|

市場調查報告書

商品編碼

1683445

東南亞國協乾混砂漿市場:市場佔有率分析、產業趨勢與成長預測(2025-2030 年)ASEAN Dry Mix Mortar - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

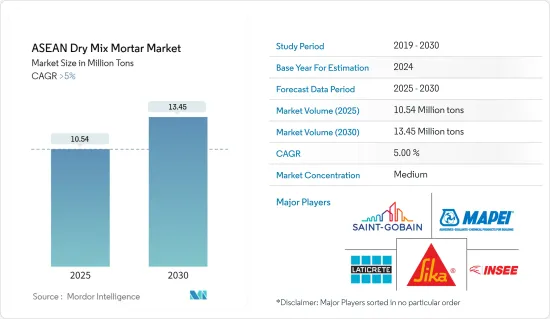

預計 2025 年東南亞國協乾混砂漿市場規模為 1,054 萬噸,到 2030 年將達到 1,345 萬噸,預測期內(2025-2030 年)的複合年成長率將超過 5%。

新冠肺炎疫情為東南亞國協帶來嚴重衝擊。疫情影響了印尼、泰國和菲律賓的建設活動,衝擊了乾混砂漿市場。然而,在新冠疫情爆發後,由於東協地區對住宅和基礎設施建設活動的需求增加,市場實現了顯著的成長率。

關鍵亮點

- 預計建築業的長期成本效益和東南亞國協建設活動的增加將推動市場成長。

- 然而,與傳統砂漿相比,鋪設乾混砂漿的成本預計會阻礙市場成長。

- 印尼工業混合乾混砂漿生產能力的不斷提高預計將為乾混砂漿市場創造機會。

- 由於建築終端用戶產業對乾混砂漿的需求不斷增加,預計印尼將佔據市場主導地位。預計在預測期內,其複合年成長率也將達到最高。

東南亞國協乾混砂漿市場趨勢

非住宅終端用戶市場佔據主導地位

- Drymix 產品具有卓越的技術性能,能夠滿足當前建築領域普遍存在的嚴格性能要求。此外,使用乾混砂漿產品經濟實惠,簡單的材料方法可以減少與結構長期完整性相關的潛在施工問題。

- 乾混砂漿含有精確混合的成分,只需要添加水就可以形成適當的砂漿。它由特殊添加劑組成,可以改善渲染的可操作性,有助於黏附背景並降低開裂的風險。它也可以用作裝飾面漆。

- 幾乎在每個建築應用中都會使用渲染來實現光滑或有意紋理的表面。預計預測期內泰國、菲律賓和越南等國家建設活動的增加將推動乾混砂漿在建築製造業的需求。

- 泰國是最大的旅遊基地之一,在購物中心、豪華酒店等方面投入了大量資金進行擴建和建設。芭堤雅萬豪侯爵酒店是泰國正在籌備的最大計劃,預計將於 2024 年開業,擁有超過 900 間客房。新建的萬豪侯爵酒店將成為兩個房地產開發項目的一部分,包括擁有 398 間客房的 JW 萬豪酒店和芭堤雅海灘度假村及水療中心。到 2027 年,萬豪可能會在泰國曼谷和芭達雅開設三個品牌的四家新酒店。萬豪在泰國的投資組合包括 45 家酒店和度假村,其中包括與 Asset World Corporation 合作的 9 家酒店。

- 同樣,菲律賓的基礎建設建設活動也在增加。 2022年12月,菲律賓與韓國簽署協議,將在2022年至2026年期間獲得高達30億美元的貸款,用於基礎設施和道路計劃。據外交部稱,新簽署的合約價值是2017年至2022年期間簽署合約價值的三倍。該合約表明該國計劃增加建築業的支出,從而對該國對乾混砂漿的需求產生積極影響。

- 此外,根據預算和管理部的數據,菲律賓公共基礎設施投資將從 2017 年佔 GDP 的 4.4% 增加到 2022 年的 GDP 的 6.3%。因此,預計公共基礎設施投資的增加將推動該國對乾混砂漿的需求。

- 因此,上述因素可能會影響預測期內對乾混砂漿的需求。

印尼佔據市場主導地位

- 印尼是東協地區最大的建築市場。印尼政府投入大量資金改善基礎設施和都市化,這推動了對住宅和商業房地產的需求。這推動了該國對乾混砂漿的需求。

- 印尼的高層建築數量顯著增加。印尼政府近日透露,將投資466兆印尼幣(約3005萬美元),在婆羅洲島建設新首都,建設工期為10年。此外,大多數住宅和房地產開發商都在印尼投資各種建築計劃,從而推動了對乾混砂漿的需求。

- 2022 年 5 月,公共工程和公共住宅部 (PUPR) 要求增加使用「源自國民內容的總公里數 (TKDN)」住宅產品。 PUPR 在印尼 19 個省份設有住宅供應實施中心 (P2P),在印尼 34 個省份設有住宅供應工作單位 (Satker),致力於開發國內住宅產品。

- 據印尼財政部稱,政府基礎設施投資預算預計將在 2024 年達到 4,300 億美元,而 2022 年為 3,658 億美元。因此,預計增加基礎設施投資將推動該國對乾混砂漿的需求。

- 作為這些努力的一部分,印尼-德國綠色基礎設施計劃得到達成。該計畫旨在建立為期五年的金融合作(FC)機制,提供高達 27.3 億美元的軟貸款和促銷貸款,以支持基礎設施計劃。預計這些因素將提振該國市場的需求,目前正在調查中。

- 因此,預計住宅和基礎設施建設活動的活性化將推動該國乾混砂漿市場的發展。

東南亞國協乾混砂漿產業概況

東南亞國協的乾混砂漿市場本質上是部分細分的。該市場的主要企業包括(不分先後順序)Sika AG、MAPEI SpA、LATICRETE International, Inc.、Saint Gobain 和 Siam City Cement Group。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 驅動程式

- 建築業的長期成本效益

- 東南亞國協建設活動增加

- 其他促進因素

- 限制因素

- 乾混砂漿與傳統砂漿的安裝成本對比

- 其他限制因素

- 價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場區隔(市場規模(以金額為準))

- 最終用戶產業

- 住宅

- 非住宅

- 商業

- 基礎設施

- 產業

- 應用

- 石膏

- 使成為

- 磁磚膠

- 水泥漿

- 防水泥漿

- 混凝土保護與維修

- 絕緣和飾面系統

- 其他用途(黏結砂漿、外牆石膏等)

- 地區

- 馬來西亞

- 印尼

- 泰國

- 新加坡

- 菲律賓

- 越南

- 緬甸

- 其他東南亞國協

第6章 競爭格局

- 併購、合資、合作、協議

- 市場佔有率(%)**/排名分析

- 主要企業策略

- 公司簡介

- 3M

- Ardex Group

- BASF SE

- Greco Asia Sdn Bhd

- Henkel AG & Co. KGaA

- HOLCIM

- Knauf Gips KG

- LATICRETE International, Inc.

- MAPEI SpA

- PT INDOCEMENT TUNGGAL PRAKARSA Tbk.

- Saint Gobain

- Siam City Cement Group

- Sika AG

第7章 市場機會與未來趨勢

- 提高印尼工業乾混砂漿產能

- 其他機會

The ASEAN Dry Mix Mortar Market size is estimated at 10.54 million tons in 2025, and is expected to reach 13.45 million tons by 2030, at a CAGR of greater than 5% during the forecast period (2025-2030).

The COVID-19 pandemic severely affected the ASEAN countries. The pandemic affected the construction activities in Indonesia, Thailand, and the Philippines, thereby affecting the market for dry mix mortar. However, post-COVID pandemic, the market registered a significant growth rate due to rising demand from residential and infrastructural construction activities in the ASEAN region.

Key Highlights

- The long-term cost-effectiveness in the construction industry and the increasing construction activities in ASEAN countries are expected to drive the market's growth.

- However, the laying cost of dry mix mortars, in comparison to conventional mortar, is expected to hinder the market growth.

- The increasing production capacity of industrially mixed dry mix mortar in Indonesia is expected to create opportunities for the dry mix mortar market.

- Indonesia is expected to dominate the market due to the rising demand for dry mix mortar in the construction end-user industry. It is also expected to register the highest CAGR during the forecast period.

ASEAN Dry Mix Mortar Market Trends

Non-residential End-user segment to Dominate the Market

- Dry mix products provide excellent technical properties to meet the stringent performance requirements that are common in the current construction scenario. Additionally, the use of dry mix mortar products is economical, as they reduce potential construction problems with the long-term integrity of structures with a simple materials approach.

- Dry mix mortar contains a precise blend of materials and only requires the addition of water to produce a suitable render. It comprises special additives that improve the workability of renders, help them bond to the background, and reduce the risk of cracking. They can also be used for decorative finishes.

- Rendering is done in almost all construction applications to achieve a smooth or deliberately textured surface. The increasing construction activities in countries like Thailand, the Philippines, and Vietnam are likely to drive the demand for dry mix mortar in manufacturing render during the forecast period.

- Thailand is one of the largest hubs for tourists and is witnessing considerable investments in the expansion and construction of malls, luxury hotels, etc. The Pattaya Marriott Marquis Hotel is the largest project in Thailand's pipeline, which may be in operation by 2024, with over 900 guest rooms. This new Marriott Marquis will be part of a dual-property development, which will also include the 398 rooms in the JW Marriott and the Pattaya Beach Resort & Spa. Marriott may add four new hotels under three of its brands across Bangkok and Pattaya in Thailand by 2027. Marriott's portfolio in Thailand includes 45 hotels and resorts, including nine properties with Asset World Corporation.

- Similarly, in the Philippines, the infrastructural construction activities are increasing. In December 2022, the Philippines signed an agreement with South Korea for a loan of up to USD 3 billion for infrastructure and road projects from 2022 to 2026. According to the Ministry of Foreign Affairs, the newly signed contract is worth three times the contract value from 2017 to 2022. This agreement showcases plans for an increment in spending in the construction sector, thereby positively influencing the demand for dry-mix mortar in the country.

- Furthermore, according to the Department of Budget and Management, public infrastructure investment increased from 4.4% of GDP in 2017 to 6.3% of GDP in the year 2022 in the Philippines. Thus, the increasing public infrastructure investments are expected to drive the demand for dry-mix mortar in the country.

- Hence, the factors mentioned above are likely to affect the demand for dry mix mortar during the forecast period.

Indonesia to Dominate the Market

- Indonesia is the largest construction market in the ASEAN region. The Indonesian government is spending more on better infrastructure and urbanization, as there is more demand for residential and commercial properties. It is driving the demand for dry mix mortar in the country.

- The number of high-rise buildings in Indonesia is growing significantly. Recently, the government of Indonesia revealed that the new capital city will be built on the island of Borneo with an investment of IDR 466 trillion (USD 30.05 million), and construction will take ten years. Further, most housing and real estate developers are investing in various construction projects in Indonesia, which is fueling the demand for dry-mix mortar.

- In May 2022, the Ministry of Public Works and Public Housing (PUPR) requested an increase in the usage of Domestic Component Level (TKDN) housing products. PUPR includes Housing Provision Implementation Centers (P2P) in 19 provinces and Housing Provision Work Units (Satker) spread across 34 provinces in Indonesia for the development of domestic housing products.

- According to the Ministry of Finance, Indonesia, the government budget for infrastructure investment is expected to reach USD 430 billion by 2024, compared to USD 365.8 billion invested in the year 2022. Thus, the growth in infrastructure investment is expected to drive the demand for dry-mix mortar in the country.

- The Indonesian-German Initiative for Green Infrastructure was agreed as part of these efforts. It aims to set up a five-year financial cooperation (FC) facility providing low-interest loans and promotional loans of up to USD 2.73 billion to support infrastructure projects. These factors will drive the demand for the currently studied market in the country.

- Thus, the rising residential and infrastructural construction activities are expected to drive the market for dry-mix mortar in the country.

ASEAN Dry Mix Mortar Industry Overview

The ASEAN dry mix mortar market is partially fragmented in nature. Some of the major players in the market include (not in any particular order) Sika AG, MAPEI S.p.A., LATICRETE International, Inc., Saint Gobain, and Siam City Cement Group., amongst others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Long-term Cost-effectiveness in the Construction Industry

- 4.1.2 Increasing Construction Activities in ASEAN Countries

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Laying Cost of Dry Mix Mortar, in Comparison to Conventional Mortar

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 End-user Industry

- 5.1.1 Residential

- 5.1.2 Non-residential

- 5.1.2.1 Commercial

- 5.1.2.2 Infrastructure

- 5.1.2.3 Industrial

- 5.2 Application

- 5.2.1 Plaster

- 5.2.2 Render

- 5.2.3 Tile Adhesive

- 5.2.4 Grout

- 5.2.5 Water Proofing Slurry

- 5.2.6 Concrete Protection and Renovation

- 5.2.7 Insulation and Finishing Systems

- 5.2.8 Other Applications (Bonding Mortar, External plaster, etc.)

- 5.3 Geography

- 5.3.1 Malaysia

- 5.3.2 Indonesia

- 5.3.3 Thailand

- 5.3.4 Singapore

- 5.3.5 Philippines

- 5.3.6 Vietnam

- 5.3.7 Myanmar

- 5.3.8 Rest of ASEAN Countries

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Ardex Group

- 6.4.3 BASF SE

- 6.4.4 Greco Asia Sdn Bhd

- 6.4.5 Henkel AG & Co. KGaA

- 6.4.6 HOLCIM

- 6.4.7 Knauf Gips KG

- 6.4.8 LATICRETE International, Inc.

- 6.4.9 MAPEI S.p.A.

- 6.4.10 PT INDOCEMENT TUNGGAL PRAKARSA Tbk.

- 6.4.11 Saint Gobain

- 6.4.12 Siam City Cement Group

- 6.4.13 Sika AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Production Capacity of Industrially Mixed Dry Mix Mortar in Indonesia

- 7.2 Other Opportunities

全球乾混砂漿市場:依產品種類、塑化劑種類、應用、黏結劑系統及地區劃分(至2032年)

全球乾混砂漿市場:依產品種類、塑化劑種類、應用、黏結劑系統及地區劃分(至2032年) 乾混砂漿市場按類型、應用、最終用途、包裝、通路和計劃類型分類-2025年至2032年全球預測乾混砂漿添加劑和化學品市場(按砂漿類型、添加劑類型、最終用途、形態和應用方法分類)—2025-2032年全球預測

乾混砂漿市場按類型、應用、最終用途、包裝、通路和計劃類型分類-2025年至2032年全球預測乾混砂漿添加劑和化學品市場(按砂漿類型、添加劑類型、最終用途、形態和應用方法分類)—2025-2032年全球預測 2025年乾混砂漿添加劑和化學品全球市場報告2025年全球工廠批量乾砂漿市場報告2025年全球乾混砂漿市場報告

2025年乾混砂漿添加劑和化學品全球市場報告2025年全球工廠批量乾砂漿市場報告2025年全球乾混砂漿市場報告 乾混砂漿添加劑和化學品市場規模、佔有率、成長分析(按添加劑類型、化學品類型、應用、最終用戶和地區)- 產業預測,2025 年至 2032 年

乾混砂漿添加劑和化學品市場規模、佔有率、成長分析(按添加劑類型、化學品類型、應用、最終用戶和地區)- 產業預測,2025 年至 2032 年 乾混砂漿添加劑和化學品:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)乾混砂漿:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)亞太地區乾混砂漿:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

乾混砂漿添加劑和化學品:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)乾混砂漿:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)亞太地區乾混砂漿:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)