|

市場調查報告書

商品編碼

1686300

丙烯腈丁二烯苯乙烯 (ABS) 樹脂:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Acrylonitrile Butadiene Styrene (ABS) Resin - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

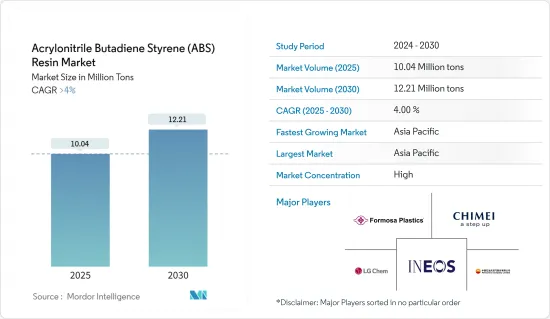

丙烯腈丁二烯苯乙烯 (ABS) 樹脂市場規模預計在 2025 年為 1,004 萬噸,預計在 2030 年達到 1,221 萬噸,預測期間(2025-2030 年)的複合年成長率將超過 4%。

ABS 樹脂市場受到 COVID-19 的嚴重影響。由於經濟放緩,市場面臨勞動力短缺、運輸和原料短缺等多重挑戰。然而,隨著大多數國家放鬆封鎖措施後全球製造和進出口活動迅速增加,對 ABS 樹脂的需求正在激增。

主要亮點

- 推動市場發展的首要因素是人們對汽車輕量化的日益關注以及在電子和消費品領域的應用不斷擴大。

- 然而,預計 ABS 替代品的可用性是預測期內抑制該行業成長的主要因素。

- 然而,PC-ABS樹脂在工業應用中的使用越來越廣泛,可能為全球市場提供有利的成長機會。

- 亞太地區佔全球市場主導地位,其中中國和印度等國家消費量最高。

丙烯腈丁二烯苯乙烯 (ABS) 樹脂的市場趨勢

電子及家電產業需求不斷成長

- ABS 在電子領域的應用主要包括傳輸電力的塑膠零件。這包括盒子、外殼、線槽、塑膠機殼等。

- ABS樹脂具有優異的抗衝擊性、耐久性、重量輕和阻燃性。因此在電子設備中被廣泛應用。此外,隨著電子元件日益小型化以及整個產業的安全措施不斷加強,電子應用對 ABS 樹脂的需求預計將會增加。

- 全球電子產業正在經歷巨大的成長。亞太地區佔全球電子產品產量的70%以上,韓國、日本和中國等國家參與製造各種電氣元件並供應全球各產業。此外,預計2025年印度將成為全球第五大家電和電子產業國。

- 預計2024年中國消費電子市場將反彈並實現正成長。中國家電零售總額預計將達到人民幣2.2兆元(3,050億美元),預計2024年成長率將進一步回升至5%。

- 由於終端消費者的需求旺盛,德國的電氣和電子產業在歐洲佔有最大的佔有率。此外,該行業還得到了跨國電子製造商的大力支持,滿足了該國廣泛的需求。電氣工程業佔德國工業總產值的11%。

- 在美國,電子產業的發展主要靠家用電子電器的銷售。此外,由於美國工業活動的不斷增加,工業電子在過去十年中發展勢頭強勁。預計電視、行動電話電腦和智慧型裝置等家用電子電器的高需求將增加塑膠產品的使用量,對市場產生正面影響。

- 在預測期內,ABS 樹脂市場可能會受到全球電子和家電行業持續擴張的推動。

亞太地區佔市場主導地位

- 隨著 ABS 樹脂在蓬勃發展的汽車產業中取代傳統塑膠,亞太地區的 ABS 樹脂市場正在快速成長。

- 在全球汽車總產量約6,900萬輛中,中國產量約佔34%。根據歐洲汽車工業協會(ACEA)的數據,日本和韓國佔其中的14.7%,南亞約佔10.8%。

- 而且,中國的汽車製造業是全世界最大的。根據國際汽車工業組織(OICA)的數據,該國的汽車產量將在2022年達到2,700萬輛,比2021年的2,608萬輛增加3%。

- 據估計,中國是世界上最大的電子製造基地之一。智慧型手機、電視、電線電纜、可攜式電腦、遊戲系統和其他個人電子設備等電子產品在電子產業中錄得最高成長。預計這將促進該國的 ABS 消費。

- 據印度投資局稱,印度電子產品市場價值 1,550 億美元,其中 65% 來自國內市場。顯示器市場正在成長,預計到 2025 年將成長到 150 億美元。 23 會計年度,印度的電子產品進口額成長 8%,達到 878.5 億美元。此外,印度國內生產年複合成長率率為 13%,從 2017 會計年度的490 億美元增至 2023 會計年度的總合億美元。

- 日本政府正在增加對電動車的補貼,並計劃在2030年將電動車充電站的數量增加到15萬個。因此,汽車產業的復甦可能會提振日本的ABS市場。

- 根據世界銀行預測,2022年韓國家庭人均支出與前一年同期比較增加4.6%。這種支出增加的趨勢可能會在未來幾年促進許多使用丙烯腈丁二烯苯乙烯 (ABS) 的產品的銷售,包括汽車、家用電器等。

- 因此,預計所有這些因素都將在預測期內影響亞太地區對丙烯腈丁二烯苯乙烯 (ABS) 樹脂市場的需求。

丙烯腈丁二烯苯乙烯 (ABS) 樹脂產業概況

丙烯腈丁二烯苯乙烯 (ABS) 樹脂市場本質上是整合的。主要企業(不分先後順序)包括 LG 化學、奇美、英力士、台塑和中國石油天然氣有限公司。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 驅動程式

- 人們對輕型汽車的興趣日益濃厚

- 在電子產品和消費品中的應用日益廣泛

- 限制因素

- ABS 替代方案的可用性

- 其他阻礙因素

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

- 價格趨勢

- 監理政策

第5章 市場區隔

- 行程類型

- 注射吹塑成型

- 擠出吹塑成型

- 注拉伸吹塑成型

- 最終用戶產業

- 汽車和運輸

- 建築學

- 電子產品

- 消費品和家用電器

- 其他最終用戶產業

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 泰國

- 越南

- 馬來西亞

- 印尼

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 俄羅斯

- 土耳其

- 北歐的

- 西班牙

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 卡達

- 奈及利亞

- 阿拉伯聯合大公國

- 埃及

- 其他中東和非洲地區

- 亞太地區

第6章 競爭格局

- 併購、合資、合作、協議

- 市場佔有率(%)**/排名分析

- 主要企業策略

- 公司簡介

- ABS樹脂製造商

- CHIMEI

- Formosa Plastics Corporation

- LOTTE Chemical Corporation

- PetroChina Company Limited

- JSR Corporation

- Trinseo

- INEOS Styrolution Group GmbH

- LG Chem

- SABIC

- TORAY INDUSTRIES INC.

- Springboard(Stack Plastics)

- DONGGUAN SINCERE TECH CO. LTD

- Jaco Products

- ReblingPower Connectors

- AcoMold Co Limited

- Rutland Plastics

- HTI Plastics

- EX MOULD Co. Ltd

- ABS樹脂製造商

第7章 市場機會與未來趨勢

- 擴大 PC-ABS 樹脂在工業應用的使用

The Acrylonitrile Butadiene Styrene Resin Market size is estimated at 10.04 million tons in 2025, and is expected to reach 12.21 million tons by 2030, at a CAGR of greater than 4% during the forecast period (2025-2030).

The ABS resin market has been significantly impacted due to COVID-19. The market has faced several challenges, such as labor shortages, transportation, and raw material shortages due to the economic slowdown. However, after the relaxation of the lockdown process in most countries, demand for ABS resins is surging as global manufacturing and export-import activities are rapidly increasing.

Key Highlights

- Major factors driving the market are the growing focus on lightweight automobiles and the increasing usage of electronics and consumer goods.

- However, the availability of substitutes for ABS is a key factor anticipated to restrain the growth of the target industry during the forecast period.

- However, the growing usage of PC-ABS resin in industrial applications will likely create lucrative growth opportunities in the global market.

- Asia-Pacific dominated the global market, with the largest consumption from countries like China and India.

Acrylonitrile Butadiene Styrene (ABS) Resin Market Trends

Increasing Demand in the Electronics and Appliances Industry

- The electronics applications for ABS resin mainly include plastic components for electricity transfer. These include boxes, casings, wiring channels, and plastic enclosures.

- ABS plastics are impact-resistant, durable, lightweight, and flame-retardant. Thus, they are widely used in electronics. Moreover, the growing miniaturization of electronic components and increased safety measures across industries are expected to increase the demand for ABS resin in electronics applications.

- The global electronics industry has witnessed massive growth. Asia-Pacific accounts for more than 70% of global electronics production, with countries like South Korea, Japan, and China involved in manufacturing various electrical components and supplying them to various industries globally. Additionally, India is expected to become the world's fifth-largest consumer electronics and appliances industry by 2025.

- China's consumer electronics market is set to bounce back with positive growth in 2024, driven by growing market demand and innovation while increasing retail spending. China's total retail sales of consumer electronics are expected to reach CNY 2.2 trillion (USD 305 billion), and the growth rate is expected to increase further to 5% in 2024.

- The German electrical and electronics industry in Europe accounts for the largest share due to high end-consumer demand. Moreover, the industry is supported by a strong presence of multinational electronics manufacturers catering to the wide demand in the country. The electrical industry accounted for 11% of the total industrial production in Germany.

- The sales of consumer electronics primarily drive the electronics industry in the United States. Moreover, industrial electronics have gained momentum in the past decade owing to the rise in industrial operations across the United States. The high demand for consumer electronics, including television, mobile phones, laptops, and smart gadgets, is expected to increase the utilization of plastic products, thereby positively impacting the market.

- During the forecast period, the market for ABS resin is likely to be driven by continued expansion in the global electronics and appliances industry.

Asia-Pacific to Dominate the Market

- The market for ABS witnessed rapid growth in Asia-Pacific, owing to the increased replacement of traditional plastics by ABS in the growing automotive industry.

- China manufactures about 34% of approximately 69 million cars worldwide each year. Japan and South Korea account for 14.7% of that volume, and South Asia accounts for around 10.8% of that volume, according to the European Automobile Manufacturers Association (ACEA).

- Moreover, the Chinese automotive manufacturing industry is the largest in the world. In 2022, the automotive production in the country reached 27 million, which increased by 3%, compared to 26.08 million vehicles produced in 2021, according to the International Organization of Motor Vehicle Manufacturers (OICA)

- China is estimated to be one of the world's largest electronics production bases. Electronic products, such as smartphones, TVs, wires, cables, portable computing devices, gaming systems, and other personal electronic devices, recorded the highest growth in the electronics segment. This is expected to drive the country's consumption of ABS.

- As per Invest India, the electronics market in India is worth USD 155 billion, with 65% of the total market being domestic. The display market is growing and is expected to grow to USD 15 billion by 2025. In FY23, electronic goods imported into India increased 8% to USD 87.85 billion. Moreover, India's domestic production registered a 13% compound annual growth rate from FY17's total of USD 49 billion to FY23's total of USD 101 billion.

- The Government of Japan has raised subsidies for EVs and aims to increase the number of EV charging stations to 150,000 by 2030. Thus, reviving the automotive industry is likely to boost the ABS market in the country.

- According to the World Bank, household expenditure per capita in South Korea grew 4.6% in 2022 over the previous year. Such growth trends in expenditure will increase the sales of numerous products, including automotive, consumer electronics, and others that utilize acrylonitrile butadiene styrene (ABS) in the coming years.

- Therefore, all these factors are expected to affect the demand in the Asia-Pacific acrylonitrile butadiene styrene resin market during the forecast period.

Acrylonitrile Butadiene Styrene (ABS) Resin Industry Overview

The acrylonitrile butadiene styrene (ABS) resin market is consolidated in nature. Some major key players (not in any particular order) include LG Chem, CHIMEI, INEOS, Formosa Plastics, and PetroChina Company Limited.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Focus on Lightweight Automobiles

- 4.1.2 Increasing Usage in Electronics and Consumer Goods

- 4.2 Restraints

- 4.2.1 Availability of Substitutes for ABS

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Price Trends

- 4.6 Regulatory Policies

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Process Type

- 5.1.1 Injection Blow Molding

- 5.1.2 Extrusion Blow Molding

- 5.1.3 Injection Stretch Blow Molding

- 5.2 End-user Industry

- 5.2.1 Automotive and Transportation

- 5.2.2 Construction

- 5.2.3 Electronics

- 5.2.4 Consumer Goods and Appliances

- 5.2.5 Other End-user Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Thailand

- 5.3.1.6 Vietnam

- 5.3.1.7 Malaysia

- 5.3.1.8 Indonesia

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Russia

- 5.3.3.6 Turkey

- 5.3.3.7 NORDIC

- 5.3.3.8 Spain

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Qatar

- 5.3.5.4 Nigeria

- 5.3.5.5 United Arab Emirates

- 5.3.5.6 Egypt

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Manufacturers of ABS Resins

- 6.4.1.1 CHIMEI

- 6.4.1.2 Formosa Plastics Corporation

- 6.4.1.3 LOTTE Chemical Corporation

- 6.4.1.4 PetroChina Company Limited

- 6.4.1.5 JSR Corporation

- 6.4.1.6 Trinseo

- 6.4.1.7 INEOS Styrolution Group GmbH

- 6.4.1.8 LG Chem

- 6.4.1.9 SABIC

- 6.4.1.10 TORAY INDUSTRIES INC.

- 6.4.1.11 Springboard (Stack Plastics)

- 6.4.1.12 DONGGUAN SINCERE TECH CO. LTD

- 6.4.1.13 Jaco Products

- 6.4.1.14 ReblingPower Connectors

- 6.4.1.15 AcoMold Co Limited

- 6.4.1.16 Rutland Plastics

- 6.4.1.17 HTI Plastics

- 6.4.1.18 EX MOULD Co. Ltd

- 6.4.1 Manufacturers of ABS Resins

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing usage of PC-ABS Resin in Industrial Applications

全球再生 ABS 樹脂市場:2031 年預測

全球再生 ABS 樹脂市場:2031 年預測 全球丙烯腈丁二烯苯乙烯市場報告:趨勢、預測和競爭分析(至 2031 年)

全球丙烯腈丁二烯苯乙烯市場報告:趨勢、預測和競爭分析(至 2031 年) 丙烯腈丁二烯苯乙烯市場規模、佔有率、趨勢分析報告:按類型、應用、地區、細分市場預測,2025-2030 年

丙烯腈丁二烯苯乙烯市場規模、佔有率、趨勢分析報告:按類型、應用、地區、細分市場預測,2025-2030 年 丙烯睛-丁二烯-苯乙烯塑膠的全球市場:市場規模·佔有率·趨勢,產業分析 (各產品種類·各終端用戶·各地區),未來預測 (2025年~2034年)

丙烯睛-丁二烯-苯乙烯塑膠的全球市場:市場規模·佔有率·趨勢,產業分析 (各產品種類·各終端用戶·各地區),未來預測 (2025年~2034年) 丙烯腈丁二烯苯乙烯(ABS)全球市場(2025-2029)

丙烯腈丁二烯苯乙烯(ABS)全球市場(2025-2029) 丙烯腈丁二烯苯乙烯 (ABS) 市場規模、佔有率和成長分析(按應用、製程、最終用戶產業和地區):產業預測 (2024-2031)

丙烯腈丁二烯苯乙烯 (ABS) 市場規模、佔有率和成長分析(按應用、製程、最終用戶產業和地區):產業預測 (2024-2031) 丙烯腈丁二烯聚苯乙烯樹脂市場:按成分、製造流程、類型、等級、最終用途產業 - 2025-2030 年全球預測丙烯腈丁二烯苯乙烯市場:按產品類型、製造流程、等級、形式、最終用途產業 - 全球預測 2025-2030ABS(丙烯□丁二烯苯乙烯)全球市場:產業分析、規模、佔有率、成長、趨勢、預測(2024-2031)丙烯腈丁二烯苯乙烯(ABS)全球市場(2016-2036)

丙烯腈丁二烯聚苯乙烯樹脂市場:按成分、製造流程、類型、等級、最終用途產業 - 2025-2030 年全球預測丙烯腈丁二烯苯乙烯市場:按產品類型、製造流程、等級、形式、最終用途產業 - 全球預測 2025-2030ABS(丙烯□丁二烯苯乙烯)全球市場:產業分析、規模、佔有率、成長、趨勢、預測(2024-2031)丙烯腈丁二烯苯乙烯(ABS)全球市場(2016-2036)