|

市場調查報告書

商品編碼

1687243

智慧水錶-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)Smart Water Meter - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

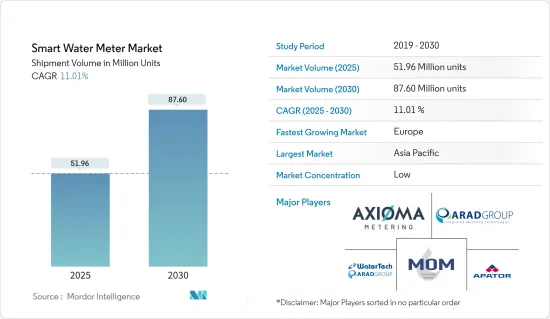

根據出貨量計算,智慧水錶市場規模預計將從 2025 年的 5,196 萬台擴大到 2030 年的 8,760 萬台,預測期內(2025-2030 年)的複合年成長率為 11.01%。

智慧水錶市場推動效率與節約

關鍵亮點

- 政府支持性法規加速採用:政府措施和法規為智慧水錶市場提供了巨大的推動力。公共和市政當局正在受益於旨在用智慧儀表取代傳統儀表的大量資金。例如,西孟菲斯獲得了 285 萬美元的津貼,用於安裝 9,000 多個智慧電錶,聖荷西水務公司獲得核准投資 1 億美元用於先進計量基礎設施 (AMI)。這些努力的重點是改善客戶服務、減少溫室氣體排放和促進節約用水。

- 政府資助大規模智慧電錶安裝

- 監管支援:允許公用事業公司投資 AMI 技術

- 環境目標:協調永續性與保護工作

- 需要提高用水量和效率:水務公司面臨提高效率和解決老化基礎設施的壓力。智慧水錶可幫助自來水公司偵測洩漏、減少水損失並提供即時使用資料。例如,杜拜電力和水務局(DEWA)檢測到超過 130 萬起漏水事件,減少了 218,373 噸二氧化碳排放。在美國,每天有近60億加侖的處理過的水被浪費,基礎設施投資正在蓬勃發展。

- 洩漏檢測:智慧儀表可快速識別和緩解

- 即時資料:支援改善節水策略

- 基礎設施投資:規劃進行重大改進

- 減少因需求增加而造成的未計費水量水損失:無收入水(NRW)損失對營業單位在財務和環境方面都構成了重大挑戰。智慧電錶可以實現精確測量、洩漏檢測和資料分析。亞洲開發銀行強調了減少無收益水對於擴大服務覆蓋範圍和滿足日益成長的需求的重要性。例如,馬尼拉的梅尼勒德水務公司採用區域計量和智慧技術,將其無收益水量 (NRW) 降低了 30.31%,同時將其服務覆蓋率擴大至 95%。

- 減少無收益水(NRW):智慧水錶有助於量化和減少水資源損失

- 區域計量:改善水損控制措施

- 公共產業的成功:利用智慧技術減少NRW以改善營運

- 數位化與業務效率:智慧水錶透過提供準確、詳細的用水資訊的 AMI 系統推動水務公司的數位轉型。這些資料有助於做出更好的決策、增加收益並提高計費效率。撒丁島的 Abbanoa SpA 和 Itron 之間的合作展示了智慧電錶技術如何利用超音波技術來幫助檢測洩漏並減少 NRW。

- AMI 系統:為公共產業公司提供實際的見解

- 即時監控:快速偵測洩漏並解決問題

- 數位轉型:改善公共產業和客戶服務

- 市場格局與競爭環境:智慧水錶市場競爭激烈,既有 Badger Meter、Honeywell 和 Itron 等老牌參與企業,也有利用物聯網技術的 WaterGroup 等新興參與企業。技術提供者和公共產業之間加強夥伴關係正在加速各地區採用客製化解決方案。

- 透過為現有參與企業提供全面的解決方案來促進創新

- 技術夥伴關係:加速智慧電錶的全球普及

- 多樣化產品:滿足多樣化公共產業需求

隨著水資源短缺和高效資源管理變得越來越重要,智慧水錶市場將進一步擴大。先進通訊協定和資料分析的整合將加強智慧水錶的作用,並鞏固其在未來水資源管理中的地位。

智慧水錶市場趨勢

預計住宅領域將佔據主要市場佔有率

- 市場主導地位與成長軌跡:自動抄表 (AMR) 技術領域將在智慧水錶市場中佔據最大市場佔有率,到 2022 年將佔整個市場的 63.95%。預計到 2028 年,AMR 技術的出貨量將達到 3,273 萬台,2023 年至 2028 年的複合年成長率為 5.04%。

- AMR市場佔有率:AMR將在智慧水錶產業保持主導地位。

- 複合年成長率預測:預計該部分將以 5.04% 的複合年成長率穩步成長。

- 成本效益:AMR 正在降低公共產業公司的營運成本並提高效率。

- 技術優勢推動採用:AMR 技術可讓公共產業公司無需實體存取電錶即可收集電錶讀數,有助於降低營運成本並提高效率。這項技術可以實現更頻繁、更準確的抄表,從而實現更好的水資源管理並減少未計費水量水損失。

- 遠端抄表:AMR 允許公共產業公司從遠端位置收集電錶資料。

- 營運效益:透過減少人事費用和運輸成本來提高效率。

- 水資源管理:頻繁抄表可改善水資源管理

- 轉向先進的解決方案雖然 AMR 仍然是主流,但市場正在逐漸轉向更先進的解決方案。先進計量基礎設施 (AMI) 領域雖然規模較小,但成長速度更快,複合年成長率為 18.27%,顯示更先進的智慧水計量系統趨勢。

- AMI 成長:AMI 技術的複合年成長率為 18.27%。

- 進階功能:AMI提供更詳細的資料和即時監控功能。

- 技術演進:向 AMI 的轉變代表著對即時資料日益成長的需求。

- 產業發展與採用:各個地區的公共產業正在將其傳統的水計量系統升級為 AMR 技術。例如,2023 年 1 月,Sweetwater 市宣布計劃在五個月內在家庭和企業安裝約 4,500 台超音波智慧水錶。

- 新發展 Sweetwater 將於 2023 年安裝智慧水錶,這將成為區域推廣的一個例子。

- 每小時資料:消費者可以詳細、即時地了解他們的用水情況。

- 漏水警報:自動漏水警報可提高節水效果並減少水損失。

- 市場促進因素與展望:許多地區對節水的需求日益成長以及水利基礎設施老化,推動著 AMR 技術的應用。例如,在美國,水資源管理是一項重大挑戰,有220萬人缺乏自來水和基本的室內管道,超過4,400萬人缺乏足夠的供水設施。預計這些因素將在未來幾年維持對 AMR 技術的需求。

- 節約用水:日益嚴重的水資源短缺是採用 AMR 技術的主要驅動力。

- 基礎設施挑戰:老化的供水系統正在推動公共產業採用智慧解決方案。

- 未來需求:由於持續存在的水資源挑戰,對 AMR 技術的需求預計將保持強勁。

預計歐洲將出現顯著成長

- 市場成長與預測:歐洲是智慧水錶市場成長最快的區域,預計出貨量將從 2022 年的 1,066 萬台增加到 2028 年的 2,101 萬台,預測期內的複合年成長率為 12.02%。

- 區域擴張:歐洲將處於領先地位,2023 年至 2028 年的複合年成長率為 12.02%。

- 強勁需求:水資源短缺問題和監管壓力正在推動該地區的需求。

- 出貨量成長:到2028年,歐洲出貨量將成長近一倍。

- 區域成長動力:歐洲的快速成長受到多種因素的推動,包括嚴格的水資源保護法規、老化的水利基礎設施以及對水資源短缺問題認知的提高。歐盟 (EU) 的水資源管理和永續性政策正在推動公共產業公司採用智慧水計量解決方案。

- 監管推動:歐盟節水措施加速採用

- 老化系統:歐洲公用事業公司正在尋找解決其老化基礎設施問題的方案。

- 永續性:該地區對永續性的關注正在推動智慧水錶的發展。

- 技術進步與創新:歐洲公司處於智慧水錶技術發展的前沿。例如,丹麥的卡姆魯普提供多種智慧水錶解決方案,包括flowIQ系列,可提供高精度、長期穩定的水量測量。

- 創新領導者:卡姆魯普等歐洲公司處於技術發展的前沿。

- 高精度工具:flowIQ 系列提供高精度水計量解決方案。

- 注重永續性:長期穩定性和節約用水。

- 市場舉措和合作歐洲各地的政府和公共產業公司正在啟動舉措,以實現其水利基礎設施的現代化。 2023 年 6 月,英國水務監管機構 Ofwat 批准了一項價值 22 億英鎊(29.3 億美元)的計劃,以加速推出七個智慧水錶方案,目標是到 2025 年底核准462,000 個智慧水錶。

- 監管支援:Ofwat 的 22 億英鎊(29.3 億美元)計畫將加速英國智慧電錶的推廣。

- 廣泛部署:2025年,英國將安裝462,000台智慧電錶。

- 基礎設施現代化舉措旨在實現水利基礎設施的現代化。

智慧水錶市場概況

全球參與企業主導整合市場

主要企業利用技術和規模:霍尼韋爾、Itron 和 Landis+Gyr 等全球參與企業利用其大規模營運和廣泛的產品系列來引領市場。例如,霍尼韋爾擁有 97,000 名員工,並不斷創新用於 AMI 的下一代蜂窩模組 (NXCM)。這些參與企業專注於技術進步和策略夥伴關係關係以保持其優勢。

大型企業:市場領導憑藉規模和影響力獲得優勢

專注於技術:創新是保持領先的關鍵

產品系列:全面的產品供應鞏固了市場地位

市場成功策略:成功的策略包括對物聯網、人工智慧和長壽命電池系統的投資。像 Xylem 這樣的公司正專注於隱藏收入定位器等創新解決方案。 Sensus 與 Larsen & Toubro 之間的夥伴關係對於解決基礎設施挑戰至關重要。

創新重點:物聯網與人工智慧推動產品開發

託管服務:幫助公用事業提高業務效率

策略聯盟:促進市場擴張和解決方案提供

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概覽

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家/消費者的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

- 產業價值鏈分析

- 智慧水錶類型的技術簡介

- 智慧電錶投資報酬率分析

- 目前使用的主要通訊協定及其比較

- LoraWAN實施步驟/關鍵使用案例/長期影響

- 公共產業透過智慧電錶實施/數位化獲得的效益

第5章市場動態

- 市場促進因素

- 政府支持限制

- 需要提高用水量和效率

- 減少非收入水損失的需求增加

- 市場限制

- 高成本和安全隱患

- 與智慧電錶整合困難

- 更換供應商的成本

第6章市場區隔

- 依技術

- 自動抄表

- 先進的測量基礎設施

- 按應用

- 住宅

- 商業

- 工業的

- 按地區

- 北美洲

- 歐洲

- 亞洲

- 澳洲和紐西蘭

- 拉丁美洲

- 中東和非洲

第7章競爭格局

- 公司簡介

- Watertech SPA(Arad Group)

- Mom Zrt

- Apator SA

- Arad Group

- Axioma Metering

- Badger Meter Inc.

- Diehl Stiftung & Co. KG

- Honeywell International Inc.

- Suntront tech Co., Ltd.

- Maddalena SPA

- WavIoT

- Itron Inc.

- BETAR Company

- Kamstrup A/S

- Landis+GYR Group AG

- Integra Metering AG

- G. Gioanola Srl

- Sensus Usa Inc.(Xylem Inc.)

- Zenner International Gmbh & Co. KG

第8章投資分析

第9章 市場機會與未來趨勢

The Smart Water Meter Market size in terms of shipment volume is expected to grow from 51.96 million units in 2025 to 87.60 million units by 2030, at a CAGR of 11.01% during the forecast period (2025-2030).

Smart Water Meter Market: Driving Efficiency and Conservation

Key Highlights

- Supportive Government Regulations Accelerate Adoption: Government initiatives and regulations are significantly advancing the smart water meter market. Utilities and municipalities are benefiting from substantial funding aimed at replacing traditional meters with smart alternatives. For instance, West Memphis received a USD 2.85 million grant to install over 9,000 smart meters, while San Jose Water secured approval for a USD 100 million investment in Advanced Metering Infrastructure (AMI). These efforts focus on enhancing customer service, reducing greenhouse gas emissions, and promoting water conservation.

- Government funding: Enables large-scale smart meter installations

- Regulatory support: Allows utilities to invest in AMI technology

- Environmental goals: Align with sustainability and conservation efforts

- Need for Improvement in Water Utility Usage and Efficiency: Water utilities are under increasing pressure to improve efficiency and address aging infrastructure. Smart water meters help utilities detect leaks, reduce water loss, and provide real-time usage data. For example, Dubai Electricity and Water Authority (DEWA) detected over 1.3 million leaks, leading to a reduction in CO2 emissions by 218,373 tons. In the U.S., where nearly 6 billion gallons of treated water are lost daily, investments in infrastructure are ramping up.

- Leak detection: Smart meters allow prompt identification and mitigation

- Real-time data: Supports improved water conservation strategies

- Infrastructure investment: Significant improvements are being planned

- Increasing Demand to Reduce Non-revenue Water Losses: Non-revenue water (NRW) losses represent a critical challenge for water utilities, both financially and environmentally. Smart meters help by providing accurate measurements, detecting leaks, and enabling data analysis. The Asian Development Bank highlights the importance of NRW reduction to improve service coverage and meet growing demand. For instance, Maynilad in Manila has reduced NRW to 30.31% while expanding service coverage to 95% using district metering and smart technology.

- NRW reduction: Smart meters help quantify and reduce water losses

- District metering: Improves water loss management efforts

- Utility success: NRW reduction through smart technology enhances operations

- Digitalization and Operational Efficiency: Smart water meters are driving the digital transformation of water utilities through AMI systems, which provide accurate, detailed information on water usage. This data improves decision-making, increases revenue, and enhances billing efficiency. Itron's collaboration with Abbanoa SpA in Sardinia demonstrates how smart metering technology can help detect leaks and reduce NRW using ultrasound technology.

- AMI systems: Offer actionable insights for utilities

- Real-time monitoring: Enables rapid leak detection and issue resolution

- Digital transformation: Improves utility operations and customer service

- Market Landscape and Competitive Environment: The smart water meter market is highly competitive, featuring established players like Badger Meter, Honeywell, and Itron, along with emerging startups such as WaterGroup, which leverage IoT technologies. Increased partnerships between technology providers and utilities are accelerating the adoption of tailored solutions across regions.

- Established players: Drive innovation through comprehensive solutions

- Tech partnerships: Accelerate smart meter adoption globally

- Diverse offerings: Cater to a variety of utility needs

As water scarcity and efficient resource management grow in importance, the smart water meter market is poised for further expansion. The integration of advanced communication protocols and data analytics will enhance the role of smart water meters, solidifying their place in the future of water management.

Smart Water Meter Market Trends

Residential Application Segment is Expected Hold Significant Market Share

- Market dominance and growth trajectory: The Automatic Meter Reading (AMR) technology segment holds the largest market share in the Smart Water Meter Market, accounting for 63.95% of the total market in 2022. AMR technology shipments are projected to reach 32.73 million units by 2028, growing at a CAGR of 5.04% from 2023 to 2028.

- AMR market share: AMR remains dominant in the smart water meter industry.

- CAGR forecast: The segment is projected to grow steadily at 5.04% CAGR.

- Cost efficiency: AMR reduces operational costs for utilities, enhancing efficiency.

- Technological advantages driving adoption: AMR technology offers utilities the ability to collect meter readings without physical access to the meter, reducing operational costs and improving efficiency. This technology enables more frequent and accurate readings, leading to better water management and reduced non-revenue water losses.

- Remote readings: AMR allows utilities to collect meter data remotely.

- Operational benefits: Improved efficiency through reduced labor and transportation costs.

- Water management: Frequent readings enable better management of water resources.

- Transition to advanced solutions: While AMR remains dominant, the market is witnessing a gradual shift towards more advanced solutions. The Advanced Metering Infrastructure (AMI) segment, though smaller, is growing at a much faster rate of 18.27% CAGR, indicating a trend towards more sophisticated smart water metering systems.

- AMI growth: AMI technology is growing at 18.27% CAGR.

- Advanced features: AMI provides more detailed data and real-time monitoring capabilities.

- Technological evolution: The shift towards AMI represents the growing demand for real-time data.

- Industry developments and implementations: Utilities across various regions are upgrading their traditional water metering systems to AMR technology. For instance, in January 2023, the city of Sweetwater announced plans to install approximately 4,500 Ultrasonic Smart Water Meters in homes and businesses over a five-month period, allowing customers to view hourly water usage data and receive automatic leak alerts.

- New deployments: Sweetwater's 2023 smart water meter installation exemplifies regional adoption.

- Hourly data: Consumers benefit from detailed, real-time water usage insights.

- Leak alerts: Automatic leak alerts improve water conservation and reduce water loss.

- Market drivers and future outlook: The growing need for water conservation, coupled with the aging water infrastructure in many regions, is driving the adoption of AMR technology. The United States, for example, faces significant water management challenges, with 2.2 million people lacking running water and basic indoor plumbing, and over 44 million having inadequate water systems. These factors are expected to sustain the demand for AMR technology in the coming years.

- Water conservation: Rising water scarcity is a key driver for AMR technology adoption.

- Infrastructure challenges: Aging water systems push utilities to adopt smart solutions.

- Future demand: AMR technology demand is expected to remain strong due to ongoing water challenges.

Europe is Expected to Witness Significant Growth

- Market growth and projections: Europe represents the fastest-growing regional segment in the Smart Water Meter Market, with shipments expected to increase from 10.66 million units in 2022 to 21.01 million units by 2028, registering a CAGR of 12.02% during the forecast period.

- Regional expansion: Europe leads with a 12.02% CAGR from 2023 to 2028.

- Strong demand: Water scarcity concerns and regulatory pressures drive demand in the region.

- Shipment growth: European shipments are set to nearly double by 2028.

- Drivers of regional growth: The rapid growth in Europe can be attributed to several factors, including stringent water conservation regulations, aging water infrastructure, and increasing awareness of water scarcity issues. The European Union's policies on water management and sustainability are driving utilities to adopt smart water metering solutions.

- Regulatory push: EU water conservation policies accelerate adoption.

- Aging systems: European utilities seek solutions for aging infrastructure.

- Sustainability: The region's focus on sustainability promotes smart water metering.

- Technological advancements and innovations: European companies are at the forefront of smart water meter technology development. For instance, Kamstrup, a Danish company, offers a range of smart water metering solutions, including the flowIQ series, which provides high accuracy and long-term stability in water measurement.

- Innovation leaders: Kamstrup and other European firms lead in technology development.

- Precision tools: flowIQ series offers high-accuracy water metering solutions.

- Sustainability focus: Long-term stability and water conservation are core features.

- Market initiatives and collaborations: Governments and utilities across Europe are launching initiatives to modernize water infrastructure. In June 2023, Britain's water regulator, Ofwat, approved a GBP 2.2 billion (USD 2.93 billion) plan to accelerate the rollout of seven smart water meter schemes, aiming to install 462,000 smart meters by the end of 2025.

- Regulatory support: Ofwat's GBP 2.2 billion (USD 2.93 billion) plan accelerates smart meter adoption in the UK.

- Broad rollout: By 2025, 462,000 smart meters will be installed in the UK.

- Infrastructure modernization: These initiatives target water infrastructure modernization.

Smart Water Meter Market Overview

Global Players Dominate Consolidated Market

Top Players Leverage Technology and Scale: Global players such as Honeywell, Itron, and Landis+Gyr lead the market, capitalizing on their large-scale operations and extensive product portfolios. Honeywell, for example, employs 97,000 people and continues to innovate with its Next Generation Cellular Module (NXCM) for AMI. These players focus on technological advancements and strategic partnerships to maintain dominance.

Large-scale operations: Market leaders dominate through size and reach

Technological focus: Innovation is key for maintaining leadership

Product portfolios: Comprehensive offerings strengthen market position

Strategies for Market Success: Successful strategies include investing in IoT, AI, and long-life battery systems. Companies like Xylem are focusing on innovative solutions like the Hidden Revenue Locator. Partnerships, such as Sensus's collaboration with Larsen & Toubro, are crucial for addressing infrastructure challenges.

Innovation focus: IoT and AI drive product development

Managed services: Support operational efficiency for utilities

Strategic collaborations: Drive market expansion and solution delivery

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Degree of Competition

- 4.3 Industry Value Chain Analysis

- 4.4 Technology Snapshot for types of Smart Water Meter

- 4.5 ROI Analysis for Smart Meters

- 4.6 Prominent Protocols Used and their Comparison

- 4.7 Steps Involved in Implementing LoraWAN/Prominent Use-cases/Long-term Implications

- 4.8 Advantages/Digitalization Achieved by Utilities by Smart Meter Implementations

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Supportive Government Regulations

- 5.1.2 Need for Improvement in Water Utility Usage and Efficiency

- 5.1.3 Increasing Demand to Reduce Non-revenue Water Losses

- 5.2 Market Restraints

- 5.2.1 High Costs and Security Concerns

- 5.2.2 Integration Difficulties with Smart Meters

- 5.2.3 Utility Supplier Switching Costs

6 MARKET SEGMENTATION

- 6.1 By Technology

- 6.1.1 Automatic Meter Reading

- 6.1.2 Advanced Metering Infrastructure

- 6.2 By Application

- 6.2.1 Residential

- 6.2.2 Commercial

- 6.2.3 Industrial

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Watertech S.P.A (Arad Group)

- 7.1.2 Mom Zrt

- 7.1.3 Apator SA

- 7.1.4 Arad Group

- 7.1.5 Axioma Metering

- 7.1.6 Badger Meter Inc.

- 7.1.7 Diehl Stiftung & Co. KG

- 7.1.8 Honeywell International Inc.

- 7.1.9 Suntront tech Co., Ltd.

- 7.1.10 Maddalena SPA

- 7.1.11 Waviot

- 7.1.12 Itron Inc.

- 7.1.13 BETAR Company

- 7.1.14 Kamstrup A/S

- 7.1.15 Landis+GYR Group AG

- 7.1.16 Integra Metering AG

- 7.1.17 G. Gioanola Srl

- 7.1.18 Sensus Usa Inc. (Xylem Inc.)

- 7.1.19 Zenner International Gmbh & Co. KG

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

全球智慧水錶市場(2025-2029)

全球智慧水錶市場(2025-2029) 全球智慧水錶市場(至 2030 年)按儀表類型(超音波、電磁、智慧機械)、應用(水公共事業、工業)、技術(AMI、AMR)和組件(儀表及配件、IT 解決方案、通訊)分類

全球智慧水錶市場(至 2030 年)按儀表類型(超音波、電磁、智慧機械)、應用(水公共事業、工業)、技術(AMI、AMR)和組件(儀表及配件、IT 解決方案、通訊)分類 2025-2033 年智慧水錶市場報告(按產品、儀表類型、配置類型(自動抄表、先進計量基礎設施)、組件、應用和區域)

2025-2033 年智慧水錶市場報告(按產品、儀表類型、配置類型(自動抄表、先進計量基礎設施)、組件、應用和區域) 智慧污水監測市場分析及預測至 2033 年:按類型、產品、服務、技術、組件、應用、部署、最終用戶和功能

智慧污水監測市場分析及預測至 2033 年:按類型、產品、服務、技術、組件、應用、部署、最終用戶和功能 用水和污水產業智慧水洩漏檢測解決方案的全球市場:市場佔有率分析、產業趨勢和成長預測(2025-2030)

用水和污水產業智慧水洩漏檢測解決方案的全球市場:市場佔有率分析、產業趨勢和成長預測(2025-2030) 印度 Jal Jeevan 任務中智慧水技術和平台的成長機會:預測(~2032 年)全球漏水檢測系統市場研究報告 - 2024 年至 2032 年產業分析、規模、佔有率、成長、趨勢和預測智慧水錶市場、機會、成長動力、產業趨勢分析與預測,2024-2032

印度 Jal Jeevan 任務中智慧水技術和平台的成長機會:預測(~2032 年)全球漏水檢測系統市場研究報告 - 2024 年至 2032 年產業分析、規模、佔有率、成長、趨勢和預測智慧水錶市場、機會、成長動力、產業趨勢分析與預測,2024-2032 到 2030 年漏水偵測系統市場預測:按類型、模式、應用和地區分類的全球分析

到 2030 年漏水偵測系統市場預測:按類型、模式、應用和地區分類的全球分析 智慧水錶市場報告:2030 年趨勢、預測與競爭分析

智慧水錶市場報告:2030 年趨勢、預測與競爭分析