|

市場調查報告書

商品編碼

1645133

資料中心機櫃:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Data Center Rack - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

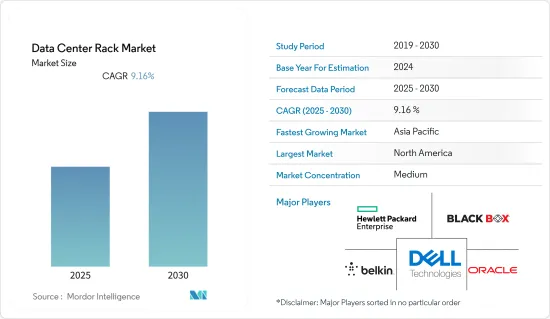

預計預測期內資料中心機櫃市場複合年成長率為 9.16%。

資料中心(無論是私人還是公共)對企業都很重要,因為它們託管關鍵任務應用程式。這些資料中心幫助企業簡化訊息,同時為世界各地的使用者和客戶提供便捷的存取。由於對雲端技術的依賴和支出的增加,資料中心正在經歷成長。

主要亮點

- 資料中心已成為許多企業IT基礎設施的關鍵組成部分。每天都會產生大量的資料,企業依賴資料中心來有效率地處理資料和儲存。因此,全球資料中心的不斷成長的部署是影響資料中心機櫃消費的主要促進因素。此外,大公司對技術服務和投資的需求不斷成長也推動了市場成長的變化。

- 這些資料中心機櫃主要用於資料中心基礎設施管理。這些機架容納資料中心的伺服器、交換器、電纜和其他設備。隨著技術的變化和高密度伺服器的引入,機架基礎設施已成為資料中心的關鍵要素,需要有效地託管伺服器、管理電纜和促進空氣流通,以確保資料中心的最佳效能。

- 最初,人們對資料中心的機架基礎設施關注甚少,部署時只考慮尺寸和成本。然而,高密度應用的採用以及資料中心冷卻和電力的重要性也是影響市場成長的因素。據估計,資料中心消耗的電力中有 39% 用於冷卻。因此,企業正在尋找高效的冷卻系統來降低能源消耗並提高整體效率。

- 此外,推動市場成長的關鍵因素是巨量資料分析和IT基礎設施現代化趨勢。巨量資料分析有助於管理跨多個資料中心處理的複雜且混亂的組織資料。

- 預計預測期內,雲端運算需求和進出資料中心的資料流量的不斷成長將推動全球需求。據思科稱,到 2021 年,雲端資料中心的 IP 流量預計將達到每年 19,509 Exabyte ,而傳統資料中心的 IP 流量為每年 1,046 Exabyte 。

- COVID-19 對整個經濟的業務永續營運產生了負面影響,影響了所有行業各種規模的組織。有效、有效率的服務能夠解決變化和問題並滿足新的需求,已成為資料中心的策略和營運要務。需求激增主要受到兩個因素推動。許多企業和機構普遍轉向在家工作,這推動了對處理能力的需求。數位基礎設施對全球經濟從未如此重要。隨著人們在室內度過的時間越來越多,視訊通話、醫療保健、數位學習、電子商務和休閒應用等數位應用也隨之增加,對資料處理能力的需求也隨之增加。

資料中心機櫃市場趨勢

預計 BFSI 行業將佔主要佔有率

- 雲端運算和資料中心已成為 BFSI 領域的支柱,尤其是在數位化浪潮中。銀行和金融領域日益激烈的競爭以及對線上服務的需求正在推動資料中心市場的發展,並最終推動資料中心機櫃市場的發展。

- 資料中心對於金融服務來說已經變得至關重要。銀行部門使用的機架需要額外的保護,以防止盜竊和損壞等風險。有了機架,銀行服務提供者就擁有了一個平台來託管他們的系統並保護它們免受不可預見的物理風險。這些機架是模組化的,允許銀行服務提供者根據需要進行升級。

- 機架供應商正在開發特定產品以滿足該行業日益成長的需求。近日,NetRack針對銀行和保險業推出了iRack/iRack Block。

- 北美和歐洲等已開發地區擁有強大的 BFSI 影響力,且數位服務的滲透率更高。這主要歸功於這些地區的數位化意識水平較高。除此之外,亞太地區由於擁有龐大的此類服務的消費群,也經歷著強勁的成長。中國和印度等國家正經歷銀行業向雲端服務的明顯轉變。

- 線上付款的興起進一步增加了 BFSI 領域對資料中心的需求。銀行和金融業務將客戶資訊安全地儲存在資料中心(本地和雲端)、交易所和分店中。

- 由於全球冠狀病毒疫情的影響,數位銀行解決方案的採用預計將加速,並進一步採用容器化、雲端處理、微服務、API 和區塊鏈等技術。因此,金融和銀行業預計將為資料中心提供一些成長機會。

北美佔有最大市場佔有率

- 行動寬頻的快速普及、巨量資料分析和雲端運算的興起是推動北美新資料中心基礎設施需求的因素之一。該地區還擁有大量資料中心。許多公司正在從硬體轉向基於軟體的服務,預計這將成為資料中心安裝的迎合市場。此外,根據 Cloud Scene 的數據,美國有超過 2,500 個資料中心,加拿大有超過 250 個資料中心。

- 美國擁有全球最多的資料中心,由於超大規模資料中心的興起,巨量資料和流量正在強勁成長。據思科稱,到2021年終,全球資料中心儲存的巨量資料量預計將達到Exabyte,其中美國預計將佔據很大佔有率。

- 此外,資料中心機櫃供應商在該地區擁有強大的影響力,推動著該地區的市場發展。其中包括 Kendall Howard LLC、Belkin International Inc.、Martin International、HPE、Dell EMC、Black Box Corporation 和 Chatsworth Products。

- 透過提供整合電源、冷卻和IT基礎設施的產品,領先的供應商正在吸引更多的消費者並佔領更大的市場佔有率。該地區的主機託管、網際網路和雲端服務供應商對大型設施計劃的投資不斷增加,推動了對機架和機架選項的需求。

- 此外,美國政府啟動了資料中心最佳化舉措(DCOI),以整合該國許多資料中心,以便在改善納稅人的投資的同時為公民提供更好的服務。這個整合資料資料並關閉表現不佳的資料中心。迄今為止,校方已關閉了北維吉尼亞州超過 3,215 平方英尺的校園空間。

資料中心機櫃產業概況

資料中心機櫃市場細分為中型細分市場。技術的變化和高密度伺服器的採用使得機架基礎設施成為資料中心的關鍵方面。為了確保資料中心的最佳效能,需要有效率地託管伺服器、管理電纜並促進氣流。整體來看,現有競爭對手之間的競爭非常激烈。大型企業的新創新策略正在推動資料中心機櫃市場的發展。

2022 年 2 月,亞馬遜公司 (Amazon.com Inc.) 的子公司 Amazon Web Services Inc. 宣布,AWS 本地區域是一種基礎設施部署,它擴展了 AWS 區域,並將運算、儲存、資料庫和其他 AWS 服務置於人口密集、工業和資訊技術 (IT) 中心附近的雲端邊緣。

2022年1月,瑞典領先的研究機構和創新合作夥伴RISE Research Institutes與全球數位基礎設施和連續性解決方案供應商Vertiv建立了新的夥伴關係。 Vertiv 與 Facebook、愛立信、Vattenfall、ABB、LTU 和諾爾布滕地區等創始合作夥伴一起以白金級別參與資料中心系統技術夥伴關係計畫。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況

- 產業價值鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 購買者和消費者的議價能力

- 新進入者的威脅

- 競爭對手之間的競爭

- 替代品的威脅

- COVID-19 對資料中心機櫃市場的影響評估

第5章 市場動態

- 市場促進因素

- 擴大資料中心設施的採用

- 雲端運算的日益普及推動了對超大規模資料中心的投資

- 預計 BFSI 行業將佔主要佔有率

- 市場限制

- 刀鋒伺服器的使用增加

第6章 市場細分

- 按框架單位

- 袖珍的

- 中等的

- 大的

- 按最終用戶產業

- BFSI

- 資訊科技/通訊

- 製造業

- 零售

- 其他最終用戶產業

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

第7章 競爭格局

- 公司簡介

- Kendall Howard LLC

- Belkin International Inc.

- Martin International Enclosures

- Black Box Corporation

- Rittal GmbH & Co. KG

- Vertiv Group Corporation

- Hewlett Packard Enterprise

- Dell EMC

- Schneider Electric SE

- Fujitsu Corporation

- Oracle Corporation

- Legrand SA

第8章投資分析

第9章:市場的未來

The Data Center Rack Market is expected to register a CAGR of 9.16% during the forecast period.

Whether private or public, data centers are critical to enterprises hosting mission-critical applications. These data centers help organizations streamline information while enabling easy access to users and customers from anywhere worldwide. Data centers have witnessed growth due to the increasing dependence and spending on cloud technologies.

Key Highlights

- Data centers have become a key component in IT infrastructure for many organizations. With large amounts of data being generated daily, companies rely on data centers to efficiently handle data and storage. Therefore, the growing deployment of data centers worldwide is the major driving factor influencing the consumption of data center racks. The increasing demand for technology services and investments from major companies are also changing the market's growth.

- These data center racks are deployed primarily for infrastructure management in the data centers. These racks host servers, switches, cables, and other equipment in the data center. With changing technologies and the adoption of high-density servers, rack infrastructure has become a crucial aspect in data centers, with the need to host servers effectively, manage cables, and facilitate airflow to ensure the optimum performance of data centers.

- Initially, the focus on rack infrastructure in data centers was minimum, with size and cost being the only considerations during deployment. However, the adoption of high-density applications and the importance of cooling and power in the data center also are influential factors in the growth of the market. It is estimated that 39% of the power consumed by the data center is spent on cooling. Thus, companies demand efficient cooling systems to reduce energy consumption and improve overall efficiency.

- Additionally, the key factors driving the market's growth are Big data analytics and the modernization of IT infrastructure trends. Big data analytics aids in the management of complex and jumbled-up organizational data that is processed across multiple data centers.

- The growing cloud demand and data traffic moving from and within the data centers are expected to bolster global demand during the forecast period. Per Cisco, the cloud data center IP traffic is expected to reach 19,509 exabytes annually by 2021, compared to 1,046 exabytes per year of traditional data center traffic.

- COVID-19 negatively influenced business continuity across all economics, affecting organizations of all sizes in every industry. Effective and efficient services that simultaneously accommodate new needs and counteract change and problems have become a strategic and operational necessity for data centers. Two main factors are fueling the tremendous rise in demand. The need for processing power was brought on by the widespread shift of many enterprises and institutions to working from home. Never before had digital infrastructure been more crucial to the global economy. As we all spent more time indoors, the corresponding increase in digital applications for video calling, healthcare, e-learning, and e-commerce, together with those for leisure led to a rise in the demand for data capabilities.

Data Center Rack Market Trends

BFSI Sector Expected to Hold a Significant Share

- Cloud and data centers have become the backbone of the BFSI sector, especially during the digitization movement. The increasing competition and the demand for online services in the banking and financial sectors drive the market for data centers and, by extension, data center racks.

- Data centers have become very crucial for financial services. The racks used in the banking sector require additional protection against theft, damage, and other risks. Racks enable the banking service providers to have a platform that hosts the systems and protects them from unforeseen physical risks. These racks are modular, owing to which the banking service providers can upgrade when required.

- The rack providers are developing particular products for this segment to cater to the increasing demand from this sector. The most recent was by NetRack, which launched iRack/iRack Block to cater to the banking and insurance sectors.

- The strong presence of BFSI in developed regions, like North America and Europe led to increased penetration of digital services. This is primarily owing to the higher degree of awareness related to digitization in these regions. Along with this, Asia-Pacific is also growing substantially due to a huge consumer base for these services. Countries like China and India are witnessing a strong shift toward cloud services in the banking sector.

- The growing scope of online payment further increases the need for data centers in the BFSI sector. Banks and financial institutions securely store customer information in both on-premise and cloud data centers, as well as on the trading floors and in branch operations.

- Due to the global coronavirus disruption, the adoption of digital banking solutions is expected to adopt further technologies like containerization, cloud computing, microservices, APIs, and blockchain. Hence, the financial and banking industry is expected to provide several growth opportunities for data centers.

North America to Hold Maximum Market Share

- The rapid growth of mobile broadband with an increase in big data analytics coupled with cloud computing are some of the factors driving the demand for new data center infrastructures in the North American region. The region also comprises a considerable amount of data centers. Multiple enterprises are switching from hardware to software-based services, and they are anticipated to be an addressable market for data center installations. Moreover, according to the cloud scene, there are more than 2500 data centers in the United States and more than 250 data centers in Canada.

- The United States has the highest number of data centers globally, and it is witnessing robust growth in terms of the volume of big data and traffic due to the increase in the number of hyperscale data centers. According to Cisco, the volume of big data in data center storage globally is expected to reach 403 exabytes by the end of 2021, of which a huge share would likely be attributed to the United States.

- Moreover, the region has a strong foothold of data center racks providers, driving the region's market. Some of them include Kendall Howard LLC, Belkin International Inc., Martin International, HPE, Dell EMC, Black Box Corporation, and Chatsworth Products.

- The leading vendors offer an integrated power, cooling, and IT infrastructure to attract a higher number of consumers and gain a larger market share. The region is likely to witness higher investment in mega facilities projects, contributed heavily by colocation, internet, and cloud service providers, thereby boosting the demand for racks and rack options.

- Moreover, the US government commenced the Data Center Optimization Initiative (DCOI) to deliver better services to the public while increasing the taxpayers' return on investment by consolidating many data centers in the country. The consolidation process includes the process of building hyper-scale data centers and shut-off the underperforming ones. To date, the government has closed over 3,215 sq ft of campus in Northern Virginia.

Data Center Rack Industry Overview

The data center rack market is medium fragmented. With changing technologies and the adoption of high-density servers, rack infrastructure has become an important aspect of data centers, with the need to host servers effectively, manage cables, and facilitate airflow to ensure the optimum performance of data centers. Overall, the competitive rivalry among the existing competitors is high. The new innovative strategies of large companies are driving the data center racks market.

In February 2022, the first 16 AWS Local Zones in the United States have been completed, and 32 new AWS Local Zones will be launched in 26 other countries, according to Amazon Web Services Inc. (AWS), an affiliate of Amazon.com Inc. and this is to enable customers to deploy applications that require single-digit millisecond latency closer to end users or on-premises data centers, AWS Local Zones are a type of infrastructure deployment that extends AWS Regions to place compute, storage, database, and other AWS services at the edge of the cloud near large population, industry, and information technology (IT) centers.

In January 2022, a major Swedish research institute and innovation partner, RISE Research Institutes, and Vertiv, a global provider of digital infrastructure and continuity solutions formed a new partnership. Vertiv is joining founding partners, including Facebook, Ericsson, Vattenfall, ABB, LTU, and the Norrbotten region, by entering the partnership program for data center systems technologies at the platinum level.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHT

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Intensity of Competitive Rivalry

- 4.3.5 Threat of Substitute Products

- 4.4 Assessment of Impact of COVID-19 on the Data Center Racks Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Deployment of Data Center Facilities

- 5.1.2 Growing Cloud Computing Adoption Leading to Investment in Hyperscale Data Centers

- 5.1.3 BFSI Sector Expected to Hold a Significant Share

- 5.2 Market Restraints

- 5.2.1 Increasing Utilization of Blade Servers

6 MARKET SEGMENTATION

- 6.1 By Rack Units

- 6.1.1 Small

- 6.1.2 Medium

- 6.1.3 Large

- 6.2 By End-user Industry

- 6.2.1 BFSI

- 6.2.2 IT and Telecom

- 6.2.3 Manufacturing

- 6.2.4 Retail

- 6.2.5 Other End-user Industries

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Kendall Howard LLC

- 7.1.2 Belkin International Inc.

- 7.1.3 Martin International Enclosures

- 7.1.4 Black Box Corporation

- 7.1.5 Rittal GmbH & Co. KG

- 7.1.6 Vertiv Group Corporation

- 7.1.7 Hewlett Packard Enterprise

- 7.1.8 Dell EMC

- 7.1.9 Schneider Electric SE

- 7.1.10 Fujitsu Corporation

- 7.1.11 Oracle Corporation

- 7.1.12 Legrand SA

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

資料中心機架市場 - 全球產業規模、佔有率、趨勢、機會和預測,按組件、按機架類型、按資料中心規模、按機架高度、按行業垂直、按地區和競爭進行細分,2020-2030F

資料中心機架市場 - 全球產業規模、佔有率、趨勢、機會和預測,按組件、按機架類型、按資料中心規模、按機架高度、按行業垂直、按地區和競爭進行細分,2020-2030F 資料中心機櫃配電單元 (PDU):市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

資料中心機櫃配電單元 (PDU):市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) IT 設備配電單元市場按類型、額定功率、相位、安裝類型和最終用戶產業分類 - 2025 年至 2030 年全球預測2025 年資料中心機架與機櫃全球市場報告資料中心機架配電裝置市場 - 全球產業規模、佔有率、趨勢、機會和預測,按計量和監控、部署模式、電力容量、地區、競爭細分 2020-2030F2025-2033 年資料中心機架市場報告(按類型、機架單元、機架尺寸、框架尺寸、框架設計、服務、應用、最終用戶和地區)

IT 設備配電單元市場按類型、額定功率、相位、安裝類型和最終用戶產業分類 - 2025 年至 2030 年全球預測2025 年資料中心機架與機櫃全球市場報告資料中心機架配電裝置市場 - 全球產業規模、佔有率、趨勢、機會和預測,按計量和監控、部署模式、電力容量、地區、競爭細分 2020-2030F2025-2033 年資料中心機架市場報告(按類型、機架單元、機架尺寸、框架尺寸、框架設計、服務、應用、最終用戶和地區) 資料中心機架和機櫃市場機會、成長促進因素、產業趨勢分析與預測 2025 - 2034 年資料中心機櫃市場:按組件、按服務、按機架類型、按機架高度、按機架寬度、按資料中心大小、按行業 - 2025-2030 年全球預測

資料中心機架和機櫃市場機會、成長促進因素、產業趨勢分析與預測 2025 - 2034 年資料中心機櫃市場:按組件、按服務、按機架類型、按機架高度、按機架寬度、按資料中心大小、按行業 - 2025-2030 年全球預測 資料中心機櫃市場-2024年至2029年預測資料中心機櫃市場規模、佔有率和趨勢分析報告:2024-2030 年按機架、高度、行業、寬度、地區和細分市場進行的預測

資料中心機櫃市場-2024年至2029年預測資料中心機櫃市場規模、佔有率和趨勢分析報告:2024-2030 年按機架、高度、行業、寬度、地區和細分市場進行的預測