|

市場調查報告書

商品編碼

1683216

電源模組封裝:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Power Module Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

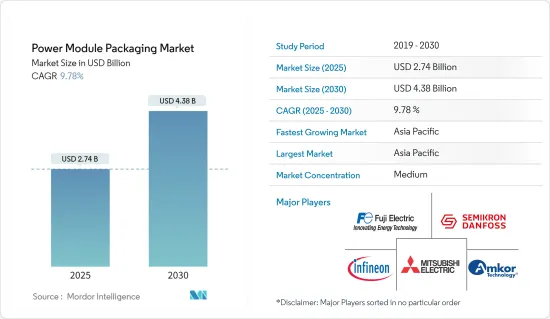

預計 2025 年功率模組封裝市場規模為 27.4 億美元,到 2030 年將達到 43.8 億美元,預測期內(2025-2030 年)的複合年成長率為 9.78%。

電力電子模組或電源模組可作為容納多個電力元件(通常是電力半導體元件)的實體容器。封裝在向更高功率密度轉變的過程中發揮關鍵作用,可實現更有效率的電源、更快的轉換、電力傳輸和更高的可靠性。隨著世界轉向更快的開關頻率和更高的功率密度,我們看到用於引線接合法、晶粒黏接、基板和系統冷卻的封裝材料也發生了相應的變化。

主要亮點

- 功率模組是電源逆變器和轉換器的關鍵元件。電源模組常用於電動車和其他馬達控制器、家用電器、電源、電鍍機、醫療設備、電池充電器、交直流逆變器和轉換器、電源開關、焊接設備等。功率模組封裝市場的成長得益於減少能源浪費、採用高效的分散式冷卻方法、縮小佔地面積以及隨之而來的功率密度的提高。此外,工業和家用電子電器領域對電源模組的需求不斷成長,正在推動電源模組封裝市場的發展。

- 家用電子電器產業正在經歷重大轉型,推動力在於對更智慧、更先進設備的需求不斷成長。電子產業的另一個重要趨勢是物聯網(IoT)的興起。隨著對智慧型設備的需求不斷成長,物聯網已成為我們日常生活中不可或缺的一部分。因此,企業主要使用這項技術來開發新產品和服務。例如,根據 GSMA 的數據,中國以 15 億個連線數領先,其次是北美和歐洲,各有 3 億個連線數。

- 不斷電系統(UPS)、伺服器電源、電源轉換器和馬達驅動器等工業設備消耗了世界上很大一部分電力。因此,提高工業電源的效率可以大幅降低企業營運成本。不斷增加的功率密度和改善的熱性能推動了對高效電源的需求呈指數級成長。

- 由於電源模組製造商面臨日益增加的複雜性、莫耳定律變得越來越難以維持且成本越來越高而導致的未來設計藍圖的丟失,以及標準不斷發展且規則各異的大量新市場的湧入,整合可能會持續下去。

- 俄烏戰爭推高了鋁價和鎳價,而能源價格上漲則影響了金屬,尤其是銅價。銅是功率模組封裝市場的重要材料,用於底板和電氣互連。銅價的波動對功率模組封裝市場有直接的影響。根據 ukraineinvest.gov 報導,預計金屬價格在 2022 年將上漲 16%,然後在 2023 年有所回落。俄羅斯和烏克蘭之間持續的戰爭、中國更嚴格的排放法規以及高昂的能源成本是造成銅短缺的主要因素。

電源模組封裝市場趨勢

互聯互通將佔據主導地位

- 功率模組是電源逆變器和轉換器的關鍵元件。電源模組常用於電動車和其他馬達控制器、家用電器、電源、電鍍機、醫療設備、電池充電器、交直流逆變器和轉換器、電源開關、焊接設備等。功率模組封裝市場的成長得益於減少能源浪費、採用高效的分散式冷卻方法、縮小佔地面積以及隨之而來的功率密度的提高。

- 互連器用於建立管理系統的電子組件中不同主動元件和被動元件之間的連接。連接器在智慧型手機、筆記型電腦、電腦和電視等通訊和消費性電子應用中很常見,推動了對創新和先進的電源模組封裝解決方案的需求。例如,根據GSMA的預測,2023年亞太地區的智慧型手機普及率將達到78%。到 2030 年,亞太地區的智慧型手機普及率預計將達到 90% 以上,這將推動市場成長。

- 值得注意的是,互連技術是封裝的關鍵且必要部分。晶片之間透過封裝相互連接,接收電能、交換訊號並最終運作。隨著互連方法改變半導體產品的速度、密度和功能,它們也在不斷發展和演變。

- 通常,電源模組內的功率元件使用引線鍵合進行電氣連接,並使用矽膠填充絕緣層進行互連。大直徑銅線鍵合、銀燒結、無線鍵結互連、基於平面軟性的封裝等技術均被不同程度地引入,以改善新型綜合能隙功率模組的寄生電感和電阻、耐溫性、可靠性和熱性能。

- 互連主要可以透過受有效功率循環限制的晶片連接的壽命來描述。焊料夾在晶片和基板之間,在主動加熱過程中僅在 Z 方向膨脹。這會導致焊料體疲勞。銀燒結技術可將鬆散的金屬粉末轉變成緊密結合的多孔結構,從而延長動力循環能力。此外,互連是透過燒結低溫活化的最小球形顆粒形成的。

亞太地區可望強勁成長

- 由於中國等國家擴大採用可再生能源以及電動/混合動力汽車的數量不斷增加,該地區預計將佔據最高佔有率。中國已成為可再生能源領域的主導力量。中國政府已經開始了擺脫煤炭的歷史性舉措,並且取得了巨大進展。根據中國國家統計局的數據,過去十年來,煤炭在能源消耗中的比例從68.5%下降到56%。

- 政府正在推動減少排放並改善空氣品質。根據世界能源監測的數據,中國的太陽能發電量達到 228 吉瓦(GW),風電發電量更是高達 310 吉瓦,超過世界其他國家的總和。中國計劃在2030年實現1,200吉瓦的目標,另外還有750吉瓦的新計畫正在籌備中。

- 印度雄心勃勃的可再生能源目標正在改變電力產業。印度可再生電力的成長正在加速,預計2026年新增發電能力將翻倍。隨著更有效率的電池用於儲存電力,且太陽能成本較現在進一步下降 66%,預計到 2040 年可再生能源將佔總發電量的 49% 左右。

- 印度政府在COP26高峰會上承諾2070年實現淨零排放,到2030年將可再生能源目標提高到500吉瓦,這對該產業的發展做出了重大貢獻。印度政府已採取多項舉措推動可再生能源產業的發展。

功率模組封裝產業概況

功率模組封裝市場已基本固體,主要參與者如下:富士電機、英飛凌科技股份公司、三菱電機株式會社 (Powerex Inc.)、賽米控和安靠科技公司。

由於整合不斷加強、技術進步和地緣政治情勢的變化,所研究的市場正在經歷波動。此外,隨著代工廠和IDM之間的垂直整合不斷加強,考慮到參與者的收益驅動型投資能力,受調查市場的競爭態勢預計將繼續加劇。

在透過創新獲得永續競爭優勢至關重要的市場中,隨著汽車等終端用戶產業的需求預計將激增,競爭只會加劇。

在這種情況下,考慮到最終用戶對播放器的包裝品質的期望,品牌標識起著重要作用。由於富士電機、三菱電機、AMKOR、ONSemi 和 Semikron 等現有主要市場參與者的存在,市場滲透率也很高。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 買家的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- 評估新冠肺炎疫情和宏觀經濟趨勢對產業的影響

- 技術簡介

第5章 市場動態

- 市場促進因素

- 工業和消費性電子領域的需求不斷成長

- 節能設備的需求不斷增加

- 市場限制

- 市場整合影響整體盈利

第6章 市場細分

- 依技術分類

- 基板

- 底板

- 晶粒黏接

- 基板安裝

- 封裝

- 互連

- 其他技術

- 按地區

- 北美洲

- 歐洲

- 亞洲

- 澳洲和紐西蘭

- 拉丁美洲

- 中東和非洲

第7章 競爭格局

- 公司簡介

- Fuji Electric Co. Ltd

- Infineon Technologies AG

- Mitsubishi Electric Corporation(Powerex Inc.)

- Semikron

- Amkor Technology Inc.

- Hitachi Ltd

- STMicroelectronics NV

- MacMic Science & Technology Co. Ltd

- Texas Instruments Inc.

- Starpower Semiconductor Ltd

- Toshiba Corporation

第8章投資分析

第9章:市場的未來

The Power Module Packaging Market size is estimated at USD 2.74 billion in 2025, and is expected to reach USD 4.38 billion by 2030, at a CAGR of 9.78% during the forecast period (2025-2030).

A power electronic module or power module acts as a physical container for storing several power components, usually power semiconductor devices. Packaging plays a crucial role in the shift toward higher power densities, which enables more efficient power supplies, faster conversion, power delivery, and improved reliability. As the world is shifting toward faster-switching frequencies and higher power densities, there is a related shift in packaging materials used for wire bonding, die-attach, substrates, and system cooling.

Key Highlights

- The power modules are the key elements in the power inverters and converters. Power modules are commonly used in electric cars and other electric motor controllers, appliances, power supplies, electroplating machinery, medical equipment, battery chargers, AC to DC inverters and converters, power switches, and welding equipment. The power module packaging market's growth is driven by a reduction in the wastage of energy, the use of efficient distributed cooling schemes, a reduction in footprint, and a consequent increase in power density. Moreover, the growing demand for power modules in the industrial and consumer electronics sector is set to drive the power module packaging market.

- The consumer electronics industry has experienced a significant transformation driven by the rising demand for smarter and more advanced devices. Another important trend in the electronics industry is the increase of the Internet of Things (IoT). With the rise in demand for smart devices, IoT has become essential to everyday life. Thus, businesses primarily use this technology to develop new products and services. For instance, according to GSMA, greater China leads significantly with 1.5 billion connections, surpassing other regions, and is followed by North America and Europe with 0.3 billion connections each.

- Industrial appliances such as uninterruptible power supplies (UPS), server power supplies, power converters, and motor drives consume a significant portion of the world's power. Therefore, any increase in efficiency in industrial power supplies will substantially reduce a company's operating costs. With greater power density and better thermal performance, the demand for high-efficiency power supplies is increasing exponentially.

- The consolidation will increase as power module manufacturers grapple with the increasing complexity, the loss of a roadmap for future designs as Moore's Law is becoming more difficult and expensive to sustain, and a flood of new markets with evolving standards and different sets of rules.

- The Russia and Ukraine War is driving the aluminum and nickel prices upward, while high energy prices have affected metals, specifically copper. Copper is a crucial material in the power module packaging market, and it is used in baseplate and electrical interconnections. Copper price fluctuations will directly impact the power module packaging market. Metal prices were expected to increase 16% in 2022 and ease somewhat in 2023, according to ukraineinvest.gov. The ongoing war between Russia and Ukraine, stricter emissions standards in China, and high energy costs are the main factors in the increasing shortage of copper.

Power Module Packaging Market Trends

Interconnections Holds Major Share

- The power modules are the key elements in the power inverters and converters. Power modules are commonly used in electric cars and other electric motor controllers, appliances, power supplies, electroplating machinery, medical equipment, battery chargers, AC to DC inverters and converters, power switches, and welding equipment. The power module packaging market's growth is driven by a reduction in the wastage of energy, the use of efficient distributed cooling schemes, a reduction in footprint, and a consequent increase in power density.

- Interconnects are used to establish connections between different active and passive components within an electronic assembly that manages a system. Connectors are commonly utilized in telecommunications and consumer electronics applications, such as smartphones, laptops, computers, and TVs, and are driving the demand for innovative and advanced power module packaging solutions. For instance, as per GSMA, in 2023, the smartphone adoption rate across the Asia-Pacific region reached 78%. By 2030, smartphone adoption in APAC is projected to reach over 90%, which would drive the market growth.

- It is important to note that interconnection technology is a critical and necessary part of packaging. Chips are interconnected through packaging to receive power, exchange signals, and, ultimately, operate. As a semiconductor product's speed, density, and functions change depending on how the interconnection is made, interconnection methods constantly evolve and develop.

- Typically, power devices in a power module are interconnected using wire bonds for electrical connection and filled with silicone gel for insulation. Technologies such as large-diameter copper wire bonds, silver sintering, wirebondless interconnects, and planar flex-based packaging to improve the parasitic inductance and resistance, temperature capability, reliability, and thermal performance of new comprehensive band gap power modules have been implemented to varying degrees of success.

- Interconnections can be explained by the lifetime of a chip connection, which is mainly limited by active power cycles. The solder is sandwiched between the chip and substrate and can expand only in the Z-direction during active heating. This leads to fatigue of the solder body. Silver sintering, which is the transformation of a loose metal powder into a firmly bonded porous structure, has been introduced to extend the power cycling capability. Further, the interconnect is formed by sintering the smallest sphere-like particles, activated at low temperatures.

Asia-Pacific is Expected to Witness Major Growth

- The region is expected to occupy the highest share, owing to the increasing adoption of renewable energy and the rising number of electric/hybrid vehicles in countries like China. China has emerged as a dominant force in the renewable energy stage. The Chinese government has made significant strides in beginning a historic shift away from coal. Over the last decade, according to China's National Bureau of Statistics, coal's share of energy consumption decreased from 68.5% to 56%.

- The government is pushing for emissions reductions and improved air quality. According to Global Energy Monitor, China's solar capacity is 228 gigawatts (GW), with wind capacity at a whopping 310 GW more than the rest of the world combined. China aims to hit its 2030 target of 1,200 GW, with another 750 GW of new wind and solar projects in the pipeline.

- India's ambitious renewable energy goals are transforming its power sector. Renewable electricity is growing faster in India, and the new capacity additions are expected to double by 2026. As more efficient batteries will be used to store electricity, which will further reduce the cost of solar energy by 66% compared to the current price, renewable energy is expected to make up around 49% of total electricity generation by 2040.

- The Indian government's commitment to achieving net zero emissions by 2070 and increasing its renewable energy target to 500 GW by 2030 at the COP26 Summit has significantly contributed to industry growth. The government is taking several initiatives to boost India's renewable energy sector.

Power Module Packaging Industry Overview

The power module packaging market is semi-consolidated, with the presence of major players such as Fuji Electric Co. Ltd, Infineon Technologies AG, Mitsubishi Electric Corporation (Powerex Inc.), Semikron, and Amkor Technology Inc. These players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

With the growing consolidation, technological advancement, and geopolitical scenarios, the market studied has been witnessing fluctuation. In addition, with the increasing vertical integration of foundries and IDMs, the intensity of competition in the market studied is expected to continue to rise, considering players' ability to invest, which results from their revenues.

In a market where the sustainable competitive advantage through innovation is significant, competition will only increase, given the anticipated surge in demand from end-user industries such as automotive.

In such a scenario, the brand identity plays a major role, considering the importance of packaging quality that the end users expect from the player. With the presence of large market incumbents, such as Fuji Electric, Mitsubishi, AMKOR, Onsemi, and Semikron, the market penetration levels are also high.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHT

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products and Services

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of the Impact of COVID-19 and Macroeconomic Trends on the Industry

- 4.4 Technology Snapshot

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand from the Industrial and Consumer Electronics Segment

- 5.1.2 Rising Demand for Energy-efficient Devices

- 5.2 Market Restraints

- 5.2.1 Market Consolidation Affecting Overall Profitability

6 MARKET SEGMENTATION

- 6.1 By Technology

- 6.1.1 Substrate

- 6.1.2 Baseplate

- 6.1.3 Die Attach

- 6.1.4 Substrate Attach

- 6.1.5 Encapsulations

- 6.1.6 Interconnections

- 6.1.7 Other Technologies

- 6.2 By Geography

- 6.2.1 North America

- 6.2.2 Europe

- 6.2.3 Asia

- 6.2.4 Australia and New Zealand

- 6.2.5 Latin America

- 6.2.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Fuji Electric Co. Ltd

- 7.1.2 Infineon Technologies AG

- 7.1.3 Mitsubishi Electric Corporation (Powerex Inc.)

- 7.1.4 Semikron

- 7.1.5 Amkor Technology Inc.

- 7.1.6 Hitachi Ltd

- 7.1.7 STMicroelectronics NV

- 7.1.8 MacMic Science & Technology Co. Ltd

- 7.1.9 Texas Instruments Inc.

- 7.1.10 Starpower Semiconductor Ltd

- 7.1.11 Toshiba Corporation