|

市場調查報告書

商品編碼

1683434

機器人和 ADAS 車輛感測器格局:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)Sensor Landscape in Robotics and ADAS Vehicles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

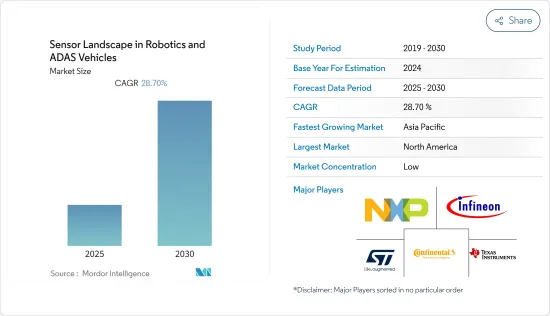

預測期內,機器人和 ADAS 車輛的感測器市場預計將以 28.7% 的複合年成長率成長

關鍵亮點

- 此外,隨著研發活動集中在部署全自動駕駛汽車,實現車輛周圍 360 度安全的感測技術變得至關重要。谷歌和優步等公司已開始致力於開發完全自動駕駛無人駕駛汽車。

- 雷達感測器市場正在經歷快速的技術創新,比以往任何時候都更具活力。雷達的新用途不斷湧現,包括生命徵象駕駛員監控系統、底盤對地監控、免持後行李箱開啟等等。業界目前正在設想雷達成像的可能性。毫無疑問,這項技術對於自動駕駛汽車、無人駕駛汽車和廣告航空領域將發揮重要作用。例如,2019 年,Velodyne 在奧蘭多舉行的研討會上推出了 Alphapuck。這是一款專為高速公路上的自動駕駛和高級車輛安全而設計的 LiDAR 感測器。它結合了遠距高解析度和寬視野。

- 政府強制安裝自動防撞煞車系統等技術正在推動市場的發展。同樣,政府強調減少車輛排放氣體,要求汽車和其他商用車輛更加節省燃料,這導致壓力感測器的成長。例如,中國政府計劃在2020年引入新的排放氣體標準“6A”,以進一步減少汽車排放氣體。

- 隨著最近 COVID-19 疫情的爆發,汽車感測器的成長率有所放緩,因為各大汽車製造廠已根據世界各國實施的封鎖措施全面停產。此外,自動駕駛汽車將受到衝擊,由於近期新冠疫情導致汽車銷售和產量急劇下滑,自動駕駛技術的到來可能會被推遲一兩年。例如,福特汽車因在新冠疫情後重新考慮其策略,已將自動駕駛汽車的生產推遲至 2022 年。

機器人和 ADAS 汽車市場中的感測器趨勢

雷達感測器有望推動市場成長

- 汽車產業目前正在經歷以提高安全性、舒適性和娛樂性為重點的技術轉型,為雷達感測器應用提供了充足的機會。無人機、自動駕駛汽車和 ADAS 應用等新興感測器密集型應用進一步推動了對雷達感測器的需求。

- 2020 年 11 月,GroundProbe 發布 SSR-Agilis,擴展了其全面的邊坡穩定性雷達 (SSR) 產品線。 SSR-Agilis 是一種 3D 實孔徑雷達,可提供不易受污染的獨特測量方法。

- 自動駕駛汽車的出現推動了雷達感測器的廣泛應用。預計預測期內技術創新將推動汽車產業對雷達感測器的需求。

- 例如,2019年3月,歐盟委員會宣布修改其通用安全法規,將自動安全技術作為歐洲製造的汽車的強制性要求,以降低該地區的事故水準。嚴格的法規促使汽車供應商推出最新的基於雷達感測器的系統。這為市場創造了機會。

- 然而,儘管雷達感測器功能多樣,但初始成本較高,取決於感測器的類型、範圍和實施技術。任何雷達感測器的確切價格都有其優點和缺點。雷達感測器的成本取決於多種因素,包括所用感測器的類型、感測器覆蓋的範圍以及感測器支援的應用,所有這些都包含在總成本中。

預計北美將佔據主要佔有率

- 北美地區是採用 ADAS 車輛和自動運輸解決方案的先驅之一。根據德意志銀行預測,到2021年美國ADAS產量將達1,845萬台。

- 由於其更好的性能,LiDAR 被Google、Uber 和豐田等大公司所採用。同時,相對較低的成本也使特斯拉決定使用雷達感測器作為其自動駕駛汽車的主要感測器。公司不斷將替代感測技術融入車輛中,以提高其系統的有效性。

- 該地區的知名汽車製造商(超過 13 家主要汽車製造商)和提供雷達感測器的供應商(如博世、洛克希德馬丁等)有望成為技術創新的源泉,並預計在市場上佔據重要地位。根據美國汽車政策委員會的數據,在過去五年中,汽車業的出口額達到6,920億美元,光是汽車業就貢獻了該地區GDP的3%,有效促進了研究市場的成長。

- 然而,由於美國貿易戰,美國政府計劃將從中國進口的汽車和汽車零件的關稅提高至多25%。中國是繼墨西哥之後美國第二大零件出口國。美國是世界上最大的汽車市場之一,此類關稅可能會對汽車產業產生影響。根據世界貿易組織(WTO)統計,這些國家之間的衝突直接影響到全球3%的貿易和8%的汽車產業。預計這種情況將影響該地區機器人和 ADAS 車輛感測器的格局。

機器人和 ADAS 車輛感測器格局產業概覽

機器人和 ADAS 車輛感測器市場由許多主要參與者組成,包括英飛凌科技股份公司、大陸集團和德州儀器公司。市場正在快速變化,未來一年許多新技術可能會挑戰現有技術。然而,科技公司和汽車製造商正在擴大其市場影響力並加強研發力度,為駕駛者提供最佳的安全功能。

- 2020年1月,大陸集團宣布將在美國德克薩斯州新布朗費爾斯興建新工廠。新工廠的建設將擴大ADAS(高級駕駛輔助系統)雷達感測器的生產能力。該公司計劃未來三年將為該工廠投資約1億歐元。

- 2019年10月,英飛凌科技股份公司AURIX汽車微控制器系列再添新成員。 TC3A 有可能實現新的汽車 77GHz 雷達應用,例如用於 ADAS(高級駕駛輔助系統)和自動駕駛的高階角雷達系統。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 市場概況

- 產業價值鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 市場促進因素

- 工人安全意識增強,法規更嚴格

- 亞太地區主要新興國家工業領域的穩定成長和擴張計劃

- 市場問題

- 近期行業內新冠疫情的爆發和主要垂直行業支出的輕微下降可能會引起製造商的擔憂

- 輕型乘用車及無人駕駛汽車銷售統計(依自動化程度)

- 主要行業標準及法規

- 汽車感測器(雷達、攝影機、LiDAR)技術藍圖

- COVID-19 工業影響評估

第5章 市場區隔

- 類型

- LiDAR(機器人汽車與 ADAS 汽車)

- 雷達(機器人汽車與 ADAS 汽車)

- 相機模組(機器人與 ADAS 車輛)

- GNSS(機器人車輛)

- 慣性測量單元(機器人車輛)

- 地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

第6章 競爭格局

- 前三大汽車LiDAR供應商排名

- 前三大汽車影像感測器供應商排名

- 前三大汽車雷達供應商排名

- 公司簡介

- Infineon Technologies AG

- NXP Semiconductor NV

- Ouster Inc.

- Velodyne LiDAR Inc.

- Luminar Technologies Inc.

- Aurora Innovation Inc.(包括 Blackmore)

- Waymo LLC

- Robert Bosch GmbH

- Continental AG

- Valeo SA

- ON Semiconductor Corp

- Omnivision Technologies Inc.

- ST Microelectronics NV

- Texas Instruments Incorporated

第7章投資分析

第8章 市場機會與未來趨勢

The Sensor Landscape in Robotics and ADAS Vehicles Market is expected to register a CAGR of 28.7% during the forecast period.

Key Highlights

- Also, the increasing research and development activities to roll out fully autonomous cars require sensing technologies that are of great importance to enable 360-degree safety around the vehicle. Companies such as Google and Uber are already working on fully automated robotic cars.

- The Radar Sensor market has never been so dynamic, this market period of rapid technological innovation. New opportunities for radar are still emerging with, for instance, vital-sign driver monitoring systems, chassis-to-ground monitoring, and hands-free trunk opening. The industry is now envisioning radar imaging as a possibility. There's no doubt this technology will be critical in autonomous and robotic cars, ad aviation. For instance, in 2019, Velodyne launched Alphapuck at the Symposium event in Orlando. It is a lidar sensor specifically made for autonomous driving and advanced vehicle safety at highway speeds. It delivers a combination of long-range high resolution and wide field of view.

- Government mandates to install technology such as collision avoiding automatic brake systems are driving the market. Similarly, the emphasis of government to lower vehicle emissions will need cars and other commercial vehicles to be more fuel-efficient, resulting in the growth of pressure sensors. The Chinese government, for example, will introduce the new "6A" emission standard by 2020 to further lower vehicle emissions.

- With the recent outbreak of COVID 19, the Automotive sensor is witnessing a decline in growth due to major automotive manufacturing plants that have entirely stopped their production in response to lockdown being enforced by many countries across the world. Moreover, the self-driving vehicle has taken a hit, and the arrival of autonomous driving tech will be slowed, probably one to two years, because of the recent drastic downturn in auto sales and production due to COVID-19. For instance, Ford delayed its autonomous vehicle production until 2022 to rethink its strategy after the COVID-19 impact.

Sensor Landscape in Robotics and ADAS Vehicles Market Trends

Radar Sensor is Expected to Drive the Market Growth

- The automotive industry, which is presently undergoing a technology transition focusing on increasing safety, comfort, and entertainment, provides ample opportunities for the application of radar sensors. Emerging sensor-rich applications, such as drones, autonomous vehicles, and ADAS applications, are further accelerating the need for radar sensors.

- In November 2020, GroundProbe has extended its comprehensive Slope Stability Radar (SSR) product offering with the release of the SSR-Agilis. The SSR-Agilis is a 3D Real Aperture Radar that provides unique measurements that are less susceptible to contamination, crucial for safety-critical monitoring in high traffic work areas.

- With the advent of autonomous/self-driving cars, increasing the adoption of radar sensors can be witnessed. Over the forecast period, innovations are expected to drive the demand for radar sensors in the automotive industry.

- For instance, In March 2019, the European Commission announced a revision of the General Safety Regulations to make autonomous safety technologies a mandatory requirement for vehicles manufactured in Europe, in a bid to bring down accident levels in the region. Stringent regulations are pushing the automotive vendors to implement the latest radar sensor-based systems. This is creating an opportunity for the market.

- However, radar sensors have high initial costs with diversified functionality, and the cost varies based on the type, range, and technology being deployed for different sensors. Ultimately, the exact price of any radar sensor is unique. The cost for the radar sensor is dependent on a variety of factors, such as the type of sensor used, the range to which the sensor is adapted, and the applications supported by the sensor, which will be bundled into the total cost.

North America is Expected to Hold Major Share

- The North America region is one of the pioneers in adopting ADAS-enabled vehicles and self-driven transportation solutions. According to the Deutsche Bank, the US ADAS unit production volume is expected to reach 18.45 million by 2021.

- Owing to the better performance, prominent companies, like Google, Uber, and Toyota, are using LiDAR. At the same time, the relatively lower cost has persuaded Tesla to use radar sensors as the primary sensors in its self-driving cars. The companies are continuously trying to incorporate multiple alternative sensing technologies in a vehicle to enhance the effectiveness of the system.

- Prominent automakers (over 13 major auto manufacturers), and vendors offering radar sensors (Bosch, Lockheed Martin, among others) in the region are expected to emerge as a source for innovation and is estimated to hold a significant position in the market. According to the American Automotive Policy Council, over the past five years, the exports from the automotive sector were valued at USD 692 billion, and the automotive industry alone contributes to 3% of the region's GDP, which effectively contributes to the growth of the market studied.

- However, due to the trade war among the USA and China, the US government is planning to increase tariffs up to 25% on vehicles and car parts imported from China. China is the second biggest exporter of components to the United States, after Mexico. The United States is one of the largest auto markets in the world, and such tariffs will likely affect the automotive sector. As per the World Trade Organization, the conflict between these countries will directly affect 3% of the global trade and 8% of the automotive industry. Such situations are expected to have an impact on the sensor landscape in robotic and ADAS vehicles in the region.

Sensor Landscape in Robotics and ADAS Vehicles Industry Overview

The market for sensor landscape in robotic and ADAS vehicle is fragmented with the presence of many major players like Infineon Technologies AG, Continental AG, Texas Instrument Incorporated, etc. The market is transforming at a rapid pace, and in the coming year, many new technologies will come to challenge the existing one. However, technology companies and car manufacturers are expanding their market presence and increase their R&D efforts to provide the best safety features to the driver.

- In January 2020, Continental AG announced the construction of a new plant in the city of New Braunfels in the U.S state of Texas. The new building will help it expand its capacity for the production of radar sensors for Advanced Driver Assistance Systems (ADAS). The company plans to invest about €100 million in the plant over the next three years.

- In October 2019, Infineon Technologies AG added a new member to its automotive microcontroller family AURIX. TC3A may address new automotive 77 GHz radar applications, such as high-end corner radar systems for advanced driver assistance systems and automated driving.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Market Drivers

- 4.4.1 Rising awareness on worker safety & stringent regulations

- 4.4.2 Steady increase in industrial sector in key emerging countries in Asia-Pacific, coupled with expansion projects

- 4.5 Market Challenges

- 4.5.1 Recent outbreak of COVID-19 and marginal decline in spending in key verticals expected to pose a concern to manufacturers

- 4.6 Light Passenger Car and Robotic Vehicle Sales Statistics by Level of Autonomy ?

- 4.7 Key Industry Standards & Regulations

- 4.8 Technological Roadmap for Automotive Sensors (Radar, Camera & LiDAR)

- 4.9 Assessment of Impact of Covid-19 on the Industry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 LiDAR (Robotic Vehicles Vs. ADAS Vehicles)

- 5.1.2 Radar (Robotics Vehicles Vs. ADAS Vehicles)

- 5.1.3 Camera Modules (Robotics Vehicles Vs. ADAS Vehicles)

- 5.1.4 GNSS (Robotic Vehicles)

- 5.1.5 Inertial Measurement Units (Robotic Vehicles)

- 5.2 Geography

- 5.2.1 North America

- 5.2.2 Europe

- 5.2.3 Asia Pacific

- 5.2.4 Latin America

- 5.2.5 Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Ranking for Top 3 Automotive LiDAR Suppliers

- 6.2 Vendor Ranking for Top 3 Automotive Image Sensor Suppliers

- 6.3 Vendor Ranking for Top 3 Automotive Radar Supplier

- 6.4 Company Profiles

- 6.4.1 Infineon Technologies AG

- 6.4.2 NXP Semiconductor N.V.

- 6.4.3 Ouster Inc.

- 6.4.4 Velodyne LiDAR Inc.

- 6.4.5 Luminar Technologies Inc.

- 6.4.6 Aurora Innovation Inc. (Incl. Blackmore)

- 6.4.7 Waymo LLC

- 6.4.8 Robert Bosch GmbH

- 6.4.9 Continental AG

- 6.4.10 Valeo SA

- 6.4.11 ON Semiconductor Corp

- 6.4.12 Omnivision Technologies Inc.

- 6.4.13 ST Microelectronics NV

- 6.4.14 Texas Instruments Incorporated

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

2030 年自動駕駛汽車感測器市場預測:按感測器類型、車輛類型、自動化程度、測量範圍、感測器技術、應用和地區進行的全球分析

2030 年自動駕駛汽車感測器市場預測:按感測器類型、車輛類型、自動化程度、測量範圍、感測器技術、應用和地區進行的全球分析 自動駕駛感測器市場:按感測器類型、銷售管道- 2025-2030 年全球預測

自動駕駛感測器市場:按感測器類型、銷售管道- 2025-2030 年全球預測 自動駕駛汽車感測器的全球市場(2024-2028)

自動駕駛汽車感測器的全球市場(2024-2028) 全球自動駕駛汽車感測器市場規模研究,按感測器類型、車輛類型、自動化程度、應用和區域預測 2022-2032全球汽車踢感測器市場規模研究與預測,按類型(電容式踢感測器、雷達感測器等)按應用(OEM、售後市場)和區域分析,2023-2030 年

全球自動駕駛汽車感測器市場規模研究,按感測器類型、車輛類型、自動化程度、應用和區域預測 2022-2032全球汽車踢感測器市場規模研究與預測,按類型(電容式踢感測器、雷達感測器等)按應用(OEM、售後市場)和區域分析,2023-2030 年 汽車用踢感測器的全球市場:實際成果與預測(2018年~2029年)

汽車用踢感測器的全球市場:實際成果與預測(2018年~2029年)