|

市場調查報告書

商品編碼

1687247

光纖傳輸網路-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)Optical Transport Network - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

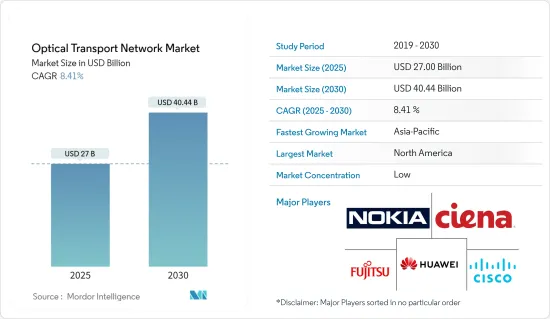

光纖傳輸網路市場規模預計在 2025 年達到 270 億美元,到 2030 年將達到 404.4 億美元,預測期內(2025-2030 年)的複合年成長率為 8.41%。

關鍵亮點

- 需求激增推動光纖傳輸網路市場成長 由於對高速網際網路的需求不斷增加以及技術的快速進步,光纖傳輸網路 (OTN) 市場正在經歷強勁成長。預計將從 2022 年的 206.8 億美元成長到 2028 年的 344.1 億美元,複合年成長率為 8.41%。

- 網路普及推動市場擴張:全球網路使用量的快速成長和對頻寬應用的需求不斷增加是推動 OTN 市場向前發展的關鍵因素。

- 增強連接性:思科預測,到 2023 年,全球 66% 的人口將能夠存取網際網路,全球用戶數量將達到 53 億。

- 設備激增:預計到 2023 年,連網設備數量將達到 293 億,平均每人擁有 3.6 台設備。

- 中國的角色:到 2021 年底,中國網路用戶將達到 10.32 億,普及率將達到 73%,凸顯了對 OTN 基礎設施管理不斷成長的資料流量的需求日益成長。

- 創新正在改變格局:OTN 解決方案供應商正在透過提高容量和效率的創新來徹底改變市場。

- Ciena 取得突破:WaveLogic 5 Extreme 技術在英國北部海底電纜上實現了創紀錄的 800GB/秒。

- 諾基亞在印尼擴張:諾基亞的部署已將爪哇島莫拉特林多的網路容量增加到 2 Terabyte,將雅加達的網路容量增加到 3 Terabyte。

- 華為的戰略願景專注於優質連接和無處不在的覆蓋,華為認為光纖傳輸解決方案是支持未來服務所需的海量頻寬的關鍵。

- 5G部署將加速市場成長:全球5G網路的快速部署是OTN市場另一個主要成長動力。

- 5G用戶成長:愛立信預測,5G用戶數將從2021年的1,200萬激增至2025年的30億以上。

- 按地區分類:北美(3.6292億),其次是西歐(3.2353億)。

- 5G 革命正在推動對先進 OTN 基礎設施日益成長的需求,以跟上資料流量的快速成長。

市場區隔揭示成長機會

關鍵亮點

- 技術領先地位:分波多工(WDM) 預計將在 2022 年佔據市場主導地位,佔有 48.08% 的佔有率,到 2028 年將以 10.68% 的複合年成長率成長。

- 產品供應:預計到 2022 年,零件將佔據 58.03% 的市場佔有率,預計成長率為 9.57%。

- 終端用戶需求:預計到 2022 年,IT 和通訊業將佔據 75.85% 的市場佔有率,複合年成長率為 9.23%。

- 地理重點:2022 年,北美將佔據 35.14% 的最高佔有率,而亞太地區將以 9.73% 的複合年成長率實現最快成長。

- 這些動態凸顯了市場在跨技術、產品和地理領域實施有針對性的成長策略的潛力。

光纖傳輸網路市場趨勢

WDM技術領域預計將佔據主要市場佔有率

- 主導市場地位:WDM 領域將鞏固其作為最大技術領域的地位,到 2022 年將佔據 OTN 市場的 48.08%。 WDM 在通訊中發揮關鍵作用,支援大容量資料傳輸,對於產業發展至關重要。

- 強勁的成長軌跡:預計 WDM 將保持高成長軌跡,2023-2028 年期間的複合年成長率為 10.68%,推動市場規模從 2022 年的 99.4 億美元成長到 2028 年的 185.8 億美元。

- 技術進步:繞過傳統傳輸系統的技術創新,例如將數位連貫光學(DCO)整合到路由器中,正在徹底改變 WDM 的採用,並為網路設計提供更大的靈活性。

- 需求激增:預計到 2021 年中期,全球 54.94% 的人口將上網,亞太地區對 WDM 的需求正在成長,尤其是在中國和印度等高成長市場。

亞太地區將經歷最快成長

- 加速市場擴張:亞太地區是 OTN 市場成長最快的地區,預計 2023 年至 2028 年的複合年成長率為 9.73%,市場規模將從 2022 年的 59.2 億美元增加到 2028 年的 106.1 億美元。

- 數位轉型的努力:中國等國家計劃在 2025 年實現 70% 的大型企業數位化,政府主導的舉措正在刺激對先進 OTN 技術的需求。

- 基礎設施投資:數位基礎設施投資,例如 Biznet 利用 Ciena 的 6500 平台在印尼的擴張,正在推動全部區域的OTN 成長。

- 5G部署和物聯網:5G的擴展和物聯網設備的激增繼續推動對大容量光纖網路的需求,尤其是在中國,2021年物聯網設備數量超過20億。

光纖傳輸網路產業概況

全球參與企業主導整合的 OTN 市場全球 OTN 市場由參與企業主導,整合程度適中。諾基亞、Ciena、思科、華為和富士通等主要通訊業者引領市場,提供廣泛的光纖傳輸解決方案,以滿足日益成長的高速資料傳輸需求。

創新和夥伴關係推動領導力創新和策略夥伴關係關係是維持市場領導地位的關鍵。例如,諾基亞和Ciena正在部署600Gbps線速等尖端解決方案,並與通訊業者合作進行大型基礎設施計劃。

成功策略:為了擴大市場佔有率,公司需要專注於投資下一代技術,如 400G光纖傳輸解決方案,開拓亞太和拉丁美洲的新興市場,以及面向服務的產品,如網路即服務模式。此外,在產品設計中注重能源效率和永續性可能是保持競爭力的關鍵。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概覽

- 產業吸引力-波特五力模型

- 新進入者的威脅

- 買家的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- 產業價值鏈分析

- COVID-19 市場影響評估

第5章市場動態

- 市場促進因素

- 由於對高速網路的需求,網路普及率不斷提高

- OTN 解決方案提供者的創新

- 市場問題

- 初期投資高

第6章市場區隔

- 依技術

- WDM

- DWDM

- 其他

- 按服務

- 服務

- 網路維護與支援

- 網路設計

- 成分

- 光纖傳輸

- 光開關

- 光學平台

- 服務

- 按行業

- 資訊科技和電信

- 醫療保健

- 政府

- 其他行業

- 按地區

- 北美洲

- 歐洲

- 亞洲

- 澳洲和紐西蘭

- 拉丁美洲

- 中東和非洲

第7章競爭格局

- 公司簡介

- Nokia Corporation

- Ciena Corporation

- Cisco Systems Incorporation

- Huawei Technologies Co. Ltd

- Fujitsu Ltd

- ZTE Corporation

- Infinera Corporation

- Telefonaktiebolaget LM Ericsson

- NEC Corporation

- Yokogawa Electric Corporation

第8章投資分析

第9章 市場機會與未來趨勢

The Optical Transport Network Market size is estimated at USD 27.00 billion in 2025, and is expected to reach USD 40.44 billion by 2030, at a CAGR of 8.41% during the forecast period (2025-2030).

Key Highlights

- Surging Demand Drives Optical Transport Network Market Growth: The Optical Transport Network (OTN) market is witnessing robust growth, spurred by rising demand for high-speed internet and rapid technological advancements. With the market projected to expand from USD 20.68 billion in 2022 to USD 34.41 billion by 2028, the industry is on track to register a CAGR of 8.41%.

- Internet Penetration Fuels Market Expansion: The surge in global internet usage and the rising demand for bandwidth-heavy applications are key factors propelling the OTN market forward.

- Increased connectivity: Cisco anticipates that by 2023, 66% of the global population will have internet access, amounting to 5.3 billion users worldwide.

- Device proliferation: Networked devices are expected to reach 29.3 billion by 2023, averaging 3.6 devices per person.

- China's role: With 1,032 million internet users and a 73% penetration rate by the end of 2021, China highlights the growing demand for OTN infrastructure to manage surging data traffic.

- Technological Innovations Reshape the Landscape: OTN solution providers are revolutionizing the market with innovations that enhance capacity and efficiency.

- Ciena's breakthrough: WaveLogic 5 Extreme technology achieved a record-breaking 800 GB/s on the NO-UK submarine cable.

- Nokia's expansion in Indonesia: Moratelindo's network capacity on Java Island was expanded to 2 terabytes, and to 3 terabytes in Jakarta, via Nokia's deployment.

- Huawei's strategic vision: Focused on premium connectivity and ubiquitous coverage, Huawei is positioning its optical transport solutions as key to supporting the massive bandwidth requirements of future services.

- 5G Deployment Accelerates Market Growth: The rapid global rollout of 5G networks is another significant growth driver for the OTN market.

- 5G subscriber growth: Ericsson projects 5G subscriptions to soar from 12 million in 2021 to over 3 billion by 2025.

- Regional adoption: North East Asia is expected to lead, with 1,460.04 million subscriptions by 2025, followed by significant growth in North America (362.92 million) and Western Europe (323.53 million).

- The 5G revolution is increasing the need for advanced OTN infrastructures capable of handling the exponential rise in data traffic.

Market Segmentation Reveals Growth Opportunities:

Key Highlights

- Technology leadership: Wavelength Division Multiplexing (WDM) dominated the market with a 48.08% share in 2022 and is expected to grow at a CAGR of 10.68% through 2028.

- Product offerings: Components led with a 58.03% market share in 2022, with a projected growth rate of 9.57%.

- End-user demand: The IT and Telecom sectors accounted for 75.85% of the market in 2022, with a forecasted 9.23% CAGR.

- Geographic focus: North America led with a 35.14% share in 2022, while Asia-Pacific is set to experience the fastest growth at a 9.73% CAGR.

- These dynamics highlight the market's potential for targeted growth strategies across technology, product, and geographic segments.

Optical Transport Network Market Trends

WDM Technology Segment is Expected to Hold Significant Market Share

- Dominant market position: The WDM segment solidified its status as the largest technology segment, capturing 48.08% of the OTN market in 2022. Its key role in telecommunications, supporting high-capacity data transmission, is critical in the industry's evolution.

- Robust growth trajectory: WDM is expected to maintain a high growth trajectory, with a projected CAGR of 10.68% from 2023 to 2028, driving its market value from USD 9.94 billion in 2022 to USD 18.58 billion by 2028.

- Technological advancements: Innovations such as the integration of digital coherent optics (DCO) into routers, bypassing traditional transport systems, are revolutionizing WDM adoption, offering greater flexibility in network design.

- Demand surge: The Asia-Pacific region, with 54.94% of the global population online by mid-2021, is driving demand for WDM, particularly in high-growth markets like China and India.

Asia-Pacific to Witness Fastest Growth

- Accelerated market expansion: Asia-Pacific is the fastest-growing region in the OTN market, with a projected CAGR of 9.73% from 2023 to 2028, reflecting a rise in market value from USD 5.92 billion in 2022 to USD 10.61 billion by 2028.

- Digital transformation initiatives: Government-led initiatives in countries like China, which aims to digitalize 70% of large enterprises by 2025, are spurring demand for advanced OTN technologies.

- Infrastructure investments: Investments in digital infrastructure, such as Biznet's expansion with Ciena's 6500 platform in Indonesia, are catalyzing OTN growth across the region.

- 5G rollout and IoT: The expansion of 5G and the proliferation of IoT devices, especially in China where IoT devices surpassed 2 billion in 2021, continue to fuel the demand for high-capacity optical networks.

Optical Transport Network Industry Overview

Global Players Dominate Consolidated OTN Market: The global OTN market is dominated by established players in a moderately consolidated landscape. Major telecoms like Nokia, Ciena, Cisco, Huawei, and Fujitsu lead the market, supplying a wide range of optical transport solutions that cater to growing demand for high-speed data transmission.

Innovation and partnerships drive leadership: Technological innovation and strategic partnerships are key to maintaining market leadership. For instance, Nokia and Ciena have introduced cutting-edge solutions, such as 600 Gbps line rates, and partnered with telecom operators for large-scale infrastructure projects.

Strategies for success: To increase market share, companies must invest in next-gen technologies like 400G optical transport solutions, tap into emerging markets in Asia-Pacific and Latin America, and focus on service-oriented offerings, such as Network-as-a-Service models. Emphasizing energy efficiency and sustainability in product design will also be critical for maintaining a competitive edge.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHT

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter Five Forces

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Internet Penetration with Demand for High-speed Internet

- 5.1.2 Technological Innovations by OTN Solution Providers

- 5.2 Market Challenges

- 5.2.1 High Initial Investment

6 MARKET SEGMENTATION

- 6.1 By Technology

- 6.1.1 WDM

- 6.1.2 DWDM

- 6.1.3 Other Technologies

- 6.2 By Offering

- 6.2.1 Service

- 6.2.1.1 Network Maintenance and Support

- 6.2.1.2 Network Design

- 6.2.2 Component

- 6.2.2.1 Optical Transport

- 6.2.2.2 Optical Switch

- 6.2.2.3 Optical Platform

- 6.2.1 Service

- 6.3 By End-user Vertical

- 6.3.1 IT and Telecom

- 6.3.2 Healthcare

- 6.3.3 Government

- 6.3.4 Other End-user Verticals

- 6.4 By Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia

- 6.4.4 Australia and New Zealand

- 6.4.5 Latin America

- 6.4.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Nokia Corporation

- 7.1.2 Ciena Corporation

- 7.1.3 Cisco Systems Incorporation

- 7.1.4 Huawei Technologies Co. Ltd

- 7.1.5 Fujitsu Ltd

- 7.1.6 ZTE Corporation

- 7.1.7 Infinera Corporation

- 7.1.8 Telefonaktiebolaget LM Ericsson

- 7.1.9 NEC Corporation

- 7.1.10 Yokogawa Electric Corporation

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

2025年全球光纖傳輸網路市場報告

2025年全球光纖傳輸網路市場報告 光纖傳輸網路市場按技術、產品、垂直和區域分類

光纖傳輸網路市場按技術、產品、垂直和區域分類 全球光纖傳輸網路設備市場(2025-2029)

全球光纖傳輸網路設備市場(2025-2029) 全球光纖傳輸網路硬體市場規模、佔有率、趨勢分析報告,依技術、OTN 設備、最終用戶、地區、展望和預測,2024-2031年光傳輸網路市場 - 按技術、產品、組件、最終用戶垂直、地區和競爭細分的全球行業規模、佔有率、趨勢、機會和預測,2019-2029F

全球光纖傳輸網路硬體市場規模、佔有率、趨勢分析報告,依技術、OTN 設備、最終用戶、地區、展望和預測,2024-2031年光傳輸網路市場 - 按技術、產品、組件、最終用戶垂直、地區和競爭細分的全球行業規模、佔有率、趨勢、機會和預測,2019-2029F 光纖傳輸網路設備市場:按技術、組件和最終用戶分類 - 全球預測 2025-20302024-2032 年按技術、組件、服務、最終用途部門和地區分類的光傳輸網路市場報告OTN 硬體市場 - 全球產業規模、佔有率、趨勢、機會和預測。按類型、按應用、服務、技術、垂直、地區、公司和地理位置細分,2018-2028 年預測和機會。全球 OTN 傳輸和交換設備市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會和預測,按通訊類型、技術類型、最終用戶垂直領域、地區、競爭細分

光纖傳輸網路設備市場:按技術、組件和最終用戶分類 - 全球預測 2025-20302024-2032 年按技術、組件、服務、最終用途部門和地區分類的光傳輸網路市場報告OTN 硬體市場 - 全球產業規模、佔有率、趨勢、機會和預測。按類型、按應用、服務、技術、垂直、地區、公司和地理位置細分,2018-2028 年預測和機會。全球 OTN 傳輸和交換設備市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會和預測,按通訊類型、技術類型、最終用戶垂直領域、地區、競爭細分 2023-2030 年全球光傳輸網路市場規模研究與預測(按技術、按組件、按服務、按最終用戶應用和地區分析

2023-2030 年全球光傳輸網路市場規模研究與預測(按技術、按組件、按服務、按最終用戶應用和地區分析