|

市場調查報告書

商品編碼

1686633

藥品包裝:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Pharmaceutical Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

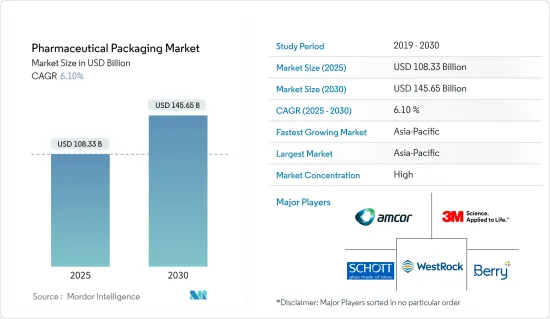

預計2025年醫藥包裝市場規模為1,083.3億美元,預計2030年將達到1,456.5億美元,預測期間(2025-2030年)的複合年成長率為6.1%。

監理環境影響包裝創新:

由於嚴格的監管標準和仿冒品措施,藥品包裝市場正在經歷顯著成長。世界各國政府都實施了嚴格的法規來確保產品安全並打擊假藥。歐盟 (EU) 指令要求所有藥品必須序列化,美國、中國、印度和土耳其也有類似的規定。這些措施正在推動先進封裝解決方案的採用。

主要亮點

- FDA 指南:FDA 已製定了非處方產品的兒童安全、防篡改包裝指南。

- 認證技術:製藥公司正在投資全像圖和隱藏批號等認證技術。

- 序列化方法:序列化方法包括線性條碼、2D條碼和無線射頻識別 (RFID)。

- 智慧包裝:使用 RFID 和 NFC 標籤的智慧包裝在產品追蹤和病人參與越來越受歡迎。

奈米技術徹底改變了包裝解決方案:

奈米技術對藥品包裝的影響正在透過新一代創新解決方案改變該產業。這些進步不僅可以打擊仿冒品,還可以提高整個供應鏈中的產品安全性和可追溯性。

主要亮點

- 可追溯性:奈米技術使得創建智慧包裝成為可能,使產品從製造到最終用戶都可以被追蹤。

- 開發智慧包裝:Schott AG 等公司正在開發智慧包裝封蓋解決方案,以實現清晰的容器為基礎的可追溯性。

- 產品發布:ENTOD Pharmaceuticals 在印度推出了一系列基於奈米技術的眼科美容產品,展示了奈米包裝的多功能性。

- 生物醫學應用:奈米粒子在生物醫學中用於疾病檢測、預防和藥物傳輸。

市場趨勢與成長動力:

由於幾個關鍵促進因素,醫藥包裝市場正在經歷強勁成長。製藥業的擴張和新興國家醫療支出的增加正在推動市場成長。

主要亮點

- 塑膠產業:預計到 2028 年塑膠產業規模將達到 544.5 億美元,複合年成長率為 6.17%。

- 瓶子部分:2022 年瓶子部分的價值為 182.4 億美元,預計到 2028 年將達到 273 億美元。

- 外國直接投資成長:印度等新興經濟體正在經歷顯著成長,其中製藥業的外國直接投資預計在 2020-21 年將成長 200%。

- 亞太地區成長:預計 2023 年至 2028 年亞太地區的複合年成長率為 6.99%,2028 年達到 545.9 億美元。

競爭格局與主要企業:

醫藥包裝市場較為分散,幾家大公司佔據主導地位。為了維持市場地位,這些公司專注於創新、永續性和策略性擴張。

主要亮點

- Amcor PLC:成立於 1860 年。提供廣泛的包裝解決方案,包括口服劑型和醫療設備包裝。

- Schott AG:該公司成立於 1853 年,專門從事醫藥管道和藥物封裝解決方案。

- Berry World Group:成立於1967年。提供醫療包裝、瓶子和管瓶。

- Gerresheimer AG:Gerresheimer AG 宣布將向其美國生產設施投資 9,400 萬美元,以提高管瓶生產能力。

永續性和未來趨勢:

醫藥包裝產業越來越關注永續性和環保解決方案。這一趨勢是由監管壓力和消費者對更環保包裝的需求所推動的。

主要亮點

- GlaxoSmithKline Plc消費者保健計畫已加入 Pulpex 紙瓶合作夥伴聯盟,共同探索可回收紙瓶。

- 投資生質塑膠:公司正在投資生質塑膠和其他生物分解性材料作為傳統塑膠的替代品。

- 先進的印刷技術:先進的印刷技術,例如 Essentra Packaging 的 Landa S10 奈米印刷機,正在提升包裝能力。

- 3D視覺化:3D 視覺化和印刷策略的採用正在突破初級和次級包裝設計的界限。

醫藥包裝市場趨勢

塑膠領域在材料類別中佔據主導地位

塑膠已成為醫藥包裝市場最大的材料類別。 2022年,該部分佔據41.84%的市場佔有率,價值380.3億美元。預計到 2028 年該部分將達到 541.5 億美元,預測期內的複合年成長率為 6.17%。這一成長由多種因素推動,包括該領域的多功能性、成本效益以及塑膠包裝解決方案的持續創新。

- 市場佔有率2022年塑膠將佔醫藥包裝市場的41.84%。

- 成本效益:塑膠價格實惠,是藥品包裝的熱門選擇。

- 創新解決方案:公司正在引入生物分解性和可回收的塑膠解決方案,以滿足永續性標準。

- 未來成長:預計到 2028 年該產業規模將達到 541.5 億美元。

- 監管標準推動塑膠包裝創新:嚴格的監管標準和仿冒品規範正在推動塑膠藥品包裝的進步。公司正在開發創新的解決方案來滿足這些要求。例如,2022 年 5 月,Bormioli Pharma推出了永續包裝產品標籤 EcoPositive,包括再生塑膠、生物基、生物分解性和可堆肥的塑膠解決方案。該舉措標誌著該行業對監管壓力和對永續包裝選擇日益成長的需求的回應。

- EcoPositive舉措Bormioli Pharma 的 EcoPositive 展示永續包裝選擇,包括生物基和可堆肥塑膠。

- 防偽:塑膠包裝的防偽措施日益複雜,以滿足全球標準。

- 監管壓力:全球範圍內不斷提高的監管標準正在影響醫藥塑膠包裝領域。

- 致力於永續性:增加生物分解性塑膠解決方案的投資符合環境法規。

- 奈米技術對塑膠包裝發展的影響:奈米技術的影響正在推動塑膠領域新一代包裝解決方案的發展。這些技術進步使得能夠創造出具有增強性能的包裝材料,例如改進的阻隔性和抗菌能力。預計奈米技術與塑膠藥品包裝的結合將在未來幾年為該領域的成長和市場主導地位做出重大貢獻。

- 阻隔功能:奈米技術可以增強塑膠藥品包裝的阻隔性能。

- 抗菌解決方案:公司正在整合抗菌奈米技術來提高包裝的安全性和使用壽命。

- 增強性能:奈米技術創新正在被用於使塑膠包裝更加智慧、更有效率。

- 未來展望:奈米技術的整合將推動塑膠包裝產業的成長。

亞太地區佔很大佔有率

亞太地區是醫藥包裝市場成長最快的地區。 2022 年,該地區的市場佔有率為 40.12%,市場規模為 366 億美元。預計到 2028 年市場規模將達到 545.9 億美元,預測期內複合年成長率將達到 6.99%。這一成長率超過其他地區,使亞太地區成為全球醫藥包裝市場的主要動力。

- 市場佔有率:亞太地區佔全球醫藥包裝市場的40.12%。

- 成長率:預計 2023 年至 2028 年期間該地區的複合年成長率為 6.99%。

- 區域優勢:中國和印度引領亞太地區的醫藥包裝市場。

- 新興趨勢:該地區的快速成長是由對創新和永續包裝的不斷成長的需求所推動的。

醫藥包裝行業概況

全球企業主導綜合市場

醫藥包裝市場的特點是全球企業憑藉多元化的產品系列佔據主導地位。 Amcor PLC、Schott AG 和 Berry Global Group Inc. 等公司是市場領導者,提供從瓶子和管瓶到泡殼包裝和注射器等廣泛的包裝解決方案。市場結構似乎相當鞏固,大型企業憑藉其廣泛的產品線、全球影響力和技術力佔據了相當大的市場佔有率。

Amcor PLC:醫藥包裝領域的全球領導者,提供從泡殼包裝到兒科瓶等廣泛的解決方案。

肖特股份公司(SCHOTT AG):專注於玻璃包裝和藥管,推動密封解決方案的創新。

Berry World Group 提供從瓶子到預填充注射器等各種塑膠包裝解決方案。

整合市場:市場由擁有技術專長和產品多樣化的大型公司主導。

創新和永續性推動市場領導地位:

市場領先的公司專注於創新和永續性。例如,Amcor PLC 在 22 財政年度推出了用於醫療保健應用的紙基 AmFiber 系列和不含 PVC 的 AmSky泡殼系統。 Berry World Group 推出了兒童安全、防篡改糖漿和液體藥品包裝的完整捆綁解決方案。這些公司也大力投資永續包裝解決方案,安姆科的目標是到 2030 年其產品組合中的再生材料佔比達到 30%。其市場領導地位透過策略擴張進一步加強,例如 Berry World 在印度班加羅爾的新製造工廠,增強了其先進醫療解決方案在區域和全球範圍內的可及性。

注重永續性:為了實現永續性目標,公司優先考慮可回收和環保材料。

創新解決方案:不含 PVC 的泡殼包裝和兒童防護瓶作為更安全、更永續的替代品越來越受歡迎。

策略擴張:在新興市場開設新工廠使全球公司能夠滿足當地需求並增加市場佔有率。

研發投入:主要企業正在投資研發,以推動藥品包裝的永續創新。

未來市場的成功因素:

市場參與者取得成功並增加市場佔有率的幾個關鍵因素如下。首先,對研發的投入是關鍵,安姆科推出的創新產品就是一個例子。其次,擴大新興市場的製造能力(例如 Berry World 在印度的新工廠)對於滿足不斷成長的需求至關重要。第三,對永續性的關注變得越來越重要,Klockner Pentaplast 推出了可回收的 PET泡殼膜。最後,策略性收購和聯盟,例如 Aptar Pharma 收購 Metaphase Design Group,可增強產品供應和服務能力。對於任何希望在未來幾年鞏固其地位或顛覆市場的公司來說,此類策略都至關重要。

研發投資:為了在快速發展的產業中保持競爭力,公司必須不斷創新。

新興市場:向亞太等高成長地區擴張對於未來的市場成功至關重要。

永續性:公司必須優先使用可回收和生物分解性的材料來解決環境問題。

策略性收購:收購和夥伴關係可以幫助擴大醫藥包裝產品供應並加速創新。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況

- 產業價值鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

- COVID-19 市場影響評估

第5章 市場動態

- 市場促進因素

- 包裝監管標準和嚴格的仿冒品措施

- 奈米技術對新一代創新包裝解決方案的影響

- 監理環境影響包裝創新

- 市場挑戰

- 原料成本因供應商議價能力而波動

第6章 市場細分

- 按材質

- 塑膠

- 玻璃

- 其他材料

- 依產品類型

- 瓶子

- 注射器

- 管瓶/安瓿瓶

- 管子

- 瓶蓋和瓶塞

- 標籤

- 其他產品類型

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太地區

- 拉丁美洲

- 巴西

- 墨西哥

- 其他拉丁美洲國家

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 北美洲

第7章 競爭格局

- 公司簡介

- Amcor PLC

- 3M Company

- Schott AG

- WestRock Company

- Berry Global Group Inc.

- McKesson Corporation

- AptarGroup Inc.

- Klockner Pentaplast Group

- CCL Industries Inc.

- FlexiTuff International Ltd

- Gerresheimer AG

- West Pharmaceutical Services Inc.

- Becton, Dickinson and Company

- Vetter Pharma International GmbH

- Catalent Inc.

- WL Gore & Associates Inc.

- Nipro Corporation

第8章投資分析

第9章 市場機會與未來趨勢

The Pharmaceutical Packaging Market size is estimated at USD 108.33 billion in 2025, and is expected to reach USD 145.65 billion by 2030, at a CAGR of 6.1% during the forecast period (2025-2030).

Regulatory Landscape Shapes Packaging Innovation:

The pharmaceutical packaging market is experiencing significant growth driven by stringent regulatory standards and anti-counterfeit measures. Governments worldwide are implementing strict regulations to ensure product safety and combat counterfeit drugs. The European Union's Directive mandates serialization numbers on all pharmaceutical products, while similar regulations exist in the United States, China, India, and Turkey. These measures are propelling the adoption of advanced packaging solutions.

Key Highlights

- FDA Guidelines: The FDA has established guidelines for child-resistant packaging and tamper-resistant packaging for OTC products.

- Authentication Technologies: Pharmaceutical companies are investing in authentication technologies like holograms and hidden batch numbers.

- Serialization Methods: Serialization methods include linear barcodes, two-dimensional barcodes, and radio frequency identification (RFID).

- Smart Packaging: Smart packaging with RFID and NFC tags is gaining traction for product tracking and patient engagement.

Nanotechnology Revolutionizes Packaging Solutions:

The impact of nanotechnology on pharmaceutical packaging is transforming the industry with innovative and new-generation solutions. These advancements not only combat counterfeiting but also enhance product safety and traceability throughout the supply chain.

Key Highlights

- Tracking Capability: Nanotechnology enables the creation of smart packaging that can track products from manufacturing to end-user.

- Smart Packaging Development: Companies like Schott AG are developing smart packaging containment solutions for clear container-based traceability.

- Product Launches: ENTOD Pharmaceuticals launched a nanotechnology-based ocular aesthetic range in India, showcasing the versatility of nano-packaging.

- Biomedicine Applications: Nanoparticles are being utilized in biomedicine for disease detection, prevention, and drug delivery.

Market Drivers and Growth Trends:

The pharmaceutical packaging market is witnessing robust growth, fueled by several key drivers. The expansion of the pharmaceutical industry in emerging economies, coupled with increasing healthcare spending, is propelling market growth.

Key Highlights

- Plastics Segment: The plastics segment is expected to reach USD 54.45 billion by 2028, growing at a CAGR of 6.17%.

- Bottles Segment: The bottles segment was valued at USD 18.24 billion in 2022 and is projected to reach USD 27.30 billion by 2028.

- FDI Growth: Emerging economies like India are experiencing significant growth, with a 200% increase in FDI in the pharmaceutical industry in 2020-2021.

- Asia-Pacific Growth: The Asia-Pacific region is expected to grow at a CAGR of 6.99% from 2023 to 2028, reaching USD 54.59 billion by 2028.

Competitive Landscape and Key Players:

The pharmaceutical packaging market is fragmented, with several major players dominating the industry. These companies are focusing on innovation, sustainability, and strategic expansions to maintain their market positions.

Key Highlights

- Amcor PLC: Established in 1860, Amcor offers a wide range of packaging solutions, including oral dose formats and medical device packaging.

- Schott AG: Founded in 1853, Schott specializes in pharmaceutical tubing and drug containment solutions.

- Berry Global Group: Established in 1967, Berry Global provides medical packaging, bottles, and vials.

- Gerresheimer AG: Gerresheimer AG announced a USD 94 million investment in a US production facility to increase its vial production capacity.

Sustainability and Future Trends:

The pharmaceutical packaging industry is increasingly focusing on sustainability and eco-friendly solutions. This trend is driven by both regulatory pressures and consumer demand for more environmentally responsible packaging.

Key Highlights

- GSK's Initiative: GlaxoSmithKline Consumer Healthcare joined the Pulpex paper bottle partner consortium to explore recyclable paper bottles.

- Bioplastics Investment: Companies are investing in bioplastics and other biodegradable materials as alternatives to traditional plastics.

- Advanced Printing Technologies: Advanced printing technologies, such as Essentra Packaging's Landa S10 Nanographic Printing Machine, are enhancing packaging capabilities.

- 3-D Visualization: The adoption of 3-D visualization and printing strategies is pushing the boundaries of both primary and secondary packaging design.

Pharmaceutical Packaging Market Trends

Plastics Segment Dominates Material Category

The Plastics segment emerges as the largest material category in the Pharmaceutical Packaging Market. In 2022, this segment accounted for 41.84% of the market share, valued at USD 38.03 billion. The segment is projected to reach USD 54.15 billion by 2028, growing at a CAGR of 6.17% during the forecast period. This growth is driven by several factors, including the segment's versatility, cost-effectiveness, and ongoing innovations in plastic packaging solutions.

- Market Share: Plastics accounted for 41.84% of the pharmaceutical packaging market in 2022.

- Cost-Effectiveness: The affordability of plastics makes it a popular choice in pharmaceutical packaging.

- Innovative Solutions: Companies are introducing biodegradable and recyclable plastic solutions to meet sustainability standards.

- Future Growth: The segment is projected to reach USD 54.15 billion by 2028.

- Regulatory Standards Drive Plastic Packaging Innovation: Stringent regulatory standards and norms against counterfeit products are propelling advancements in plastic pharmaceutical packaging. Companies are developing innovative solutions to meet these requirements. For instance, Bormioli Pharma launched EcoPositive in May 2022, a label for sustainable packaging offerings, including recycled plastics, bio-based, biodegradable, and compostable plastic solutions. This initiative demonstrates the industry's response to regulatory pressures and the growing demand for sustainable packaging options.

- EcoPositive Initiative: Bormioli Pharma's EcoPositive showcases sustainable packaging options, including bio-based and compostable plastics.

- Counterfeit Prevention: Anti-counterfeit measures in plastic packaging are becoming increasingly sophisticated to meet global standards.

- Regulatory Pressure: The rise of global regulatory standards is shaping the pharmaceutical plastic packaging segment.

- Sustainability Efforts: Increased investment in biodegradable plastic solutions aligns with environmental regulations.

- Nanotechnology Impacts Plastic Packaging Development: The impact of nanotechnology is driving the development of new-generation packaging solutions in the plastics segment. This technological advancement is enabling the creation of packaging materials with enhanced properties, such as improved barrier functions and antimicrobial capabilities. The integration of nanotechnology in plastic pharmaceutical packaging is expected to contribute significantly to the segment's growth and market dominance in the coming years.

- Barrier Functions: Nanotechnology enables the creation of enhanced barrier properties in plastic pharmaceutical packaging.

- Antimicrobial Solutions: Companies are integrating antimicrobial nanotechnology to improve the safety and longevity of packaging.

- Enhanced Properties: Nanotech innovations are being used to make plastic packaging smarter and more efficient.

- Future Prospects: The integration of nanotechnology is set to propel growth in the plastic packaging sector.

Asia-Pacific to Occupy Major Share

The Asia-Pacific region stands out as the fastest-growing segment in the Pharmaceutical Packaging Market. In 2022, this region held a 40.12% market share, valued at USD 36.60 billion. The market is projected to reach USD 54.59 billion by 2028, exhibiting a robust CAGR of 6.99% during the forecast period. This growth rate outpaces other regions, positioning Asia-Pacific as a key driver of the global pharmaceutical packaging market.

- Market Share: Asia-Pacific holds 40.12% of the global pharmaceutical packaging market.

- Growth Rate: The region is expected to grow at a CAGR of 6.99% from 2023 to 2028.

- Regional Dominance: China and India lead the pharmaceutical packaging market in Asia-Pacific.

- Emerging Trends: The region's rapid growth is driven by increasing demand for innovative and sustainable packaging.

Pharmaceutical Packaging Industry Overview

Global Players Dominate Consolidated Market:

The pharmaceutical packaging market is characterized by the dominance of global players with diverse product portfolios. Companies like Amcor PLC, Schott AG, and Berry Global Group Inc. lead the market, offering a wide range of packaging solutions from bottles and vials to blister packs and syringes. The market structure appears fairly consolidated, with these major players holding significant market share due to their extensive product lines, global presence, and technological capabilities.

Amcor PLC: A global leader in pharmaceutical packaging, with solutions ranging from blister packs to child-resistant bottles.

Schott AG: Specializes in glass-based packaging and pharmaceutical tubing, driving innovation in containment solutions.

Berry Global Group Inc.: Offers extensive plastic packaging solutions, from bottles to prefillable syringes, and is expanding in emerging markets.

Consolidated Market: The market is dominated by large companies with significant technological expertise and product diversity.

Innovation and Sustainability Drive Market Leadership:

Market leaders are distinguished by their focus on innovation and sustainability. Amcor PLC, for instance, introduced the AmFiber family of paper-based products and the PVC-free AmSky blister system for healthcare applications in FY22. Berry Global Group launched a complete bundle solution for child-resistant and tamper-evident syrup and liquid medicine packaging. These companies are also investing heavily in sustainable packaging solutions, with Amcor targeting 30% recycled material across its portfolio by 2030. Their market leadership is further solidified by strategic expansions, such as Berry Global's new manufacturing facility in Bangalore, India, enhancing regional and global access to advanced healthcare solutions.

Sustainability Focus: Companies are prioritizing recyclable and eco-friendly materials to meet sustainability goals.

Innovative Solutions: PVC-free blister packs and child-resistant bottles are gaining traction as safer, sustainable alternatives.

Strategic Expansions: New facilities in emerging markets enable global players to tap into regional demand and grow market share.

R&D Investment: Leading companies invest in R&D to drive sustainable innovation in pharmaceutical packaging.

Factors for Future Success in the Market:

For market players to succeed and grow their market share, several key factors emerge. Firstly, investment in research and development is crucial, as exemplified by Amcor's introduction of innovative products. Secondly, expanding manufacturing capabilities in emerging markets, like Berry Global's new facility in India, is essential for tapping into growing demand. Thirdly, a focus on sustainability is becoming increasingly important, with companies like Klockner Pentaplast introducing recyclable PET blister films. Lastly, strategic acquisitions and partnerships, such as Aptar Pharma's acquisition of Metaphase Design Group, can enhance product offerings and service capabilities. These strategies will be critical for companies looking to strengthen their position or disrupt the market in the coming years.

R&D Investment: Companies must continue to innovate to stay competitive in a rapidly evolving industry.

Emerging Markets: Expansion in high-growth regions like Asia-Pacific is crucial for future market success.

Sustainability Mandate: Companies must address environmental concerns by prioritizing recyclable and biodegradable materials.

Strategic Acquisitions: Acquisitions and partnerships will help expand product offerings and accelerate innovation in pharmaceutical packaging.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Degree of Competition

- 4.4 Assessment of Impact of the COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Regulatory Standards on Packaging and Stringent Norms Against Counterfeit Products

- 5.1.2 Impact of Nanotechnology due to Innovative and New- generation Packaging Solutions

- 5.1.3 Regulatory Landscape Shapes Packaging Innovation

- 5.2 Market Challenges

- 5.2.1 Fluctuations in Raw Material Cost Due to Suppliers Bargaining Power

6 MARKET SEGMENTATION

- 6.1 By Material

- 6.1.1 Plastics

- 6.1.2 Glass

- 6.1.3 Other Materials

- 6.2 By Product Type

- 6.2.1 Bottles

- 6.2.2 Syringes

- 6.2.3 Vials and Ampoules

- 6.2.4 Tubes

- 6.2.5 Caps and Closures

- 6.2.6 Labels

- 6.2.7 Other Product Types

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 Germany

- 6.3.2.2 United Kingdom

- 6.3.2.3 France

- 6.3.2.4 Italy

- 6.3.2.5 Spain

- 6.3.2.6 Rest of Europe

- 6.3.3 Asia-Pacific

- 6.3.3.1 China

- 6.3.3.2 Japan

- 6.3.3.3 India

- 6.3.3.4 South Korea

- 6.3.3.5 Rest of Asia-Pacific

- 6.3.4 Latin America

- 6.3.4.1 Brazil

- 6.3.4.2 Mexico

- 6.3.4.3 Rest of Latin America

- 6.3.5 Middle East and Africa

- 6.3.5.1 United Arab Emirates

- 6.3.5.2 Saudi Arabia

- 6.3.5.3 South Africa

- 6.3.5.4 Rest of Middle East and Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Amcor PLC

- 7.1.2 3M Company

- 7.1.3 Schott AG

- 7.1.4 WestRock Company

- 7.1.5 Berry Global Group Inc.

- 7.1.6 McKesson Corporation

- 7.1.7 AptarGroup Inc.

- 7.1.8 Klockner Pentaplast Group

- 7.1.9 CCL Industries Inc.

- 7.1.10 FlexiTuff International Ltd

- 7.1.11 Gerresheimer AG

- 7.1.12 West Pharmaceutical Services Inc.

- 7.1.13 Becton, Dickinson and Company

- 7.1.14 Vetter Pharma International GmbH

- 7.1.15 Catalent Inc.

- 7.1.16 W. L. Gore & Associates Inc.

- 7.1.17 Nipro Corporation

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

全球營養保健品包裝市場(按產品形態、產品類型、包裝類型、材料、成分和地區分類)- 預測至 2030 年

全球營養保健品包裝市場(按產品形態、產品類型、包裝類型、材料、成分和地區分類)- 預測至 2030 年 保健食品包裝市場-全球產業規模、佔有率、趨勢、機會和預測,按產品形式、產品類型、包裝類型、材料、成分、地區和競爭細分,2020-2030F醫藥瓶市場 - 全球產業規模、佔有率、趨勢、機會和預測,按瓶子、按應用、按最終用戶、按地區和競爭進行細分,2020-2030F

保健食品包裝市場-全球產業規模、佔有率、趨勢、機會和預測,按產品形式、產品類型、包裝類型、材料、成分、地區和競爭細分,2020-2030F醫藥瓶市場 - 全球產業規模、佔有率、趨勢、機會和預測,按瓶子、按應用、按最終用戶、按地區和競爭進行細分,2020-2030F 臨床試驗包裝市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

臨床試驗包裝市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 醫藥塑膠包裝:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)2025年益生菌包裝全球市場報告

醫藥塑膠包裝:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)2025年益生菌包裝全球市場報告 醫藥塑膠包裝市場,依產品類型、應用、最終用戶、國家及地區分類-2025 年至 2032 年全球產業分析、市場規模、市場佔有率及預測2025年全球醫藥包裝設備市場報告

醫藥塑膠包裝市場,依產品類型、應用、最終用戶、國家及地區分類-2025 年至 2032 年全球產業分析、市場規模、市場佔有率及預測2025年全球醫藥包裝設備市場報告 栓劑包裝市場預測至 2030 年:按包裝類型、材料、應用和地區進行的全球分析醫藥包裝設備市場規模、佔有率、成長分析,按產品、按配方、按自動化、按最終用戶、按地區 - 行業預測,2025 年至 2032 年

栓劑包裝市場預測至 2030 年:按包裝類型、材料、應用和地區進行的全球分析醫藥包裝設備市場規模、佔有率、成長分析,按產品、按配方、按自動化、按最終用戶、按地區 - 行業預測,2025 年至 2032 年