|

市場調查報告書

商品編碼

1686632

農業界面活性劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Agricultural Surfactant - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

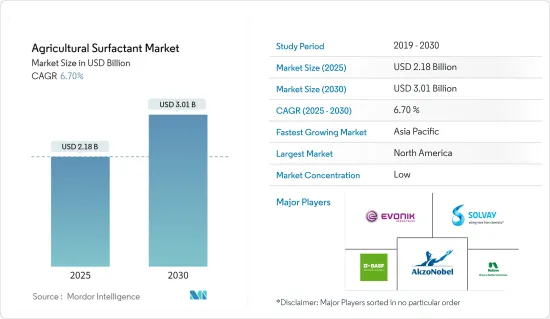

預計 2025 年農業界面活性劑市場規模為 21.8 億美元,到 2030 年將達到 30.1 億美元,預測期內(2025-2030 年)的複合年成長率為 6.7%。

農業界面活性劑主要用於水性除草劑噴霧溶液,以增強乳化、分散、鋪展、潤濕和其他表面改質性能。這些添加劑在除草劑處理中非常重要,可以提高噴霧液滴的保留率並提高活性成分向植物葉子的滲透率。為了滿足不斷成長的世界人口,對糧食生產的需求不斷增加,因此農業界面活性劑的使用量顯著成長。根據《哈佛商業評論》預測,到2050年世界人口預計將達到97億,同期糧食需求預計將增加70%。因此,農民擴大採用農業表面活性劑來提高作物產量並滿足日益成長的需求。

傳統界面活性劑通常來自石化產品,並且面臨日益嚴重的環境問題和監管挑戰。 2023年,歐盟委員會提案更新歐盟界面活性劑框架,以確保食品安全和環境永續性。這推動了對生物基、生物分解性和環境友善的表面活性劑作為更永續的替代品的需求。這些界面活性劑來自可再生資源,包括植物來源和農產品,並且易於生物分解,從而最大限度地減少對環境的影響。隨著製造商開發出滿足農業性能要求並符合環境管理目標的產品,向永續表面活性劑解決方案的轉變正在刺激產業內部的創新。

農用表面活性劑的市場趨勢

穀物和穀類佔據市場主導地位

小麥、米、玉米和大麥等穀類是世界上種植最廣泛的作物之一。這些是世界相當一部分人口的主食,需要大規模生產。如此大規模的種植導致對農業表面活性劑的需求龐大,以提高作物產量,改善土壤健康,並促進農作物保護產品的有效應用。根據聯合國糧食及農業組織統計,2023年全球整體小麥種植面積超過2.191億公頃,玉米種植面積約2.034億公頃,水稻種植面積約1.651億公頃。這些驚人的數字凸顯了穀物和穀類生產的巨大規模,需要廣泛使用農業界面活性劑。

此外,世界人口正在呈指數級成長,每天全世界的糧食需求將增加近20萬人。根據聯合國統計,過去100年來世界人口增加了近四倍。向不斷成長的人口供應穀物和穀類對全球構成了威脅。此外,各種作物害蟲每年造成全球10-16%的作物損失,使情況更加惡化。因此,農民採用作物保護作為滿足全球日益成長的穀物需求的關鍵策略。

用於種植穀物和穀類的可耕地面積的減少也增加了對保護性耕作和犁地農業等永續農業實踐的需求。農業界面活性劑在這些實踐中發揮關鍵作用,它使農藥能夠有效地施用和吸收,而不會過度擾動土壤。

北美佔據市場主導地位

北美佔據農業表面活性劑市場的最大佔有率。預計該地區在估計和預測期內將穩步成長,特別是由於政府採取各種措施來提高產量並保持食品、飼料和生質燃料行業原料的持續供應。推動成長的關鍵因素是生物表面活性劑的使用量不斷增加以及原料的豐富可得性。

由於大規模商業性農業經營的存在,美國在全部區域的市場中佔據主導地位,這對高效農藥製劑產生了巨大的需求,從而推動了對兼容表面活性劑的需求。此外,美國農民的購買力增強,更願意投資先進的農業投入,導致界面活性劑的使用量更高。例如,根據美國農業部的數據,到2023年,美國農場的平均收入將超過178,692美元,因此可以為農作物保護產品進行大量投資。此外,由於擔心環境影響、土壤健康和長期農業生產力,該國越來越重視永續農業實踐。因此,對生物表面活性劑的需求十分強烈,以最大限度地減少對環境的影響並促進土壤健康。

農用表面活性劑產業概況

農用界面活性劑市場較為分散。市場的主要企業正在採取策略,透過收購、新產品發布、業務擴展和投資、協議、夥伴關係、合資企業和合資企業等方式拓展到新的地區。投資研發也是市場領導所採取的策略之一。市場的主要企業包括 Evonik Industries AG、 BASF SE、Solvay SA、Akzo Nobel NV 和 Kao Corporation。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 市場概況

- 市場促進因素

- 提高農作物產量對農藥的需求不斷增加

- 農業技術進步

- 更重視永續農業和環保解決方案

- 市場限制

- 生物基界面活性劑生產成本高

- 有關化學品使用的嚴格環境法規

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭強度

第5章 市場區隔

- 類型

- 陰離子

- 非離子

- 陽離子

- 男女皆宜

- 油性界面活性劑

- 應用

- 殺蟲劑

- 除草劑

- 殺菌劑

- 其他用途

- 基材

- 合成

- 生物基

- 作物用途

- 以作物為基礎

- 糧食

- 油籽

- 水果和蔬菜

- 非作物

- 草坪和觀賞草

- 其他作物

- 以作物為基礎

- 地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 北美其他地區

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 其他亞太地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 南非

- 其他中東和非洲地區

- 北美洲

第6章 競爭格局

- 最受歡迎的策略

- 市場佔有率分析

- 公司簡介

- Akzo Nobel NV

- Evonik Industries

- BASF SE

- Nouryon

- Solvay SA

- Wilbur-Ellis Company

- Croda International PLC

- Canopus International

- Nufarm Limited

- Marubeni Corporation

- Air Products and Chemicals

- Kao Corporation

- Clariant

- Lamberti SPA

- Brandt Consolidated Inc.

- Bionema Limited

- Zhejiang Transfar(Tanatex Chemicals)

- Garrco Products Inc.

第7章 市場機會與未來趨勢

The Agricultural Surfactant Market size is estimated at USD 2.18 billion in 2025, and is expected to reach USD 3.01 billion by 2030, at a CAGR of 6.7% during the forecast period (2025-2030).

Agricultural surfactants are primarily used in water-based herbicide spray solutions to enhance their emulsifying, dispersing, spreading, wetting, or other surface-modifying properties. These additives are crucial in herbicide treatments, improving spray droplet retention and the penetration of active ingredients into plant foliage. The use of agricultural surfactants has grown significantly due to the increasing demand for food production to support the growing global population. According to Harvard Business Review projections, the world population is expected to reach 9.7 billion by 2050, with food demand estimated to increase by 70% during the same period. As a result, farmers are increasingly adopting agricultural surfactants to improve crop yield and meet this rising demand.

Traditional surfactants, typically derived from petrochemical sources, have raised environmental concerns and faced regulatory challenges. In 2023, the European Commission proposed an update to the EU framework on surfactants for food safety and environmental sustainability. This has led to a growing demand for bio-based, biodegradable, and eco-friendly surfactants as more sustainable alternatives. These surfactants are derived from renewable sources, such as plant-based materials or agricultural byproducts, and are designed to be readily biodegradable, minimizing their environmental impact. The shift towards sustainable surfactant solutions has spurred innovation within the industry, with manufacturers developing products that meet agricultural performance requirements while aligning with environmental stewardship goals.

Agricultural Surfactants Market Trends

Grains and Cereals Dominates the Market

Grains and cereals, such as wheat, rice, maize, and barley, are among the most widely cultivated crops worldwide. They serve as staple foods for a significant portion of the global population and necessitate large-scale production. This large cultivation translates into a significant need for agricultural surfactants to enhance crop yields, improve soil health, and facilitate the efficient application of crop protection products. According to the Food and Agriculture Organization, in 2023, wheat was cultivated on over 219.1 million hectares of land globally, while maize occupied around 203.4 million hectares, and rice covered approximately 165.1 million hectares. These staggering figures highlight the immense scale of grain and cereal production, necessitating the extensive use of agricultural surfactants.

Moreover, the global population is increasing exponentially, and every day, nearly 200,000 people are being added to the world's food demand. According to the United Nations, the world's human population increased nearly fourfold in the past 100 years. Supplying grains and cereals to this growing population has become a global threat. Moreover, various crop pests are causing 10-16% of global crop losses annually, worsening the scenario. Therefore, farmers are adopting crop protection as the key strategy to meet the growing demand for grains and cereals globally.

The shrinking of arable land for grains and cereals has also driven the need for sustainable agricultural practices, such as conservation tillage and no-till farming. Agricultural surfactants play a crucial role in these practices by enabling the effective application and absorption of agrochemicals without the need for excessive soil disturbance.

North America Dominates the Market

North America holds one the largest part of the agricultural surfactant market. The region is estimated to grow steadily during the forecast period, especially with the various government initiatives to increase yield and maintain a continuous supply of raw materials for the food, feed, and biofuel industries. Major factors driving the growth are the increasing usage of bio-surfactants and the abundant availability of raw materials.

The United States dominated the market across the region due to the presence of large-scale commercial agricultural operations has created a significant demand for efficient and effective agrochemical formulations, which in turn has driven the need for compatible surfactants. Additionally, the United States farmers have high purchasing power and willingness to invest in advanced agricultural inputs contributing to the high usage of surfactants. For instance, the United States farm median income was more than USD 178,692 in 2023, according to the United States Department of Agriculture, allowing for significant investment in crop protection products. Moreover, there is a growing emphasis on sustainable farming practices in the country, driven by concerns over environmental impact, soil health, and long-term agricultural productivity. As a result, the demand for bio surfactants is growing significantly to minimize the environmental impact and promote soil health.

Agricultural Surfactants Industry Overview

The market for agricultural surfactants is fragmented. The key players in the market have been following strategies to explore new regions through acquisitions, new product launches, expansions and investments, agreements, partnerships, collaborations, and joint ventures. Investment in R&D is another strategy adopted by market leaders. Some of the major players in the market are Evonik Industries AG, BASF SE, Solvay SA, Akzo Nobel N.V., and Kao Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand for Agrochemicals to Boost Crop Yield

- 4.2.2 Technological Advancements in Agricultural Practices

- 4.2.3 Rising Focus on Sustainable Agriculture and Eco-Friendly Solutions

- 4.3 Market Restraints

- 4.3.1 High Production Costs of Bio-based Surfactants

- 4.3.2 Stringent Environmental Regulations on Chemical Use

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Anionic

- 5.1.2 Nonionic

- 5.1.3 Cationic

- 5.1.4 Amphoteric

- 5.1.5 Oil- Based Surfactants

- 5.2 Application

- 5.2.1 Insecticide

- 5.2.2 Herbicide

- 5.2.3 Fungicide

- 5.2.4 Other Applications

- 5.3 Substrate

- 5.3.1 Synthetic

- 5.3.2 Bio-based

- 5.4 Crop Application

- 5.4.1 Crop-based

- 5.4.1.1 Grains and Cereals

- 5.4.1.2 Oilseeds

- 5.4.1.3 Fruits and Vegetables

- 5.4.2 Non-crop-based

- 5.4.2.1 Turf and Ornamental Grass

- 5.4.2.2 Other Crop Applications

- 5.4.1 Crop-based

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Spain

- 5.5.2.5 Italy

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Rest of Middle-East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Akzo Nobel N.V.

- 6.3.2 Evonik Industries

- 6.3.3 BASF SE

- 6.3.4 Nouryon

- 6.3.5 Solvay SA

- 6.3.6 Wilbur-Ellis Company

- 6.3.7 Croda International PLC

- 6.3.8 Canopus International

- 6.3.9 Nufarm Limited

- 6.3.10 Marubeni Corporation

- 6.3.11 Air Products and Chemicals

- 6.3.12 Kao Corporation

- 6.3.13 Clariant

- 6.3.14 Lamberti SPA

- 6.3.15 Brandt Consolidated Inc.

- 6.3.16 Bionema Limited

- 6.3.17 Zhejiang Transfar (Tanatex Chemicals)

- 6.3.18 Garrco Products Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

2025 年全球農業界面活性劑市場報告

2025 年全球農業界面活性劑市場報告 農業表面活性劑市場:按產品類型、基材類型、作物類型、應用和最終用戶 - 2025-2030 年全球預測

農業表面活性劑市場:按產品類型、基材類型、作物類型、應用和最終用戶 - 2025-2030 年全球預測 農業表面活性劑市場規模、佔有率和成長分析:按產品類型、按基材類型、按作物類型、按應用、按地區 - 產業預測,2024-2031年

農業表面活性劑市場規模、佔有率和成長分析:按產品類型、按基材類型、按作物類型、按應用、按地區 - 產業預測,2024-2031年 農業表面活性劑市場規模、佔有率、趨勢分析報告:按類型、基礎、作物類型、應用、地區、細分市場預測,2025-2030

農業表面活性劑市場規模、佔有率、趨勢分析報告:按類型、基礎、作物類型、應用、地區、細分市場預測,2025-2030 全球農業界面活性劑市場評估:依類型、基質、作物類型、應用、地區、機會、預測,2017-2031年

全球農業界面活性劑市場評估:依類型、基質、作物類型、應用、地區、機會、預測,2017-2031年 農業界面活性劑市場報告:2030 年趨勢、預測與競爭分析

農業界面活性劑市場報告:2030 年趨勢、預測與競爭分析 農業界面活性劑市場:按類型、應用、作物類型分類:2024-2031 年全球機會分析與產業預測

農業界面活性劑市場:按類型、應用、作物類型分類:2024-2031 年全球機會分析與產業預測 2030 年農業界面活性劑市場預測:按類型、作物類型、功能、劑型、應用、最終用戶和地區進行的全球分析

2030 年農業界面活性劑市場預測:按類型、作物類型、功能、劑型、應用、最終用戶和地區進行的全球分析 農業界面活性劑市場 - 2023-2030

農業界面活性劑市場 - 2023-2030 農業界面活性劑的全球市場:市場規模和佔有率分析(依類型,應用,基質和作物),行業收入估計和需求預測(截至2030 年)

農業界面活性劑的全球市場:市場規模和佔有率分析(依類型,應用,基質和作物),行業收入估計和需求預測(截至2030 年)