|

市場調查報告書

商品編碼

1685686

農業中的螯合化合物:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)Agricultural Chelates - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

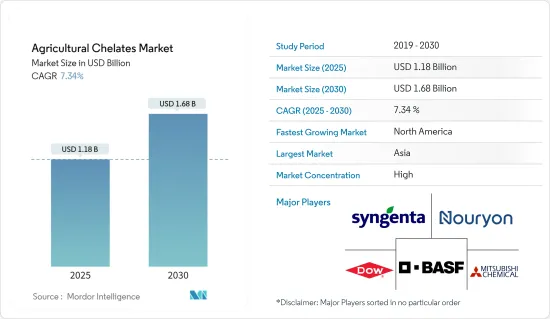

預計 2025 年農業螯合物市場規模為 11.8 億美元,到 2030 年將達到 16.8 億美元,預測期內(2025-2030 年)的複合年成長率為 7.34%。

主要亮點

- 氣候變遷、可耕地減少以及世界人口迅速成長引發了人們對糧食安全的擔憂。美國農業部(USDA)進行的2022年農業普查顯示,美國的農場數量已降至200萬個以下。具體來說,2022年美國有190萬個農場,比2017年人口普查數據下降了7%。此外,人口普查也強調,到 2022 年,美國農地總面積將減少 2.2%,至 8.8 億英畝。鑑於這些發展情況,必須透過適當的農業投入來提高生產力。因此,農業中使用螯合劑來提高作物產量以滿足世界糧食需求的現象顯著增加。螯合劑可增強植物對營養素的吸收,使某些營養素更容易被利用。這可以改善植物的生長和發育,最終提高作物的產量和品質。

- 獨立實驗室的分析表明,英國數千個土壤樣本中,小麥作物缺氮 10%,缺乏磷 25%。螯合是一種保護微量營養素免受溶液和土壤中不良反應影響的機制。透過提高鐵、銅、錳和鋅等微量營養素的生物利用度,螯合肥料在提高經濟作物生產的生產力和盈利方面發揮著至關重要的作用。特別是在 pH 值高於 6.5 和/或微量營養素壓力較低的土壤中,螯合肥料與標準微量營養素相比,表現出更高的提高商業性產量的能力。

- 隨著永續農業的發展勢頭強勁以及人們對合成螯合劑對環境影響的認知不斷提高,尋找生物分解性替代品的趨勢明顯。鑑於這種情況,公司正在策略性地定位自己,以滿足日益成長的需求並增加其在市場上的佔有率。

農業螯合物市場趨勢

農業領域對 EDTA 的青睞日益成長

- 乙二胺四乙酸 (EDTA) 已成為農業中的主要合成螯合劑,廣泛應用於土壤和葉面營養。如果土壤 pH 值約為 6.0,則 EDTA 作為肥料在戶外施用是有效的。這種多功能性確保了EDTA在市場上的主導地位。

- EDTA 螯合物比傳統礦物質更受歡迎,因為它們能有效地將鐵 (Fe)、錳 (Mn)、銅 (Cu) 和鋅 (Zn) 等必需的微量元素從土壤直接轉移到植物根部。印度土壤科學研究所強調了普遍存在的微量營養素缺乏的令人擔憂的趨勢。印度土壤的平均缺鋅水準為43.0%、鐵為12.1%、銅為5.4%、錳為5.6%、硼為18.3%。令人擔憂的是,酸性土壤缺乏鋅和磷酸鹽,半乾旱地區缺乏鋅和鐵,這表明未來的種植系統面臨潛在挑戰。鋅是一種重要的微量營養素,對於維持植物激素平衡和促進生長至關重要。有機螯合鋅源,尤其是 Zn-EDTA(含 12% 的鋅),通常被認為優於無機替代品。例如,當將Zn-EDTA螯合物肥料施用於玉米、豆類等作物時,農民只需要使用傳統硫酸鋅(ZnSO4)的一半。此外,與目前市面上許多其他商業農業螯合物相比,EDTA螯合物具有價格更低、更容易取得的優勢。

- 市場主要企業正在展示各種適合農業用途的 EDTA 產品。例如,科迪華 (Corteva) 以 Versenol 和 Crop Max 品牌提供 EDTA 螯合劑,這兩種產品在農業產業都很受歡迎。 EDTA除了作為營養物以外,還具有對受到汞、鎘、鉛等重金屬污染的土壤進行解毒的能力,因此其市場正在不斷擴大。然而,EDTA 也並非沒有挑戰。與許多合成藥物一樣,EDTA 面臨高成本、生物分解性有限和潛在交叉污染風險等挑戰。這些挑戰可能會阻礙該領域的成長軌跡。

亞太地區佔市場主導地位

- 在亞太地區,中國、印度、日本和澳洲是農業螯合劑市場需求的主導者。根據澳洲政府統計,鹼性土壤覆蓋了澳洲約24%的土地面積,尤其是在西部地區,pH值在4到8.5之間。因此,由於微量元素缺乏阻礙了農業生產力,澳洲對螯合劑的需求正在增加。

- 中國是世界上人口最多的國家,同時也擁有最廣泛的農業設施。人口迅速成長和糧食需求不斷增加迫使中國農民提高作物產量。然而,中國各地普遍存在著石灰性土壤微量營養素缺乏的問題。為了應對這些挑戰,中國正在進行一項全面的土壤普查,該普查由總部位於北京的非營利環保組織主導,計劃於 2025 年完成。從此次土壤調查中獲得的資訊可以凸顯土壤的缺陷,並促進螯合劑在中國的銷售。

- 微量營養素缺乏影響了包括泰國在內的稻米生產國的生產力。一項獨立研究指出關鍵微量營養素(鐵、錳、鋅、銅)至關重要,並表明這些營養素的缺乏會導致水稻產量減少 24.12% 至 46.46%。然而,隨著 DTPA 的應用,添加這些微量營養素可以顯著提高產量。

農業螯合物產業概況

全球農業螯合物市場正在整合,BASF公司、三菱化學、先正達公司、陶氏公司和諾力昂化學控股公司等主要參與者佔了相當大的佔有率。這些公司的巨大市場佔有率歸功於其高度多樣化的產品系列以及在審查期間進行的收購和合作。這些公司也專注於研發和產品創新,以擴大其地理影響力。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 市場概覽

- 市場促進因素

- 對農作物更高產量的需求

- 螯合物在微量營養素毒性的應用。

- 土壤微量營養素缺乏

- 市場限制

- 生物分解性螯合物產品供應不足

- 加強合成螯合劑使用的限制

- 波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭強度

第5章市場區隔

- 類型

- 合成

- EDTA

- EDDHA

- DTPA

- IDHA

- 其他合成類型

- 有機的

- 硫酸蘋果酸

- 胺基酸

- 七葡萄糖酸鹽

- 其他有機類型

- 合成

- 應用

- 土壤

- 葉面噴布

- 受精

- 其他用途

- 作物類型

- 糧食

- 豆類和油籽

- 經濟作物

- 水果和蔬菜

- 草坪和觀賞植物

- 地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 北美其他地區

- 歐洲

- 西班牙

- 英國

- 法國

- 德國

- 俄羅斯

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 其他亞太地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 非洲

- 南非

- 其他非洲國家

- 北美洲

第6章競爭格局

- 最受歡迎的策略

- 市場佔有率分析

- 公司簡介

- Nouryon Chemicals Holding BV

- Shandong Iro Chelating Chemical Co. Ltd

- Ava Chemicals Private Limited

- Protex International

- Innospec Inc.

- Syngenta Ag

- Mitsubishi Group(Mitsubishi Chemical Corporation)

- Dow Inc

第7章 市場機會與未來趨勢

The Agricultural Chelates Market size is estimated at USD 1.18 billion in 2025, and is expected to reach USD 1.68 billion by 2030, at a CAGR of 7.34% during the forecast period (2025-2030).

Key Highlights

- Concerns over food security are rising due to changing climate conditions, diminishing arable land, and a swiftly expanding global population. The 2022 Census of Agriculture, conducted by the United States Department of Agriculture (USDA), revealed that the number of farms in the United States (U.S.) has dipped below 2 million. Specifically, in 2022, the U.S. counted 1.9 Million farms, marking a 7% decrease from the figures in the 2017 Census. Additionally, the Census highlighted a 2.2% reduction in total U.S. farmland, bringing it down to 880 million acres in 2022. Given these developments, boosting productivity through appropriate agricultural inputs has become imperative. Consequently, there's been a notable surge in the adoption of chelating agents in agriculture, to enhance crop yields to satisfy global food requirements. Chelating agents facilitate plants' uptake of nutrients, making certain nutrients more accessible. This leads to improved plant growth and development, ultimately enhancing crop yield and quality.

- Independent laboratory analyses highlight troubling trends, includes wheat crops in the UK are experiencing a 10% nitrogen deficiency and a 25% phosphorus deficiency, as evidenced by thousands of soil samples. Chelation serves as a protective mechanism, shielding micronutrients from unwanted reactions in both solutions and soil. By boosting the bioavailability of micronutrients like Fe, Cu, Mn, and Zn, chelated fertilizers play a pivotal role in enhancing the productivity and profitability of commercial crop production. Notably, in soils with a pH exceeding 6.5 or those under low-micronutrient stress, chelated fertilizers have demonstrated a superior capacity to boost commercial yields compared to standard micronutrients.

- With the rising momentum of sustainable farming and growing awareness about the environmental repercussions of synthetic chelating agents, there's a marked pivot towards exploring biodegradable alternatives. In light of this, companies are strategically positioning themselves to meet this evolving demand, thereby strengthening their market presence.

Agricultural Chelates Market Trends

Increasing Preference for EDTA in Agriculture

- Ethylenediaminetetraacetic acid (EDTA) has emerged as the premier synthetic chelating agent in agriculture, widely employed for both soil and foliar nutrient applications. At soil pH levels around 6.0, EDTA demonstrates its efficacy in open-field fertigation. This adaptability plays a pivotal role in cementing EDTA's leading market position.

- EDTA chelates are preferred over conventional inorganic sources due to their superior efficiency in transferring essential trace elements such as iron (Fe), manganese (Mn), copper (Cu), and zinc (Zn)-from the soil directly to plant roots. The Indian Institute of Soil Science highlights a concerning trend of micronutrient deficiencies are widespread, with average deficiencies in Indian soils being 43.0% for Zinc, 12.1% for Iron, 5.4% for Copper, 5.6% for Manganese, and 18.3% for Boron. Alarmingly, the combined deficiency of Zn and B in acidic soils, and Zn and Fe in semi-arid regions, signals potential challenges for future cropping systems. Zinc, a crucial micronutrient, is essential for maintaining plant hormone balance and fostering growth. Organic chelated zinc sources, particularly Zn-EDTA (which contains 12% Zn), are frequently regarded as superior to their inorganic alternatives. For instance, when treating crops like corn and beans, the application of Zn-EDTA chelate fertilizer allows farmers to use only half the quantity compared to traditional zinc sulfate (ZnSO4). Additionally, EDTA chelates not only come at a lower price point but also boast greater accessibility than numerous other commercial agricultural chelates available today.

- Prominent players in the market showcase a wide array of EDTA products tailored for agricultural use. Corteva, for instance, offers its EDTA chelating agents under the brand names Versenol and Crop Max, both of which are in high demand within the agricultural community. Beyond its nutrient application, EDTA's ability to detoxify soils contaminated with heavy metals like mercury, cadmium, and lead further fuels its market expansion. However, EDTA isn't without its challenges. Like many synthetic agents, it grapples with issues such as high costs, limited biodegradability, and potential secondary pollution risks. These challenges could hinder the segment's growth trajectory.

Asia-Pacific Dominates the Market

- In the Asia-Pacific region, China, India, Japan, and Australia lead in market demand for agricultural chelates. According to the Australian Government, alkaline soils account for about 24% of Australia's land, particularly in the western regions, where pH levels range from 4 to 8.5. As a result, Australia is experiencing an increasing demand for chelating agents, driven by trace element deficiencies that impede agricultural productivity growth.

- China, home to the world's largest population, also hosts some of the most expansive agricultural facilities. With its population surging and food demand rising, Chinese farmers are under pressure to achieve higher crop yields. Yet, various regions in China grapple with micronutrient deficiencies in their calcareous soils. To address these challenges, China is undertaking a comprehensive soil census, led by a nonprofit environmental organization from Beijing, with an anticipated completion in 2025. Insights from this soil survey are poised to illuminate soil deficiencies, potentially boosting chelate sales in the nation.

- Micronutrient deficiencies are currently undermining productivity in rice-growing nations, notably Thailand. An independent study identified key micronutrients (Fe, Mn, Zn, and Cu) as pivotal, revealing their deficiency could slash rice grain yields by a staggering 24.12%-46.46%. However, with the application of DTPA, these yields can be significantly bolstered through the addition of these micronutrients.

Agricultural Chelates Industry Overview

The global agricultural chelates market is consolidated, with the major players in the market including BASF SE, Mitsubishi Chemical Corporation, Syngenta Ag, Dow Inc, Nouryon Chemicals Holding B.V, etc holding a significant share of the market. The significant market share of these players can be attributed to a highly diversified product portfolio and acquisitions and partnerships during the review period. These players also focus on R&D and product innovations to widen their geographical presence.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Demand For Higher Crop Yields

- 4.2.2 Application of Chelates in Micronutrient Intoxication

- 4.2.3 Micronutrient Deficiency In Soil

- 4.3 Market Restraints

- 4.3.1 Poor Product Offering in Biodegradable Chelates

- 4.3.2 Rising Regulation on Use of Synthetic Chelating Agents

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitutes

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Synthetic

- 5.1.1.1 EDTA

- 5.1.1.2 EDDHA

- 5.1.1.3 DTPA

- 5.1.1.4 IDHA

- 5.1.1.5 Other Synthetic Types

- 5.1.2 Organic

- 5.1.2.1 LingoSulphates

- 5.1.2.2 Aminoacids

- 5.1.2.3 Heptagluconates

- 5.1.2.4 Other Organic Types

- 5.1.1 Synthetic

- 5.2 Application

- 5.2.1 Soil

- 5.2.2 Foliar

- 5.2.3 Fertigation

- 5.2.4 Other Applications

- 5.3 Crop Type

- 5.3.1 Grains and Cereals

- 5.3.2 Pulses and Oilseeds

- 5.3.3 Commercial Crops

- 5.3.4 Fruits and Vegetables

- 5.3.5 Turf and Ornamentals

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Spain

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Germany

- 5.4.2.5 Russia

- 5.4.2.6 Italy

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Africa

- 5.4.5.1 South Africa

- 5.4.5.2 Rest of Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Nouryon Chemicals Holding B.V

- 6.3.2 Shandong Iro Chelating Chemical Co. Ltd

- 6.3.3 Ava Chemicals Private Limited

- 6.3.4 Protex International

- 6.3.5 Innospec Inc.

- 6.3.6 Syngenta Ag

- 6.3.7 Mitsubishi Group (Mitsubishi Chemical Corporation)

- 6.3.8 Dow Inc

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

2025 年全球農業螯合物市場報告

2025 年全球農業螯合物市場報告 生物分解性分解螯合劑市場報告:趨勢、預測和競爭分析(至 2031 年)

生物分解性分解螯合劑市場報告:趨勢、預測和競爭分析(至 2031 年) 鋅甲硫胺酸螯合物市場規模、佔有率和成長分析(按產品類型、形式、牲畜、應用和地區)- 2025-2032 年行業預測

鋅甲硫胺酸螯合物市場規模、佔有率和成長分析(按產品類型、形式、牲畜、應用和地區)- 2025-2032 年行業預測 綠色螯合物市場報告:2031 年趨勢、預測與競爭分析

綠色螯合物市場報告:2031 年趨勢、預測與競爭分析 螯合劑市場報告(按類型(氨基多羧酸、葡萄糖酸鈉、有機膦酸鹽等)、應用和地區分類)2025 年至 2033 年

螯合劑市場報告(按類型(氨基多羧酸、葡萄糖酸鈉、有機膦酸鹽等)、應用和地區分類)2025 年至 2033 年 全球螯合劑市場:產業分析、規模、佔有率、成長、趨勢和預測(2025-2032 年)

全球螯合劑市場:產業分析、規模、佔有率、成長、趨勢和預測(2025-2032 年) 農業螯合化合物市場規模、佔有率、成長分析、按類型、按作物類型、按微量營養素類型、按應用、按最終用途、按地區 - 行業預測,2024-2031 年

農業螯合化合物市場規模、佔有率、成長分析、按類型、按作物類型、按微量營養素類型、按應用、按最終用途、按地區 - 行業預測,2024-2031 年 螯合劑的全球市場(2018年~2034年)

螯合劑的全球市場(2018年~2034年) 檸檬醛產品市場:依產品類型、最終用途、通路分類 - 2025-2030 年全球預測

檸檬醛產品市場:依產品類型、最終用途、通路分類 - 2025-2030 年全球預測 螯合劑市場:按類型、產品類型、應用分類 - 2025-2030 年全球預測

螯合劑市場:按類型、產品類型、應用分類 - 2025-2030 年全球預測