|

市場調查報告書

商品編碼

1683460

光纖收發器:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Optical Transceiver - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

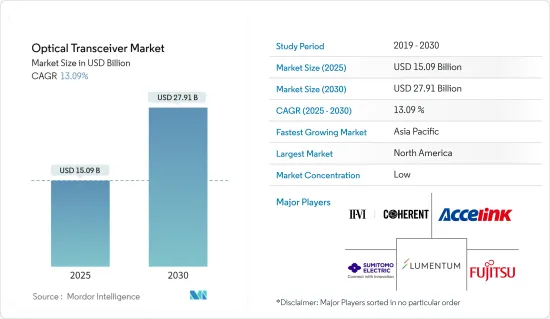

光收發器市場規模在 2025 年預計為 150.9 億美元,預計到 2030 年將達到 279.1 億美元,在市場估計和預測期(2025-2030 年)內複合年成長率為 13.09%。

光收發器,也稱為光纖收發器,是用於在光纖網路中發送和接收資料的互連組件。它由兩個主要部分組成:發射器和接收器。發射器將電訊號轉換為光訊號並透過光纖電纜傳輸。另一方面,接收器接收光訊號並將其轉換為電訊號。

主要亮點

- 光纖收發器可以實現遠距高速資料傳輸。它可以支援視訊串流、雲端運算和資料中心等高頻寬應用。光纖收發器能夠遠距傳輸資料,且訊號不會明顯劣化。它通常用於需要透過數公里光纖電纜傳輸資料的通訊和網路應用。

- 有幾個因素推動了電訊業對先進通訊的需求。這些因素包括對能源效率的需求、對提供先進連接的關注以及物聯網 (IoT) 和人工智慧 (AI) 等新技術的興起。通訊業者致力於為客戶提供先進的連接和更佳的性能。其中包括採用 5G、邊緣運算和改進的網路基礎設施等技術。這些進步使得通訊服務更快、更可靠。由於承載網的提前建設和升級,預計隨著5G技術的進步和基地台的部署,光纖網路設備的需求將會增加。

- 近年來,雲端基礎的服務的需求大幅成長。雲端處理使企業不再需要本地伺服器和硬體,從而降低了IT基礎設施成本。相反,企業可以按需獲取運算資源和服務,只需為其使用的部分付費。雲端服務還允許您根據需求擴大或縮小資源。由於其顯著的優勢,雲端服務的日益普及將對先進的通訊基礎設施產生巨大的需求,從而推動光收發器市場的發展。

- 光收發器對於資料中心等大容量資料傳輸網路至關重要。近年來,光收發器網路變得越來越複雜。現代網路所需的高資料速率推動了能夠以 1G 至 400G 速度傳輸資料的光收發器的發展。更高的資料速率需要更先進的設計和技術來確保可靠、高效的資料傳輸。

- COVID-19 疫情導致資料使用量增加。根據中國領先的創新網路娛樂服務平台貓眼娛樂發布的《新冠肺炎疫情對中國娛樂業影響》報告顯示,電影業受到疫情的嚴重打擊,但由於人們仍被困在家中,包括電視和串流媒體平台在內的線上娛樂市場卻蓬勃發展。這導致了市場的成長。

光收發器市場趨勢

資料中心成為光收發器成長最快的應用

- 作為現代化數位服務支柱的資料中心的激增需要高效可靠的連接解決方案。光纖收發器提供了這些資料中心內資料不間斷流動所需的速度、容量和擴充性。

- 資料中心已成為研究市場的關鍵促進因素。隨著資料和人工智慧、高效能運算 (HPC) 等技術的激增,快速、可靠且經濟高效地連接資料中心資產的需求呈指數級成長。吞吐量、延遲、操作簡單性、維護、智慧和安全性正在成為資料中心供應商的首要任務。

- 資料中心網路正迅速採用光纖技術。資料中心的光纖網路是透過組合多台光纖設備建構的。光纖收發器在這種大容量網路中發揮關鍵作用。如今,大多數現代資料中心網路都需要大容量的資料傳輸。

- Inphi 總部位於美國,正擴大瞄準資料中心應用,並透過利用矽光電和 DSP 技術的 400G資料中心互連光學模組等先進產品擴大其市場。據Cloudscene稱,截至2023年9月,美國共有5,375個資料中心,比世界上任何其他國家都多。另外有 522 人在德國,517 人在英國。

- 雲端應用、人工智慧和巨量資料的日益普及正在推動各個地區對資料中心建設的需求。隨著越來越多的組織將業務轉移到雲端,他們需要更先進的資料中心來支援其需求。例如,MetroEdge 於 2023 年 1 月與 Kroon Construction 和其他建設公司簽署了最終協議,以設計和建造資料中心設施。該計劃預計將在未來幾個月內獲得全面授權,並預計很快就會破土動工。

- 2023年11月,微軟宣布將在未來兩年內投資5億美元擴展在雲端處理和人工智慧基礎設施。公告提到了未來資料中心的位置,包括 L'Ancienne-Lorette、Donnacona、Saint-Augustin-de-Desmaures 和 Levis,並且即將開始建造。

北美佔有最大市場佔有率

- 北美是由於通訊環境的擴大和網際網路的普及而對光收發器市場的發展做出重大貢獻的國家之一。這些趨勢推動了對增強連接性的需求,從而增加了北美對光纖收發器的需求。根據 SaaS 解決方案公司和線上媒體監測公司 Meltwater 的數據,截至 2023 年 10 月,美國的網路普及率為 91.8%。

- 美國網際網路普及率高以及人工智慧、5G、物聯網和高效能運算等先進技術的採用,推動了對高資料傳輸速度的需求,從而推動了市場成長。

- 資料流量的增加產生了開發許多資料中心以支援企業和消費者產生的資料的額外需求。預計美國雲端處理服務和應用的使用也將成長,從而推動大型超大規模雲端為基礎的資料中心的發展。

- 谷歌(美國)、微軟(美國)、亞馬遜(美國)等主要資料中心公司的存在也為北美光收發器市場的成長做出了重大貢獻。谷歌和微軟等雲端服務供應商正在其資料中心部署高資料速率光收發器。

- 資料的快速成長以及人工智慧和高效能運算 (HPC) 等技術的擴展,推動了對快速、可靠且經濟高效地連接資料中心資產的巨大需求。吞吐量、延遲、易於操作和維護、智慧和安全性等因素正在成為該地區資料中心供應商的首要考慮因素。美國在5G部署方面的投資率較高,是5G市場領先的創新者和投資者之一。

光收發器市場概況

光收發器市場高度分散,主要參與者包括 II-VI Incorporated、Accelink Technologies、Lumentum Operations LLC、住友工業工業株式會社和富士通光學元件有限公司。市場參與者正在採取聯盟和收購等策略來加強其產品供應並獲得永續的競爭優勢。

- 2023 年 12 月,II-VI Incorporated 宣布推出適用於光纖網路的超緊湊 QSFP-DD 和 OSFP 外形尺寸的 800G ZR/ZR+ 收發器。相干公司的 800G ZR/ZR+ 收發器是世界上第一款可直接插入 IP 路由器的 QSFP-DD 和 OSFP 收發器插槽的數位連貫光學 (DCO)。

- 2023 年 10 月,Source 光電宣佈在蘇格蘭格拉斯哥舉行的 ECOC 2023 上推出用於 AI 集群連接的 800Gbps 短距離多模 (MMF) 收發器和主動電纜。這使得人工智慧資料中心基礎設施能夠在短距離光學可插拔模組和主動電纜應用方面呈指數級加速。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況

- 產業價值鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 新冠肺炎疫情及其他宏觀經濟因素對市場的影響

第5章 市場動態

- 市場促進因素

- 對先進通訊的需求日益增加

- 對雲端基礎服務的需求不斷增加

- 市場限制

- 網路複雜度不斷增加

第6章 市場細分

- 按通訊協定

- 乙太網路

- 光纖通道

- CWDM/DWDM

- FTTX

- 其他通訊協定

- 按資料速率

- 低於 10Gbps

- 10 Gbps~40 Gbps

- 100 Gbps

- 100Gbps 或更高

- 按應用

- 資料中心

- 通訊

- 按地區

- 北美洲

- 歐洲

- 亞洲

- 澳洲和紐西蘭

- 拉丁美洲

- 中東和非洲

第7章 競爭格局

- 公司簡介

- Coherent Corp.(II-VI Incorporated)

- Accelink Technologies

- Lumentum Operations LLC(Lumentum Holdings)

- Sumitomo Electric Industries Ltd

- Fujitsu Optical Components Limited(Fujitsu Ltd)

- Smiths Interconnect(Reflex Photonics Inc.)

- Source Photonics(Redview Capital)

- Huawei Technologies Co. Ltd

- Broadcom Inc.

- HUBER+SUHNER Cube Optics

第8章投資分析

第9章 市場機會與未來趨勢

The Optical Transceiver Market size is estimated at USD 15.09 billion in 2025, and is expected to reach USD 27.91 billion by 2030, at a CAGR of 13.09% during the forecast period (2025-2030).

An optical transceiver, also known as a fiber optic transceiver, is an interconnect component used to transmit and receive data in a fiber-optic network. It consists of two main parts: a transmitter and a receiver. The transmitter converts electrical signals into light signals, which are transmitted through fiber optic cables. The receiver, on the other hand, receives light signals and converts them back into electrical signals.

Key Highlights

- Optical transceivers enable high-speed data transmission over long distances. They can support high bandwidth applications like video streaming, cloud computing, and data centers. They can transmit data over long distances without significant signal degradation. They are commonly used in telecommunications and networking applications that require data transmission over kilometers of fiber optic cables.

- Due to several factors, the telecom industry is experiencing an increasing need for advanced communication. These factors include the demand for energy efficiency, the focus on delivering advanced connectivity, and the rise of new technologies such as the Internet of Things (IoT) and artificial intelligence (AI). Telecom companies strive to deliver advanced connectivity and higher performance to their customers. This includes deploying technologies like 5G, edge computing, and improved network infrastructure. These advancements enable faster and more reliable communication services. The advanced development and upgrade of the bearer network is anticipated to drive the demand for optical communication network equipment to increase as 5G technology progresses and base stations are deployed.

- Cloud-based services have experienced a significant increase in demand in recent years. Cloud computing allows businesses to reduce their IT infrastructure costs by eliminating the need for on-premises servers and hardware. Instead, companies can access computing resources and services on demand, paying only for what they use. Cloud services also offer the ability to scale resources up or down based on demand. The increasing adoption of cloud services owing to their significant advantages would create massive demand for advanced communication infrastructure, thereby driving the optical transceivers market.

- Optical transceivers, such as data centers, are critical in high-capacity data transmission networks. In recent years, there has been an increase in network complexity in optical transceivers. The demand for high data rates in modern networks has led to the development of optical transceivers capable of transmitting data at speeds ranging from 1G to 400 G. The higher data rates require more sophisticated designs and technologies to ensure reliable and efficient data transmission.

- The outbreak of COVID-19 increased the usage of data. According to a report on the impact of the COVID-19 pandemic on China's entertainment industry by Maoyan Entertainment, a leading platform providing innovative Internet-empowered entertainment services in China, the movie industry was severely hit by the pandemic, whereas the online entertainment market, including TV and streaming platforms, were booming as people were confined to their homes. This has led to the growth of the market.

Optical Transceiver Market Trends

Data Centers to the Fastest Growing Application for Optical Transceivers

- The proliferation of data centers, which serve as the backbone of modern digital services, requires efficient and reliable connectivity solutions. Optical transceivers offer the speed, capacity, and scalability required to maintain the uninterrupted data flow within these data centers.

- Data centers are emerging as significant drivers in the market studied. With the proliferation of data and technologies, like AI and high-performance computing (HPC), the need to connect data center assets quickly, reliably, and cost-effectively is growing significantly. Throughput, latency, simplified operations, maintenance, intelligence, and security are becoming significant priorities for data center vendors.

- Data center networks are rapidly adopting fiber optics technology. A fiber-based network for data centers is built by combining many fiber optic devices. In these high-capacity networks, optical transceivers play a significant role. The majority of modern data center networks currently necessitate high-capacity data transmission.

- US-based Inphi is increasingly targeting data center applications and extending its marketplace with advanced products, including 400G data center interconnect optical modules, which leverage their silicon photonics and DSP technologies. According to Cloudscene, as of September 2023, there were 5,375 data centers in the United States, the most of any country worldwide. A further 522 were in Germany, while 517 were in the United Kingdom.

- The growing adoption of cloud applications, AI, and big data drives the demand for data center construction across various regions. As more organizations shift their operations to the cloud, they require more advanced data centers to support their needs. For instance, in January 2023, Metro Edge finalized agreements with Clune Construction and other construction firms to design and build the data center facility. The project is expected to have full entitlements within the next few months and break ground shortly after.

- In November 2023, Microsoft announced it would invest USD 500 million in expanding its cloud computing and AI infrastructure in Quebec over the next two years. The announcement references future data center locations in L'Ancienne-Lorette, Donnacona, Saint-Augustin-de-Desmaures, and Levis, with construction starting soon.

North America Holds Largest Market Share

- North America is one of the significant contributors to the optical transceiver market's development due to the growing communication landscape and the massive internet penetration. These trends demand improved connectivity, increasing the demand for optical transceivers in North America. According to Meltwater, a software-as-a-service solution company and an online media monitoring company, as of October 2023, the internet penetration rate as of October 2023 in the United States was 91.8%.

- The high adoption of the Internet and advanced technologies like AI, 5G, IoT, and high-performance computing in the United States is driving the need for a high data transmission rate, which drives the market's growth.

- Increasing data traffic has created additional demand for developing many data centers that support data generated by businesses and consumers. The use of cloud-computing services and applications is also expected to grow in the United States, leading to the development of large hyperscale cloud-based data centers.

- The presence of some of the key data center companies like Google (US), Microsoft (US), and Amazon (US) has also contributed significantly to the growth of the optical transceiver market in North America. Cloud service providers like Google and Microsoft are implementing high-data-rate optical transceivers in their data centers.

- With the proliferation of data and expansion of technologies like AI and high-performance computing (HPC), the need to connect data center assets quickly, reliably, and cost-effectively is growing significantly. Factors such as throughput, latency, simplified operations and maintenance, intelligence, and security are becoming major priorities for regional data center vendors. The United States is one of the major innovators and investors in the 5G market, owing to a high investment rate for 5G deployment.

Optical Transceiver Market Overview

The optical transceiver market is highly fragmented, with the presence of major players like Coherent Corp. (II-VI Incorporated), Accelink Technologies, Lumentum Operations LLC (Lumentum Holdings), Sumitomo Electric Industries Ltd, and Fujitsu Optical Components Limited (Fujitsu Ltd). Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- December 2023: II-VI Incorporated introduced its 800G ZR/ZR+ transceiver in ultracompact QSFP-DD and OSFP form factors for optical communications networks. The 800G ZR/ZR+ transceivers from Coherent are the world's first digital coherent optics (DCO) that can plug directly into QSFP-DD and OSFP transceiver slots on IP routers.

- October 2023: Source Photonics announced the availability of 800 Gbps short-reach multimode (MMF) transceivers and active cables for AI cluster connectivity at ECOC 2023 in Glasgow, Scotland, that enables AI data center infrastructure to achieve dramatically higher speeds for short-reach optical pluggable modules and active cable applications.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Need for Advanced Communication

- 5.1.2 Increasing Demand for Cloud-based Services

- 5.2 Market Restraints

- 5.2.1 Increase in Network Complexity

6 MARKET SEGMENTATION

- 6.1 By Protocol

- 6.1.1 Ethernet

- 6.1.2 Fiber Channel

- 6.1.3 CWDM/DWDM

- 6.1.4 FTTX

- 6.1.5 Other Protocols

- 6.2 By Data Rate

- 6.2.1 Less than 10 Gbps

- 6.2.2 10 Gbps to 40 Gbps

- 6.2.3 100 Gbps

- 6.2.4 Greater than 100 Gbps

- 6.3 By Application

- 6.3.1 Data Center

- 6.3.2 Telecommunication

- 6.4 By Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia

- 6.4.4 Australia and New Zealand

- 6.4.5 Latin America

- 6.4.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Coherent Corp. (II-VI Incorporated)

- 7.1.2 Accelink Technologies

- 7.1.3 Lumentum Operations LLC (Lumentum Holdings)

- 7.1.4 Sumitomo Electric Industries Ltd

- 7.1.5 Fujitsu Optical Components Limited (Fujitsu Ltd)

- 7.1.6 Smiths Interconnect (Reflex Photonics Inc.)

- 7.1.7 Source Photonics (Redview Capital)

- 7.1.8 Huawei Technologies Co. Ltd

- 7.1.9 Broadcom Inc.

- 7.1.10 HUBER+SUHNER Cube Optics

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

全球光纖收發器市場研究報告 - 產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年

全球光纖收發器市場研究報告 - 產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年 2025 年全球光收發器市場報告

2025 年全球光收發器市場報告 2025-2029 年全球光收發器市場

2025-2029 年全球光收發器市場 2025-2033 年光收發器市場(按外形尺寸、光纖類型、資料速率、連接器類型、應用和地區分類)2024-2032 年日本光收發器市場報告(按外形尺寸、光纖類型、資料速率、連接器類型、應用和地區分類)光收發器市場:按形式、資料速率、光纖類型、距離、波長、連接器、應用分類 - 2025-2030 年全球預測第三方光收發器市場:按資料速率、外形規格和應用分類 - 2025-2030 年全球預測光收發器市場 - 全球產業規模、佔有率、趨勢、機會和預測,按協議、數據速率、應用、地區和競爭細分,2019-2029F

2025-2033 年光收發器市場(按外形尺寸、光纖類型、資料速率、連接器類型、應用和地區分類)2024-2032 年日本光收發器市場報告(按外形尺寸、光纖類型、資料速率、連接器類型、應用和地區分類)光收發器市場:按形式、資料速率、光纖類型、距離、波長、連接器、應用分類 - 2025-2030 年全球預測第三方光收發器市場:按資料速率、外形規格和應用分類 - 2025-2030 年全球預測光收發器市場 - 全球產業規模、佔有率、趨勢、機會和預測,按協議、數據速率、應用、地區和競爭細分,2019-2029F 光收發器市場規模、佔有率、成長分析,按外形規格、按資料速率、按光纖類型、按距離、按地區 - 行業預測,2024-2031 年2024 年多模光收發器全球市場報告

光收發器市場規模、佔有率、成長分析,按外形規格、按資料速率、按光纖類型、按距離、按地區 - 行業預測,2024-2031 年2024 年多模光收發器全球市場報告