|

市場調查報告書

商品編碼

1686592

三聚氰胺:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Melamine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

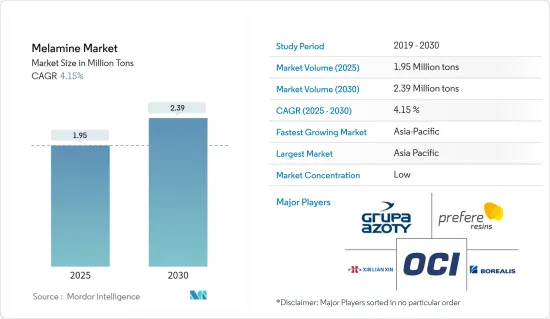

預計2025年三聚氰胺市場規模為195萬噸,預計2030年將達到239萬噸,預測期(2025-2030年)的複合年成長率為4.15%。

2020年,三聚氰胺市場在新冠疫情期間受到負面影響。 2021年,市場有所改善。建築和汽車製造活動從封鎖中恢復,對層壓板、油漆、被覆劑和木材黏合劑等建築材料的需求增加了。建設產業正在迅速復甦,預計未來幾年將進一步成長,這可能會增加對三聚氰胺的需求。

主要亮點

- 短期內,建設產業對層壓板、塗料和木材黏合劑的需求不斷成長,預計將推動市場成長。

- 液化木材、大豆和粉末塗料等替代品的出現,以及消費者對三聚氰胺基成型化合物甲醛排放的日益擔憂,預計會阻礙市場的成長。

- 然而,三聚氰胺基發泡體的成長趨勢很可能在未來成為一個機會。

- 亞太地區佔全球市場主導地位,其中中國和印度的消費量最大。

三聚氰胺黏合劑的市場趨勢

層壓板佔據市場主導地位

- 三聚氰胺樹脂是用於製造層壓板、檯面和桌面、廚櫃、地板、家具等的外層和裝飾層的首選聚合物。

- 三聚氰胺樹脂具有硬度、透明度、抗污性、不變色性和整體耐用性。在本應用中,用於浸潤覆蓋層和裝飾板的樹脂是透過每莫耳三聚氰胺與約兩莫耳甲醛發生反應而製備的。

- 這些板材通常應用於牆壁、柱子、桌面、家具、懸吊天花板等表面裝飾計劃。

- 據加拿大建築協會稱,建築業是加拿大最大的就業行業之一,為該國的經濟成功做出了重大貢獻。它是加拿大經濟的支柱。據加拿大建築協會稱,建築業僱用了超過 140 萬人,每年為加拿大經濟貢獻約 1,410 億美元。它也佔國內生產總值(GDP)的7.5%。

- 根據美國人口普查資料,2022 年 2 月的總建築支出約為 17,044 億美元,而 2022 年 1 月為 1,6955 億美元。

- 根據美國人口普查局的數據,2022 年 7 月美國住宅建築業成長 14%,達到 9,297 億美元,而 2021 年 7 月為 8,155 億美元。破舊的住宅通常需要增加新功能並修理或更換舊零件,這表明改造市場正在成長。全國各地住宅的上漲也鼓勵住宅在住宅維修上花費更多。

亞太地區佔市場主導地位

- 亞太地區佔據整體市場佔有率的主導地位。中國、印度和日本的建設活動不斷增加,推動了對層壓板、木材膠粘劑以及油漆和被覆劑的需求,從而導致該地區三聚氰胺的使用量增加。

- 中國佔全球塗料市場的四分之一以上。根據中國塗料工業協會統計,近年來,該產業成長率達7%。

- 中國政府已啟動一項大規模建設計畫,其中包括在未來十年內將 2.5 億人遷移到新的特大城市。這些計劃可能會增加對油漆的需求,而油漆的配方中會用到三聚氰胺。

- 預計2023年至2026年中國整體建設產業將實際成長4.6%。根據中國國家統計局發布的報告,2022年上半年交通運輸投資成長了6.7%。

- 印度政府與日本政府合作啟動了德里-孟買工業走廊計畫。該計畫旨在向德里-孟買工業走廊地區投資 2,000 億美元,開發一座新的工業城市。班加羅爾-清奈走廊等地區也可能推出類似的計畫。

- 根據中國民航局介紹,目前,政府已復工80%以上的機場計劃,全國共有65個機場計劃復工。其中國家重大機場計劃27個。預計這些計劃將增加三聚氰胺的需求。

三聚氰胺黏合劑產業概況

三聚氰胺市場較為分散,五大主要企業佔總產能的約40%。這些公司包括(不分先後順序):OCI NV、Borealis AG、河南心連心化工集團、Prefere Resins Holding GmbH 和 Grupa Azoty。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 驅動程式

- 建設產業需求強勁

- 其他促進因素

- 限制因素

- 消費者越來越擔心三聚氰胺基模塑膠的甲醛釋放量

- 液化木材、大豆和粉末塗料等替代品的可用性

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

- 原料分析和趨勢

- 生產流程

- 進出口趨勢

- 價格趨勢

- 專利分析

- 監理政策分析

第5章 市場區隔

- 應用

- 層壓板

- 木材膠黏劑

- 模塑膠

- 油漆和塗料

- 其他用途(阻燃劑、纖維樹脂)

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 俄羅斯

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭格局

- 併購、合資、合作、協議

- 市場佔有率(%)分析

- 主要企業策略

- 公司簡介

- BASF SE

- Borealis AG

- Cornerstone Chemical Company

- Grupa Azoty

- Gujarat State Fertilizers & Chemicals Limited(GSFC)

- Prefere Resins Holding GmbH

- Methanol Holdings(Trinidad)Limited(MHTL)

- Mitsui Chemicals Inc.

- Hexion

- Nissan Chemical Corporation

- OCI NV

- Qatar Melamine Company

- Sichuan Chemical Works Group Ltd

- Henan Xinlianxin Chemicals Group Co. Ltd

- Eurochem Group

第7章 市場機會與未來趨勢

- 三聚氰胺泡沫的成長趨勢

The Melamine Market size is estimated at 1.95 million tons in 2025, and is expected to reach 2.39 million tons by 2030, at a CAGR of 4.15% during the forecast period (2025-2030).

The melamine market was negatively impacted during the COVID-19 pandemic in 2020. The market improved in 2021. With construction and automotive manufacturing activities recovering from the lockdown, the demand for construction materials such as laminates, paints, and coatings, and wood adhesives increased. The construction industry is recovering rapidly and is estimated to grow further in the coming years, which may boost the demand for melamine.

Key Highlights

- Over the short term, the rising demand for laminates, coatings, and wood adhesives from the construction industry is expected to drive the market's growth.

- The availability of substitutes like liquefied wood, soy, and powder coatings and increasing consumer concerns about formaldehyde emissions from melamine-based molding compounds are expected to hinder the market's growth.

- However, the increasing trend of melamine-based foams is likely to act as an opportunity in the future.

- Asia-Pacific dominates the market across the world, with the largest consumption from China and India.

Melamine-based Adhesives Market Trends

Laminates Segment to Dominate the Market

- Melamine resins are the polymers of choice used in the outer or decorative layer of laminates and in manufacturing counters and tabletops, kitchen cabinets, flooring, furniture, etc.

- Melamine resins impart a hardness, transparency, stain resistance, freedom from discoloration, and overall durability. For this application, the resin used to saturate the overlay or decorative sheet is prepared by reacting approximately two moles of formaldehyde per mole of melamine.

- These sheets are commonly applied to the surface decoration projects, such as walls, columns, tabletops, furniture, and suspended ceilings.

- According to the Canadian Construction Association, the construction sector is one of Canada's largest employers and a major contributor to the country's economic success. It is the backbone of the country's economy. As per the Canadian Construction Association, the construction sector employs more than 1.4 million people and generates about USD 141 billion for the Canadian economy annually. Also, the industry accounts for 7.5% of the country's Gross Domestic Product (GDP).

- According to the US Census data, the total construction spending in February 2022 was around USD 1,704.4 billion compared to USD 1,695.5 billion in January 2022.

- As per the United States Census Bureau, the residential construction industry in the United States was valued at USD 929.7 billion in July 2022, as compared to USD 815.5 billion in July 2021, registering a growth of 14%. The aging houses signal a growing remodeling market, as old structures normally need to add new amenities or repair/replace old components. Rising home prices in the country have also encouraged homeowners to spend more on home improvements.

Asia-Pacific to Dominate the Market

- The Asia-Pacific region dominates the overall market share. With growing construction activities and the increasing demand for laminates, wood adhesives, and paints and coatings in China, India, and Japan, the usage of melamine is increasing in the region.

- China accounts for more than one-fourth of the global coatings market. According to the China National Coatings Industry Association, the industry registered a 7% growth in recent years.

- The Chinese government rolled out massive construction plans, including making provisions for the movement of 250 million people to its new megacities over the next 10 years. Such plans will increase the demand for paints where melamine is used to prepare paints.

- The overall Chinese construction industry is expected to increase by 4.6% in real terms in 2023-2026. According to the report published by the National Bureau of Statistics of China, transportation investment increased by 6.7% in the first half of 2022.

- The Indian government launched the Delhi-Mumbai Industrial Corridor program in collaboration with the Japanese government, which aims at developing new industrial cities with an investment of 200 billion USD in the Delhi-Mumbai Industrial Corridor region. Similar programs may be launched in regions such as the Bangalore Chennai Corridor etc.

- According to the Civil Aviation Administration of China, the government has resumed construction work on more than 80% of total airport projects, representing 65 airport projects across the country. Out of these, 27 airports are national major airport projects. Such projects are expected to increase the demand for melamine.

Melamine-based Adhesives Industry Overview

The melamine market is fragmented, and the top five players account for around 40% of the total production capacity. These companies include (not in any particular order) OCI NV, Borealis AG, Henan Xinlianxin Chemicals Group Co. Ltd, Prefere Resins Holding GmbH, and Grupa Azoty.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Strong Demand from the Construction Industry

- 4.1.2 Other Drivers

- 4.2 Restraints

- 4.2.1 Increasing Consumer Concerns About Formaldehyde Emission from Melamine-based Molding Compounds

- 4.2.2 Availability of Substitutes, like Liquefied Wood, Soy, and Powder Coatings

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Feedstock Analysis and Trends

- 4.6 Production Process

- 4.7 Import-export Trends

- 4.8 Price Trends

- 4.9 Patent Analysis

- 4.10 Regulatory Policy Analysis

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Application

- 5.1.1 Laminates

- 5.1.2 Wood Adhesives

- 5.1.3 Molding Compounds

- 5.1.4 Paints and Coatings

- 5.1.5 Other Applications (Flame Retardants and Textile Resins)

- 5.2 Geography

- 5.2.1 Asia-Pacific

- 5.2.1.1 China

- 5.2.1.2 India

- 5.2.1.3 Japan

- 5.2.1.4 South Korea

- 5.2.1.5 Rest of Asia-Pacific

- 5.2.2 North America

- 5.2.2.1 United States

- 5.2.2.2 Canada

- 5.2.2.3 Mexico

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 United Kingdom

- 5.2.3.3 Italy

- 5.2.3.4 France

- 5.2.3.5 Russia

- 5.2.3.6 Rest of Europe

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Rest of South America

- 5.2.5 Middle-East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 South Africa

- 5.2.5.3 Rest of Middle-East and Africa

- 5.2.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 BASF SE

- 6.4.2 Borealis AG

- 6.4.3 Cornerstone Chemical Company

- 6.4.4 Grupa Azoty

- 6.4.5 Gujarat State Fertilizers & Chemicals Limited (GSFC)

- 6.4.6 Prefere Resins Holding GmbH

- 6.4.7 Methanol Holdings (Trinidad) Limited (MHTL)

- 6.4.8 Mitsui Chemicals Inc.

- 6.4.9 Hexion

- 6.4.10 Nissan Chemical Corporation

- 6.4.11 OCI NV

- 6.4.12 Qatar Melamine Company

- 6.4.13 Sichuan Chemical Works Group Ltd

- 6.4.14 Henan Xinlianxin Chemicals Group Co. Ltd

- 6.4.15 Eurochem Group

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Trend of Melamine-based Foams

三聚氰胺泡沫塊市場報告:2031 年趨勢、預測與競爭分析

三聚氰胺泡沫塊市場報告:2031 年趨勢、預測與競爭分析 三聚氰胺市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測

三聚氰胺市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測 三聚氰胺甲醛市場(全球)(2018-2034)

三聚氰胺甲醛市場(全球)(2018-2034) 三聚氰胺市場規模、佔有率、成長分析、按形狀、按應用、按最終用途、按地區 - 產業預測,2024-2031年三聚氰胺甲醛市場規模、佔有率和成長分析(按類型、形狀、應用、地區):產業預測(2024-2031)三聚氰胺市場(全球)(2018-2034)

三聚氰胺市場規模、佔有率、成長分析、按形狀、按應用、按最終用途、按地區 - 產業預測,2024-2031年三聚氰胺甲醛市場規模、佔有率和成長分析(按類型、形狀、應用、地區):產業預測(2024-2031)三聚氰胺市場(全球)(2018-2034) 全球三聚氰胺甲醛市場規模依產品類型、應用、最終用途產業、地區、範圍及預測

全球三聚氰胺甲醛市場規模依產品類型、應用、最終用途產業、地區、範圍及預測 三聚氰胺甲醛市場:依形式、應用分類 - 2025-2030 年全球預測2024-2032 年按產品類型、等級、應用、最終用途產業和地區分類的三聚氰胺甲醛市場報告三聚氰胺市場-2024年至2029年預測

三聚氰胺甲醛市場:依形式、應用分類 - 2025-2030 年全球預測2024-2032 年按產品類型、等級、應用、最終用途產業和地區分類的三聚氰胺甲醛市場報告三聚氰胺市場-2024年至2029年預測