|

市場調查報告書

商品編碼

1687079

氣溶膠塗料:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)Aerosol Paints - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

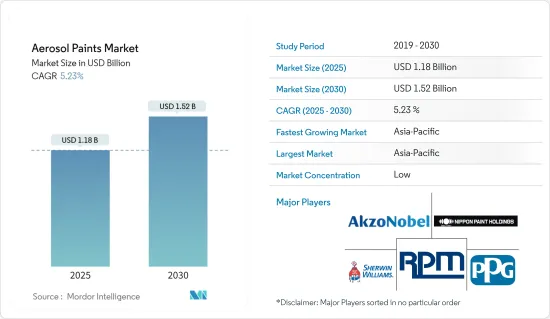

預計 2025 年氣霧漆市場規模為 11.8 億美元,到 2030 年將達到 15.2 億美元,預測期內(2025-2030 年)的複合年成長率為 5.23%。

由於製造部門關閉、建設活動停止以及供應鏈中斷,COVID-19 導致對噴漆的需求下降。目前,市場已從疫情中恢復,並呈現顯著的成長率。

預計預測期內,住宅和商業建設活動的增加以及 DIY 活動中噴漆使用量的增加將推動噴漆市場的發展。

然而,嚴格的VOC法規可能會對市場產生限制作用。

噴漆新技術可望為市場帶來新的機會。

亞太地區在全球市場佔據主導地位,其中中國需求強勁,其次是印度和日本。

氣霧漆市場趨勢

建築業佔據市場主導地位

- 建築業佔據了氣霧塗料市場的需求。氣溶膠塗料用於各種建築塗裝應用,包括清漆、底漆、內外塗料和著色劑。它們也用於住宅、商業和機構建築施工現場。

- 噴漆通常用於修補和修復建築表面,例如牆壁、天花板和裝飾。噴漆可以幫助您獲得一致的效果,特別是在傳統噴漆方法難以應用的區域。此外,噴漆具有多種顏色和飾面,可實現建築設計的客製化和創意。

- 在亞太地區,印度、中國、菲律賓、越南和印尼等國家的住宅正在強勁成長。在北美,由於移民數量的增加和核心家庭趨勢的出現,對住宅和修繕工程的需求正在成長。

- 印尼是東南亞最大、成長最快的建築市場之一。印尼政府已啟動一項在全國建造約一百萬套住宅的計劃,政府為此已累計約10億美元。

- 此外,美國擁有世界上最大的建築業之一。根據美國人口普查局的數據,預計2023年美國建築量將達到19,787億美元,較2022年增加7%以上。此外,2024年2月核准建築許可的私人住宅單位數量為151.8萬套,較2023年同期成長2.4%。

- 德國擁有歐洲大陸最大的建築業。然而,近幾個月來建築業一直呈下滑趨勢。德國聯邦統計局數據顯示,2023年德國頒發的住宅建築許可數量為26.01萬份,減少9.41萬份。此外,預計2023年德國公寓建築許可數量將下降27%,凸顯建築和房地產行業需求低迷。

- 因此,預計預測期內建築建設活動的增加將主導氣霧塗料市場。

亞太地區佔市場主導地位

- 預計亞太地區將主導全球市場。由於中國、印度和日本等國家在汽車、建築、木材和包裝等行業的消費不斷成長,該地區的噴漆使用量呈上升趨勢。

- 氣溶膠塗料用於汽車領域,塗覆汽車和汽車OEM零件的表面,以保護表面並增強美觀度。由於消費者和汽車愛好者廣泛採用噴漆進行修補、客製化和細節處理等各種用途,因此噴漆的售後市場需求高於生產用途。

- 根據OICA預測,2023年中國乘用車銷量將達2,600萬輛,較2022年成長10%以上;商用車銷量將達403萬輛,較2022年成長22%以上。

- 此外,2023年印度汽車總銷量將達507萬輛,比2022年成長7.5%以上。其中,印度乘用車總銷量為410萬輛,較2022年成長8.2%。

- 在意識到小規模使用噴漆的成本效益和美學優勢後,建築業擴大在建築應用中使用噴漆。噴漆被塗在表面以提供光滑、均勻的表面並改善結構的美觀。噴漆用於在牆壁和其他表面上創造複雜的設計、圖案和藝術作品。

- 建築業是中國持續經濟發展的重要貢獻者。根據住宅及城鄉建設部預測,2025年,中國建築業佔GDP的比重預計將維持在6%。

- 此外,近年來日本的住宅和建築業也經歷了名義成長。日本正在興建許多豪華公寓和多用戶住宅。例如,三菱集團正在建造日本最高的建築,該建築將包含50套豪華公寓,每套月租金為43,000美元。該計劃正在東京車站附近建設,預計2027年竣工。

- 因此,預計預測期內亞太地區汽車銷量的成長和建築建設的增加將推動對氣霧塗料的需求。

氣霧漆產業概況

氣霧漆市場比較分散。主要參與企業(不分先後順序)包括 Sherwin Williams、AkzoNobel NV、Nippon Paint Holdings、RPM International 和 PPG Industries Inc.

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 驅動程式

- 住宅和商業建設活動增加

- DIY 活動中噴漆的使用增加

- 限制因素

- 嚴格的VOC法規阻礙成長

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場區隔

- 樹脂

- 丙烯酸纖維

- 環氧樹脂

- 聚氨酯

- 醇酸

- 其他樹脂(聚酯、矽膠、乙烯基)

- 科技

- 溶劑型

- 水性

- 最終用戶產業

- 車

- 建築學

- 木質包裝

- 運輸

- 其他終端用戶產業(牆面塗鴉、金屬、塑膠、冰箱、自行車等)

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭格局

- 併購、合資、合作與協議

- 市場排名分析

- 主要企業策略

- 公司簡介

- Aeroaids Corporation

- Akzo Nobel NV

- BASF SE

- Kobra Paint

- Masco Corporation

- Nippon Paint Holdings Co. Ltd

- PPG Industries Inc.

- RPM International Inc.

- Rusta LLC

- The Sherwin-Williams Company

第7章 市場機會與未來趨勢

- 新技術創造成長機會

The Aerosol Paints Market size is estimated at USD 1.18 billion in 2025, and is expected to reach USD 1.52 billion by 2030, at a CAGR of 5.23% during the forecast period (2025-2030).

The demand for aerosol paints decreased due to COVID-19 owing to the shutdown of manufacturing units, a halt in construction activities, and disruption in the supply chain. Currently, the market has recovered from the pandemic and is growing at a significant rate.

Rising residential and commercial construction activities and increasing usage of aerosol paints in DIY activities are likely to drive the aerosol paints market during the forecast period.

However, stringent VOC regulations are likely to act as restraints for the market.

Nevertheless, emerging technologies for aerosol paints are expected to provide new opportunities for the market.

Asia-Pacific dominates the global market, with robust demand from China, followed by India and Japan.

Aerosol Paints Market Trends

Architectural Industry to Dominate the Market

- The architectural segment dominates the demand in the aerosol paints market. Aerosol paints are used in various architectural finishing applications, including varnishes, primers, interior and exterior paints, and stains. These are also utilized in architectural structure sites, including residential, commercial, or institutional structures.

- Aerosol paints are often employed for touch-up and repair work on architectural surfaces, such as walls, ceilings, and trims. They can help achieve a consistent finish, especially in areas that are challenging to access with traditional painting methods. Additionally, aerosol paints come in various colors and finishes, allowing for customization and creativity in architectural designs.

- Asia-Pacific has been witnessing strong growth in residential construction in countries such as India, China, the Philippines, Vietnam, and Indonesia. Besides, in North America, there has been a high housing and repair construction demand owing to increased immigrants and the trend of nuclear families.

- In Southeast Asia, Indonesia is one of the largest and fastest-growing architectural markets. The Indonesian government started a program to build about one million housing units across the country, for which the government has allocated about USD 1 billion in the budget.

- Additionally, the United States has one of the world's largest construction industries. According to the United States Census Bureau, in 2023, the construction value in the country reached USD 19,78,700 million, registering an increase of more than 7% compared to 2022. Moreover, in February 2024, privately owned housing units authorized by building permits stood at 1,518,000 units, registering an increase of 2.4% compared to the same period in 2023.

- Germany has the largest construction industry in the European continent. However, the country has been facing a downward trend in the construction industry for the past few months. According to the Federal Office of Statistics in Germany, in 2023, the construction of 260,100 dwellings was permitted in Germany, which was a decrease of 94,100 building permits. Furthermore, building permits for apartments in Germany fell by 27% in 2023, underscoring a downturn in construction and real estate industry demand.

- Hence, the rising architectural construction activities are expected to dominate the market for aerosol paints during the forecast period.

Asia-Pacific to Dominate the Market

- Asia-Pacific is expected to dominate the global market. With growing consumption from industries such as automotive, architecture, wood, and packaging from countries such as China, India, and Japan, the usage of aerosol paints is increasing in the region.

- Aerosol paints are used in the automotive sector to coat the surfaces of vehicles and automotive OEM parts to protect the surface and enhance its aesthetic appearance. The aftermarket demand for aerosol coatings is higher than that for production usage owing to the diverse applications and widespread adoption of aerosol coatings for touch-up, customization, and detailing purposes by consumers and automotive enthusiasts.

- According to OICA, in 2023, the sales of passenger vehicles in China stood at 26 million units, registering an increase of more than 10% as compared to 2022, while those of commercial vehicles stood at 4.03 million units, registering an increase of more than 22% as compared to 2022.

- Furthermore, in 2023, the total sales of vehicles in India stood at 5.07 million units, registering an increase of more than 7.5% compared to 2022. The sales of passenger vehicles in the country stood at 4.1 million units, registering an increase of 8.2% compared to 2022.

- Manufacturers are increasingly using aerosol paints for architectural applications after realizing the cost benefits and aesthetic quality associated with aerosol paints when used on a small scale. Aerosol paints are applied on surfaces to provide a smooth and even finish, enhancing the aesthetics of structures. They are used to create intricate designs, patterns, and artworks on walls and other surfaces.

- The construction sector is a key contributor to China's continued economic development. As per the forecast given by the Ministry of Housing and Urban-Rural Development, China's construction sector is expected to maintain a 6% share of the country's GDP going into 2025.

- In addition, the housing and construction industry has also witnessed nominal growth in Japan in the past couple of years. Many luxury apartments and residential complexes are under construction in Japan. For instance, Mitsubishi State is constructing Japan's tallest building, which comprises 50 luxury apartments, each generating USD 43,000 monthly rent. The project is being built near the Tokyo station and is likely to be completed by 2027.

- Hence, growing sales of automobiles and rising architectural construction in Asia-Pacific are expected to boost the demand for aerosol paints during the forecast period.

Aerosol Paints Industry Overview

The aerosol paints market is fragmented in nature. The major players (not in any particular order) include Sherwin Williams, AkzoNobel NV, Nippon Paint Holdings Co. Ltd, RPM International, and PPG Industries Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Rising Residential and Commercial Construction Activities

- 4.1.2 Increasing Usage of Aerosol Paints in DIY Activities

- 4.2 Restraints

- 4.2.1 Stringent VOC Regulations to Hinder the Growth

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Resin

- 5.1.1 Acrylic

- 5.1.2 Epoxy

- 5.1.3 Polyurethane

- 5.1.4 Alkyd

- 5.1.5 Other Resins (Polyester, Silicone, and Vinyl)

- 5.2 Technology

- 5.2.1 Solvent-borne

- 5.2.2 Water-borne

- 5.3 End-User Industry

- 5.3.1 Automotive

- 5.3.2 Architectural

- 5.3.3 Wood and Packaging

- 5.3.4 Transportation

- 5.3.5 Other End-user Industries (Wall Graffiti, Metals, Plastics, Refrigerators, Bicycles, etc.)

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Aeroaids Corporation

- 6.4.2 Akzo Nobel NV

- 6.4.3 BASF SE

- 6.4.4 Kobra Paint

- 6.4.5 Masco Corporation

- 6.4.6 Nippon Paint Holdings Co. Ltd

- 6.4.7 PPG Industries Inc.

- 6.4.8 RPM International Inc.

- 6.4.9 Rusta LLC

- 6.4.10 The Sherwin-Williams Company

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Emerging Technologies to Create Growth Opportunities

氣霧閥市場報告(按類型(連續式、計量式)、容器類型(玻璃、金屬)、最終用途行業(個人護理、家庭護理、醫療保健、汽車等)和地區)2025 年至 2033 年

氣霧閥市場報告(按類型(連續式、計量式)、容器類型(玻璃、金屬)、最終用途行業(個人護理、家庭護理、醫療保健、汽車等)和地區)2025 年至 2033 年 北美氣霧罐:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)氣霧罐:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

北美氣霧罐:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)氣霧罐:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 氣霧閥市場規模、佔有率及成長分析(按產品類型、材料、應用和地區)-2025-2032 年產業預測氣霧劑市場規模、佔有率及成長分析(按推進劑類型、推進力、閥門類型、材料、類型、最終用途、應用和地區)-2025-2032 年產業預測

氣霧閥市場規模、佔有率及成長分析(按產品類型、材料、應用和地區)-2025-2032 年產業預測氣霧劑市場規模、佔有率及成長分析(按推進劑類型、推進力、閥門類型、材料、類型、最終用途、應用和地區)-2025-2032 年產業預測 全球氣霧劑市場研究報告 - 產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年

全球氣霧劑市場研究報告 - 產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年 2025 年全球氣霧閥市場報告全球氣霧罐市場:未來預測(2025-2030)氣霧罐市場 - 全球行業規模、佔有率、趨勢、機會和預測,細分,按產品類型、按推進劑類型、按最終用戶、按地區和競爭,2020-2030F

2025 年全球氣霧閥市場報告全球氣霧罐市場:未來預測(2025-2030)氣霧罐市場 - 全球行業規模、佔有率、趨勢、機會和預測,細分,按產品類型、按推進劑類型、按最終用戶、按地區和競爭,2020-2030F 氣霧罐市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測

氣霧罐市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測