|

市場調查報告書

商品編碼

1684041

汽車MLCC:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)Automotive MLCC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

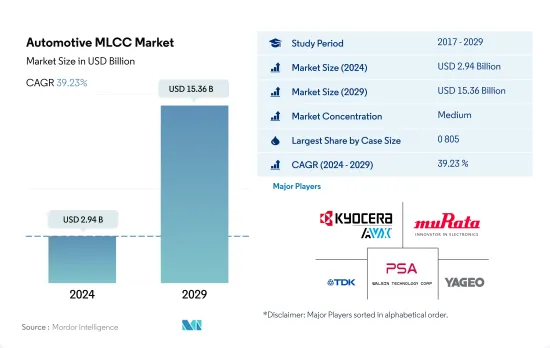

預計 2024 年汽車 MLCC 市場規模將達到 29.4 億美元,到 2029 年將達到 153.6 億美元,預測期內(2024-2029 年)的複合年成長率為 39.23%。

了解MLCC在汽車發展中的多方面作用正在推動對MLCC的需求

- 在不斷發展的汽車產業中,MLCC 的作用已超越了簡單的電子元件。這些微型動力源是現代汽車系統的核心,執行從配電和噪音抑製到訊號調節和電壓調節等一系列功能。

- 0603 MLCC體積小巧,但不可或缺。這些電容器在轉向更小、更節能的設計過程中發揮著至關重要的作用。隨著汽車技術的進步,對精簡解決方案的需求推動了 0 603 領域的存在。

- 0805 電容器在市場上佔有重要地位,尤其是隨著電動車 (EV) 成為主流。電動車的迅速普及凸顯了有效電力分配和控制的必要性,並強調了 0 805 段的重要性。隨著電動車重新定義汽車格局,這些電容器成為性能和效率的推動者。

- 1 206 電容器在尺寸和多功能性之間取得了良好的平衡,使其成為各種汽車應用的絕佳選擇。隨著汽車產業擁抱技術進步,1210 細分市場的重要性變得顯而易見。

- 「其他」部分涵蓋了滿足特殊汽車要求的一系列電容值。從新技術到獨特的應用,這個多樣化領域展示了 MLCC 滿足汽車不同需求的適應性。

揭示MLCC在亞太、歐洲和北美的影響力

- 亞太、歐洲和北美正在推動汽車產業的轉型。對技術進步、永續性和智慧運輸解決方案的追求凸顯了積層陶瓷電容(MLCC) 在支援汽車發展方面發揮的關鍵作用。隨著各地區朝著創新和高效的未來邁進,對高品質 MLCC 的需求持續成長,鞏固了其在汽車價值鏈中的重要性。

- 亞太地區是汽車創新的中心,其特點是技術進步迅速、消費者需求不斷成長。該地區是中國、日本和韓國等主要汽車中心的所在地,在電動車 (EV) 普及、聯網汽車和自動駕駛方面處於領先地位。

- 歐洲汽車工業是創新、永續性和嚴格的環境法規的代名詞。該地區致力於減少碳排放,轉向更清潔的移動解決方案,重塑汽車格局。隨著電動和混合動力汽車越來越受歡迎,對電源管理、噪音抑制和電壓調節用 MLCC 的需求也日益增加。

- 北美汽車產業的特點是追求智慧運輸解決方案和先進技術。隨著北美消費者對改善駕駛體驗和尖端功能的需求,電動車、資訊娛樂系統和 ADAS 等應用程式對 MLCC 的需求正在上升。該地區充滿活力的汽車格局是 MLCC 市場擴張的主要驅動力。

汽車MLCC市場的全球趨勢

加氫站基礎建設持續推動銷售成長

- 燃料電池電動車(FCEV)利用燃料電池將儲存的氫能轉化為電能,其推進機制與電動車類似。與傳統內燃機動力來源的汽車相比,FCEV 不會排放有害廢氣。

- 預計2022年燃料電池電動車的出貨量將達到4.3萬輛,2029年將達到7.1萬輛。隨著風能、太陽能等可再生能源對氫氣生產過程的貢獻越來越大,對節能型FCEV的需求將大幅增加。

- 隨著對低排放氣體汽車的需求不斷增加,更嚴格的二氧化碳排放法規正在實施,快速加油等優勢使得 FCEV 得到更廣泛的採用。為了促進燃料電池電動車的發展,多個政府機構和商業實體正在共同投資燃料電池技術的進步和加氫基礎設施的建設。根據國際能源總署的數據,到 2021年終,全球將有約 730 個加氫站 (HRS),為約 51,600 輛 FCEV 供應燃料。這意味著從2020年起,全球FCEV保有量將增加近50%,HRS數量將增加35%。這些因素有助於 FCEV 未來的高速成長。

嚴格的政府法規推動電動車的普及

- MLCC 具有耐高溫和易於表面黏著技術的外形規格,已成為電動車電子設備和子系統的首選組件。一輛電動車大約使用 8,000 到 10,000 個 MLCC。電動車中的 MLCC 通常用於電池管理系統 (BMS)、車載充電器 (OBC) 和 DC/DC 轉換器。除了滿足這些電動汽車子系統所需的通用規格並能夠在電動車內部的惡劣環境中可靠運作外,零件製造商還必須符合 IATF16949 資格和 AEC-Q200 標準。

- 預計2022年電動車出貨量將達1,640萬輛,2029年將增加至2,552萬輛。為減少溫室氣體排放、應對氣候變化,多個國家實施了嚴格的環境法規。因此,汽車製造商面臨越來越大的壓力,需要生產更多的電動車並減少對石化燃料的依賴。消費者的環保意識也越來越強,尋求傳統汽油動力汽車的永續替代品。

- 新冠疫情和俄羅斯在烏克蘭的戰爭擾亂了全球供應鏈,汽車產業受到嚴重影響。但從長遠來看,電動車市場在世界某些地區的銷售量正在成長。同時,政府和企業努力支持部署公共充電基礎設施,為電動車銷售的進一步成長奠定了堅實的基礎。全球公共充電樁數量已接近180萬個,2021年安裝量將接近50萬個,其中三分之一為快速充電樁,超過2017年安裝的公共充電樁總數。

汽車MLCC產業概況

汽車MLCC市場適度整合,前五大企業佔60.58%。此市場的主要企業有:京瓷AVX元件株式會社(京瓷株式會社)、村田製作所、TDK株式會社、華新科技株式會社和國巨株式會社(依字母順序排列)。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章執行摘要和主要發現

第2章 報告要約

第3章 引言

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 汽車銷售

- 全球BEV(純電動車)產量

- 全球電動車銷量

- 全球FCEV(燃料電池電動車)產量

- 全球HEV(混合動力電動車)產量

- 全球重型商用車銷售

- 全球ICEV(內燃機汽車)產量

- 全球輕型商用車銷售

- 非電動車的全球銷量

- 全球插電式混合動力汽車(PHEV)產量

- 全球乘用車銷量

- 全球摩托車銷售

- 法律規範

- 價值鍊和通路分析

第5章市場區隔

- 車輛類型

- 重型商用車

- 輕型商用車

- 搭乘用車

- 摩托車

- 燃料類型

- 電動車

- 非電動車

- 推進類型

- 純電動車

- FCEV-燃料電池電動車

- HEV-混合動力電動車

- ICEV-內燃機汽車

- PHEV - 插電式油電混合動力電動車

- 其他

- 組件類型

- ADAS

- 資訊娛樂

- 動力傳動系統

- 安全系統

- 其他

- 錶殼尺寸

- 0 603

- 0 805

- 1 206

- 1 210

- 1 812

- 其他

- 電壓

- 50V~200V

- 小於50V

- 200V以上

- 電容

- 10μF 至 1,000μF

- 小於10μF

- 1,000μF 以上

- 介電類型

- 1級

- 2級

- 地區

- 亞太地區

- 歐洲

- 北美洲

- 世界其他地區

第6章 競爭格局

- 關鍵策略趨勢

- 市場佔有率分析

- 商業狀況

- 公司簡介

- Kyocera AVX Components Corporation(Kyocera Corporation)

- Maruwa Co ltd

- Murata Manufacturing Co., Ltd

- Nippon Chemi-Con Corporation

- Samsung Electro-Mechanics

- Samwha Capacitor Group

- Taiyo Yuden Co., Ltd

- TDK Corporation

- Vishay Intertechnology Inc.

- Walsin Technology Corporation

- Wurth Elektronik GmbH & Co. KG

- Yageo Corporation

第 7 章 CEO 的關鍵策略問題CEO 的關鍵策略問題

第 8 章 附錄

- 世界概況

- 概述

- 五力分析框架

- 全球價值鏈分析

- 市場動態(DRO)

- 資訊來源及延伸閱讀

- 圖片列表

- 關鍵見解

- 資料包

- 詞彙表

簡介目錄

Product Code: 50001984

The Automotive MLCC Market size is estimated at 2.94 billion USD in 2024, and is expected to reach 15.36 billion USD by 2029, growing at a CAGR of 39.23% during the forecast period (2024-2029).

Unveiling the multifaceted role of MLCCs in the automotive evolution is driving MLCC demand

- In the ever-evolving landscape of the automotive industry, the role of MLCCs has moved beyond mere electronic components. These miniature powerhouses are the cornerstone of modern vehicular systems, orchestrating a symphony of functions ranging from power distribution and noise suppression to signal conditioning and voltage regulation.

- The 0 603 MLCCs are compact yet indispensable contributors. These capacitors play a pivotal role in shifting toward compact and energy-efficient designs. With advancements in automotive technologies, the demand for streamlined solutions has elevated the prominence of the 0 603 segment.

- The 0 805 capacitors occupy a significant position in the market, particularly as electric vehicles (EVs) become mainstream. The surge in EV adoption emphasizes the need for effective power distribution and control, underscoring the relevance of the 0 805 segment. As EVs redefine the automotive landscape, these capacitors act as enablers of performance and efficiency.

- The 1 206 capacitors represent a balance between size and versatility, making them a preferred choice for diverse automotive applications. As the automotive industry embraces technological advancements, the importance of the 1 210 segment becomes evident.

- The 'others' segment encompasses an array of capacitance values that cater to specialized automotive requirements. From emerging technologies to unique applications, this diverse segment exemplifies the adaptable nature of MLCCs in meeting distinct automotive needs.

Unveiling the impact of MLCCs in Asia-Pacific, Europe, and North America

- Asia-Pacific, Europe, and North America are driving transformative changes in the automotive industry. Their pursuit of technological advancements, sustainability, and smart mobility solutions underscores the crucial role of multi-layer ceramic capacitors (MLCCs) in supporting the evolution of vehicles. As each region propels toward a future of innovation and efficiency, the demand for high-quality MLCCs continues to grow, cementing their significance in the automotive value chain.

- Asia-Pacific stands as an epicenter of automotive innovation characterized by rapid technological advancements and growing consumer demand. With major automotive hubs like China, Japan, and South Korea, this region is at the forefront of electric vehicle (EV) adoption, connected cars, and autonomous driving.

- Europe's automotive industry is synonymous with innovation, sustainability, and stringent environmental regulations. The region's commitment to reducing carbon emissions and transitioning toward cleaner mobility solutions is reshaping the automotive landscape. As electric and hybrid vehicles gain traction, the demand for MLCCs for power management, noise suppression, and voltage regulation is escalating.

- North America's automotive sector is characterized by its pursuit of smart mobility solutions and advanced technologies. As North American consumers seek enhanced driving experiences and cutting-edge features, the demand for MLCCs in applications like EVs, infotainment systems, and ADAS is on the rise. The region's dynamic automotive landscape positions it as a key driver of the MLCC market's expansion.

Global Automotive MLCC Market Trends

Infrastructure improvement for hydrogen stations continues to increase sales

- Fuel cell electric vehicles (FCEVs) use hydrogen energy stored as fuel, which is then converted into electricity by the fuel cell and has a propulsion mechanism similar to that of an electric vehicle. Compared to vehicles powered by conventional internal combustion engines, FCEVs do not emit any harmful exhaust emissions.

- Fuel cell electric vehicle shipments accounted for 0.043 million units in 2022, and these are expected to reach 0.071 million units in 2029. As renewable energies like wind and solar contribute increasingly to the hydrogen manufacturing process, there will be a huge increase in the demand for energy-efficient FCEVs.

- As the demand for low-emission vehicles rises, stricter carbon emission standards are being implemented, and more emphasis is being placed on the adoption of FCEVs due to benefits like quick refueling. To encourage the development of FCEVs, several government and commercial organizations are collaborating and investing in advancing fuel cell technology and the development of hydrogen refueling infrastructure. According to the IEA, at the end of 2021, there were about 730 hydrogen refueling stations (HRSs) globally providing fuel for about 51,600 FCEVs. This represents an increase of almost 50% in the global stock of FCEVs and a 35% increase in the number of HRSs from 2020. These factors contribute to the high growth of FCEVs in the future.

Stringent government regulations are increasing the penetration of electric vehicles

- MLCCs have emerged as a perfect component for EV electronics and subsystems, offering high-temperature resistance and an easy surface-mount form factor. Approximately 8,000-10,000 MLCCs are used in an electric vehicle. MLCCs in electric vehicles are commonly used in battery management systems (BMS), onboard chargers (OBC), and DC/DC converters. In addition to meeting the general specifications required for these EV subsystems and having the ability to function reliably in harsh environments inside an EV, component manufacturers should also be IATF 16949-certified and compliant with AEC-Q200.

- Electric vehicle shipments accounted for 16.4 million units in 2022, and it is expected to rise to 25.52 million units in 2029. Several countries have implemented strict environmental regulations to reduce greenhouse gas emissions and combat climate change. As a result, automakers are under increasing pressure to produce more electric vehicles and reduce their reliance on fossil fuels. Consumers are becoming more environmentally conscious and are looking for more sustainable alternatives to traditional gasoline-powered vehicles.

- The COVID-19 pandemic and Russia's war in Ukraine disrupted global supply chains, and the automotive industry has been heavily impacted. However, in the longer term, the EV market is witnessing sales growth in some regions of the world as government and corporate efforts to support the deployment of publicly available charging infrastructure are providing a solid basis for further increase in EV sales. Publicly accessible chargers worldwide approached 1.8 million, with nearly 500,000 chargers installed in 2021, of which a third were fast chargers, which accounted for more than the total number of public chargers installed in 2017.

Automotive MLCC Industry Overview

The Automotive MLCC Market is moderately consolidated, with the top five companies occupying 60.58%. The major players in this market are Kyocera AVX Components Corporation (Kyocera Corporation), Murata Manufacturing Co., Ltd, TDK Corporation, Walsin Technology Corporation and Yageo Corporation (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Automotive Sales

- 4.1.1 Global BEV (Battery Electric Vehicle) Production

- 4.1.2 Global Electric Vehicles Sales

- 4.1.3 Global FCEV (Fuel Cell Electric Vehicle) Production

- 4.1.4 Global HEV (Hybrid Electric Vehicle) Production

- 4.1.5 Global Heavy Commercial Vehicles Sales

- 4.1.6 Global ICEV (Internal Combustion Engine Vehicle) Production

- 4.1.7 Global Light Commercial Vehicles Sales

- 4.1.8 Global Non-Electric Vehicle Sales

- 4.1.9 Global PHEV (Plug-in Hybrid Electric Vehicle) Production

- 4.1.10 Global Passenger Vehicles Sales

- 4.1.11 Global Two-Wheeler Sales

- 4.2 Regulatory Framework

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 Vehicle Type

- 5.1.1 Heavy Commercial Vehicle

- 5.1.2 Light Commercial Vehicle

- 5.1.3 Passenger Vehicle

- 5.1.4 Two-Wheeler

- 5.2 Fuel Type

- 5.2.1 Electric Vehicle

- 5.2.2 Non-Electric Vehicle

- 5.3 Propulsion Type

- 5.3.1 BEV - Battery Electric Vehicle

- 5.3.2 FCEV - Fuel Cell Electric Vehicle

- 5.3.3 HEV - Hybrid Electric Vehicle

- 5.3.4 ICEV - Internal Combustion Engine Vehicle

- 5.3.5 PHEV - Plug-in Hybrid Electric Vehicle

- 5.3.6 Others

- 5.4 Component Type

- 5.4.1 ADAS

- 5.4.2 Infotainment

- 5.4.3 Powertrain

- 5.4.4 Safety System

- 5.4.5 Others

- 5.5 Case Size

- 5.5.1 0 603

- 5.5.2 0 805

- 5.5.3 1 206

- 5.5.4 1 210

- 5.5.5 1 812

- 5.5.6 Others

- 5.6 Voltage

- 5.6.1 50V to 200V

- 5.6.2 Less than 50V

- 5.6.3 More than 200V

- 5.7 Capacitance

- 5.7.1 10 µF to 1000 µF

- 5.7.2 Less than 10 µF

- 5.7.3 More than 1000µF

- 5.8 Dielectric Type

- 5.8.1 Class 1

- 5.8.2 Class 2

- 5.9 Region

- 5.9.1 Asia-Pacific

- 5.9.2 Europe

- 5.9.3 North America

- 5.9.4 Rest of the World

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Kyocera AVX Components Corporation (Kyocera Corporation)

- 6.4.2 Maruwa Co ltd

- 6.4.3 Murata Manufacturing Co., Ltd

- 6.4.4 Nippon Chemi-Con Corporation

- 6.4.5 Samsung Electro-Mechanics

- 6.4.6 Samwha Capacitor Group

- 6.4.7 Taiyo Yuden Co., Ltd

- 6.4.8 TDK Corporation

- 6.4.9 Vishay Intertechnology Inc.

- 6.4.10 Walsin Technology Corporation

- 6.4.11 Wurth Elektronik GmbH & Co. KG

- 6.4.12 Yageo Corporation

7 KEY STRATEGIC QUESTIONS FOR MLCC CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms