- 5.2.3 BFSI

- 5.2.4 Healthcare

- 5.2.5 Retail

- 5.2.6 Manufacturing

- 5.2.7 Other End Users

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Rest of Europe

- 5.3.3 Asia Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Mexico

- 5.3.4.3 Rest of Latin America

- 5.3.5 Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 IBM Corporation

- 6.1.2 Microsoft Corporation

- 6.1.3 Oracle Corporation

- 6.1.4 SAP SE

- 6.1.5 Hewlett-Packard Company

- 6.1.6 SAS Institute Inc.

- 6.1.7 Accenture PLC

- 6.1.8 Information Builders Inc.

- 6.1.9 Google LLC

- 6.1.10 Amazon Web Services Inc.

- 6.1.11 Alteryx Ltd

- 6.1.12 Wipro Ltd

- 6.1.13 Opera Solutions LLC

- 6.1.14 Guavus Inc.

7 MARKET INVESTMENT

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

2025 年至 2033 年巨量資料即服務市場報告,依解決方案(Hadoop 即服務、資料即服務、資料分析即服務)、部署模型、平台類型、組織規模、垂直產業和地區分類

2025 年至 2033 年巨量資料即服務市場報告,依解決方案(Hadoop 即服務、資料即服務、資料分析即服務)、部署模型、平台類型、組織規模、垂直產業和地區分類 巨量資料即服務市場:按解決方案類型、組織規模、部署模型和產業 - 2025-2030 年全球預測

巨量資料即服務市場:按解決方案類型、組織規模、部署模型和產業 - 2025-2030 年全球預測 全球 BDaaS(巨量資料即服務)市場規模、佔有率和趨勢分析:按部署、按解決方案、按公司規模、按最終用途、按地區、前景和預測,2024-2031 年

全球 BDaaS(巨量資料即服務)市場規模、佔有率和趨勢分析:按部署、按解決方案、按公司規模、按最終用途、按地區、前景和預測,2024-2031 年 全球大數據即服務 (BDaaS) 市場規模按服務類型、最終用戶、部署模式、地區、範圍和預測劃分

全球大數據即服務 (BDaaS) 市場規模按服務類型、最終用戶、部署模式、地區、範圍和預測劃分 到 2030 年 BDaaS(巨量資料即服務)市場預測:按解決方案類型、部署模型、組織規模、最終用戶和區域進行的全球分析

到 2030 年 BDaaS(巨量資料即服務)市場預測:按解決方案類型、部署模型、組織規模、最終用戶和區域進行的全球分析 全球 BDaaS(大數據即服務)市場:依產品類型、最終用戶、地區:產業分析、規模、佔有率、成長、趨勢、預測(2024-2032 年)

全球 BDaaS(大數據即服務)市場:依產品類型、最終用戶、地區:產業分析、規模、佔有率、成長、趨勢、預測(2024-2032 年) BDaaS(巨量資料即服務)的全球市場 2024-2028

BDaaS(巨量資料即服務)的全球市場 2024-2028 巨量資料即服務市場 - 全球產業規模、佔有率、趨勢、機會和預測,2018-2028F - 按解決方案類型、按部署模型、按組織規模、按行業垂直、按地區和競爭

巨量資料即服務市場 - 全球產業規模、佔有率、趨勢、機會和預測,2018-2028F - 按解決方案類型、按部署模型、按組織規模、按行業垂直、按地區和競爭 全球巨量資料即服務市場 (BDaaS)

全球巨量資料即服務市場 (BDaaS)