|

市場調查報告書

商品編碼

1685759

滑石粉 -市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Talc - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

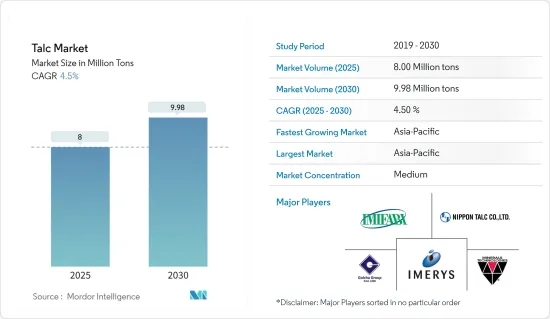

滑石市場規模預計在2025年為800萬噸,預計在2030年達到998萬噸,預測期間(2025-2030年)的複合年成長率為4.5%。

過去幾年,新冠疫情影響了全球市場,迫使陶瓷製造商、紙漿和造紙製造商以及油漆和塗料製造商停工,從而降低了 2022 年對滑石粉的需求。不過,預計這種情況將會恢復,所研究市場的成長軌跡將在預測期的後半段恢復。

主要亮點

- 短期內,工業和船舶被覆劑需求的成長將推動滑石粉的需求。

- 然而,對滑石粉化妝品的健康擔憂預計會阻礙市場成長。

- 航太工業對熱塑性塑膠的需求不斷成長,這可能會成為未來的一個機會。

- 由於中國塑膠市場的崛起以及印度等國家擁有白色滑石蘊藏量,亞太地區在全球滑石市場佔據主導地位。

滑石市場趨勢

塑膠和橡膠產業佔據市場主導地位

- 滑石粉為聚丙烯提供了多種益處,包括增加剛性和改善尺寸穩定性。

- 它主要用作塑膠的填充材,並在生產過程中充當吸收劑和抗結塊劑。板狀滑石顆粒可增加聚乙烯、聚丙烯、尼龍、乙烯基和聚酯等產品的硬度。它還可以提高耐熱性並減少收縮。

- 滑石是化學、塑膠、橡膠等各行業最常使用的添加劑、改質劑和填充物之一。可明顯提高塑膠製品的拉伸強度、衝擊性能、耐熱性、抗蠕變性、撕裂強度等。

- 據歐洲塑膠協會稱,歐洲約三分之二的塑膠需求集中在五個國家:德國25.4%、義大利14.3%、法國9.7%、英國7.6%和西班牙7.5%。

- 在歐洲塑膠市場營運的領先公司正在轉向戰略市場開發以擴大其地理影響力。例如,2022 年 6 月,林德工程公司被三井商船集團旗下的 Slovnaft 選中。 Lines Group 對斯洛伐克的一家聚丙烯工廠進行維修。這將使聚丙烯年產能提高 18%,達到約 30 萬噸,並將倉儲設施從 45 個筒倉擴大到 61 個筒倉。

- 2022年12月,埃克森美孚公司開始在路易斯安那州首府巴吞魯日運作新的聚丙烯製造工廠。該廠的聚丙烯產能為 45 萬噸/年。此外,總部位於美國的台塑集團正在美國德克薩斯州州 Point Comfort 建造一座新的聚丙烯生產工廠。工程預計2024年完工,年產10萬噸α烯烴,用於生產高密度聚苯乙烯(HDPE)。其中 63,000 噸 α 烯烴將供公司使用,剩餘 37,000 噸則銷往國際。

- 由於電子商務行業需要包裝,印尼的塑膠使用量正在增加。豐益集團、Mayora 和 Indofood 等快速消費品公司正在印尼建立綜合包裝生產部門。埃克森美孚也在投資印尼的塑膠產業。 2022年11月,埃克森美孚與PT Indomobil Prima Energi(IPE)簽署合作備忘錄,將在印尼大規模應用先進的塑膠回收技術。

- 因此,行業內各公司開展的此類擴建計劃可能會在預測期內推動市場成長。

亞太地區佔市場主導地位

- 由於中國、印度和日本等國家的需求不斷成長,亞太地區佔據了全球市場佔有率的主導地位。

- 中國是亞太地區滑石粉的主要消費國之一。該國在陶瓷、食品飲料、紙漿和造紙等眾多行業中使用滑石。根據工業信部資料顯示,2023年第一季,全國飲料產量4,435萬噸,年增6%。

- 中國也是世界主要陶瓷生產國和消費國之一。它是世界上最大的瓷磚生產商之一,年產量約84.7億平方公尺瓷磚。國內和出口市場的激烈競爭迫使陶瓷製造商改善生產過程和產品品質。

- 印度是少數擁有蘊藏量的國家之一。滑石礦床遍布全國各地。所生產的白色滑石大部分供國內消費。

- 在印度,滑石的大部分商業生產都發生在拉賈斯坦邦。該國兩家最大的滑石粉生產商——Golcha Group 和 Golcha Associated——總部位於拉賈斯坦邦齋浦爾,為化妝品和聚合物行業供應優質滑石粉。

- 印度塑膠工業市場是該國最重要的經濟部門之一。根據印度品牌股權基金會的數據,2022 年 4 月至 9 月塑膠出口總值為 63.8 億美元。

- 此外,中國擁有龐大的塑膠市場,需要大量的滑石供應才能正常運作。中國滑石分佈於15個省區,其中遼寧、山東、廣西、江西、青海等省區最為集中,佔全國蘊藏量的90%以上。

- 預計所有這些因素都將在預測期內推動該地區對滑石的需求。

滑石行業概況

滑石市場本質上處於中等整合狀態,有多家參與者在全球和區域層面開展業務。市場的主要企業(不分先後順序)包括 ELEMENTIS PLC、Imerys、IMI Fabi SpA、Nippon Talc 和 Minerals Technologies Inc.

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 驅動程式

- 塑膠需求不斷成長

- 工業和船舶被覆劑需求不斷成長

- 限制因素

- 化妝品中的健康問題

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場區隔

- 訂金

- 滑石綠泥石

- 碳酸滑石

- 最終用戶產業

- 陶瓷製品

- 食品和飲料

- 畫

- 個人護理

- 塑膠和橡膠

- 紙漿和造紙

- 其他最終用戶產業

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭格局

- 併購、合資、合作與協議

- 市場佔有率(%)**/排名分析

- 主要企業策略

- 公司簡介

- AKJ MinChem

- ANAND TALC

- Chanda Minerals

- ELEMENTIS PLC

- Eurominerals Gmbh

- Golcha Group

- Imerys

- IMI Fabi SpA

- LITHOS Industrial Minerals GmbH

- Magris Performance Materials

- Minerals Technologies Inc.

- Nippon Talc Co. Ltd

第7章 市場機會與未來趨勢

- 航太工業對熱塑性塑膠的需求不斷增加

The Talc Market size is estimated at 8.00 million tons in 2025, and is expected to reach 9.98 million tons by 2030, at a CAGR of 4.5% during the forecast period (2025-2030).

The COVID-19 pandemic affected the market in the past years on a global scale and forced ceramic makers, pulp and paper manufacturers, and paints and coatings manufacturers to shut down their operations, lowering the demand for talc in 2022. However, the condition is expected to recover, which will restore the growth trajectory of the market studied during the latter half of the forecast period.

Key Highlights

- Over the short term, increasing demand for industrial and marine coatings is driving the demand for talc, as it provides benefits such as corrosion protection, solvent reduction, and good adhesion.

- On the flip side, health issues pertaining to talc-based cosmetic products are expected to hamper the market's growth.

- The growing demand for thermoplastics in the aerospace industry is likely to act as an opportunity in the future.

- Asia-Pacific dominated the talc market globally, owing to the rising plastics market in China and the presence of white talc reserves in countries like India.

Talc Market Trends

Plastic and Rubber Industry to Dominate the Market

- Talc imparts a variety of benefits to polypropylene, such as higher stiffness and improved dimensional stability.

- It is mainly used as a filler in plastics and acts as an absorbent and anti-caking agent during production. The plate shape of talc particles increases the hardness of products such as polyethylene, polypropylene, nylon, vinyl, and polyester. It also increases heat resistance and reduces shrinkage.

- Talc is the most commonly used additive, modifier, or filler in a variety of industries, including chemicals, plastics, and rubber. It can significantly improve the tensile strength of plastic products, impact properties, heat resistance, creep resistance, tear resistance, etc.

- According to Plastics Europe, about two-thirds of Europe's plastics demand is concentrated in five countries, including 25.4% in Germany, 14.3% in Italy, 9.7% in France, 7.6% in the United Kingdom, and 7.5% in Spain, according to Plastics Europe.

- The major companies operating in the European plastic market are more inclined towards strategic business development to expand their geographical presence. For instance, in June 2022, Linde Engineering was selected by Slovnaft - a member company of MOL Group, to conduct a revamp of a polypropylene plant in Slovakia. This revamped the plant capacity of polypropylene per year by 18% to around 300 kilotons, and the storage facility expanded from 45 to 61 silos.

- In December 2022, Exxon Mobil Corporation started a new manufacturing facility for polypropylene in Baton Rouge, the capital of Louisiana. This plant can produce 450,000 MT/year of polypropylene. Further, Formosa Plastics Corporation, in the United States, is constructing a new manufacturing facility for polypropylene in Point Comfort, Texas in the United States. Upon completion in 2024, this plant will produce 100,000 tonnes of Alpha olefins to manufacture high-density polyethylene (HDPE). 63,000 tonnes of Alpha olefins would be used by the company while the remaining 37,000 tonnes would be sold internationally.

- The usage of plastic in Indonesia is increasing since the e-commerce industry requires packaging. FMCG companies, including Wilmar Group, Mayora, and Indofood, have established integrated packaging production units in Indonesia. Exxon Mobil is also investing in the Indonesian plastic industry. It signed a memorandum of understanding with PT Indomobil Prima Energi (IPE), in November 2022, regarding the application of advanced plastic recycling technology on a large scale in Indonesia.

- Hence, such expansion projects carried out by various companies in the industry are likely to drive the market growth during the forecast period.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region dominated the global market share with the growing demand from the countries such as China, India, and Japan.

- China is one of the major consumers of talc in the Asia-Pacific region. The country uses talc in a wide range of industries, such as ceramics, food and beverage, pulp and paper, and others. According to the data from the Ministry of Industry and Information Technology, the country witnessed increase in its beverage production by 6 percent year-on-year, reaching 44.35 million tons during Q1 2023.

- Also, China is the leading producer and consumer of ceramics worldwide. It is one of the largest producers of ceramic tiles in the world and has produced around 8.47 billion square meters of ceramic tiles. The fierce competition in the domestic and export markets forces ceramic producers to improve their production process and product quality in the region.

- India is one of the few countries with white talc reserves. The deposits of talc are found throughout the country. Most of the white talc produced is consumed in the country itself.

- In India, most of the commercial production of talc comes from Rajasthan. The two leading talc producers in the country (Golcha Group and Golcha Associated) are based in Jaipur, Rajasthan, catering cosmetics and polymer industry with talc of superior grades.

- The Indian plastic industry market is one of the country's most important economic sectors. According to the India Brand Equity Foundation, the total value of plastics exported between April and September 2022 was USD 6.38 billion.

- Furthermore, China has a huge plastics market that requires a high supply of talc to function. In China, talc is found in 15 provinces, with Liaoning, Shandong, Guangxi, Jiangxi, and Qinghai as the prominent areas that account for more than 90% of the total reserves.

- All these factors, in turn, are expected to drive the demand for talc in the region during the forecast period.

Talc Industry Overview

The talc market is moderately consolidated in nature, with several companies operating on both global and regional levels. Some of the major players in the market (not in any particular order) include ELEMENTIS PLC, Imerys, IMI Fabi SpA, Nippon Talc Co. Ltd, and Minerals Technologies Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand for Plastics

- 4.1.2 Increasing Demand for Industrial and Marine Coatings

- 4.2 Restraints

- 4.2.1 Health Issues in Cosmetic Products

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Deposit

- 5.1.1 Talc Chlorite

- 5.1.2 Talc Carbonate

- 5.2 End-user Industry

- 5.2.1 Ceramic

- 5.2.2 Food and Beverage

- 5.2.3 Paints and Coatings

- 5.2.4 Personal Care

- 5.2.5 Plastics and Rubber

- 5.2.6 Pulp and Paper

- 5.2.7 Other End-user Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 AKJ MinChem

- 6.4.2 ANAND TALC

- 6.4.3 Chanda Minerals

- 6.4.4 ELEMENTIS PLC

- 6.4.5 Eurominerals Gmbh

- 6.4.6 Golcha Group

- 6.4.7 Imerys

- 6.4.8 IMI Fabi SpA

- 6.4.9 LITHOS Industrial Minerals GmbH

- 6.4.10 Magris Performance Materials

- 6.4.11 Minerals Technologies Inc.

- 6.4.12 Nippon Talc Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Demand for Thermoplastics in the Aerospace Industry

2025年滑石全球市場報告葉蠟石市場 - 全球產業規模、佔有率、趨勢、機會和預測,按應用細分(陶瓷、耐火材料和鑄造、填料、其他)、按地區和競爭,2020-2030 年預測

2025年滑石全球市場報告葉蠟石市場 - 全球產業規模、佔有率、趨勢、機會和預測,按應用細分(陶瓷、耐火材料和鑄造、填料、其他)、按地區和競爭,2020-2030 年預測 葉蠟石市場規模、佔有率、趨勢分析報告:按應用、地區、細分市場、預測,2025-2030 年

葉蠟石市場規模、佔有率、趨勢分析報告:按應用、地區、細分市場、預測,2025-2030 年 滑石粉市場:按沉澱物、最終用戶產業分類 - 2025-2030 年全球預測

滑石粉市場:按沉澱物、最終用戶產業分類 - 2025-2030 年全球預測 全球滑石粉市場規模:按滑石粉沉積類型、應用、最終用戶產業、地區、範圍和預測2024-2032 年按存款類型、形式、最終用途行業和地區分類的滑石粉市場報告

全球滑石粉市場規模:按滑石粉沉積類型、應用、最終用戶產業、地區、範圍和預測2024-2032 年按存款類型、形式、最終用途行業和地區分類的滑石粉市場報告 北美滑石市場預測至 2030 年 - 區域分析 - 按礦床類型(綠泥石滑石和碳酸滑石)和最終用途行業(塑膠、紙漿和造紙、陶瓷、油漆和塗料、橡膠、藥品、食品等)

北美滑石市場預測至 2030 年 - 區域分析 - 按礦床類型(綠泥石滑石和碳酸滑石)和最終用途行業(塑膠、紙漿和造紙、陶瓷、油漆和塗料、橡膠、藥品、食品等) 2030 年亞太地區滑石市場預測 - 區域分析 - 按礦床類型(綠泥石滑石和碳酸滑石)和最終用途行業(塑膠、紙漿和造紙、陶瓷、油漆和塗料、橡膠、藥品、食品等)

2030 年亞太地區滑石市場預測 - 區域分析 - 按礦床類型(綠泥石滑石和碳酸滑石)和最終用途行業(塑膠、紙漿和造紙、陶瓷、油漆和塗料、橡膠、藥品、食品等) 歐洲滑石粉市場預測至 2030 年 - 區域分析 - 按礦床類型(綠泥石滑石粉和碳酸滑石粉)和最終用途行業(塑膠、紙漿和造紙、陶瓷、油漆和塗料、橡膠、藥品、食品等)

歐洲滑石粉市場預測至 2030 年 - 區域分析 - 按礦床類型(綠泥石滑石粉和碳酸滑石粉)和最終用途行業(塑膠、紙漿和造紙、陶瓷、油漆和塗料、橡膠、藥品、食品等) 葉蠟石:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)

葉蠟石:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)