|

市場調查報告書

商品編碼

1685862

零售業巨量資料分析:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Big Data Analytics in Retail - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

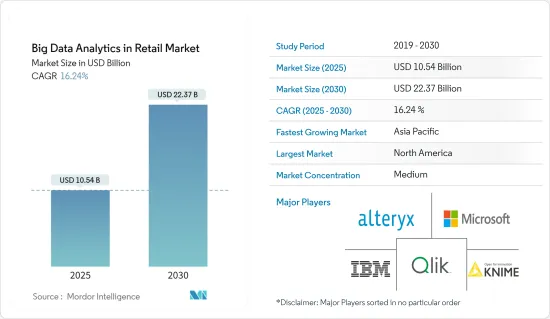

零售巨量資料分析市場規模預計在 2025 年為 105.4 億美元,預計到 2030 年將達到 223.7 億美元,預測期內(2025-2030 年)的複合年成長率為 16.24%。

推動市場成長的關鍵因素是不斷發展的技術、資產、工程導向的價值鏈以及工業4.0驅動的快速工業自動化。市場規模和估值反映了市場供應商透過向半導體、航太和汽車等各類終端用戶提供製造解決方案的巨量資料分析而產生的收益。

主要亮點

- 複雜的生產流程、供應鏈中公司之間的關係以及持續避免錯誤的壓力是工業製造商必須應對的。因此,製造商需要擴大資料來源以降低成本、提高產品品質和提高效率。使用巨量資料分析的公司可以改善關鍵流程、消除瓶頸、預測需求並預測潛在的故障和延誤。

- 連網型設備和感測器的普及以及M2M通訊的實現,正在急劇增加製造業產生的資料。這些資料點的範圍可以是材料經過一個製程週期所需時間的詳細指標,也可以是汽車產業中材料應力容量等更複雜的計算。

- 隨著世界各地的製造商意識到在石油和天然氣、汽車、食品和飲料、煉油廠、塑膠和化學品等行業的製造業中整合巨量資料分析的好處,製造業巨量資料正在興起。製造公司擴大採用巨量資料分析解決方案來生產高度準確和精確的產品和設備。例如,以製造噴射引擎、機車、渦輪機和醫學成像設備而聞名的通用電氣公司也在利用其產生的大量資料開發其設備的智慧連網版本。

- 阻礙市場成長的因素之一是缺乏有效處理和分析非結構化資料的數位技能和意識。對巨量資料安全性的擔憂也是阻礙工業製造商採用巨量資料的一個主要因素。

- 新冠肺炎疫情擾亂了一些企業的經營,但也加速了一些產業向數位化的轉變。在一些數位技術採用緩慢的地區,這可能永久改變了各個行業製造商的行為。

零售業巨量資料分析市場趨勢

汽車產業是快速成長的終端用戶

- 全球汽車產業正在經歷變革時期,車型和燃料選項數量不斷增加,二手車價值波動,以及供應鏈挑戰,使得OEM難以預測未來價值和了解總體擁有成本。透過利用巨量資料、分析和洞察,行業供應商可以建立解決方案來幫助OEM適應不斷變化的行業需求。

- 巨量資料分析使汽車產業能夠從 ERP 系統收集資料,並結合來自業務和供應鏈成員的多個功能領域的資訊。 M2M/IoT 連接是一種網路通訊,它使不同的設備能夠共用資料並在無需人工干預的情況下執行自動化任務。

- RFID、感測器、條碼閱讀器和機器人現已成為工業製造車間的標準。這些設備成倍地增加了資料生成點的數量。

- 汽車產業目前正在發展成為一個更資料主導的產業,以降低與組裝缺陷和庫存過剩相關的成本。現在可以更準確地進行組裝的維護計劃。這一切都歸功於在產業中引入預測分析。

北美將經歷最高成長

- 在工業4.0的推動下,美國在巨量資料分析產業不斷創新,鞏固了在全球市場的地位。智慧技術在市場上的採用也對國民經濟產生直接影響。

- 美國是提供巨量資料分析解決方案的供應商的重要市場。由於工廠自動化的早期採用,預計在預測期內將顯著成長。此外,受訪的市場上所有領先供應商都位於美國。美國正處於第四次工業革命的邊緣,利用資料進行大規模生產,同時整合整個供應鏈中不同的製造系統和資料。這刺激了該國引進先進的系統。

- 此外,中國汽車產業巨量資料成長的一個主要驅動力是技術供應商的大量存在。這些參與者專注於建立夥伴關係、進行併購並提供創新解決方案,以在區域和全球競爭格局中取得進展。

- 汽車產業是工業自動化系統最大的消費者之一。加拿大擁有豐田、雪佛蘭、本田和福特等汽車品牌的八家大型製造廠。此外,加拿大擁有700家製造商,生產滿足汽車產業需求的零件。汽車產業是該地區最重要的產業,因為它對製造業的貢獻最大,因此預計會對所研究的市場產生正面影響。

零售巨量資料分析市場概況

製造業市場的巨量資料分析是半靜態的。隨著開放原始碼工具的出現以及巨量資料分析技術功能的大幅擴展,企業在必須與其他參與者競爭的環境中,可能會傾向於在提高產品性能方面投入過多資金,從而導致成本不斷上升並侵蝕行業盈利。主要參與者包括 Alteryx Inc.、IBM Corporation、Knime AG、Microsoft Corporation 和 Qliktech International AB。

- 2023 年 12 月,KNIME AG 宣布推出 KNIME Analytics Platform 5.2。新版本具有改進的使用者介面、更聰明、更透明的人工智慧助理以及現代化的人工智慧腳本體驗。

- 2023 年 6 月,穆迪公司與微軟宣佈建立夥伴關係,為金融服務提供下一代資料、分析、研究、協作和風險解決方案。此次夥伴關係將藉助微軟人工智慧和穆迪專有的資料、分析和研究,創造創新產品,增強企業情報和風險評估洞察力。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 產業價值鏈分析

- COVID-19 產業影響評估

第5章 市場動態

- 市場促進因素

- 不斷發展的技術、資產和工程驅動的價值鏈

- 利用工業 4.0 實現快速工業自動化

- 市場限制

- 缺乏意識和安全問題

- 市場機會

- 增加預測分析工具的使用

- 工業物聯網 (IIoT) 的採用日益增多

第6章 市場細分

- 按最終用戶產業

- 半導體

- 航太

- 車

- 其他最終用戶產業

- 按應用

- 狀態監測

- 品管

- 庫存管理

- 其他用途

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 其他亞太地區

- 拉丁美洲

- 中東和非洲

- 北美洲

第7章 競爭格局

- 公司簡介

- Alteryx Inc.

- IBM Corporation

- Knime AG

- Microsoft Corporation

- Qliktech International AB

- Oracle Corporation

- Altair Engineering Inc.(RapidMiner Inc.)

- SAP SE

- SAS Institute Inc.

- Tibco Software Inc.(Cloud Software Group)

- NEC Corporation

- Fujitsu Ltd

- Toshiba Digital Solutions Corporation

第8章投資分析

第9章:市場的未來

The Big Data Analytics in Retail Market size is estimated at USD 10.54 billion in 2025, and is expected to reach USD 22.37 billion by 2030, at a CAGR of 16.24% during the forecast period (2025-2030).

The primary factors driving the market's growth include evolving technology, assets, engineering-oriented value chains, and rapid industrial automation led by Industry 4.0. The market sizing estimates reflect the revenue generated by the market vendors by offering big data analytics in manufacturing solutions to various end-users, such as semiconductors, aerospace, and automotive.

Key Highlights

- Complex production processes, cross-company relationships in the supply chain, and constant pressure to avoid errors must be addressed by industrial manufacturers. Therefore, manufacturers need to expand their data sources so that costs can be reduced, the quality of products can be improved, and efficiency is increased. Companies using big data analytics improve key processes, eliminate bottlenecks, predict demand, and anticipate potential failures and delays.

- With the widespread use of connected devices and sensors, along with the enabling of M2M communication, there has been a significant increase in the data generated in the manufacturing industry. These data points can be of different types, from a metric detailing the time a material takes to pass through one process cycle to a more complex one, such as calculating the material stress capability in the automotive industry.

- Big data in manufacturing is increasing as manufacturers across the globe are seeing the benefits of integrating big data analytics in manufacturing across industries like oil and gas, automotive, food and beverages, refineries, plastics, and chemicals. Manufacturing companies are increasingly adopting big data analytics solutions to manufacture products and devices with high precision and accuracy. For instance, GE, known as the manufacturer of jet engines, locomotives, turbines, and medical imaging equipment, also develops smart, connected versions of the equipment in the massive data they generate.

- One of the factors hindering the growth of the market studied is the lack of digital skills and awareness to handle the unstructured data effectively for analysis. Big data security concerns are another major factor restraining the market adoption of industrial manufacturers.

- The COVID-19 pandemic disrupted several businesses but accelerated the shift to digitization in several sectors. In several regions that have been lagging in adopting digital technologies, manufacturers' behavior in various sectors may have been permanently changed.

Big Data Analytics in Retail Market Trends

Automotive Industry to be the Fastest Growing End User

- The global automobile industry is undergoing a transformation that includes an ever-increasing array of models and fuel types, fluctuations in used car values, and supply chain challenges that hinder OEMs in projecting future value and understanding the total cost of ownership. By leveraging big data, analytics, and insights, industry vendors can create a solution that helps OEMs adapt to the changing industry demands.

- Big data analytics allows the automobile industry to collect data from ERP systems and combine information from multiple functional units of the business and the supply chain members. With the emergence of industry IoT, a networked system, and M2M communication, the automotive industry is positioning itself towards Industry 4.0, Where M2M/IoT connections are networked communications that allow different devices to share data and carry out automatic tasks without the need for human interaction.

- RFIDs, sensors, barcode readers, and robots are now standard in the industry's manufacturing floor. These devices have increased the data generation points exponentially.

- The automotive industry is now evolving into a more data-driven industry to reduce the costs associated with faulty assembly and over-inventory stockings. It can now plan the maintenance of the assembly lines more accurately. It has all been possible due to the adoption of predictive analytics in the industry.

North America to Witness Highest Growth

- Fueled by Industry 4.0, the United States continues to innovate and consolidate its position in the global market in the big data analytics industry. The embracing of smart technologies in the market has also directly impacted the national economy.

- The United States is a substantial market for vendors offering solutions for big data analytics. It is expected to grow significantly over the forecast period, owing to the early adoption of factory automation. Moreover, all the major vendors studied in the market are US-based. The United States is on the verge of the fourth industrial revolution, where data is used in large-scale production while integrating data with various manufacturing systems throughout the supply chain. This is fueling the country's adoption of the advanced system.

- Moreover, the major driver for the growth of big data in the country's automotive sector is the significant presence of technology providers. These players focus on entering into partnerships, merger acquisitions, and innovative solutions offerings to stay in the regional and globally competitive landscape.

- The automotive industry is one of the largest consumers of industrial automation systems. Canada has eight large manufacturing plants operated by Toyota, Chevrolet, Honda, and Ford. Moreover, the country has 700 manufacturers that create parts that meet the automotive industry's requirements. The automotive industry is the most significant in this region as it contributes the most to the manufacturing sector, and it is expected to impact the market studied positively.

Big Data Analytics in Retail Market Overview

Big data analytics in the manufacturing market is semi-consolidated. The huge expansion of capabilities in big data analytics technology, with the availability of open-source tools, may tempt companies to compete with other players and give away too much of their improved product performance in an environment that escalates costs and erodes industry profitability. Some of the major players include Alteryx Inc., IBM Corporation, Knime AG, Microsoft Corporation, and Qliktech International AB.

- In December 2023, Knime AG announced that KNIME Analytics Platform 5.2. is now available. The new version features user interface improvements, a smarter and more transparent Artificial Intelligence assistant, and a modernized scripting experience with AI.

- In June 2023, Moody's Corporation and Microsoft announced a partnership to deliver next-generation data, analytics, research, collaboration, and risk solutions for financial services. The partnership would create innovative products to enhance insights into corporate intelligence and risk assessment with the help of Microsoft's AI and Moody's proprietary data, analytics, and research.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Competitive Rivalry within the Industry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of the Impact of COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Evolving Technology, Asset, and Engineering-oriented Value Chain

- 5.1.2 Rapid Industrial Automation led by Industry 4.0

- 5.2 Market Restraints

- 5.2.1 Lack of Awareness and Security Concerns

- 5.3 Market Opportunities

- 5.3.1 Increasing Use of Predictive Analytics Tools

- 5.3.2 Increasing Adoption of IIoT

6 MARKET SEGMENTATION

- 6.1 By End-user Industry

- 6.1.1 Semiconductor

- 6.1.2 Aerospace

- 6.1.3 Automotive

- 6.1.4 Other End-user Industries

- 6.2 By Application

- 6.2.1 Condition Monitoring

- 6.2.2 Quality Management

- 6.2.3 Inventory Management

- 6.2.4 Other Applications

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 Germany

- 6.3.2.3 France

- 6.3.2.4 Rest of the Europe

- 6.3.3 Asia-Pacific

- 6.3.3.1 China

- 6.3.3.2 Japan

- 6.3.3.3 India

- 6.3.3.4 Rest of the Asia-Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Alteryx Inc.

- 7.1.2 IBM Corporation

- 7.1.3 Knime AG

- 7.1.4 Microsoft Corporation

- 7.1.5 Qliktech International AB

- 7.1.6 Oracle Corporation

- 7.1.7 Altair Engineering Inc. (RapidMiner Inc.)

- 7.1.8 SAP SE

- 7.1.9 SAS Institute Inc.

- 7.1.10 Tibco Software Inc.(Cloud Software Group)

- 7.1.11 NEC Corporation

- 7.1.12 Fujitsu Ltd

- 7.1.13 Toshiba Digital Solutions Corporation

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

2025年全球農業巨量資料分析市場報告2025年巨量資料軟體全球市場報告2025年全球石油天然氣巨量資料市場2025年半導體和電子巨量資料分析全球市場報告2025年巨量資料基礎設施全球市場報告

2025年全球農業巨量資料分析市場報告2025年巨量資料軟體全球市場報告2025年全球石油天然氣巨量資料市場2025年半導體和電子巨量資料分析全球市場報告2025年巨量資料基礎設施全球市場報告 零售業巨量資料分析市場規模、佔有率和成長分析(按組件、部署、組織規模、應用和地區)- 產業預測 2025-2032製造業巨量資料市場規模、佔有率和成長分析(按產品、部署、應用和地區)- 產業預測 2025-2032

零售業巨量資料分析市場規模、佔有率和成長分析(按組件、部署、組織規模、應用和地區)- 產業預測 2025-2032製造業巨量資料市場規模、佔有率和成長分析(按產品、部署、應用和地區)- 產業預測 2025-2032 全球石油與天然氣領域巨量資料市場(2025-2029)

全球石油與天然氣領域巨量資料市場(2025-2029) 巨量資料服務,全球市場,2025-2029

巨量資料服務,全球市場,2025-2029 戰爭的未來:科技觀點

戰爭的未來:科技觀點