|

市場調查報告書

商品編碼

1683197

垂直共振腔面射型雷射市場:市場佔有率分析、產業趨勢和成長預測(2025-2030 年)Vertical Cavity Surface Emitting Laser - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

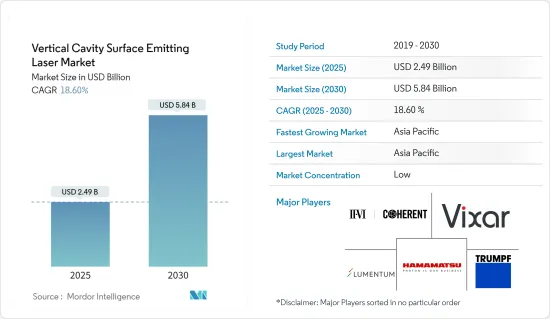

垂直共振腔面射型雷射市場規模預計在 2025 年為 24.9 億美元,預計到 2030 年將達到 58.4 億美元,預測期內(2025-2030 年)的複合年成長率為 18.6%。

就出貨量而言,市場預計將從 2025 年的 51.4 億台成長到 2030 年的 160.6 億台,預測期間(2025-2030 年)的複合年成長率為 25.60%。

垂直共振腔面射型雷射(VCSEL) 是一種雷射垂直發射於其頂面的半導體。這與從邊射型雷射不同。 VCSEL 以經濟高效的解決方案提供高精度、高效率、高可靠性和高速度,是雷射物理學領域最有前途的新發展。 VCSEL 具有多種優勢,包括低功耗、光束品質、調變速度和製造成本。

關鍵亮點

- 由於對高速、高效和遠距資料傳輸的需求不斷增加,汽車雷射雷達應用和工業應用對 VCSEL 雷射的需求不斷增加等多種因素,預計 VCSEL 市場將在預測期內實現強勁成長。 2023 年 8 月,Innoviz Technologies 與BMW集團將擴大合作,啟動新一代 LiDAR 的 B 樣開發階段。

- 在過去的幾年中,資料中心的光互連基礎設施已經從 100Gbit/s 發展到下一代資料速率 400Gbit/s。這主要歸因於AI、VR/AR、物聯網(IoT)等新興技術市場的快速成長,以及5G行動網路系統的引入導致資料中心內資料流量的持續增加。

- 智慧型手機製造商擴大在智慧型手機中採用 VCSEL 進行 3D 感應和接近感應應用,這是推動市場成長的主要因素之一。 3D 感應的成長是由 iPhone 中 Face ID 模組的引入所推動的。自那時起,3D感測領域取得了巨大進步。漸漸地,3D感測已經從前置的臉部認證模組轉移到後置的拍照功能。

- 由於 InP 基 VCSEL 具有低色散和低光纖損耗的特點,因此通常適用於光纖通訊等應用。然而,由於反射率高、穿透深度低,基於 InP 的 VSCEL 無法提供大屈光對比的 DBR 鏡。有效共振器長限制了調諧範圍和限制因子。

- COVID-19 疫情對所研究的市場產生了重大影響,部署 VCSEL 的幾個終端用戶產業面臨多重挑戰。受全國範圍的停工影響,工業陷入停滯,但自2020年第二季起已逐步恢復營運。由於原料從中國購買,因此受到美國徵收關稅的影響。

- 世界各地的地緣政治緊張和衝突正在推動軍事需求。根據斯德哥爾摩國際和平實驗室(SIPRI)統計,2022年美國軍費開支高達8,770億美元,位居世界最高國家之頭。這佔當年世界軍費開支總額2.2兆美元的近40%。這占美國國內生產總值的3.5%。

垂直共振腔面射型雷射市場趨勢

ADAS 和 LiDAR 是快速成長的應用

- 汽車產業是 VCSEL 製造商的主要新興市場之一,受到自動駕駛汽車和汽車高階內裝功能等趨勢的推動。儘管近年來汽車產業受到衰退的打擊,但每輛汽車感測器數量的增加是推動供應商發展的主要動力。大多數市場供應商正在擴大其在汽車市場(內部和外部應用)的影響力。

- LiDAR 是 ADAS 的關鍵組件,高效的 VCSEL 因其佔用空間小、價格誘人、可靠性和性能卓越而非常適合 ADAS LiDAR。 VCSEL 用於 LiDAR 系統中的物體偵測和距離測繪、ADAS 和自動駕駛的外部感測技術以及用於汽車內部和外部的 3D 感測。

- 為了實現 LEVEL 4 級自動駕駛,大多數已開發地區和新興地區都已強製或計劃強制在新車中安裝 ADAS,這預計將為市場供應商創造巨大的成長機會。例如,在美國,80-90%的新車都配備至少一項ADAS功能。

- 根據國家安全委員會的數據,到 2026 年,大約 71% 的註冊車輛將配備後視攝影機,60% 的註冊車輛將配備後部停車感測器。 ADAS 的普及可能會推動市場的成長。

- 自動駕駛和自動駕駛汽車的日益普及是 ADAS 市場的主要成長要素。例如,根據英特爾預測,2030 年全球汽車銷售將達到 1.014 億輛以上,自動駕駛汽車預計將佔 2030 年汽車註冊量的 12% 左右。

由於中國佔據市場主導地位,預計亞太地區將顯著成長

- 在亞太地區,由於汽車、醫療和消費電子產業對 VCSEL 的應用日益廣泛,預計中國將顯著成長。

- 中國是世界領先的家用電子電器製造國之一。該地區的製造業正在快速成長,並引進了一系列製造和通訊技術。

- 隨著來自世界各地的各種電子設備不斷湧入中國,中國的半導體消費成長速度快於其他國家。全球五大知名行動電話公司中有三家總部位於韓國,這為半導體應用提供了絕佳的機會。

- 中國政府也致力於創建一個動力來源的科技權威國家,以追蹤和監控其公民。預計此類項目將提振該國研究市場的需求。中國政府的「中國製造2025」計畫旨在2030年將半導體產業產值提升至3,050億美元,滿足80%的國內需求。預計這些發展將促進該國市場的成長。

- 領先的公司正專注於開發創新產品以鞏固其市場地位。例如,VCSEL 半導體研發先驅、高速光纖通訊和 3D 深度攝影機用 VCSEL 製造商 Berxel Photonics 於 2023 年 9 月在中國深圳舉行的中國國際光電博覽會上宣布現場演示搭載 106Gbps VCSEL 的 800G 收發器。

- 推動 VCSEL 成長的另一個因素是電動車的日益普及。例如,該技術有望應用於汽車行業,用於手勢識別、駕駛員監控和自動駕駛感測器等應用。該地區的汽車工業正在以驚人的速度成長。該地區對自訂半導體和感測器的需求正在增加。因此,VCSEL 技術有望在該領域發揮關鍵作用。根據中汽協的數據,2023年8月中國純電動車產量為58.9萬輛,其中搭乘用55.1萬輛,商用車3.8萬輛。同月,中國生產了25.4萬輛PHEV,其中搭乘用PHEV 25.3萬輛,商用車PHEV 1000輛。

- 中國政府把汽車產業,包括零件產業定位為重點產業之一。政府預計到 2025 年中國汽車產量將達到 3,500 萬輛。這些案例表明,預計在預測期內市場將會成長。

垂直共振腔面射型雷射產業概況

VCSEL 市場比較分散,主要參與者包括 Coherent Corporation、Lumentum Operations LLC、Vixar Inc(OSRAM AG)、Hamamatsu Photonics KK 和 TRUMPF Group。市場參與企業正在採取聯盟和收購等策略來加強其產品供應並獲得永續的競爭優勢。

- 2023 年 10 月 -資料通訊用高速 VCSEL 和光電二極體解決方案的全球參與企業通快光子元件公司 (Trumpf Photonic Components) 和西班牙高速光纖網路連結解決方案專家 KDPOF 在格拉斯哥舉行的歐洲光纖通訊會議 (ECOC) 上展示了首個用於車載系統的 980nm 多Gigabit互載系統。

- 2023 年 6 月 - 全球領先的光學解決方案供應商 AMS Osram 宣布推出 TARA2,000-AUT-SAFE 系列垂直共振腔面射型雷射(VCSEL)。該公司加強了用於汽車內部感測的紅外線雷射模組產品組合,並增加了更可靠、更強大的眼部安全功能。新型 TARA2,000-AUT-SAFE 可產生嚴格控制的紅外線光束,峰值波長為 940nm。它支援與現有TARA2,000-AUT系列相同的應用場景,包括駕駛員監控、手勢感應和車內監控。此緊湊模組包含一個歐司朗 VCSEL 晶片和一個 ams 微透鏡陣列 (MLA)。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 購買者和消費者的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 專利狀況

- COVID-19 的副作用和其他宏觀經濟因素將如何影響市場

第4章 市場動態

- 市場促進因素

- 資料中心擴大採用 VCSEL

- 智慧型手機對 3D 感測應用的需求不斷增加

- 市場限制

- InP基VCSEL滲透率低,資料傳輸範圍有限

第5章:材料趨勢分析

- 氮化鎵

- 砷化鎵

- 其他材料類型

第6章 市場細分

- 按波長

- 紅色 (650-750 奈米)

- 近紅外線(750-1,400 nm)

- 短波紅外線(1,400 至 3,000 nm)

- 按晶粒尺寸

- 0.02~0.06 mm2

- 0.06~0.4 mm2

- 0.4~1.3 mm2

- 10~75 mm2

- 按最終用戶產業

- 電信

- 行動和消費電子

- 車

- 醫療

- 產業

- 航太和國防

- 按應用

- 資料通訊

- 光電滑鼠

- 臉部辨識和深度相機

- 手勢姿態辨識

- 雷射自動對焦

- 接近感測器

- 虹膜掃描

- 醫療的

- ADAS LiDAR

- 工業應用

- 其他

- 按地區

- 北美洲

- 歐洲

- 台灣

- 中國

- 韓國

- 日本

- 其他

第7章 競爭格局

- 公司簡介

- Coherent Corporation

- Lumentum Operations LLC

- Vixar Inc(OSRAM AG)

- Hamamatsu Photonics KK

- TRUMPF Group

- ams OSRAM AG

- HLJ Technology Co. Ltd

- Teledyne FLIR Systems Inc.

- Vertilite Inc.

- Leanardo Electronics US(Lasertel)

- Broadcom Inc.

- Santec Corporation

第8章投資分析

第9章 市場機會與未來趨勢

The Vertical Cavity Surface Emitting Laser Market size is estimated at USD 2.49 billion in 2025, and is expected to reach USD 5.84 billion by 2030, at a CAGR of 18.6% during the forecast period (2025-2030). In terms of shipment volume, the market is expected to grow from 5.14 billion units in 2025 to 16.06 billion units by 2030, at a CAGR of 25.60% during the forecast period (2025-2030).

The vertical-cavity surface-emitting laser (VCSEL) is a semiconductor whose laser is emitted perpendicular to the top surface. It differs from an edge-fired laser, which emits the laser from the edge. VCSELs offer precision, high efficiency, reliability, and high speed with a cost-effective solution, and these are the most promising new technological developments in laser physics. VCSELs offer various advantages, such as lower power consumption, beam quality, modulation speeds, and manufacturing costs.

Key Highlights

- The VCSEL market is anticipated to witness robust growth during the forecast period owing to several factors like increasing requirements for transmitting data over long distances with high speed and efficiency, rising demand for these lasers in automotive LiDAR applications, and industrial applications. In August 2023, Innoviz Technologies and the BMW Group are expanding their collaboration by starting a B-sample development phase on a new generation of LiDAR.

- Over the past few years, optical interconnect infrastructures in the data centers have advanced to the next-generation 400 Gbit/s data rate from 100 Gbit/s. This is primarily driven by the ever-increasing data traffic in data centers due to the rapid market growth of emerging technologies, such as AI, VR/AR, and the Internet of Things (IoT), and the introduction of 5G mobile network systems.

- The increasing adoption of VCSELs in smartphones by smartphone manufacturers for 3D sensing or proximity sensing applications is one of the primary factors driving the market growth. The growth of 3D sensing was propelled by the introduction of face ID modules in iPhones. Since then, there have been significant developments in 3D sensing. Slowly, there was a transition of 3D sensing from front-side face ID modules to the rear side for photography applications.

- InP-based VCSELs are typically preferred for applications such as optical communication due to their low dispersion and low fiber loss. However, InP-based VSCELs cannot provide large refractive index contrast DBR mirrors, owing to the high reflectivity and low penetration depth. The effective cavity length limits the tuning range and the confinement factor.

- The COVID-19 pandemic had a remarkable impact on the market studied, with several end-user industries that deploy VCSEL facing several difficulties. The industries were stuck with nationwide lockdowns, which brought them to a standstill, but after Q2 of 2020, they gradually started their operation. Since the raw materials are bought in China, the sourcing has been affected by the tariffs imposed by the United States.

- Geopolitical tensions and conflicts worldwide drive the demand for military spending. According to the Stockholm International Peace Research Institute (SIPRI), the United States led the ranking of countries with the highest military expenditure in 2022, with USD 877 billion dedicated to the military. That constituted nearly 40 percent of the total military spending worldwide that year, which amounted to USD 2.2 trillion. This amounted to 3.5 percent of the US gross domestic product.

Vertical Cavity Surface Emitting Laser Market Trends

ADAS and LiDAR to be the Fastest-growing Application

- The automotive industry is one of the major emerging markets for the VCSEL manufacturers, owing to trends like autonomous vehicles and high-end interior features in vehicles. Although the automotive industry has been witnessing a recession in recent years, the growing number of sensors per vehicle is mainly motivating the market vendors. Most of the market vendors are expanding their scope for the automotive market (interior and exterior applications).

- LiDAR is a critical component of ADAS, and highly efficient VCSELs, with their tiny footprint, attractive pricing, and remarkable reliability and performance, are making them suitable for ADAS LIDAR. VCSELs are used in LiDAR systems for object detection and mapping distances, exterior sensing technologies for ADAS and autonomous driving, and automotive 3D sensing for in-cabin and outside the vehicle, among others.

- In order to achieve LEVEL 4 autonomy, most of the developed and developing regions have mandated or are planning to mandate ADAS in new vehicles, which is expected to create massive growth opportunities for the market vendors. For instance, 80-90% of new vehicles in the United States have at least one ADAS feature.

- According to the National Safety Council, by 2026, approximately 71% of registered vehicles will be equipped with rear cameras, while 60% will have rear parking sensors. Such increasing adoption of ADAS would aid the growth of the market studied.

- The increasing adoption of self-driving or autonomous vehicles is a primary growth factor for the ADAS market. For instance, according to Intel, global car sales are expected to reach over 101.4 million units in 2030, and autonomous vehicles are expected to account for about 12% of car registrations by 2030.

Asia-Pacific Expected to Witness Significant Growth with China Dominating the Market

- China is expected to grow substantially in the Asia-Pacific region due to the increasing adoption of VCSEL in the automotive, healthcare, and consumer electronics industries.

- China is one of the prominent consumer electronics producers across the world. The manufacturing industry is rapidly growing in the region and is witnessing the deployment of various manufacturing and telecommunications technologies, which is expected to aid in the market's growth.

- Due to the continued flow of global, diversified electronics equipment into China, the consumption of semiconductors in China is growing faster than in others. Three of the world's top five most prominent mobile phone companies are based in this country, which presents enormous opportunities for adopting semiconductors.

- The Chinese government is also working to create a techno-authoritarian state powered by artificial intelligence and sensors to track and monitor its citizens. The demand for market studied in the country is expected to grow with such programs. The Chinese government's "Made in China 2025" initiative aims to make its semiconductor industry reach USD 305 billion in output by 2030 and meet 80% of domestic demand. Such instances are estimated to boost the market's growth in the country.

- Major players focus on developing innovative products to strengthen their market positions. For instance, in September 2023, Berxel Photonics, a pioneer in VCSEL semiconductor R&D and manufacturer of high-speed optical communications VCSELs and 3D depth cameras, announced a live demo of its 106 Gbps VCSEL-powered 800G transceiver in China International Optoelectronic Exposition in Shenzhen, China.

- Another factor contributing to the growth of VCSEL is the growing adoption of electric vehicles. For example, this technology is anticipated to be used in the vehicle industry for applications like recognition of gestures, driver monitoring, and autonomous driving sensors. In this region, the auto industry is growing at an excellent rate. The demand for custom semiconductors and sensors is increasing in the area. Therefore, VCSEL technology is expected to play a significant role in the region. As per CAAM, 589,000 battery-electric vehicles were made in China in August 2023, with 551,000 passenger BEVs and 38,000 business BEVs. In the same month, 254,000 PHEVs were produced in China, of which 253,000 were passenger PHEVs, and 1,000 were commercial PHEVs.

- The Chinese government views its automotive industry, including the auto parts sector, as one of its pillar industries. The government expects China's automobile output to reach 35 million units by 2025. Such instances show that the market is anticipated to grow over the forecast period.

Vertical Cavity Surface Emitting Laser Industry Overview

The VCSEL market is fragmented with the presence of major players like Coherent Corporation, Lumentum Operations LLC, Vixar Inc (OSRAM AG), Hamamatsu Photonics KK, and TRUMPF Group. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- October 2023 - TRUMPF Photonic Components, a global player in high-speed VCSEL and photodiode solutions for data communication, and KDPOF, an expert in high-speed optical networking solutions based in Spain, showcased its first 980nm multi-gigabit interconnect system for automotive systems at the European Conference for Optical Communication (ECOC), held in Glasgow.

- June 2023 - AMS Osram, the world's significant supplier of optical solutions, announced the launch of the TARA2000-AUT-SAFE family of vertical cavity surface emitting lasers (VCSELs), Reliable and more robust eye safety features while enhancing the portfolio of infrared laser modules for automotive in-cabin sensing. The new TARA2000-AUT-SAFE generates a tightly controlled beam of infrared light at a peak wavelength of 940nm. It suits the same application scenarios as the existing TARA2000-AUT series: driver monitoring, gesture sensing, and in-cabin monitoring. The compact module contains an ams Osram VCSEL chip and a microlens array (MLA).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

- 3.1 Market Overview

- 3.2 Industry Attractiveness - Porter's Five Forces Analysis

- 3.2.1 Bargaining Power of Suppliers

- 3.2.2 Bargaining Power of Buyers/Consumers

- 3.2.3 Threat of New Entrants

- 3.2.4 Threat of Substitute Products and Services

- 3.2.5 Intensity of Competitive Rivalry

- 3.3 Patent Landscape

- 3.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Increasing Adoption of VCSEL in Data Centers

- 4.1.2 Growing Demand for 3D Sensing Applications in Smartphones

- 4.2 Market Restraints

- 4.2.1 Low Penetration of InP-based VCSELs and Limited Data Transmission Range

5 MATERIAL TREND ANALYSIS

- 5.1 Gallium Nitride

- 5.2 Gallium Arsenide

- 5.3 Other Material Types

6 MARKET SEGMENTATION

- 6.1 By Wavelength

- 6.1.1 Red (650-750 nm)

- 6.1.2 Near-infrared (750-1400 nm)

- 6.1.3 Shortwave-infrared (1400-3000 nm)

- 6.2 By Die-size

- 6.2.1 0.02 - 0.06 mm2

- 6.2.2 0.06 - 0.4 mm2

- 6.2.3 0.4 - 1.3 mm2

- 6.2.4 10 - 75 mm2

- 6.3 By End-user Industry

- 6.3.1 Telecom

- 6.3.2 Mobile and Consumer

- 6.3.3 Automotive

- 6.3.4 Medical

- 6.3.5 Industrial

- 6.3.6 Aerospace and Defense

- 6.4 By Application

- 6.4.1 Datacom

- 6.4.2 Optical Mouse

- 6.4.3 Facial Recognition and Depth Camera

- 6.4.4 Gesture Recognition

- 6.4.5 Laser Autofocus

- 6.4.6 Proximity sensing

- 6.4.7 Iris Scan

- 6.4.8 Medical

- 6.4.9 ADAS LiDAR

- 6.4.10 Industrial Applications

- 6.4.11 Other Applications

- 6.5 By Geography

- 6.5.1 North America

- 6.5.2 Europe

- 6.5.3 Taiwan

- 6.5.4 China

- 6.5.5 South Korea

- 6.5.6 Japan

- 6.5.7 Rest of the World

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Coherent Corporation

- 7.1.2 Lumentum Operations LLC

- 7.1.3 Vixar Inc (OSRAM AG)

- 7.1.4 Hamamatsu Photonics KK

- 7.1.5 TRUMPF Group

- 7.1.6 ams OSRAM AG

- 7.1.7 HLJ Technology Co. Ltd

- 7.1.8 Teledyne FLIR Systems Inc.

- 7.1.9 Vertilite Inc.

- 7.1.10 Leanardo Electronics US (Lasertel)

- 7.1.11 Broadcom Inc.

- 7.1.12 Santec Corporation

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

垂直腔面發射雷射器市場報告(按類型、材料、波長(紅色、近紅外線、短波紅外線)、應用、最終用途產業和地區)2025 年至 2033 年

垂直腔面發射雷射器市場報告(按類型、材料、波長(紅色、近紅外線、短波紅外線)、應用、最終用途產業和地區)2025 年至 2033 年 2025年垂直共振腔面射型雷射(VCSEL)全球市場報告

2025年垂直共振腔面射型雷射(VCSEL)全球市場報告 垂直共振腔面射型雷射(VCSEL) 市場規模、佔有率和成長分析(按類型、波長、材料、應用、資料速率、垂直和地區)- 產業預測 2025-2032到 2030 年垂直共振腔面射型雷射(VCSEL) 市場預測:按類型、波長、技術、封裝類型、輸出功率、應用、最終用戶和地區進行的全球分析垂直共振腔面射型雷射市場:按類型、材質、波長、晶粒尺寸、應用、最終用戶 - 2025-2030 年全球預測

垂直共振腔面射型雷射(VCSEL) 市場規模、佔有率和成長分析(按類型、波長、材料、應用、資料速率、垂直和地區)- 產業預測 2025-2032到 2030 年垂直共振腔面射型雷射(VCSEL) 市場預測:按類型、波長、技術、封裝類型、輸出功率、應用、最終用戶和地區進行的全球分析垂直共振腔面射型雷射市場:按類型、材質、波長、晶粒尺寸、應用、最終用戶 - 2025-2030 年全球預測 垂直共振腔面射型雷射(VCSEL) 的全球市場 2024-2028

垂直共振腔面射型雷射(VCSEL) 的全球市場 2024-2028 垂直共振腔面射型雷射的全球市場:趨勢、預測和競爭分析(截至 2030 年)VCSEL 市場,按類型、應用、國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測

垂直共振腔面射型雷射的全球市場:趨勢、預測和競爭分析(截至 2030 年)VCSEL 市場,按類型、應用、國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測 全球 VCSEL 市場:按類型、波長、材料、應用、資料速率、產業、地區分類 - 到 2029 年的預測

全球 VCSEL 市場:按類型、波長、材料、應用、資料速率、產業、地區分類 - 到 2029 年的預測 垂直共振腔面射型雷射(VCSEL) 的全球市場

垂直共振腔面射型雷射(VCSEL) 的全球市場