|

市場調查報告書

商品編碼

1685951

奈米碳管-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)Carbon Nanotubes - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

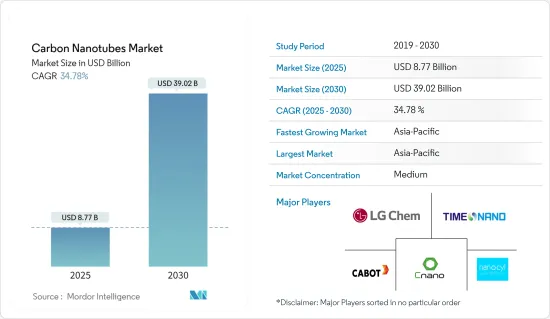

預計 2025 年奈米碳管市場規模為 87.7 億美元,到 2030 年預計將達到 390.2 億美元,預測期內(2025-2030 年)的複合年成長率為 34.78%。

新冠疫情為奈米碳管市場帶來了各種挑戰,但也為某些領域提供了成長機會。隨著世界從疫情中復甦,奈米碳管市場正在逐漸恢復勢頭,預計在預測期內將繼續成長。

由於能源、汽車、電子、航太和其他工業應用等各行業的應用不斷增加,市場需求也隨之增加。

從中期來看,電動車中奈米碳管的使用量不斷增加以及許多應用對先進材料的需求不斷成長是推動市場發展的關鍵因素。

另一方面,環境和健康安全問題預計會抑制市場成長。

預計未來幾年對能源儲存設備的需求不斷成長將為市場帶來機會。

亞太地區貢獻了最大的市場佔有率,預計在預測期內將佔據市場主導地位。

奈米碳管市場趨勢

能源領域佔市場主導地位

- 由於其高表面積和電導率,奈米碳管(CNT) 已引起人們的關注,主要作為太陽能電池、燃料電池催化劑和儲氫等能源應用的觸媒撐體。這些獨特的特性使得 CNT 可用作能量轉換和儲存設備中的補充材料。

- 可再生能源的成長受到主要市場更雄心勃勃的擴張政策的推動,部分原因是為了應對當前的能源危機。過去五年可再生能源的擴張速度加快主要歸因於兩個因素。

- 首先,全球能源危機導致石化燃料和電力價格飆升,使得可再生能源發電技術更具經濟吸引力。

- 其次,俄羅斯入侵烏克蘭導致石化燃料進口國,尤其是歐洲國家,更重視可再生能源的能源安全效益。

- 儘管對風能和太陽能的補貼正在逐步取消,但中國仍計劃在未來五年內加速成長,並在 2022 年至 2027 年期間安裝全球近一半的可再生能源發電產能。 「十四五」規劃中雄心勃勃的可再生能源目標、市場改革以及地方政府的大力支持,為可再生提供了長期收益保障。

- 歐盟是繼中國之後全球第二大成長市場。 2010年至2015年,歐盟可再生能源產能擴張速度在過去五年中趨於穩定。然而,預計2022年至2027年期間,歐盟可再生能源產能擴張速度將增加一倍以上。一些歐盟成員國在俄羅斯入侵烏克蘭之前就已製定雄心勃勃的目標和政策,以加速再生能源的採用。而歐盟則在再生能源一攬子計畫下提案了更積極的目標,即到2027年完全停止進口俄羅斯石化燃料。

- 在美國,可再生能源的部署在過去五年中幾乎加倍。 《個人退休帳戶法》於 2022 年 8 月通過,將再生能源的稅額扣抵抵免延長至 2032 年,為風能和太陽能發電工程提供了前所未有的長期可見性。在印度,預計預測期內新增裝置容量將加倍,其中太陽能光電發電將占主導地位,這得益於競爭性競標,有助於政府實現到 2030 年安裝 500 吉瓦可再生能源的雄心勃勃的目標。

- 因此,這些因素有望推動奈米碳管在能源產業的消費。

亞太地區佔市場主導地位

- 中國是亞太地區最大的碳奈米材料生產國和消費國。豐富的原料和低廉的生產成本支撐著該國碳奈米材料市場的成長。

- CNT 卓越的電氣性能使其能夠應用於光伏、感測器、半導體裝置、顯示器、導體、燃料電池、收集器和電池等電氣和電子應用。

- 中國擁有全球最廣泛的電子產品生產基地,為韓國、新加坡和台灣等現有的上游生產商帶來了激烈的競爭。智慧型手機、OLED 電視和平板電腦等電子產品是成長最快的家用電子電器領域。隨著中階可支配收入的增加,電子產品的需求預計將成長,這將很快推動CNT市場的發展。

- 印度政府正在與主要半導體公司討論推出本地製造工廠。印度政府已根據修改後的「印度半導體計畫」邀請新一輪招標,自 2023 年 6 月起在印度建立半導體和顯示器工廠,總投資額為 7,600 億印度盧比(約 100 億美元)。

- 在印度,汽車產業已經進行了大規模的投資。汽車領域近期的投資與發展趨勢包括:

- 2023年1月,MG 馬達 India宣布將投資1億美元擴大產能。 2022 年 12 月,Mahindra & Mahindra 宣布計劃投資 1,000 億印度盧比(12 億美元)在普納建立電動車製造廠。這項投資凸顯了電動車產業日益成長的重要性。

- 日本電子產業是日本半導體銷售需求最重要的驅動力。日本約有30家半導體工廠,涉及各種半導體晶片的製造。預計2021年日本半導體產量將與前一年同期比較增13%,2022年將成長10%,產值將達到3.746兆日圓(233.1億美元)。預計2023年的成長率為1%。

- 根據日本汽車工業協會(JAMA)的報告,2022年日本的乘用車產量將為7,427,179輛,卡車產量將為1,286,414輛。這可能會對CNT市場產生影響。

- 因此,由於上述原因,預計亞太地區將在預測期內推動市場成長。

奈米碳管產業概況

全球奈米碳管市場本質上是部分整合的,由不同地區的少數國際和國內參與者組成。市場的主要企業包括 LG 化學、成都有機化學(Timesnano)、卡博特公司、江蘇天奈科技和 Nanocyl SA。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 驅動程式

- 奈米碳管在電動車的應用不斷擴大

- 許多應用領域對先進材料的需求不斷增加

- 限制因素

- 環境問題與健康與安全問題

- 其他阻礙因素

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

- 專利分析

第5章市場區隔

- 按類型

- 多壁奈米碳管(MWCNT)

- 單壁奈米碳管(SWCNT)

- 其他類型(扶手椅奈米碳管、鋸齒形奈米碳管管)

- 按最終用戶產業

- 電子產品

- 航太與國防

- 車

- 衛生保健

- 能源

- 其他終端用戶產業(紡織品、塑膠和複合材料、建築)

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 西班牙

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章競爭格局

- 併購、合資、合作與協議

- 市場佔有率(%)/排名分析

- 主要企業策略

- 公司簡介

- Arkema

- Cabot Corporation

- CHASM

- Chengdu Organic Chemicals Co. Ltd(Timesnano)

- Hyperion Catalysis International

- Jiangsu Cnano Technology Co. Ltd

- Kumho Petrochemical

- LG Chem

- Meijo Nano Carbon

- Nano-C

- Nanocyl SA

- Ocsial

- Raymor Industries Inc.

- Showa Denko KK(Resonac Holdings Corporation)

第7章 市場機會與未來趨勢

- 對能源儲存設備的需求不斷增加

- 製藥業備受追捧的材料

The Carbon Nanotubes Market size is estimated at USD 8.77 billion in 2025, and is expected to reach USD 39.02 billion by 2030, at a CAGR of 34.78% during the forecast period (2025-2030).

The COVID-19 pandemic posed various challenges in the Carbon nanotubes market but also represented opportunities for growth in specific areas. The industry has adapted to the changing landscape in the automotive sector and various other advanced applications, As the world is recovering from the pandemic, the carbon nanotubes market is gradually regaining its momentum and will continue to grow during the forecast period.

The market saw a rise in demand with the increase in applications in various industries, including energy, automotive, electronics, aerospace, and other such industrial applications.

In the medium term, the major factors driving the market studied are the growing usage of carbon nanotubes in electric vehicles and the increasing demand for advanced materials in numerous applications.

On the flip side, environmental concerns and health safety issues are anticipated to restrain the market growth.

Increasing demand for energy storage devices is expected to act as an opportunity for the market in the coming years.

Asia-Pacific accounted for the highest market share, and the region is expected to dominate the market during the forecast period.

Carbon Nanotubes Market Trends

Energy Segment to Dominate the Market

- Carbon nanotubes (CNTs) received much attention as catalyst support for energy applications, primarily solar cells, fuel cell catalysts, and hydrogen storage, due to their high surface area and conductivity. These unique properties allow CNTs to be used as supplemental material for energy conversion and storage devices.

- Renewable growth is propelled by more ambitious expansion policies in critical markets, partly in response to the current energy crisis. The accelerated adoption of renewable energy in the last five years' expansion rate results primarily from two factors.

- First, high fossil fuel and electricity prices resulting from the global energy crisis made renewable power technologies much more economically attractive,

- Second, Russia's invasion of Ukraine increasingly caused fossil fuel importers, especially in Europe, to value renewable energy's energy security benefits.

- China plans to install almost half of new global renewable power capacity over 2022-2027, as growth accelerates in the next five years despite the phaseout of wind and solar PV subsidies. Ambitious renewable energy targets in the 14th Five-Year Plan, market reforms, and provincial solid government support provide long-term revenue certainty for renewables.

- The European Union, the second-largest growth market after China, had stable renewable capacity expansion in the past five years compared to 2010-2015. But its pace of development is expected to more than double during 2022-2027. While several EU member countries had already introduced ambitious targets and policies to accelerate renewable energy deployment before Russia invaded Ukraine since then, the European Union proposed even more aggressive goals under the REPowerEU package to eliminate Russian fossil fuel imports by 2027.

- In the United States, renewable energy expansion almost doubled in the last five years. The IRA passed in August 2022 extended tax credits for renewables until 2032, providing unprecedented long-term visibility for wind and solar PV projects. In India, new installations are set to double over our forecast period, led by solar PV and driven by competitive auctions implemented to achieve the government's ambitious target of 500 GW of renewable power by 2030.

- Therefore, these factors are projected to boost the consumption of carbon nanotubes in the energy industry.

Asia-Pacific to Dominate the Market

- China is the largest producer and consumer of carbon nanomaterials in Asia-Pacific. The abundance of available raw materials and the low cost of production supported the growth of the carbon nanomaterials market in the country.

- Because of CNT's extraordinary electrical properties, CNT finds applications in electrical and electronic applications such as photovoltaics, sensors, semiconductor devices, displays, conductors, fuel cells, harvesters, and batteries.

- China includes the world's most extensive electronics production base and offers tough competition to existing upstream producers, such as South Korea, Singapore, and Taiwan. Electronic products, such as smartphones, OLED TVs, tablets, etc., include the highest growth in the market in the consumer electronics segment. With the increase in the disposable income of the middle-class population, the demand for electronic products is estimated to grow, thereby driving the CNT market shortly.

- The Indian government is talking with significant semiconductor companies to set up local manufacturing. The government invited new applications for setting up Semiconductor Fabs and Display Fabs in India from June 2023 under the Modified Semicon India Programme with an outlay of INR 76,000 crore (~10 billion USD).

- The country saw large investments in the automotive sector. Recent and planned investments and developments in the automobile sector include

- In January 2023, MG Motor India announced a USD 100 million investment to expand capacity. In December 2022, Mahindra & Mahindra revealed plans to invest INR 10,000 crore (USD 1.2 billion) in an EV manufacturing plant in Pune. This investment emphasizes the growing significance of the EV sector.

- Japan's electronic products industry is the most significant factor driving demand for semiconductor sales in Japan. Japan includes about 30 semiconductor fab industries that are involved in the manufacturing of various semiconductor chips. Japan's semiconductor production registered a 13% y-o-y in 2021 and 10% in 2022, with production value reaching JPY 3,074.6 billion (USD 23.31 billion). The growth for the year 2023 is forecasted at 1%.

- As per the reports by the Japan Automobile Manufacturers Association (JAMA), the country produced 7,427,179 units of passenger cars and 1,286,414 units of trucks in 2022. It is likely to impact the CNT market.

- Hence, due to the reasons mentioned above, Asia-Pacific is anticipated to drive the market's growth during the forecast period.

Carbon Nanotubes Industry Overview

The global carbon nanotube market is partially consolidated in nature, with a few international and domestic players across different regions. Some of the major companies in the market include LG Chem, Chengdu Organic Chemicals Co. Ltd (Timesnano), Cabot Corporation, Jiangsu Cnano Technology Co. Ltd, and Nanocyl SA, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Usage of Carbon Nantotubes in Electric Vehicles

- 4.1.2 Increasing Demand for Advance Materials in Numerous Applications

- 4.2 Restraints

- 4.2.1 Environmental Concerns and Health Safety Issues

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Patent Analysis

5 MARKET SEGMENTATION (Market Size in Value and Volume)

- 5.1 By Type

- 5.1.1 Multi-walled Carbon Nanotubes (MWCNT)

- 5.1.2 Single-walled Carbon Nanotubes (SWCNT)

- 5.1.3 Other Types (armchair carbon nanotubes and zigzag carbon nanotubes)

- 5.2 By End-user Industry

- 5.2.1 Electronics

- 5.2.2 Aerospace and Defense

- 5.2.3 Automotive

- 5.2.4 Healthcare

- 5.2.5 Energy

- 5.2.6 Other End-user Industries (Textiles, Plastics and Composites, and Construction)

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Spain

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers, Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Arkema

- 6.4.2 Cabot Corporation

- 6.4.3 CHASM

- 6.4.4 Chengdu Organic Chemicals Co. Ltd (Timesnano)

- 6.4.5 Hyperion Catalysis International

- 6.4.6 Jiangsu Cnano Technology Co. Ltd

- 6.4.7 Kumho Petrochemical

- 6.4.8 LG Chem

- 6.4.9 Meijo Nano Carbon

- 6.4.10 Nano-C

- 6.4.11 Nanocyl SA

- 6.4.12 Ocsial

- 6.4.13 Raymor Industries Inc.

- 6.4.14 Showa Denko KK (Resonac Holdings Corporation)

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Demand for Energy Storage Devices

- 7.2 Highly Desired Material in the Pharmaceutical Sector

2025年碳奈米材料全球市場報告

2025年碳奈米材料全球市場報告 2030 年單壁奈米碳管市場預測:按產品類型、合成方法、應用、最終用戶和地區進行的全球分析

2030 年單壁奈米碳管市場預測:按產品類型、合成方法、應用、最終用戶和地區進行的全球分析 奈米碳管市場規模、佔有率、趨勢分析報告:2025 年至 2030 年按產品、應用、地區和細分市場預測石墨烯增強混凝土市場:2033 年市場分析與預測 - 按類型、產品、技術、應用、形式、材料類型、最終用戶、功能、施工類型、解決方案

奈米碳管市場規模、佔有率、趨勢分析報告:2025 年至 2030 年按產品、應用、地區和細分市場預測石墨烯增強混凝土市場:2033 年市場分析與預測 - 按類型、產品、技術、應用、形式、材料類型、最終用戶、功能、施工類型、解決方案 奈米管:市場佔有率分析、產業趨勢、成長預測(2025-2030)

奈米管:市場佔有率分析、產業趨勢、成長預測(2025-2030) 奈米碳管(CNT)市場:現狀分析與預測(2024-2032年)奈米碳管市場規模、佔有率、成長分析、按產品類型、按方法、按應用、按最終用戶、按地區 - 產業預測,2024-2031 年

奈米碳管(CNT)市場:現狀分析與預測(2024-2032年)奈米碳管市場規模、佔有率、成長分析、按產品類型、按方法、按應用、按最終用戶、按地區 - 產業預測,2024-2031 年 奈米碳窗膜市場報告:2030 年趨勢、預測與競爭分析

奈米碳窗膜市場報告:2030 年趨勢、預測與競爭分析 奈米碳管的全球市場:按類型、按方法、按最終用途行業、按地區 - 預測至 2029 年

奈米碳管的全球市場:按類型、按方法、按最終用途行業、按地區 - 預測至 2029 年 碳奈米材料市場:按材料、製造方法、最終用戶產業分類 - 2025-2030 年全球預測

碳奈米材料市場:按材料、製造方法、最終用戶產業分類 - 2025-2030 年全球預測