|

市場調查報告書

商品編碼

1685778

精準灌溉:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Precision Irrigation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

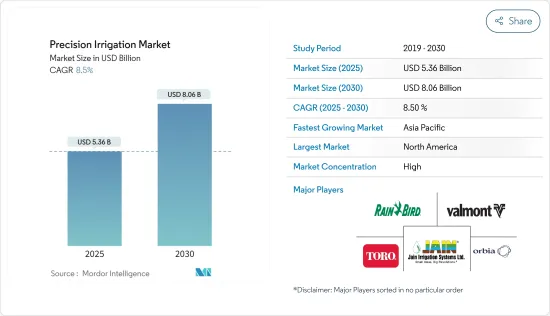

精準灌溉市場規模在 2025 年預計為 53.6 億美元,預計到 2030 年將達到 80.6 億美元,預測期內(2025-2030 年)的複合年成長率為 8.5%。

主要亮點

- 水資源短缺是一項重大挑戰,推動精準灌溉系統的長期採用。隨著消費需求的上升,為確保作物產量進行的人工灌溉的需求也在急劇增加。此外,全球農地的整合使得農民能夠投資精準灌溉等昂貴的系統,從而進一步推動市場的發展。

- 技術發展將進一步促進各地區的市場擴張。例如,2020 年,Nelson Irrigation Corporation 推出了 R55VT 和 R75 末端樞軸噴灌,它們可以輕鬆連接到除衝擊樞軸噴灌之外的任何中心樞軸系統。隨著技術變得越來越便宜和高效,精準灌溉機械的採用預計會增加。預計這將加速預測期內的市場成長。然而,滴灌、噴灌等精準灌溉系統技術複雜,安裝成本高,阻礙了其廣泛應用。

- 此外,由於政府對低利率貸款和採用現代先進精準灌溉系統的補貼政策,精準灌溉市場在未來幾年很可能在南美洲和亞太等新興市場迅速擴張。亞太地區對新技術的認知度不斷提高和適應性高度增強,推動著市場快速成長。

精準灌溉市場趨勢

溫室蔬菜產量快速成長

自動滴灌對於土壤濕度管理至關重要,尤其是對於專業溫室蔬菜。透過完全自動化這些系統,種植者可以精確管理土壤濕度和灌溉。此外,這種自動化預計會增加單位產量的利潤。

水資源短缺是歐洲各地蔬菜種植者面臨的主要挑戰。因此,精準灌溉系統在該地區迅速普及起來。 2021年,比利時園藝競標協會報告稱,比利時溫室蔬菜產量達40.54萬噸,其中番茄產量為30.41萬噸。此外,在有利的天氣條件和對更高作物產量和投資收益不斷成長的需求的推動下,瑞典溫室番茄產量從 2020 年到 2021 年激增了 17.9%。

無土栽培主要用於美國、加拿大、日本、印度、中東和歐洲的溫室蔬菜生產。由於溫室蔬菜需要足夠的水,農民正在轉向噴灌和滴灌系統來實現更高的作物產量,而市場參與者即將推出的技術創新正在推動他們的採用。例如,2023 年 8 月,Netafim 鼓勵透過位於 Shivpuri 的四個 Better Life Farming (BLF) 中心在 1,600 公頃土地上提供滴灌系統,用於番茄的保護性種植。

北美佔據市場主導地位

精準灌溉系統的主要基地在北美,美國佔據該地區一半以上的市場佔有率。聯邦、州和地方的水資源開發計劃以及地下水抽取技術的進步正在大大擴展美國的灌溉面積。美國阿馬裡洛市德克薩斯A&M 農業生命研究與推廣中心 2023 年的一項研究指出,對地面滴灌系統的評估和使用提高了德克薩斯州高原半乾旱多風地區高價值蔬菜生產的用水效率。在番茄的露天種植中,可能會因生物和生物脅迫因素造成嚴重損失,即使採用地面滴灌系統也難以獲得經濟上可行的產量。

墨西哥的巴希奧地區是大麥的主要產地,以地下水消耗量大而聞名。該地區地下水位下降迫切需要開發創新節水技術。 2021 年的一項研究發現,滴灌與保護性農業實踐相結合可使大麥種植的用水量減少多達 40%。這項發現支持在該地區廣泛採用精準灌溉進行大麥種植。 2021年,威立雅水務技術公司旗下的阿瓜斯卡連特斯水基金會與大自然保護協會和當地市政當局進行了合作。他們的共同努力旨在支持阿瓜斯卡連特斯的弱勢農民,鼓勵他們投資滴灌設備,增強農場的復原力,並促進此類系統的採用。

此外,加拿大農民以其專業知識而聞名,並且能夠快速採用新技術,預計將推動該地區的強勁成長。加拿大統計局稱,2022 年加拿大農民的農作物灌溉用水量與 2020 年相比增加了 23%。近年來,加拿大農場採用滴灌技術的現像明顯增加。根據加拿大統計局的數據,2022年採用滴灌的農場數量比2020年增加了33.2%。因此,不可預測的天氣條件和創新節水技術的持續採用可能會在預測期內增加北美農業生產中精準灌溉的使用。

精準灌溉業概況

精準灌溉市場由 Orbia(Netafim Limited)、Jain Irrigation Systems Limited、The Toro Company 和 Valmont 等主要企業主導。 Orbia(Netafim Limited)的市場佔有率最高,其次是Jain Irrigation Systems Limited。建立強大的分銷網路是成熟市場參與者採取的關鍵策略。此外,一些公司與廣泛的經銷商簽訂了最終分銷協議,以提高可訪問性。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 市場概況

- 市場促進因素

- 市場限制

- 波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場區隔

- 類型

- 噴水灌溉

- 傳統噴灌

- 中心樞軸灑水噴灌

- 側向/線性噴灌

- 滴灌

- 地面滴灌

- 地下滴灌

- 精準移動滴灌

- 其他類型

- 噴水灌溉

- 作物類型

- 田間作物

- 種植作物

- 果園和葡萄園

- 草坪和觀賞作物

- 地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 北美其他地區

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 其他亞太地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 非洲

- 南非

- 非洲其他地區

- 北美洲

第6章 競爭格局

- 最受歡迎的策略

- 市場佔有率分析

- 公司簡介

- Jain Irrigation Systems Ltd

- Lindsay Corporation

- Nelson Irrigation Corporation

- Netafim Ltd

- Rain Bird Corporation

- Rivulis Irrigation Ltd

- The Toro Company

- Valmont Industries Inc.

- Mahindra EPC Industries Limited

- Tl Irrigation Co.

- Deere & Company

第7章 市場機會與未來趨勢

The Precision Irrigation Market size is estimated at USD 5.36 billion in 2025, and is expected to reach USD 8.06 billion by 2030, at a CAGR of 8.5% during the forecast period (2025-2030).

Key Highlights

- Water scarcity poses a significant challenge, driving the long-term adoption of precision irrigation systems. As consumer demand grows, the need for artificial irrigation has surged to secure high crop yields. Additionally, the consolidation of farmlands globally enables farmers to invest in costly systems like precision irrigation, further propelling the market.

- Technological developments are further catalyzing the expansion of the market across various regions. For example, in 2020, Nelson Irrigation Corporation introduced the R55VT and R75 End of Pivot Sprinklers, which can be easily attached to any center pivot system, excluding the impact pivot sprinklers. As technology is made affordable and efficient, the adoption rate of precision irrigation machinery is anticipated to increase. This is expected to increase the growth of the market during the forecast period. However, precision irrigation systems such as drip and sprinkler systems come with technical complexities, and the steep installation costs of these systems are hindering their widespread adoption.

- Moreover, due to favorable government policies regarding low-interest loans and subsidies for implementing modern and advanced precision irrigation systems, the precision irrigation market is likely to increase quickly in developing markets such as South America and Asia-Pacific in the coming years. Increasing awareness and high adaptability of new technologies in Asia-Pacific are driving market growth at a rapid pace.

Precision Irrigation Market Trends

Rapid Growth of Greenhouse Vegetable Production

Automatic drip irrigation is crucial in managing soil moisture, particularly for specialized greenhouse vegetables. By fully automating these systems, growers can precisely control soil moisture and water application. Moreover, such automation is anticipated to boost profits per yield.

Water scarcity poses significant challenges for vegetable farmers across various European nations. As a result, precision irrigation systems are rapidly gaining traction in the region. In 2021, the Association of Belgian Horticultural Auctions reported that Belgium's greenhouse vegetable production reached 405.4 thousand metric tons, with tomatoes accounting for 304.1 thousand metric tons. Additionally, bolstered by favorable climatic conditions and rising demand for enhanced crop yields and returns on investment, Sweden's greenhouse tomato production surged by 17.9% from 2020 to 2021.

Soilless cultivation is primarily used for greenhouse vegetable production in the United States, Canada, Japan, India, the Middle East, and Europe. As greenhouse vegetables require ample amounts of water, farmers are switching to sprinkler and drip irrigation systems to achieve higher crop productivity, and technological innovation by the market players in the future motivates the adoption. For instance, in August 2023, Netafim encouraged drip irrigation systems to be provided through four Better Life Farming (BLF) Centers in Shivpuri under protected cultivation for tomatoes on 1,600 hectares of land.

North America Dominates the Market

Precision irrigation systems find their primary hub in North America, with the United States leading the charge, commanding over half of the region's market share. Federal, state, and local water development initiatives and advancements in groundwater pumping technologies have significantly broadened the US irrigated landscape. In 2023, research conducted by the Texas A&M AgriLife Research and Extension Center, Amarillo, United States, stated that the evaluation and usage of Surface Drip Irrigation Systems escalated the water-use efficiency in high-value vegetable production in the semi-arid, windy region of the Texas high plains. It could be challenging for tomatoes in open-field conditions to achieve an economically viable crop, even when using a surface drip irrigation system, due to the potential for extreme losses to both biotic and abiotic stressors.

The Bajio region of Mexico is a leading producer of barley, a crop known for its substantial groundwater consumption. As groundwater levels in the region dwindle, there is an urgent call for innovative water-saving technologies. A 2021 study highlighted that a blend of drip irrigation and conservation agriculture could slash water usage in barley farming by as much as 40%. This finding is set to champion the broader adoption of precision irrigation in the region's barley farming. In 2021, the Aguascalientes Water Fund, a division of Veolia Water Technologies, collaborated with The Nature Conservancy and the local municipality. Their joint effort aimed to assist vulnerable farmers in Aguascalientes, encouraging them to invest in drip irrigation equipment, thereby bolstering farm resilience and potentially increasing the uptake of these systems.

Moreover, Canadian farmers, known for their expertise, are quick to adopt new technologies, leading to anticipated high growth rates in the region. According to Statistics Canada, Canadian farmers increased their water usage for crop irrigation by 23% in 2022 compared to 2020, which is majorly attributed to the drier climatic conditions in various regions throughout the country. In recent years, there has been a notable surge in the prevalence of drip irrigation on Canadian farms. According to Canadian statistics, in 2022, the number of farms adopting drip irrigation increased by 33.2% compared to 2020. Therefore, unpredictable climatic conditions and the growing adoption of innovative water-saving techniques may increase the use of precision irrigation in North American agricultural production during the forecast period.

Precision Irrigation Industry Overview

The precision irrigation market is consolidated with major companies such as Orbia (Netafim Limited), Jain Irrigation Systems Limited, The Toro Company, and Valmont. Orbia (Netafim Limited) held the highest market share, followed by Jain Irrigation Systems Limited. Establishing a strong distribution network is a prime strategy well-established market players follow. Moreover, some companies have signed definitive dealership agreements with a wide range of dealers to enhance accessibility.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Force Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitutes

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Sprinkler Irrigation

- 5.1.1.1 Traditional Sprinklers

- 5.1.1.2 Center Pivot Sprinklers

- 5.1.1.3 Lateral Move/ Linear Sprinklers

- 5.1.2 Drip Irrigation

- 5.1.2.1 Surface Drip Irrigation

- 5.1.2.2 Sub-Surface Drip Irrigation

- 5.1.2.3 Precision Mobile Drip Irrigation

- 5.1.3 Other Types

- 5.1.1 Sprinkler Irrigation

- 5.2 Crop Type

- 5.2.1 Field Crops

- 5.2.2 Plantation Crops

- 5.2.3 Orchards and Vineyards

- 5.2.4 Turf and Ornamentals

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Spain

- 5.3.2.5 Italy

- 5.3.2.6 Russia

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Africa

- 5.3.5.1 South Africa

- 5.3.5.2 Rest of Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Jain Irrigation Systems Ltd

- 6.3.2 Lindsay Corporation

- 6.3.3 Nelson Irrigation Corporation

- 6.3.4 Netafim Ltd

- 6.3.5 Rain Bird Corporation

- 6.3.6 Rivulis Irrigation Ltd

- 6.3.7 The Toro Company

- 6.3.8 Valmont Industries Inc.

- 6.3.9 Mahindra EPC Industries Limited

- 6.3.10 T-l Irrigation Co.

- 6.3.11 Deere & Company