|

市場調查報告書

商品編碼

1645164

特種化學品-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Specialty Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

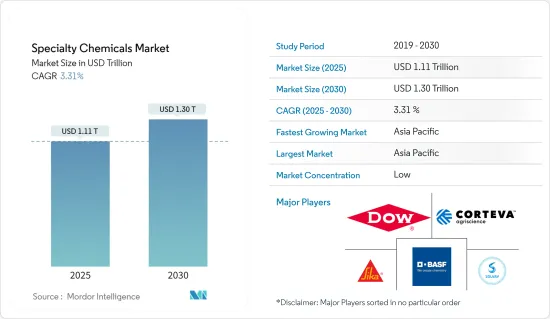

特種化學品市場規模預計在 2025 年為 1.11 兆美元,預計到 2030 年將達到 1.3 兆美元,預測期內(2025-2030 年)的複合年成長率為 3.31%。

2020 年,市場受到了 COVID-19 疫情的負面影響。疫情導致多個國家停擺,造成供應鏈中斷、業務停頓和勞動力短缺。然而,自從限制解除以來,該行業已經恢復良好。住宅銷售量的增加和新計畫的推出推動了對油漆、被覆劑和建築化學品的需求。過去兩年,半導體、積體電路和農業化學品的需求增加帶動市場復甦。

關鍵亮點

- 市場成長的主要動力是建設活動的強勁成長,尤其是在亞太地區、中東和非洲。此外,人口成長正推高全球糧食需求。

- 然而,日益嚴格的環境法規和日益減少的石化燃料蘊藏量正在抑制市場的成長。

- 預計在預測期內,新產品研發的發展將為市場研究提供機會。

- 亞太地區憑藉龐大的基本客群、不斷成長的工業產量以及建築業的強勁成長而佔據全球市場的主導地位,從而對特種化學品的需求很高。

特種化學品市場趨勢

農業化學品領域主導市場需求

- 在專用化學品市場中,農業化學品佔據主導地位。這一部分的成長主要受到人均可耕地面積減少和全球糧食需求增加的推動。

- 世界人口正在迅速成長。人口成長刺激了對食物的需求。養活不斷增加的人口正成為一項威脅。同時,由於工業化、都市化的發展,可耕地面積不斷減少。人們長期以來一直使用肥料來提高作物產量,因此在預測期內對農藥的需求將會增加。

- 隨著人均收入的提高和人口的成長,全球對作物和經濟作物的需求預計會增加。例如,根據糧農組織的數據,到2050年,美國的糧食需求預計將增加50-90%。

- 聯合國糧食及農業組織(FAO)和國際糧食政策研究所(IFPRI)預測,2050年全球糧食需求將會增加。根據糧農組織的預測,到2050年全球糧食需求可能增加70%,其中全球糧食需求預計大部分成長將來自亞太地區、東歐和拉丁美洲消費者收入的成長。

- 此外,由於人們對植物有效吸收養分的關注度日益提高,以及對監管健康和環境問題的日益關注,微量營養素肥料、生物基肥料和特種肥料(如液體肥料)越來越受歡迎。

- 生物除草劑利用微生物作為生物害蟲防治劑,與合成除草劑一起在綜合害蟲管理技術中也越來越受歡迎。儘管這一領域僅佔行業一小部分,但預計它將經歷顯著的成長。

- 2021年各國肥料出口總額總合約832億美元。這一金額反映出,2020 年所有化肥出口商的平均增幅為 50.7%,當年化肥出口總額為 552 億美元5。

- 2021年俄羅斯出口額為124億美元,較2020年(69.9億美元)成長約78%。此外,中國出口大幅成長近74.6%。 2021年中國化肥出口總額為114.7億美元。

- 此外,農業用地減少和病蟲害造成的作物損失也是推動農藥市場發展的主要因素。

- 因此,預計所有這些有利趨勢將在預測期內推動農業化學品市場的需求。預計這將推動對特種化學品的需求。

亞太地區佔市場主導地位

- 亞太地區主導特種化學品市場。由於建築業的強勁成長、化妝品需求的增加、電氣和電子行業的投資和生產的增加、包裝行業對粘合劑和塑膠的需求的增加以及該地區工業對水處理系統的安裝增加,預計該行業在預測期內仍將保持其地位。

- 該地區人口不斷成長,特別是中國和印度等國家,導致糧食需求增加。預計這將推動農業化學品市場的發展,進而促進預測期內專門食品聚合物市場的成長。

- 亞太地區建築業的成長主要由於服務業擴張導致的辦公空間需求上升、住宅建築計劃增加以及跨國公司流入該地區建設工業基礎的投資。預計這些因素將在預測期內推動該地區對油漆和被覆劑、黏合劑和密封劑、建築化學品和特殊聚合物的需求。

- 根據中國國家統計局數據,2021年中國建築業企增加價值額81380億元(約11516.1億美元) ,年增2.15%。

- 預計未來七年印度的住宅投資也將達到約 1.3 兆美元。預計該國將建造 6,000 萬套新住宅。預計到 2025 年,印度經濟適用住宅數量將增加 70% 左右。此外,印度政府「2022年實現全民住宅」的目標對該行業來說也是一個重大變化。

- 黏合劑已成為汽車應用中的關鍵技術部件,並不斷取代傳統的黏合和黏附方法。該地區的黏合劑和密封劑產量正在增加,從而導致對化妝品化學品的需求增加。

- 根據日本汽車工業協會(JAMA)的數據,2021年日本生產了7,846,955輛乘用車和輕型車。

- 黏合劑在電子工業中有多種用途,包括三防膠、端子電極保護和表面黏著型元件的黏合。電子業是印度成長最快的行業之一。據電子和資訊技術部稱,2021年該行業的市場規模預計在4.95兆盧比至5.0兆盧比之間(約合669.5億至676.2億美元)。

- 因此,預計所有這些有利趨勢將在預測期內推動該地區特種化學品市場的成長。

特種化學品產業概況

特種化學品市場高度細分,眾多參與企業佔據了相當大的市場佔有率。市場的主要參與企業(不分先後順序)包括BASF SE、Dow、Corteva、Sika AG 和 Solvay。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 驅動程式

- 亞太地區、中東和非洲建設活動強勁成長

- 人口成長推動全球糧食需求

- 波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

- 原料分析

第 5 章 市場區隔(以金額為準的市場規模)

- 油漆和塗料

- 動態

- 應用

- 建築學

- 車

- 工業的

- 木頭

- 其他

- 催化劑

- 動態

- 催化功能

- 化學合成催化劑

- 精製催化劑

- 聚合催化劑

- 建築化學品

- 動態

- 應用

- 商務用

- 工業的

- 基礎設施

- 住宅

- 公共空間

- 化妝品

- 動態

- 應用

- 頭髮護理

- 護膚

- 口腔護理

- 個人衛生

- 其他

- 染料、油墨、顏料

- 動態

- 類型

- 墨水

- 染料

- 有機顏料

- 無機顏料

- 電子化學品

- 動態

- 應用

- 半導體和積體電路

- 印刷基板

- 水處理化學品

- 動態

- 功能

- 凝聚劑

- 凝聚劑

- 除生物劑和殺菌劑

- 消泡劑和消泡劑

- pH 調節劑和軟化劑

- 其他

- 食品添加物

- 動態

- 類型

- 天然添加物

- 合成添加劑

- 農藥

- 動態

- 類型

- 肥料

- 除草劑

- 殺菌劑

- 殺蟲劑

- 殺線蟲劑

- 滅螺劑

- 其他作物保護化學品

- 工業和公共設施清潔工

- 動態

- 應用

- 一般清潔劑

- 殺菌劑和消毒劑

- 衣物洗護產品

- 洗車用品

- 潤滑油添加劑

- 動態

- 產品類型

- 分散劑和乳化劑

- 清洗劑

- 抗氧化劑

- 極壓抗磨添加劑

- 黏度指數改進劑

- 摩擦改進劑

- 腐蝕抑制劑

- 其他

- 礦業化學品

- 動態

- 功能

- 浮選化學品

- 萃取化學品

- 研磨助劑

- 油田化學品

- 動態

- 應用

- 除生物劑

- 腐蝕和水垢抑制劑

- 去乳化劑

- 聚合物

- 界面活性劑

- 其他化學品

- 黏合劑和密封劑

- 動態

- 科技

- 水性膠黏劑

- 溶劑型膠黏劑

- 熱熔膠

- 反應性黏合劑

- 其他膠黏劑

- 密封劑

- 塑膠添加劑

- 動態

- 塑膠類型

- 聚乙烯 (PE)

- 聚苯乙烯(PS)

- 聚丙烯(PP)

- 聚醯胺(PA)

- 聚對苯二甲酸乙二醇酯(PET)

- 聚氯乙烯(PVC)

- 聚碳酸酯(PC)

- 其他塑膠

- 橡膠加工化學品

- 動態

- 應用

- 胎

- 無輪胎

- 特種聚合物

- 動態

- 紡織化學品

- 動態

- 應用

- 塗料和施膠化學品

- 著色劑和助劑

- 整理加工劑

- 退漿劑

- 其他

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 北美其他地區

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 西班牙

- 歐洲其他地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭格局

- 併購、合資、合作與協議

- 市場佔有率分析

- 黏合劑和密封劑

- 農藥

- 建築化學品

- 潤滑油和石油添加劑

- 礦業化學品

- 油田化學品

- 油漆和被覆劑

- 特種聚合物

- 水處理化學品

- 主要企業策略

- 公司簡介

- 3M

- AECI

- Afton Chemical

- Akzo Nobel NV

- Albemarle Corporation

- ALTANA

- Archroma

- Arkema Group

- Ashland

- Asian Paints

- Axalta Coating Systems

- Baker Hughes Company

- BASF SE

- Berger Paints India Limited

- Buckman

- Chevron Corporation

- Clariant

- Corteva

- Covestro AG

- DIC Corporation

- Dow

- DSM

- DuPont

- Eastman Chemical Company

- Ecolab

- Evonik Industries AG

- Exxon Mobil Corporation

- Ferro Corporation

- Flint Group

- FMC Corporation

- GCP Applied Technologies Inc.

- HB Fuller Company

- Halliburton

- Henkel AG & Co. KGaA

- Hexcel Corporation

- Huntsman International LLC

- Infineum International Limited

- Kemira

- KRONOS Worldwide Inc.

- Kurita Water Industries Ltd

- Holcim

- LANXESS

- Lonza

- MAPEI SpA

- Merck KGaA

- NIPSEA GROUP

- Nouryon

- Nutrien Ltd

- Pidilite Industries Ltd

- PPG Industries Inc.

- Procter & Gamble

- RPM International Inc.

- SABIC

- Schlumberger Limited

- Sika AG

- Solenis

- Solvay

- Syngenta

- The Chemours Company

- The Lubrizol Corporation

- The Sherwin-Williams Company

- Venator Materials PLC

- Veolia

- WR Grace & Co.

- Wacker Chemie AG

- Yara

第7章 市場機會與未來趨勢

The Specialty Chemicals Market size is estimated at USD 1.11 trillion in 2025, and is expected to reach USD 1.30 trillion by 2030, at a CAGR of 3.31% during the forecast period (2025-2030).

The market was negatively impacted by the COVID-19 outbreak in 2020. Owing to the pandemic scenario, several countries went into lockdown, which led to supply chain disruptions, work stoppages, and labor shortages. However, the sector is recovering well since restrictions were lifted. An increase in house sales and new project launches have led to a rise in the demand for paints, coatings, and construction chemicals. The increasing demand for semiconductors, integrated circuits, and agrochemicals led to the market recovery over the last two years.

Key Highlights

- The major factors driving the market's growth are the robust growth of construction activities, especially in Asia-Pacific and the Middle East & Africa. Furthermore, the growing population is propelling the demand for food worldwide.

- On the flip side, increasing environmental regulations and decreasing fossil fuel reserves are the restraints hampering the market's growth.

- Growing research and development for creating novel products will likely provide an opportunity for the market studied over the forecast period.

- Asia-Pacific dominated the global market, owing to the vast customer base, leading to high demand for specialty chemicals, increasing industrial production, and robust growth of the construction sector in the region.

Speciality Chemicals Market Trends

Agrochemicals Segment to Dominate the Market Demand

- The agrochemicals segment dominated the share in the specialty chemicals market. The segment's growth is extensively driven by the decreasing per capita arable land and increasing demand for food worldwide.

- The global population is increasing rapidly. This growing population is adding to the food demand. Supplying food to this ever-increasing population is becoming a threat. On the other hand, arable land is declining due to industrialization and urbanization. Fertilizers have been used for a long time to increase crop productivity, thus, enhancing agrochemicals demand over the forecast period.

- With the increasing per capita income and growing population, food and cash crops demand is estimated to increase globally. For instance, as per the FAO, the food demand in the United States is expected to increase by 50-90% by 2050.

- The Food and Agriculture Organization of the United Nations (FAO) and the International Food Policy Research Institute (IFPRI) have published projections of an increase in global food demand by 2050. The FAO projections indicate that world food demand may increase by 70% by 2050, with much of the projected increase in global food demand expected to come from rising consumer incomes in Asia-Pacific, Eastern Europe, and Latin America.

- Furthermore, owing to the growing concerns about nutrient efficiency uptake by plants and the growing regulatory health and environmental concerns, micronutrient fertilizers, bio-based fertilizers, and specialty fertilizers (like liquid fertilizers) are gaining popularity.

- Bio-herbicides that use microbes as biological weed control agents are also gaining popularity in integrated pest management techniques, along with synthetic herbicides. Although the segment constitutes only a tiny part of the industry, it is expected to grow significantly.

- Fertilizers exported by all countries totaled around USD 83.2 billion in 2021. That dollar amount reflects an average 50.7%5 increase for all shippers of fertilizers in 2020 when overall fertilizer exports were worth USD 55.2 billion.

- Russia exported USD 12.4 billion in 2021, an increase of around 78% compared to 2020 (USD 6.99 billion), with India being one of the largest importers from the Federation. Additionally, China experienced a significant increase in exports of almost 74.6%. Fertilizer exports from China totaled 11.47 billion USD in 2021.

- Moreover, contracting agricultural land and losing crops owing to pests and diseases are the significant factors driving the insecticide market.

- Hence, all such favorable trends are expected to drive the demand for the agrochemicals market during the forecast period. It is expected to drive the need for specialty chemicals.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region dominated the specialty chemicals market. It is likely to retain its position during the forecast period due to robust growth of the construction sector, increasing cosmetic products demand, growing investment and production in the increasing electrical and electronics industry output, increasing demand for adhesives and plastics from the packaging industry, and increasing installations of water treatment systems from the industries in the region.

- The growing population in the region, especially in countries such as China and India, is increasing the demand for food. It is expected to drive the agrochemical market and consequently help the specialty polymers market grow over the forecast period.

- The growth of the Asia-Pacific construction sector is majorly driven by the service sector expansion, leading to an increase in the demand for office spaces, an increase in residential construction projects, and an inflow of investments from multinational companies to set up an industrial base in the region. Such factors will likely increase the demand for paints and coatings, adhesives and sealants, construction chemicals, and specialty polymers in the area during the forecast period.

- According to the National Bureau of Statistics of China, in 2021, the value added of construction enterprises in China was CNY 8,013.8 billion (~USD 1151.61 billion), up by 2.15% over the previous year.

- India will also likely witness an investment of around USD 1.3 trillion in housing over the next seven years. The country is expected to see the construction of 60 million new homes. The availability of affordable housing is likely to rise by around 70% by 2025 in India. Besides, the Indian government's 'Housing for All by 2022' is also a significant game-changer for the industry.

- Adhesives have become a prime technology component in automotive applications, continuously replacing traditional bonding or adhesion methods. It is increasing adhesives and sealants production in the region, leading to a rise in demand for cosmetic chemicals.

- According to Japan Automobile Manufacturers Association (JAMA), the country produced 7,846,955 units of passenger cars and light vehicles in 2021.

- The electronics industry uses adhesives for various applications, including conformal coatings, protecting terminal electrodes, and bonding of surface mount devices, among many others. The electronics industry is one of the fastest-growing industries in India. According to the Ministry of Electronics and IT, the industry's market size is INR 4,950-5,000 billion (~ USD 66.95-67.62 billion) as of fiscal 2021.

- Hence, all such favorable trends are collectively likely to drive the growth of the specialty chemicals market in the region during the forecast period.

Speciality Chemicals Industry Overview

The specialty chemicals market is highly fragmented, with numerous players holding a significant market share. Some of the major players in the market (in no particular order) include BASF SE, Dow, Corteva, Sika AG, and Solvay, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Robust Growth of Construction Activities in Asia-Pacific, and Middle East and Africa

- 4.1.2 Growing Population is Propelling the Demand for Food Worldwide

- 4.2 Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products and Services

- 4.2.5 Degree of Competition

- 4.3 Raw Material Analysis

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Paints and Coatings

- 5.1.1 Dynamics

- 5.1.2 Application

- 5.1.2.1 Architectural

- 5.1.2.2 Automotive

- 5.1.2.3 Industrial

- 5.1.2.4 Wood

- 5.1.2.5 Other Applications

- 5.2 Catalysts

- 5.2.1 Dynamics

- 5.2.2 Function

- 5.2.2.1 Chemical Synthesis Catalysts

- 5.2.2.2 Petroleum Refining Catalysts

- 5.2.2.3 Polymerization Catalysts

- 5.3 Construction Chemicals

- 5.3.1 Dynamics

- 5.3.2 Application

- 5.3.2.1 Commercial

- 5.3.2.2 Industrial

- 5.3.2.3 Infrastructure

- 5.3.2.4 Residential

- 5.3.2.5 Public Space

- 5.4 Cosmetic Chemicals

- 5.4.1 Dynamics

- 5.4.2 Application

- 5.4.2.1 Hair Care

- 5.4.2.2 Skin Care

- 5.4.2.3 Oral Care

- 5.4.2.4 Personal Hygiene

- 5.4.2.5 Other Applications

- 5.5 Dyes, Inks, and Pigments

- 5.5.1 Dynamics

- 5.5.2 Type

- 5.5.2.1 Inks

- 5.5.2.2 Dyes

- 5.5.2.3 Organic Pigments

- 5.5.2.4 Inorganic Pigments

- 5.6 Electronic Chemicals

- 5.6.1 Dynamics

- 5.6.2 Application

- 5.6.2.1 Semiconductors and Integrated Circuits

- 5.6.2.2 Printed Circuit Boards

- 5.7 Water Treatment Chemicals

- 5.7.1 Dynamics

- 5.7.2 Function

- 5.7.2.1 Flocculants

- 5.7.2.2 Coagulants

- 5.7.2.3 Biocides and Disinfectants

- 5.7.2.4 Defoamers and Defoaming Agents

- 5.7.2.5 pH Adjusters and Softeners

- 5.7.2.6 Other Functions

- 5.8 Food Additives

- 5.8.1 Dynamics

- 5.8.2 Type

- 5.8.2.1 Natural Additives

- 5.8.2.2 Synthetic Additives

- 5.9 Agrochemicals

- 5.9.1 Dynamics

- 5.9.2 Type

- 5.9.2.1 Fertilizers

- 5.9.2.2 Herbicide

- 5.9.2.3 Fungicide

- 5.9.2.4 Insecticide

- 5.9.2.5 Nematicide

- 5.9.2.6 Molluscicide

- 5.9.2.7 Other Crop Protection Chemicals

- 5.10 Industrial and Institutional Cleaners

- 5.10.1 Dynamics

- 5.10.2 Application

- 5.10.2.1 General Purpose Cleaners

- 5.10.2.2 Disinfectants and Sanitizers

- 5.10.2.3 Laundry Care Products

- 5.10.2.4 Vehicle Wash Products

- 5.11 Lubricant Additives

- 5.11.1 Dynamics

- 5.11.2 Product Type

- 5.11.2.1 Dispersants and Emulsifiers

- 5.11.2.2 Detergents

- 5.11.2.3 Oxidation Inhibitors

- 5.11.2.4 Extreme-pressure Additives and Anti-wear Additives

- 5.11.2.5 Viscosity Index Modifiers

- 5.11.2.6 Friction Modifiers

- 5.11.2.7 Corrosion Inhibitors

- 5.11.2.8 Other Product Types

- 5.12 Mining Chemicals

- 5.12.1 Dynamics

- 5.12.2 Function

- 5.12.2.1 Flotation Chemicals

- 5.12.2.2 Extraction Chemicals

- 5.12.2.3 Grinding Aids

- 5.13 Oilfield Chemicals

- 5.13.1 Dynamics

- 5.13.2 Application

- 5.13.2.1 Biocide

- 5.13.2.2 Corrosion and Scale Inhibitor

- 5.13.2.3 Demulsifier

- 5.13.2.4 Polymer

- 5.13.2.5 Surfactant

- 5.13.2.6 Other Chemical Types

- 5.14 Adhesives and Sealants

- 5.14.1 Dynamics

- 5.14.2 Technology

- 5.14.2.1 Water-borne Adhesives

- 5.14.2.2 Solvent-borne Adhesives

- 5.14.2.3 Hot-melt Adhesives

- 5.14.2.4 Reactive Adhesives

- 5.14.2.5 Other Adhesives

- 5.14.2.6 Sealants

- 5.15 Plastic Additives

- 5.15.1 Dynamics

- 5.15.2 Plastic Type

- 5.15.2.1 Polyethylene (PE)

- 5.15.2.2 Polystyrene (PS)

- 5.15.2.3 Polypropylene (PP)

- 5.15.2.4 Polyamide (PA)

- 5.15.2.5 Polyethylene Terephthalate (PET)

- 5.15.2.6 Polyvinyl Chloride (PVC)

- 5.15.2.7 Polycarbonate (PC)

- 5.15.2.8 Other Plastic Types

- 5.16 Rubber Processing Chemicals

- 5.16.1 Dynamics

- 5.16.2 Application

- 5.16.2.1 Tire

- 5.16.2.2 Non-tire

- 5.17 Specialty Polymers

- 5.17.1 Dynamics

- 5.18 Textile Chemicals

- 5.18.1 Dynamics

- 5.18.2 Application

- 5.18.2.1 Coating and Sizing Chemicals

- 5.18.2.2 Colorants and Auxiliaries

- 5.18.2.3 Finishing Agents

- 5.18.2.4 Desizing Agents

- 5.18.2.5 Other Application

- 5.19 Geography

- 5.19.1 Asia-Pacific

- 5.19.1.1 China

- 5.19.1.2 India

- 5.19.1.3 Japan

- 5.19.1.4 South Korea

- 5.19.1.5 ASEAN Countries

- 5.19.1.6 Rest of Asia-Pacific

- 5.19.2 North America

- 5.19.2.1 United States

- 5.19.2.2 Canada

- 5.19.2.3 Mexico

- 5.19.2.4 Rest of North America

- 5.19.3 Europe

- 5.19.3.1 Germany

- 5.19.3.2 United Kingdom

- 5.19.3.3 Italy

- 5.19.3.4 France

- 5.19.3.5 Spain

- 5.19.3.6 Rest of Europe

- 5.19.4 South America

- 5.19.4.1 Brazil

- 5.19.4.2 Argentina

- 5.19.4.3 Rest of South America

- 5.19.5 Middle-East and Africa

- 5.19.5.1 Saudi Arabia

- 5.19.5.2 South Africa

- 5.19.5.3 Rest of Middle-East and Africa

- 5.19.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share Analysis

- 6.2.1 Adhesives and Sealants

- 6.2.2 Agrochemicals

- 6.2.3 Construction Chemicals

- 6.2.4 Lubricants and Oil Additives

- 6.2.5 Mining Chemicals

- 6.2.6 Oilfield Chemicals

- 6.2.7 Paints and Coatings

- 6.2.8 Specialty Polymers

- 6.2.9 Water Treatment Chemicals

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 AECI

- 6.4.3 Afton Chemical

- 6.4.4 Akzo Nobel NV

- 6.4.5 Albemarle Corporation

- 6.4.6 ALTANA

- 6.4.7 Archroma

- 6.4.8 Arkema Group

- 6.4.9 Ashland

- 6.4.10 Asian Paints

- 6.4.11 Axalta Coating Systems

- 6.4.12 Baker Hughes Company

- 6.4.13 BASF SE

- 6.4.14 Berger Paints India Limited

- 6.4.15 Buckman

- 6.4.16 Chevron Corporation

- 6.4.17 Clariant

- 6.4.18 Corteva

- 6.4.19 Covestro AG

- 6.4.20 DIC Corporation

- 6.4.21 Dow

- 6.4.22 DSM

- 6.4.23 DuPont

- 6.4.24 Eastman Chemical Company

- 6.4.25 Ecolab

- 6.4.26 Evonik Industries AG

- 6.4.27 Exxon Mobil Corporation

- 6.4.28 Ferro Corporation

- 6.4.29 Flint Group

- 6.4.30 FMC Corporation

- 6.4.31 GCP Applied Technologies Inc.

- 6.4.32 H.B. Fuller Company

- 6.4.33 Halliburton

- 6.4.34 Henkel AG & Co. KGaA

- 6.4.35 Hexcel Corporation

- 6.4.36 Huntsman International LLC

- 6.4.37 Infineum International Limited

- 6.4.38 Kemira

- 6.4.39 KRONOS Worldwide Inc.

- 6.4.40 Kurita Water Industries Ltd

- 6.4.41 Holcim

- 6.4.42 LANXESS

- 6.4.43 Lonza

- 6.4.44 MAPEI SpA

- 6.4.45 Merck KGaA

- 6.4.46 NIPSEA GROUP

- 6.4.47 Nouryon

- 6.4.48 Nutrien Ltd

- 6.4.49 Pidilite Industries Ltd

- 6.4.50 PPG Industries Inc.

- 6.4.51 Procter & Gamble

- 6.4.52 RPM International Inc.

- 6.4.53 SABIC

- 6.4.54 Schlumberger Limited

- 6.4.55 Sika AG

- 6.4.56 Solenis

- 6.4.57 Solvay

- 6.4.58 Syngenta

- 6.4.59 The Chemours Company

- 6.4.60 The Lubrizol Corporation

- 6.4.61 The Sherwin-Williams Company

- 6.4.62 Venator Materials PLC

- 6.4.63 Veolia

- 6.4.64 W. R. Grace & Co.

- 6.4.65 Wacker Chemie AG

- 6.4.66 Yara

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

環氧丙醇市場規模、佔有率及成長分析(按應用、配方類型、分銷管道、最終用途產業和地區)-2025-2032 年產業預測

環氧丙醇市場規模、佔有率及成長分析(按應用、配方類型、分銷管道、最終用途產業和地區)-2025-2032 年產業預測 2025 年特用化學品全球市場報告

2025 年特用化學品全球市場報告 東南亞特種化學品市場:按應用、產品類型和國家/地區進行的分析和預測(2024-2034 年)特種化學品市場規模、佔有率和成長分析(按類型、應用和地區)- 產業預測 2025-2032

東南亞特種化學品市場:按應用、產品類型和國家/地區進行的分析和預測(2024-2034 年)特種化學品市場規模、佔有率和成長分析(按類型、應用和地區)- 產業預測 2025-2032 特用化學品,全球市場 2025-2029

特用化學品,全球市場 2025-2029 全球鑄造化學品市場:產業分析、規模、佔有率、成長、趨勢與預測(2025-2032 年)2024 年特用化學品分佈全球市場報告

全球鑄造化學品市場:產業分析、規模、佔有率、成長、趨勢與預測(2025-2032 年)2024 年特用化學品分佈全球市場報告 特用化學品市場:按類型、功能、產業分類 - 2025-2030 年全球預測

特用化學品市場:按類型、功能、產業分類 - 2025-2030 年全球預測 縮水甘油全球市場

縮水甘油全球市場 二氨基耆二磺酸(DASDA)全球市場(2024-2028)

二氨基耆二磺酸(DASDA)全球市場(2024-2028)