|

市場調查報告書

商品編碼

1685886

潤滑脂:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)Grease - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

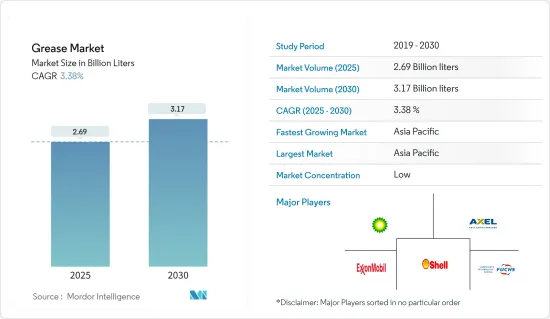

預計2025年潤滑脂市場規模為26.9億公升,到2030年預計將達到31.7億公升,預測期內(2025-2030年)的複合年成長率為3.38%。

主要亮點

- 汽車保有量的快速成長、發電投資的強勁成長是拉動油脂市場需求的主要因素。

- 然而,有關潤滑脂使用的環境法規預計會阻礙市場成長。

- 然而,技術進步、產品創新和聚脲潤滑脂使用量的增加有望為所研究的市場創造新的機會。

- 預計亞太地區將主導全球市場,其中中國和印度將佔據大部分需求。

潤滑脂市場趨勢

汽車和其他運輸業將主導市場

- 汽車和運輸業作為潤滑脂市場的推動者發揮著至關重要的作用。隨著汽車產業OEM和 RMO 市場的擴大,它們將在未來幾年直接影響潤滑脂需求。

- 潤滑脂需求量大主要是由於新興市場對輕量化、高性能汽車的需求不斷成長、汽車輪轂數量不斷增加以及可支配收入不斷提高。

- 國際汽車製造商組織(OICA)報告稱,2023年全球新車銷量將呈現穩健成長,較2022年成長11.9%,超過9,270萬輛。其中,新乘用車銷量與前一年同期比較增11.3%至6,530萬輛,高於2022年的5,860萬輛。同時,2023年全球新商用車註冊量將為2,750萬輛,較2022年的2,420萬輛成長13.3%。

- 在北美,預計2023年汽車銷量為1,919萬輛,較2022年的1,693萬輛成長13.4%。總銷量1919萬輛中,乘用車398萬輛,商用車1521萬輛,其餘為重型卡車、客車和長途客車。

- 此外,根據歐洲汽車工業協會的資料,預計2023年歐洲新車註冊量與前一年同期比較成長18.7%。預計2023年乘用車銷售量將達到1,500萬輛,商用車銷售量將達290萬輛,而2022年分別為1,264萬輛及244萬輛。

- 航太部門正在經歷快速的技術進步,從而增強了飛機製造能力。波音公司對 2023-2042 年商用飛機的展望顯示,受國際和國內航空旅行復甦的推動,到 2042 年全球對新商用飛機的需求將達到 48,575 架。 2023年,波音公司將交付528架飛機,並獲得1,314份淨新訂單,較2022年的480架交付和774份訂單大幅增加。雖然該公司實現了交付超過375架窄體737飛機的修訂目標,但仍未達到400至450架的最初目標。

- 空中巴士提供的資料顯示,2023年該公司向全球87家客戶交付了735架民航機,在複雜的商業環境中表現出強勁的業績。該公司「民航機」業務同年錄得2,319架新訂單。

- 由於這些趨勢,預計未來幾年潤滑脂消費量將會增加。

亞太地區佔市場主導地位

- 亞太地區將引領油脂消費,其次是北美和歐洲。預計預測期內中國、印度和印尼等國家將推動強勁的潤滑脂需求。

- 目前,中國是潤滑油和潤滑脂的最大消費國。其在各個領域的廣泛製造活動,加上工業和汽車領域的快速成長,鞏固了其作為全球領先的潤滑脂消費和生產者的地位。

- 一些領先的潤滑脂製造商正在積極推行擴大策略,以期進入新市場,從而增加所研究市場的需求。例如

- 2024年6月,殼牌完成了位於曼谷的潤滑脂製造廠的大規模擴建,生產能力提高了兩倍。此次擴建使該工廠能夠滿足泰國一半的油脂需求,年產量從 5,000 噸增加到 15,000 噸。

- 殼牌印尼公司於2024年3月宣布,計劃在印尼勿加泗建造第一家潤滑脂製造廠(GMP),年產能為12千噸。該設施將對現有的 Maroondah 潤滑油調配廠 (LOBP) 進行補充。

- 中國汽車業是潤滑油的主要消費產業,反映出汽車持有強勁成長和技術進步。根據中國工業協會的資料,2023年中國汽車產銷量將分別突破3,000萬輛,與前一年同期比較實現兩位數成長。

- 預計預測期內中國發電產業對潤滑脂的需求將保持強勁。根據社區利益公司 Ember 的報告顯示,中國發電產業正在快速成長,不久的將來很可能會實現 10% 以上的成長。

- 2023年中國電力需求成長4%以上,2022年成長3%以上。中國目前運作核能發電廠47座,總設備容量4876萬千瓦。總合11座新核能發電廠建,總裝置容量為1,175.9萬千瓦。

- 2023年,印度乘用車銷量將首度突破400萬輛大關。收入增加、SUV 的普及以及優惠的貸款利率都是促成因素。根據印度汽車工業協會(SIAM)的資料,2020年乘用車、轎車和多用途車的銷量將從2022年的379萬輛成長8.2%至410多萬輛,其中多用途車佔銷量的57.4%。

- 在不斷成長的能源需求和永續性願望的推動下,印尼的發電行業正處於變革之中。目前,煤炭佔電力供應的 60% 以上,但正在努力實現可再生能源多樣化並擴大其作用。水力發電潛力接近 75 吉瓦,西爪哇省的 1,040 兆瓦發電廠等計劃已在利用這項資源。地熱能源目標雄心勃勃,到 2025 年達到 5GW,到 2035 年達到 9.3GW,彰顯了該國致力於利用其巨大的可再生能源潛力的決心。

- 預計上述因素將增加亞太地區對潤滑脂的需求。

油脂業概況

油脂市場比較分散。主要公司(排名不分先後)包括殼牌公司、埃克森美孚公司、英國石油公司、福斯公司和阿克塞爾·克里斯蒂恩森。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 市場促進因素

- 汽車保有量快速成長推動潤滑脂需求

- 發電業投資強勁成長

- 其他促進因素

- 市場限制

- 有關潤滑脂使用的環境法規

- 其他阻礙因素

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場區隔

- 按增稠劑

- 鋰基

- 鈣基

- 鋁基

- 聚脲

- 其他增稠劑

- 按最終用戶產業

- 發電

- 汽車和其他交通工具

- 重型機械

- 食品和飲料

- 冶金與金屬加工

- 化學製造

- 其他最終用戶產業

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 馬來西亞

- 泰國

- 印尼

- 越南

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐國家

- 土耳其

- 俄羅斯

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 卡達

- 阿拉伯聯合大公國

- 奈及利亞

- 埃及

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章競爭格局

- 併購、合資、合作與協議

- 市場佔有率(%)**/排名分析

- 主要企業策略

- 公司簡介

- Axel Christiernsson

- BECHEM Lubrication Technology LLC

- BP PLC

- Carl Bechem Gmbh

- Chevron Corporation

- China Petroleum & Chemical Corporation

- ENEOS Corporation

- ETS

- Exxon Mobil Corporation

- FUCHS

- Gazprom Neft PJSC

- Kluber Lubrication

- Lukoil

- Orlen Oil Ltd

- Penrite Oil

- Petromin

- PETRONAS Lubricants International

- Shell PLC

- TotalEnergies

第7章 市場機會與未來趨勢

- 技術進步與產品創新

- 擴大聚脲潤滑脂的用途

- 其他機會

簡介目錄

Product Code: 48925

The Grease Market size is estimated at 2.69 billion liters in 2025, and is expected to reach 3.17 billion liters by 2030, at a CAGR of 3.38% during the forecast period (2025-2030).

Key Highlights

- The surging vehicle population and the robust growth of investments in power generation are the major factors driving the demand for the grease market.

- However, environmental regulations concerning the usage of grease are expected to hinder the market's growth.

- Nevertheless, technological advancements, product innovations, and the growing usage of polyurea greases are expected to create new opportunities for the market studied.

- Asia-Pacific is expected to dominate the global market, with the majority of demand coming from China and India.

Grease Market Trends

Automotive and Other Transportation Segment to Dominate the Market

- The automotive and transportation sector plays a pivotal role in driving the grease market. As the OEM and RMO markets in the automotive industry expand, they are poised to directly influence grease demand in the coming years.

- The major reasons for the high demand for grease are the growing demand for lightweight, high-performance cars in emerging markets, increasing automotive hubs, and rising disposable income.

- In 2023, global new vehicle sales saw a robust growth of 11.9% over 2022, totaling over 92.7 million units, as reported by the Organisation Internationale des Constructeurs d'Automobiles (OICA). Specifically, new passenger vehicle sales climbed by 11.3% year-over-year, hitting 65.3 million units, up from 58.6 million units in 2022. Concurrently, new commercial vehicle registrations worldwide rose to 27.5 million units in 2023, marking a notable 13.3% increase from the 24.2 million units recorded in 2022.

- In North America, motor vehicle sales in 2023 accounted for 19.19 million units, an increase of 13.4% compared to 16.93 million units sold in 2022. Out of the total 19.19 million units, passenger cars accounted for 3.98 million units, commercial vehicles made up 15.21 million units, and the remaining units were a combination of heavy trucks, buses, and coaches.

- Furthermore, as per the data from the European Automobile Manufacturers Association, in Europe, the overall registration of new motor vehicles increased by 18.7% in 2023 compared to the previous year. In 2023, passenger car and commercial vehicle sales reached 15 million units and 2.90 million units, respectively, compared to 12.64 million units and 2.44 million units in 2022.

- The aerospace sector is witnessing swift technological advancements, bolstering aircraft manufacturing. Boeing's Commercial Outlook for 2023-2042 anticipates global demand for 48,575 new commercial jets by 2042, driven by a rebound in international and domestic air travel. In 2023, Boeing delivered 528 aircraft and secured 1,314 net new orders, a significant rise from 480 deliveries and 774 orders in 2022. Notably, while it met its revised goal of delivering at least 375 narrowbody 737 jets, it fell short of its initial target of 400 to 450 jets.

- As per the data provided by Airbus, in 2023, the company delivered 735 commercial aircraft to 87 customers around the world, demonstrating strong performance despite a complex operating environment. The company's "Commercial Aircraft" business registered 2,319 gross new orders during the same year.

- Given these dynamics, grease consumption is set to rise in the coming years.

Asia-Pacific to Dominate the Market

- Asia-Pacific leads in grease consumption, with North America and Europe following. Countries like China, India, and Indonesia are poised to drive strong grease demand during the forecast period.

- Currently, China stands as the dominant consumer of lubricants and greases. Its extensive manufacturing activities across various sectors, coupled with rapid growth in both industrial and automotive domains, have solidified its position as a major global consumer and producer of grease.

- Some of the key grease manufacturers are actively pursuing expansion strategies, eyeing entry into new markets, thereby augmenting the demand for the market studied. For instance,

- In June 2024, Shell completed a significant expansion at its grease manufacturing plant in Bangkok, tripling its production capacity. This enhancement positions the plant to meet half of Thailand's grease demand, boosting its annual output from 5,000 to 15,000 metric tons.

- Shell Indonesia unveiled plans in March 2024 to construct its inaugural Grease Manufacturing Plant (GMP) in Bekasi, Indonesia, with a capacity of 12 kilotonnes per annum. This facility will complement the company's existing Marunda Lubricants Oil Blending Plant (LOBP).

- China's automotive industry stands out as the leading consumer of lubricants, reflecting its robust vehicle fleet growth and technological advancements. In 2023, both automobile sales and production in China reached a milestone, hitting 30 million units each, marking a double-digit increase from the previous year, as per the data from the China Association of Automobile Manufacturers (CAAM).

- The demand for grease in China's power generation sector is likely to perform well during the forecast period. According to reports by Ember, a community interest company, the country's power generation industry is growing rapidly and may register over 10% growth in the near future.

- China's electricity demand rose by over 4% in 2023 and by over 3% in 2022. There are 47 nuclear power stations in service in China, with a total installed capacity of 48.76 GW. A total of 11 new nuclear power plants with an installed capacity of 11.759 GW were being built.

- In 2023, India's passenger vehicle sales crossed the 4 million mark for the first time, driven by rising incomes, a surge in sport-utility vehicles, and favorable loan rates. As per the data from the Society of Indian Automobile Manufacturers (SIAM), over 4.1 million cars, sedans, and utility vehicles were sold, marking an 8.2% uptick from 3.79 million units in 2022, with utility vehicles making up 57.4% of the sales.

- Indonesia's power generation sector is in a state of evolution, spurred by escalating energy demands and ambitious sustainability aspirations. While coal currently dominates, accounting for over 60% of the electricity supply, there is a determined effort to diversify and amplify the role of renewables. With a hydropower potential nearing 75 GW, projects like the 1,040 MW facility in West Java are already capitalizing on this resource. Geothermal energy targets stand at 5 GW by 2025, with an ambitious leap to 9.3 GW by 2035, underscoring the nation's commitment to harnessing its vast renewable energy potential.

- The above-mentioned factors are likely to increase the demand for grease in Asia-Pacific.

Grease Industry Overview

The grease market is fragmented in nature. The major players (not in any particular order) include Shell PLC, Exxon Mobil Corporation, BP PLC, FUCHS, and Axel Christiernsson.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Surging Vehicle Population to Drive the Demand for Grease

- 4.1.2 Robust Growth of Investments in the Power Generation Sector

- 4.1.3 Other Drivers

- 4.2 Market Restraints

- 4.2.1 Environmental Regulations Concerning Usage of Grease

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 By Thickeners

- 5.1.1 Lithium-based

- 5.1.2 Calcium-based

- 5.1.3 Aluminium-based

- 5.1.4 Polyurea

- 5.1.5 Other Thickeners

- 5.2 By End-user Industry

- 5.2.1 Power Generation

- 5.2.2 Automotive and Other Transportation

- 5.2.3 Heavy Equipment

- 5.2.4 Food and Beverage

- 5.2.5 Metallurgy and Metalworking

- 5.2.6 Chemical Manufacturing

- 5.2.7 Other End-user Industries

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 NORDIC Countries

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 Qatar

- 5.3.5.3 United Arab Emirates

- 5.3.5.4 Nigeria

- 5.3.5.5 Egypt

- 5.3.5.6 South Africa

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/ Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Axel Christiernsson

- 6.4.2 BECHEM Lubrication Technology LLC

- 6.4.3 BP PLC

- 6.4.4 Carl Bechem Gmbh

- 6.4.5 Chevron Corporation

- 6.4.6 China Petroleum & Chemical Corporation

- 6.4.7 ENEOS Corporation

- 6.4.8 ETS

- 6.4.9 Exxon Mobil Corporation

- 6.4.10 FUCHS

- 6.4.11 Gazprom Neft PJSC

- 6.4.12 Kluber Lubrication

- 6.4.13 Lukoil

- 6.4.14 Orlen Oil Ltd

- 6.4.15 Penrite Oil

- 6.4.16 Petromin

- 6.4.17 PETRONAS Lubricants International

- 6.4.18 Shell PLC

- 6.4.19 TotalEnergies

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Technological Advancements and Product Innovation

- 7.2 Growing Usage of Polyurea Greases

- 7.3 Other Opportunities

02-2729-4219

+886-2-2729-4219

全球食品機械潤滑脂市場:市場佔有率和排名、總銷量和需求預測(2024-2030 年)

全球食品機械潤滑脂市場:市場佔有率和排名、總銷量和需求預測(2024-2030 年) 全球潤滑脂市場:預測(2025-2030)

全球潤滑脂市場:預測(2025-2030) 2024年鋰基潤滑脂全球市場報告

2024年鋰基潤滑脂全球市場報告 非鋰基潤滑脂市場:按類型、基礎油、類別、分銷管道、最終用途分類 - 全球預測 2025-2030

非鋰基潤滑脂市場:按類型、基礎油、類別、分銷管道、最終用途分類 - 全球預測 2025-2030 潤滑脂市場:按類型、基礎油、組別、最終用途 - 2025-2030 年全球預測

潤滑脂市場:按類型、基礎油、組別、最終用途 - 2025-2030 年全球預測 潤滑脂市場:按類型、應用分類 - 2025-2030 年全球預測

潤滑脂市場:按類型、應用分類 - 2025-2030 年全球預測 2030 年亞太地區潤滑脂市場預測 - 區域分析 - 按基礎油、稠化劑類型和最終用途行業

2030 年亞太地區潤滑脂市場預測 - 區域分析 - 按基礎油、稠化劑類型和最終用途行業 2030 年歐洲潤滑脂市場預測 - 區域分析 - 按基礎油、稠化劑類型和最終用途行業

2030 年歐洲潤滑脂市場預測 - 區域分析 - 按基礎油、稠化劑類型和最終用途行業 到 2030 年北美潤滑脂市場預測 - 區域分析 - 按基礎油、稠化劑類型和最終用途行業

到 2030 年北美潤滑脂市場預測 - 區域分析 - 按基礎油、稠化劑類型和最終用途行業 潤滑脂市場報告:2030 年趨勢、預測與競爭分析

潤滑脂市場報告:2030 年趨勢、預測與競爭分析

▼