|

市場調查報告書

商品編碼

1686631

再生 PET:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)Recyclate PET - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

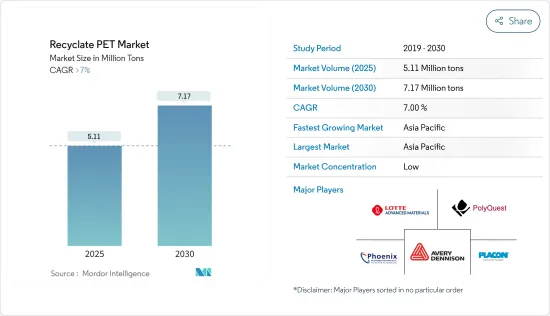

2025年再生PET市場規模預計為511萬噸,預計2030年將達到717萬噸,預測期內(2025-2030年)的複合年成長率將超過7%。

2020 年,COVID-19 疫情對市場產生了負面影響。這是因為製造設施和工廠因封鎖和限制而關閉。供應鏈和運輸中斷進一步擾亂了市場。但2021年,產業復甦,市場需求回歸。

主要亮點

- 從中期來看,消費者和包裝產品對永續性關注以及紡織業不斷成長的需求正在推動市場成長。

- 另一方面,行業利潤率下降預計將阻礙市場成長。

- 然而,回收技術的創新以及塑膠自動加工和分類的新材料來源的發現可能會在預測期內為研究市場提供機會。

- 由於中國、印度和日本等國家的需求大幅成長,亞太地區在全球市場佔據主導地位。

再生 PET 的市場趨勢

工業絲領域主導市場需求

- 再生PET工業絲是一種由回收的寶特瓶所生產的環保合成材料。 寶特瓶收集、分類後,可以切成薄片,熔化,然後紡成紗線。由寶特瓶成的聚酯纖維、萊卡纖維和尼龍纖維可用於製作服飾和鞋子。

- 各種政府舉措、為實現零廢棄物和循環經濟目標而進行的工業投資、環境因素以及全球對聚酯紗的需求不斷成長正在推動市場需求。

- 對此,歐盟為紡織業設定了若干目標。根據報告,到2030年,所有紡織產品必須耐用、可修復、可回收、主要由再生纖維製成且不含有害物質,這表明預測期內再生 PET 市場將會成長。

- 此外,H&M 和 Inditex 等零售時尚品牌已設定目標,到 2025-2030 年在其成衣 (RMG) 領域使用 100% 再生纖維。根據德國聯邦統計局的數據,德國紡織業的收益預計到 2022 年將達到約 140 億美元,高於 2021 年的約 129 億美元。同樣,服飾的收益從去年的 62.3 億美元成長至近 75 億美元。

- 此外,2022 年 8 月,信實工業有限公司宣布計劃將其瓶子回收能力提高一倍至每年 50 億瓶,以保持在 PET 回收領域的領先地位。該公司正在投資提高其時尚業務部門的紗線和纖維產量。預計這將在不久的將來推動再生 PET 市場的成長。

- 因此,這些趨勢可能會在預測期內影響產業對再生 PET 的需求。

亞太地區佔市場主導地位

- 在亞太地區,中國是GDP最大的經濟體。即使與美國的貿易戰導致貿易中斷,該國的 GDP 在 2022 年仍成長了 3% 左右。

- 2020 年中國實際 GDP 成長 2.2%,2021 年成長 8.4%,這在很大程度上得益於疫情後消費支出的復甦。此外,國際貨幣基金組織預測,2023年GDP成長率為5.2%,2024年放緩至4.5%。

- 由於包裝、紡織和汽車行業的不斷發展,中國成為該地區最大的再生PET(rPET)消費國。預計預測期內這些產業的生產將推動該國對聚對苯二甲酸乙二醇酯樹脂的需求。

- 該國的 rPET 製造商包括威立雅華飛和瑪氏。威立雅華飛是日本最大的再生PET生產商之一。 2021年,公司將rPET瓶片產能從3萬噸擴大至10萬噸。在越南和馬來西亞等鄰國,中國投資者對再生 PET 托盤的待開發區投資正在增加。

- 2023年2月,全球糖果零食製造商瑪氏箭牌中國分公司推出了首款完全由消費後回收PET(rPET)製成的包裝。該公司已向本土巧克力品牌璀璨米(CXM)引入了再生 PET 包裝。

- 此外,印度是全球新興經濟體之一,人口、生活水準和人均收入不斷增加,幾乎幾乎所有終端用戶產業成長。

- 國內已有多家公司參與rPET的生產。例如,印度 PET 回收先驅 Ganesha Ecosphere Ltd 的子公司 Ganesha Ecopet Private Limited 已在瓦朗加爾開設了一家新工廠,品牌名為 Go Rewise,生產用於長絲、纖維和食品包裝的 rPET。該公司在位於 Telangana 省 Warangal 的工廠安裝了兩條 Sterling PET 回收生產線。

- 此外,由於塑膠不可分解,人們對其對環境的有害影響的日益關注和日益嚴格的監管預計將在未來幾年為亞太地區再生 PET 市場提供巨大的機會。

再生 PET 行業概況

再生 PET 市場較為分散。該市場的知名企業包括 Phoenix Technologies、Placon(EcoStar)、PolyQuest、樂天化學株式會社和艾利丹尼森株式會社(不分先後順序)。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 驅動程式

- 越來越重視消費品和包裝商品的永續性

- 紡織業需求不斷成長

- 限制因素

- 沒有塑膠收集和分類框架

- 環境問題和健康危害

- 沒有塑膠收集和分類框架

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場區隔

- 依產品類型

- 聚酯短纖維

- PET打包帶

- PET 片材或薄膜

- 按應用

- 包裝

- 工業絲

- 單絲

- 帶子

- 建材

- 其他用途

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭格局

- 併購、合資、合作、協議

- 市場佔有率分析

- 主要企業策略

- 公司簡介

- Alpla Group

- Avery Dennison Corporation

- Ds Smith

- Far Eastern New Century Corporation

- Indorama Ventures Public Company Limited

- Jiangsu Zhongyuan Industrial Group Co. Ltd

- Kaptan Group Holdings AS

- Krones AG

- Libolon

- Lotte Chemical Corporation

- Placon

- Phoenix Technologies

- Polyquest Inc.

- Reliance Industries Ltd

- Repro-PET

- Veolia

- Verdeco Recycling Inc.

第7章 市場機會與未來趨勢

- 塑膠自動加工和分類回收技術的創新

- 增加循環經濟舉措

The Recyclate PET Market size is estimated at 5.11 million tons in 2025, and is expected to reach 7.17 million tons by 2030, at a CAGR of greater than 7% during the forecast period (2025-2030).

The COVID-19 pandemic negatively impacted the market in 2020. This was because of the shutdown of the manufacturing facilities and plants due to the lockdown and restrictions. Supply chain and transportation disruptions further created hindrances for the market. However, the industry witnessed a recovery in 2021, thus rebounding the demand for the market studied.

Key Highlights

- Over the medium term, factors such as the growing emphasis on sustainability among consumers and packaging products and the increasing demand from the textile industry are driving the market growth.

- On the flip side, lower profit margins in the industry are expected to hamper the market's growth.

- Nevertheless, the innovations in recycling technologies for automatic processing and sorting of plastics and the discovery of new material sources are likely to provide opportunities for the market studied during the forecast period.

- Asia-Pacific dominated the global market due to the significant growth in demand coming from countries such as China, India, and Japan.

Recyclate PET Market Trends

The Industrial Yarn Segment to Dominate the Market Demand

- Recycled PET industrial yarn is an environmentally friendly synthetic material manufactured from recycled PET bottles. After collecting and sorting PET plastic bottles, they can be turned into flakes, melted down, and spun into yarn. Polyester, lycra, and nylon fibers spun from PET plastic can create clothing and shoes.

- Various government initiatives, industrial investments to reach zero waste and circularity targets, environmental factors, and the rising demand for polyester yarns worldwide are driving the market demand.

- In this regard, the European Union has set several goals for the textile industry. As per reports, by 2030, all textile products must be durable, repairable, and recyclable, primarily made from recycled fibers and free from hazardous substances, indicating an increase in the recyclate PET market in the forecast period.

- Additionally, retailer fashion brands like H&M and Inditex have set targets to use 100% recycled fibers by 2025-2030 in the ready-made garments (RMG) sector. In Germany, as per the Federal Statistical Office of Germany, the textile industry's revenue in 2022 was nearly USD 14 billion, an increase from roughly USD 12.9 billion in 2021. Similarly, the revenue from the clothing industry was nearly USD 7.5 billion, an increase from USD 6.23 billion in the previous year.

- Furthermore, in August 2022, Reliance Industries Ltd. announced its plan to maintain its leadership position in PET recycling by doubling its bottle recycling capacity to 5 billion bottles per year. The company invests in boosting its yarn and fiber production for its fashion business segment. It is expected to enhance growth in the recyclate PET market in the near future.

- Therefore, these trends are likely to influence the industry's demand for recycled PET during the forecast period.

Asia-Pacific Region to Dominate the Market

- In the Asia-Pacific region, China is the largest economy in terms of GDP. The country witnessed about 3% growth in its GDP in 2022, even after the trade disturbance caused due to its trade war with the United States.

- China's real GDP grew by 2.2% in 2020 and by 8.4% in 2021, largely driven by the consumer spending rebound post-pandemic. Furthermore, in 2023, as per IMF forecasts, the country's GDP grew by 5.2% and is expected to decline to 4.5% in 2024.

- China is the largest consumer of recyclate PET (rPET) in the region, owing to its growing packaging, textile, and automotive industries. The production in these industries is expected to drive the demand for polyethylene terephthalate resin in the country during the forecast period.

- Some of the manufacturers of rPET in the country include Veolia Huafei and Mars. Veolia Huafei is one of the largest manufacturers of recycled PET in the country. In 2021, the company scaled up its rPET bottle flakes capacity from 30,000 metric tons to 100,000 metric tons. There is an increase in greenfield investment for recycled PET pallets by Chinese investors in neighboring countries, such as Vietnam and Malaysia.

- In February 2023, the Chinese branch of the global confectionery company Mars Wrigley launched its first package made entirely from post-consumer recycled PET (rPET). The company adopted this recycled PET packaging for its local chocolate brand, Cui Xiang Mi (CXM).

- Furthermore, India is one of the emerging economies globally, and almost all the end-user industries have been growing, owing to the rising population, living standards, and per capita income.

- There are many companies that have been involved in the production of rPET in the country. For instance, Ganesha Ecopet Private Limited, a subsidiary of Indian PET recycling pioneer Ganesha Ecosphere Ltd, opened its new Warangal facility under the brand name Go Rewise, where it produces rPET for filament yarns and fibers, as well as for food-grade packaging. The company has installed two Starlinger PET recycling lines in its facility in Warangal, Telangana.

- Besides, the increased concerns related to harmful environmental impact due to the no-degradability of plastic and the growing regulations are expected to provide enormous opportunities for the recyclate PET market in Asia-Pacific in the coming years.

Recyclate PET Industry Overview

The recyclate PET market is fragmented in nature. Some of the noticeable players in the market include (in no particular order) Phoenix Technologies, Placon (EcoStar), PolyQuest, Lotte Chemical Corporation, and Avery Dennison Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Emphasis on Sustainability among the Consumer and Packaging Products

- 4.1.2 Increasing Demand from the Textile Industry

- 4.2 Restraints

- 4.2.1 Absence of the Required Framework for Plastic Collection and Segregation

- 4.2.1.1 Environmental Concerns and Health Hazards

- 4.2.1 Absence of the Required Framework for Plastic Collection and Segregation

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION

- 5.1 By Product Type

- 5.1.1 PET Staple Fiber

- 5.1.2 PET Straps

- 5.1.3 PET Sheets or Films

- 5.2 By Application

- 5.2.1 Packaging

- 5.2.2 Industrial Yarn

- 5.2.3 Mono Filaments

- 5.2.4 Strapping

- 5.2.5 Building Materials

- 5.2.6 Other Applications

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East & Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East & Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Alpla Group

- 6.4.2 Avery Dennison Corporation

- 6.4.3 Ds Smith

- 6.4.4 Far Eastern New Century Corporation

- 6.4.5 Indorama Ventures Public Company Limited

- 6.4.6 Jiangsu Zhongyuan Industrial Group Co. Ltd

- 6.4.7 Kaptan Group Holdings AS

- 6.4.8 Krones AG

- 6.4.9 Libolon

- 6.4.10 Lotte Chemical Corporation

- 6.4.11 Placon

- 6.4.12 Phoenix Technologies

- 6.4.13 Polyquest Inc.

- 6.4.14 Reliance Industries Ltd

- 6.4.15 Repro-PET

- 6.4.16 Veolia

- 6.4.17 Verdeco Recycling Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Innovations in Recycling Technologies for Automatic Processing and Sorting of Plastics

- 7.2 Increasing Circular Economy Initiatives

再生PET市場規模、佔有率及成長分析(按類型、等級、來源、顏色、應用和地區)-2025-2032年產業預測

再生PET市場規模、佔有率及成長分析(按類型、等級、來源、顏色、應用和地區)-2025-2032年產業預測 全球再生 PET 薄片市場研究報告-產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年

全球再生 PET 薄片市場研究報告-產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年 再生 PET 市場:按產品類型、等級、顏色、收集來源、最終用戶、最終產品- 2025-2030 年全球預測再生 PET 部分取向紗線市場:按類型、應用分類 - 2025-2030 年全球預測

再生 PET 市場:按產品類型、等級、顏色、收集來源、最終用戶、最終產品- 2025-2030 年全球預測再生 PET 部分取向紗線市場:按類型、應用分類 - 2025-2030 年全球預測 熱洗無色 R-PET 瓶級薄片和顆粒市場,按產品類型、加工類型、等級、最終用戶、國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測

熱洗無色 R-PET 瓶級薄片和顆粒市場,按產品類型、加工類型、等級、最終用戶、國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測 全球再生PET市場(2016-2036)全球再生 PET 市場研究報告 - 2024 年至 2032 年產業分析、規模、佔有率、成長、趨勢和預測全球再生 PET 市場 - 2024-2031再生 PET 市場:按類型、來源和應用分類:2023-2032 年全球機會分析和行業預測

全球再生PET市場(2016-2036)全球再生 PET 市場研究報告 - 2024 年至 2032 年產業分析、規模、佔有率、成長、趨勢和預測全球再生 PET 市場 - 2024-2031再生 PET 市場:按類型、來源和應用分類:2023-2032 年全球機會分析和行業預測 熱洗無色 R-PET 瓶級薄片和顆粒市場(產品:薄片和顆粒;等級:食品級和非食品級)- 全球行業分析、規模、佔有率、成長、趨勢和預測,2023 年- 2031

熱洗無色 R-PET 瓶級薄片和顆粒市場(產品:薄片和顆粒;等級:食品級和非食品級)- 全球行業分析、規模、佔有率、成長、趨勢和預測,2023 年- 2031