|

市場調查報告書

商品編碼

1686590

矽膠:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Silicone - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

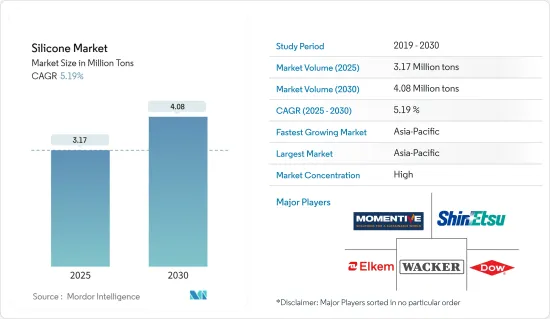

預計2025年矽膠市場規模為317萬噸,預計2030年將達到408萬噸,預測期內(2025-2030年)的複合年成長率為5.19%。

COVID-19 阻礙了矽膠市場的發展。在疫情初期,封鎖和旅行限制擾亂了全球供應鏈,導致原料採購延遲和生產停頓。這導致矽膠產品暫時短缺,影響了我們的製造業務。然而,隨著封鎖措施的放鬆和經濟活動的恢復,汽車、建築、電子和醫療保健等行業對矽膠的需求龐大。

推動矽膠市場發展的因素主要有:醫療保健產業矽膠的使用量不斷增加、電力傳輸和配電產業的需求不斷成長、以及汽車產業矽膠的應用不斷增加。

然而,政府法規和替代品的競爭預計將阻礙市場成長。

預測期內,各類終端用戶對電活性聚合物 (EAP) 的潛在需求不斷成長,以及有機矽膠材料對建築能源效率和永續性的貢獻不斷增加,可能會為矽膠市場帶來機會。

預計亞太地區將在矽膠市場中佔據主導地位,其中中國和印度將引領該地區的成長。

矽膠市場趨勢

工業製程部門主導市場

- 矽膠在製造過程領域的主要應用包括消泡劑、工業被覆劑、流體、油、常溫硫化密封劑、模製品和聚合物添加劑。

- 矽膠廣泛應用於海上鑽井,由於空間和重量的限制,泡沫和廢棄物管理至關重要。矽膠可以釋放鑽井泥漿中滯留的氣體。由於泡沫具有破壞性並且需要耗時的維護,消泡劑可以減少消費量和化學品的使用,同時提高產量。

- 因此,全球石油和天然氣工業的擴張預計將有利於矽膠的需求。預計各種正在進行的擴建計劃將推動成長。印度是亞太地區石油和天然氣領域的重要經濟體。根據印度品牌股權基金會(IBEF)發布的報告,預計到2045年印度的石油需求將達到1,100萬桶。此外,到2024年底,印度的天然氣消費量預計將增加250億立方公尺。

- 此外,根據能源研究所發布的資料,2022年全球石油產量將達44.72億噸。

- 此外,根據石油輸出國組織(OPEC)發布的報告,原油需求正在增加,到2023年將增加至每天1.189億桶。這將導致石油和天然氣產業對矽膠的需求增加。

- 中國海關資料顯示,2023年,中國作為全球最大的原油進口國,原油進口量為1,130萬桶/日,較上年增加10%。 2023年,中國煉油廠進口的原油數量超過其他國家,以滿足運輸燃料的需求,並為越來越多的石化產品生產原料。

- 由於上述因素,預測期內市場預計將復甦並以穩定的速度成長。

亞太地區可望主導市場

- 亞太地區是最大的矽膠消費地區,其中中國、印度和日本市場引領該地區的成長。

- 半導體是電子產業的重要組成部分之一,矽膠用於封裝、塗覆和黏附矽膠、PCB 和 ECU 以提供保護。根據半導體產業協會和世界半導體貿易統計組織(WSTS)的數據顯示,2023年1月中國半導體銷售額為116.6億美元。

- 此外,中國擁有幾家大型造船集團,包括中國船舶重工集團公司(CSIC)、中國船舶工業集團公司(CSSC)、中遠海運集團、招商局國際和中國外運。中國造船廠建造的船舶種類繁多,包括貨船、貨櫃船、油輪、海軍船、客輪和豪華遊輪,這產生了對矽的需求。

- 此外,根據印度品牌股權基金會(IBEF)的預測,到2025年,印度對半導體產品的需求預計將達到4,000億美元。北方邦政府也致力於成為該國的半導體中心,因為與生產連結獎勵計畫預計將幫助印度從晶片產業7,600億印度盧比(90.9366億美元)的投資中獲益。

- 2024年中國家電市場將復甦並實現正成長。預計2024年,中國電力零售總額將達2.2兆元(3,050億美元),成長速度將進一步回升至5%。

- 因此,預計上述因素將在預測期內促進亞太地區對矽膠的需求增加。

矽膠產業概況

矽膠市場正在整合。主要企業(排名不分先後)包括瓦克化學股份公司、陶氏化學、信越化學、邁圖和埃肯公司。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 驅動程式

- 在汽車產業的應用日益廣泛

- 擴大醫療保健產業的應用

- 輸配電產業需求不斷成長

- 限制因素

- 政府法規

- 與替代品的競爭

- 價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場區隔

- 按形式

- 彈性體

- 體液

- 樹脂

- 其他

- 按最終用戶

- 運輸

- 建築材料

- 電子產品

- 衛生保健

- 工業流程

- 個人護理和消費品

- 其他最終用戶(紡織品和塗料)

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 泰國

- 馬來西亞

- 印尼

- 越南

- 東南亞國協

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 西班牙

- 土耳其

- 俄羅斯

- 北歐的

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 奈及利亞

- 卡達

- 埃及

- 阿拉伯聯合大公國

- 其他中東和非洲地區

- 亞太地區

第6章 競爭格局

- 併購、合資、合作與協議

- 市場佔有率(%)**/排名分析

- 主要企業策略

- 公司簡介

- BRB International(PETRONAS Chemicals Group Berhad)

- CHT Germany GmbH

- Dow

- DyStar Singapore Pte Ltd

- Elkem ASA

- Evonik Industries AG

- Hoshine Silicon Industry Co. Ltd

- Jiangsu Mingzhu Silicone Rubber Material Co. Ltd

- KANEKA CORPORATION

- Mitsubishi Chemical Corporation

- Momentive

- Shin-Etsu Chemical Co. Ltd

- Wacker Chemie AG

- Wynca Tinyo Silicone Co. Ltd

- Zhejiang Sucon Silicone Co. Ltd

第7章 市場機會與未來趨勢

- 電活性聚合物(EAP)的潛在需求成長

- 矽膠材料對建築能源效率和永續性的貢獻日益增強

The Silicone Market size is estimated at 3.17 million tons in 2025, and is expected to reach 4.08 million tons by 2030, at a CAGR of 5.19% during the forecast period (2025-2030).

COVID-19 hampered the silicone market. During the early stages of the pandemic, lockdowns and restrictions on movement disrupted global supply chains, leading to delays in raw material procurement and production shutdowns. This resulted in temporary shortages of silicone products and impacted manufacturing operations. However, as lockdown measures eased and economic activities resumed, enormous demand for silicone was released across various industries such as automotive, construction, electronics, and healthcare.

The major factors driving the silicone market are the increased usage of silicone in the healthcare industry, the growing demand from the power transmission and distribution segment, and rising applications of silicone in the automotive industry.

On the flip side, government regulations and competition from substitutes are expected to hinder the growth of the market.

Rising potential demand for electroactive polymers (EAP) from various end users and increasing contribution of silicone-based materials to energy efficiency and sustainability in construction are likely to act as an opportunity in the silicone market during the forecast period.

Asia-Pacific is expected to dominate the silicone market among other regions, with China and India leading the region's growth.

Silicone Market Trends

The Industrial Processes Segment to Dominate the Market

- The main applications of silicones in the field of manufacturing processes include antifoaming agents, industry coatings, fluids and oils, room-temperature vulcanizing sealants, moldings, and additives for polymers.

- Silicones are widely used in offshore drilling because of space and weight limitations, where the management of foam and waste is essential. Silicones allow the gas trapped in the drilling mud to be released. Due to the presence of foam, which hinders the process and requires time for maintenance work, antifoaming agents reduce energy consumption and chemical use while boosting production.

- Thus, expanding the global oil and gas industry is anticipated to benefit from the demand for silicone. Various expansion projects underway are expected to drive the growth. India is a significant economy in Asia-Pacific in the oil and gas segment. According to the report released by the India Brand Equity Foundation (IBEF), the oil demand in India is projected to reach 11 million barrels by 2045. In addition, India's natural gas consumption is expected to increase by 25 billion cubic meters by the end of 2024.

- Moreover, according to the data published by the Energy Institute, global oil production reached 4,407.2 million metric tons in 2022.

- Also, according to the report released by the Organization of the Petroleum Exporting Countries (OPEC), there is a rise in demand for crude oil, which increased to 101.89 million barrels per day in 2023. This leads to increased demand for silicone from the oil and gas industries.

- In 2023, China, the globe's top importer of crude oil, brought in 11.3 million barrels of crude oil daily, marking a 10% rise from the previous year, as per data from China's customs. Refineries in China saw their highest crude oil imports in 2023 to meet the nation's rising demand for refining, aiming to meet transportation fuel needs and generate raw materials for its expanding petrochemical.

- Due to all the above factors, the market is expected to witness post-recovery solid growth during the forecast period.

Asia-Pacific is Expected to Dominate the Market

- Asia-Pacific is the largest consumer of silicone, with the Chinese, Indian, and Japanese markets driving growth in the region over the years.

- Semiconductors are one of the significant parts of the electronics segment, which involves the usage of silicones as silicone encapsulates, coats, and adheres to the protection of semiconductors, PCBs, and ECUs. According to the Semiconductor Industry Association and the World Semiconductor Trade Statistics (WSTS), the semiconductor sales value in China stood at USD 11.66 billion in January 2023.

- Moreover, China has several large shipbuilding conglomerates, including China Shipbuilding Industry Corporation (CSIC), China State Shipbuilding Corporation (CSSC), COSCO shipping, CMHI, and Sinotrans. China's shipyards build a wide variety of ships, including freighters, containerships, oil tankers, naval vessels, passenger craft, luxury carriers, and so on, which leads to the demand for silicone.

- Also, according to the India Brand Equity Foundation (IBEF), the demand for semiconductor goods in India is expected to be USD 400 billion by FY 2025. The Government of Uttar Pradesh also aims to become a semiconductor hub in the country, given that India is estimated to benefit from INR 76,000 crore (USD 9,093.66 million) as an investment into the chip industry under the Production Linked Incentive scheme.

- China's consumer electronics market is set to bounce back with positive growth in 2024, driven by growing market demand and innovation while increasing retail spending. China's total retail sales of consumer electronics are expected to reach CNY 2.2 trillion (USD 305 billion), and the growth rate is expected to increase further to 5% in 2024.

- Thus, the above-mentioned factors are expected to contribute to the increasing demand for silicone in Asia-Pacific during the forecast period.

Silicone Industry Overview

The silicone market is consolidated. The major players (not in any particular order) include Wacker Chemie AG, Dow, Shin-Etsu Chemical Co. Ltd, Momentive, and Elkem ASA.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Rising Application in Automotive Industry

- 4.1.2 Increasing Usage in Healthcare Industry

- 4.1.3 Growing Demand from Power Transmission and Distribution

- 4.2 Restraints

- 4.2.1 Government Regulation

- 4.2.2 Competition from Substitutes

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Form

- 5.1.1 Elastomers

- 5.1.2 Fluids

- 5.1.3 Resins

- 5.1.4 Other Forms

- 5.2 End User

- 5.2.1 Transportation

- 5.2.2 Construction Materials

- 5.2.3 Electronics

- 5.2.4 Healthcare

- 5.2.5 Industrial Processes

- 5.2.6 Personal Care and Consumer Products

- 5.2.7 Other End Users (Textiles and Coatings)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Thailand

- 5.3.1.6 Malaysia

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 ASEAN Countries

- 5.3.1.10 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Spain

- 5.3.3.6 Turkey

- 5.3.3.7 Russia

- 5.3.3.8 NORDIC

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Nigeria

- 5.3.5.4 Qatar

- 5.3.5.5 Egypt

- 5.3.5.6 United Arab Emirates

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 BRB International (PETRONAS Chemicals Group Berhad)

- 6.4.2 CHT Germany GmbH

- 6.4.3 Dow

- 6.4.4 DyStar Singapore Pte Ltd

- 6.4.5 Elkem ASA

- 6.4.6 Evonik Industries AG

- 6.4.7 Hoshine Silicon Industry Co. Ltd

- 6.4.8 Jiangsu Mingzhu Silicone Rubber Material Co. Ltd

- 6.4.9 KANEKA CORPORATION

- 6.4.10 Mitsubishi Chemical Corporation

- 6.4.11 Momentive

- 6.4.12 Shin-Etsu Chemical Co. Ltd

- 6.4.13 Wacker Chemie AG

- 6.4.14 Wynca Tinyo Silicone Co. Ltd

- 6.4.15 Zhejiang Sucon Silicone Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Rising Potential Demand For Electro Active Polymers (EAP)

- 7.2 Increasing Contribution of Silicone-based Materials to Energy-efficiency and Sustainability in Construction

全球汽車矽膠市場報告 - 產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年

全球汽車矽膠市場報告 - 產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年 2025 年全球汽車矽膠市場報告2025 年電氣和電子產品全球矽膠市場報告

2025 年全球汽車矽膠市場報告2025 年電氣和電子產品全球矽膠市場報告 汽車護理產品中矽膠的市場規模、佔有率和趨勢分析報告:按產品、應用、最終用途、地區和細分市場預測,2025-2030 年

汽車護理產品中矽膠的市場規模、佔有率和趨勢分析報告:按產品、應用、最終用途、地區和細分市場預測,2025-2030 年 醫用級矽膠市場報告:2031 年趨勢、預測與競爭分析2025 年全球重型機械矽膠市場報告

醫用級矽膠市場報告:2031 年趨勢、預測與競爭分析2025 年全球重型機械矽膠市場報告 2025 年至 2033 年期間矽膠市場報告,按產品類型(彈性體、流體、凝膠、樹脂)、應用(工業流程、建築材料、家庭和個人護理、交通運輸、能源、醫療保健、電子等)和地區分類

2025 年至 2033 年期間矽膠市場報告,按產品類型(彈性體、流體、凝膠、樹脂)、應用(工業流程、建築材料、家庭和個人護理、交通運輸、能源、醫療保健、電子等)和地區分類 矽膠薄膜市場規模、佔有率和成長分析(按類型、最終用途和地區)- 產業預測 2025-20322033 年矽膠市場分析及預測:按類型、產品、應用、技術、形式、最終用戶、材料類型、功能和解決方案

矽膠薄膜市場規模、佔有率和成長分析(按類型、最終用途和地區)- 產業預測 2025-20322033 年矽膠市場分析及預測:按類型、產品、應用、技術、形式、最終用戶、材料類型、功能和解決方案 汽車矽膠市場:全球產業分析、市場規模、佔有率、成長、趨勢與未來預測(2025-2032 年)

汽車矽膠市場:全球產業分析、市場規模、佔有率、成長、趨勢與未來預測(2025-2032 年)