|

市場調查報告書

商品編碼

1687260

寵物食品包裝:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)Pet Food Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

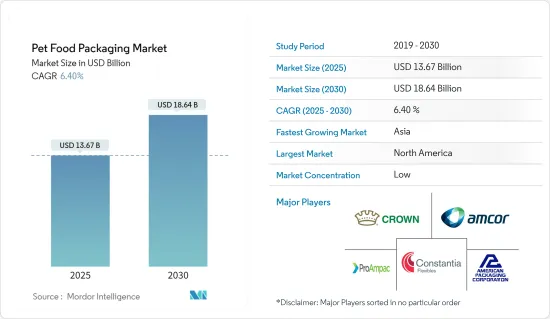

寵物食品包裝市場規模預計在 2025 年為 136.7 億美元,預計到 2030 年將達到 186.4 億美元,預測期內(2025-2030 年)的複合年成長率為 6.4%。

寵物食品包裝正在經歷顯著的成長。適當的包裝對於保持寵物食品的新鮮度和營養價值至關重要,可以保護寵物食品免受污染物、濕氣和空氣的影響。適當的包裝可確保食品免受害蟲和其他可能影響食品品質的環境因素的侵害。這使得寵物飼主更容易處理、儲存和分配食物。

關鍵亮點

- 隨著越來越多的人養寵物作為伴侶,以及飼主對維護寵物健康的意識不斷提高,寵物食品包裝市場也受到越來越多的關注。人們對寵物健康的日益關注推動了先進的防溢包裝的採用,以確保寵物食品的品質。 2023 年收容所動物統計資料顯示,進入收容所的狗的數量比離開收容所的狗的數量多 3%。具體而言,220萬隻狗找到了新家,62.5萬隻狗與飼主團聚,56.1萬隻狗在機構之間轉移。

- 美國寵物產品協會報告稱,2023-2024 年,約有 6,510 萬美國家庭擁有至少一隻狗。緊隨其後的是貓和淡水魚,分別約有 4,650 萬戶和 1,110 萬戶。隨著越來越多的寵物飼主將寵物視為家庭成員,對優質寵物食品的需求也不斷增加。

- 隨著社會契約的變化以及將寵物視為忠誠的家庭成員越來越成為一種社會規範,優質寵物食品類別的成長和發展似乎是自然而然的。新品牌的出現和 SKU 的激增以及戲劇性的包裝正在推動寵物食品行業的發展。此外,寵物食品的網路銷售正在成長,從而產生了對支援運輸和處理的包裝的需求。根據加拿大農業及農業食品部的報告,到 2023 年,寵物食品網路零售業%。寵物食品在線銷售的擴張可能會為所研究的市場創造需求。

- 食品安全法規的日益嚴格為寵物食品包裝市場的成長帶來了許多挑戰。更嚴格的食品安全法規要求製造商投資合規的包裝材料、技術和製程。這意味著更高的生產成本,小企業可能難以負擔。如果發現包裝不合規,加強監管可能會導致檢查更加頻繁,並增加召回的可能性。召回可能會損害品牌聲譽並導致經濟損失。

- 此外,通貨膨脹率上升推高了原料、能源和運輸成本,增加了與寵物食品包裝生產相關的成本。包裝成本的增加反過來可能會提高寵物食品本身的價格。此外,隨著通貨膨脹影響生活成本,消費者變得更加重視預算。這種優先事項的轉變可能會導致消費者將注意力集中在基本開支上,而減少在優質或特殊寵物食品及其相關包裝上的支出。

寵物食品包裝市場趨勢

預計乾糧市場將佔據相當大的佔有率。

- 乾寵物食品保存期限長,易於儲存,為寵物飼主和零售商提供了便利。這種穩定性和對冷藏的最低需求是它如此受歡迎的原因。根據官方資訊來源,2023 年印度乾狗糧市場規模估計約 4.82 億美元。預計到 2028 年底,這一數字將進一步成長,達到約 9.63 億美元。保存期限、大量購買和保存期限等因素是乾狗糧佔印度整個狗糧市場 88% 以上的關鍵原因。預計這些因素將推動市場成長。

- 乾糧水分活度低,微生物學上穩定,保存期限長。然而,乾糧通常不像濕糧或半濕糧那樣受寵物歡迎,可能是因為它的味道不太吸引人。相比之下,有些寵物更喜歡乾燥寵物食品,因為它的質地。這推動了乾寵物食品包裝市場的成長。

- 此外,全球寵物主人數量的不斷成長也導致對各種寵物食品的需求增加,包括乾寵物食品,乾寵物食品因其實用性和成本效益而受到青睞。根據官方資料,到2023年,印度的寵物狗數量將超過3,300萬隻。預計到2028年,這數字將超過5,100萬隻。受人喜愛的狗的數量導致全國範圍內寵物食品銷量增加。

- 乾寵物食品的包裝過去很簡單,知名品牌都使用紙袋。雀巢普瑞納等公司正在嘗試新的包裝概念。他們正在測試新的紙本材料和顧客可以自備填充用容器的系統。根據截至 2023 年 6 月 18 日當週的 IRI資料,雀巢普瑞納寵物護理是美國最暢銷的乾狗糧品牌,創造了約 25 億美元的收益。

- 據英國寵物食品協會稱,2023年英國狗糧市場價值將達18.4億英鎊(約2.33億美元)。隨著寵物食品銷售的成長,對包裝材料的需求也在成長。這種成長意味著寵物食品包裝製造商可以期待更多用於製造各種包裝解決方案的塑膠、紙張和金屬等材料的訂單。

- 此外,乾寵物食品的生產成本比濕食品低,這使其成為製造商和消費者經濟可行的選擇,也是其受歡迎程度的原因之一。此外,可重複密封的包裝袋和環保材料等先進的包裝技術正在增強乾燥寵物食品的吸引力。這些技術創新正在提高便利性和永續性,推動市場成長。

預計北美市場將出現顯著成長

- 北美對寵物食品包裝市場的成長做出了重大貢獻。美國和加拿大等國家是世界上寵物擁有率最高的國家之一。如此龐大的寵物主人群體推動了對各種寵物食品產品及其包裝的巨大需求。根據加拿大農業和食品部統計,幾年前,加拿大的寵物數量約為 2,793 萬隻,其中包括狗、貓、魚、小型哺乳動物和爬蟲類。預測顯示,到 2025 年,這一數字將超過 2,850 萬。

- 在北美,寵物食品包裝需求的不斷成長與寵物飼養量(尤其是救援犬)的成長趨勢密切相關。隨著該地區寵物擁有量的擴大,尤其是救援犬受到關注,對寵物食品的需求自然也會增加。寵物擁有量的增加推動了對寵物食品的需求,擴大了對寵物包裝的需求,並為包裝製造商提供了有利可圖的機會。

- 此外,寵物人性化是重塑寵物照護模式的關鍵趨勢。 Mondi 的研究顯示,75% 的參與者傾向於在優先考慮永續包裝的品牌上花費更多。因此,寵物食品領域的品牌將永續性放在首位,並將其解決方案與這些企業價值觀結合。此外,Mondi 等公司憑藉 BarrierPac Recyclable 等產品引領此領域。這些解決方案包括利用塑膠層壓板的預製袋和FFS卷材。這些層壓板在接受軟包裝的地區是可回收的,並且可以透過店內投遞退回,並保持其原始功能。

- BASF美國公司是使用水性乳液「JONCRYL HPB 1702」的永續寵物食品包裝的先驅。此創新解決方案可滿足寵物食品市場所需的耐油性和食品安全認證。

- 此外,美國寵物產品協會報告稱,預計到 2023 年,美國寵物產業的支出將達到 1,470 億美元,上年度的 905 億美元大幅成長。隨著寵物支出的增加,對寵物食品的需求也在增加,對包裝的需求也隨之增加,以支持這種成長的生產和消費。

- 北美是包裝創新的中心,各組織投資於獨特的材料和技術,以提高包裝的效率、功能性和美觀性。預計這些因素將推動北美寵物食品包裝市場的發展,使其成為關鍵地區。

寵物食品包裝市場概覽

寵物食品包裝市場是細分的。主要參與企業包括 Amcor Group GmbH、American Packaging Corporation、ProAmpac LLC、Constantia flexibles Group GmbH 和 Crown Holdings Inc. 隨著寵物食品產品的技術創新和寵物食品包裝市場競爭的加劇,製造商正在選擇高品質和永續的包裝來吸引更多客戶。

- 2024 年 7 月,Mondi 推出了“FlexiBag Reinforced”,這是一系列基於單一 PE 的可回收包裝解決方案,增強了其預製塑膠袋產品組合。據 Mondi 稱,這些袋子具有優異的機械性能,包括增強的抗穿刺性、增加的剛度和改善的密封性。可調節的屏障保護可提供中等至高的抗脂肪、氧氣和濕氣能力,確保內容物的新鮮度。 Mondi 特別強調寵物食品產業是這項創新功能的重點目標。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概覽

- 產業價值鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章市場動態

- 市場促進因素

- 對高級產品和品牌產品的需求不斷增加

- 提高維護寵物健康的意識

- 市場限制

- 加強食品安全監管

第6章 寵物食品市場現狀

- 寵物食品產業概況

- 寵物食品類型

- 按動物類型分類的寵物食品

第7章市場區隔

- 按材質

- 紙和紙板

- 金屬

- 塑膠

- 依產品類型

- 小袋

- 折疊式紙盒

- 金屬罐

- 包包

- 其他

- 依食物類型

- 乾糧

- 濕糧

- 冷藏/冷凍

- 按動物

- 狗糧

- 貓糧

- 其他動物

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

第8章競爭格局

- 公司簡介

- American Packaging Corporation

- ProAmpac LLC

- Constantia Flexibles Group GmbH

- Amcor Group GmbH

- Crown Holdings Inc.

- Coveris Holdings

- Polymerall LLC

- Mondi PLC

- Sonoco Products Company

- Berry Global Inc.

- Ardagh Group SA

- Wipak

- Silgan Holdings Inc.

第9章投資分析

第10章:市場的未來

The Pet Food Packaging Market size is estimated at USD 13.67 billion in 2025, and is expected to reach USD 18.64 billion by 2030, at a CAGR of 6.4% during the forecast period (2025-2030).

Pet food packaging is growing significantly. Proper packaging is essential for maintaining the freshness and nutritional value of pet food by protecting it from contaminants, moisture, and air. Proper packaging ensures the food remains safe from pests and other environmental factors that could compromise its quality. This makes it easier for pet owners to handle, store, and dispense food.

Key Highlights

- The pet food packaging market is gaining traction due to the growing adoption of pets as companions and the increasing awareness among owners about maintaining a pet's health. Growing concerns over pet health are driving the adoption of advanced, spill-proof packaging for pet food, ensuring its quality is preserved. Data from Shelter Animals Count in 2023 revealed that 3% more dogs entered shelters than exited. Specifically, 2.2 million dogs found new homes, 625,000 were reunited with their owners, and 561,000 were moved between organizations.

- In 2023-2024, the American Pet Products Association Inc. reported that around 65.1 million US households had at least one dog. Cats and freshwater fish followed, with about 46.5 million and 11.1 million households, respectively. As pet owners increasingly view their pets as family, there is an increasing demand for premium and high-quality packaged pet food.

- As the social contract shifts and treating pets as faithful family members is more of a social norm, the growth and development of the premium pet food category emerged as a natural consequence. The emergence of new brand players and the proliferation of SKUs unleashing dramatic packaging drive the pet food industry. In addition, online pet food sales are rising, which boosts demand for packaging that supports shipping and handling. As reported by Agriculture and Agri-Food Canada, online retailing in India saw pet food making up 14.5% of its sales in 2023. Such expansion in online pet food sales may create demand in the studied market.

- The increasing adoption of food safety regulations poses several challenges to the growth of the pet food packaging market. Stricter food safety regulations require manufacturers to invest in compliant packaging materials, technologies, and processes. This leads to higher production costs, which can be difficult for smaller companies to absorb. Tighter regulations may result in more frequent inspections and a higher likelihood of recalls if packaging is found to be non-compliant. Recalls can damage a brand's reputation and lead to financial losses.

- Moreover, increasing inflation drives up costs for raw materials, energy, and transportation, raising the expenses associated with pet food packaging production. This uptick in packaging material costs can, in turn, elevate the prices of the pet food products themselves. Furthermore, as inflation impacts the cost of living, consumers are likely to adopt a budget-conscious approach. This shift in priorities may lead them to focus on essential expenses, shortening their spending on premium or specialty pet foods and their associated packaging.

Pet Food Packaging Market Trends

The Dry Food Segment is Expected to Hold a Considerable Share in the Market

- Dry pet food is convenient for pet owners and retailers due to its longer shelf life and ease of storage. This stability and minimal need for refrigeration boost its popularity. According to an official source, the market value of dry dog food in India was approximately USD 482 million in 2023. This was forecast to increase further and reach approximately USD 963 million by the end of 2028. Factors such as storage, bulk purchase, and shelf life were the primary reasons for dry dog food to have a share of over 88% of all dog food in India. Such factors are expected to propel the market's growth.

- Dry pet foods have a long shelf life due to low water activity and consequent microbiological stability. However, they are typically less appealing to pets than moist or semi-moist pet foods, probably due to their low flavor appeal. In contrast, some pets may prefer dry pet foods due to their textural qualities. This drives the growth of the dry pet food packaging market.

- In addition, the rising number of pet owners globally contributes to increased demand for all types of pet food, including dry pet food, which is often preferred for its practicality and cost-effectiveness. As per official data, India had a pet dog population exceeding 33 million in 2023. Projections indicate this figure will surpass 51 million by 2028. The number of pet dogs has led to increased pet food sales nationwide.

- Packaging for dry pet food has usually been simple, with major brands using paper bags. Companies like Nestle Purina are trying new packaging ideas. They are testing new paper materials and a system where customers bring their containers for refills. Data from IRI for the week ending June 18, 2023, showed Nestle Purina PetCare as the top-selling dry dog food brand in the United States, earning about USD 2.5 billion.

- According to the UK Pet Food, the market value for dog food in the UK was GBP 1840 million (about USD 2303 million) in 2023. As pet food sales grow, so does the need for packaging materials. This increase means pet food packaging manufacturers can expect more orders for materials like plastic, paper, and metal, which are used to make various packaging solutions.

- Furthermore, dry pet food has a lower production cost than wet food, making it a more economically viable option for manufacturers and consumers, contributing to its widespread use. Also, advances in packaging technology, such as resealable pouches and eco-friendly materials, enhance dry pet food's appeal. These innovations improve convenience and sustainability, driving the market's growth.

North America is Expected to Witness a Significant Growth in the Market

- North America significantly contributes to the growth of the pet food packaging market. Countries like the United States and Canada have some of the highest pet ownership rates globally. This large pet owner base drives substantial demand for various pet food products and their packaging. According to Agriculture and Agri-Food Canada, Canada's pet population, encompassing dogs, cats, fish, small mammals, and reptiles, stood at around 27.93 million a few years ago. Projections indicate this number is expected to surpass 28.5 million by 2025.

- In North America, the rising demand for pet food packaging aligns closely with the growing trend of pet adoption, particularly for rescue dogs. As pet ownership expands in the region, especially with a focus on rescue dogs, the need for pet food naturally escalates. This uptick in pet ownership boosts the demand for pet food and amplifies the need for its packaging, presenting lucrative opportunities for packaging manufacturers.

- Furthermore, pet humanization is a pivotal trend reshaping the pet care landscape. A survey by Mondi revealed that 75% of participants are inclined to spend more on brands that prioritize sustainable packaging. As a result, brands in the pet food sector are aligning their solutions with these corporate values, placing sustainability at the forefront. Moreover, companies like Mondi lead the range with offerings like BarrierPack Recyclable. These solutions, which include premade pouches and FFS roll-stock, utilize plastic laminates. These laminates are recyclable in regions that accept flexible packaging and can be returned through store drop-off while maintaining their intended functionality.

- BASF America is pioneering sustainable pet food packaging using its water-based emulsion, JONCRYL HPB 1702. This innovative solution meets the pet food market's demands for grease resistance and food safety certifications.

- Moreover, in 2023, the US pet industry spending reached an impressive USD 147 billion, marking a substantial increase from the USD 90.5 billion recorded in prior years, as the American Pet Products Association Inc. reported. As pet expenditures rise, so does the demand for pet food, leading to an increased need for packaging to support this heightened production and consumption.

- North America is a hub for packaging innovation, with organizations investing in unique materials and technologies to improve packaging efficiency, functionality, and aesthetics. These factors are expected to drive the North American pet food packaging market, making it a critical region.

Pet Food Packaging Market Overview

The pet food packaging market is fragmented. Some of the key players are Amcor Group GmbH, American Packaging Corporation, ProAmpac LLC, Constantia Flexibles Group GmbH, and Crown Holdings Inc. With innovation in pet food products and rising competition in the pet food packaging market, manufacturers opt for quality and sustainable packaging to attract more customers.

- July 2024: Mondi introduced 'FlexiBag Reinforced,' a new line of recyclable, mono-PE-based packaging solutions, enhancing its premade plastic bags portfolio. According to Mondi, these bags boast superior mechanical properties, including enhanced puncture resistance, increased stiffness, and better sealability. The adjustable barrier protection offers medium to high resistance against fat, oxygen, and moisture, ensuring content freshness. Mondi specifically highlights the pet food industry as a prime target for this innovative feature.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increased Demand for Premium and Branded Products

- 5.1.2 Increasing Awareness about Maintaining Pet's Health

- 5.2 Market Restraints

- 5.2.1 Increasing Adoption of Food Safety Regulations

6 PET FOOD MARKET LANDSCAPE

- 6.1 Pet Food Industry Overview

- 6.2 Types of Pet Food

- 6.3 Pet Food by Animal Type

7 MARKET SEGMENTATION

- 7.1 By Material

- 7.1.1 Paper and Paperboard

- 7.1.2 Metal

- 7.1.3 Plastic

- 7.2 By Product Type

- 7.2.1 Pouches

- 7.2.2 Folding Cartons

- 7.2.3 Metal Cans

- 7.2.4 Bags

- 7.2.5 Other Product Types

- 7.3 By Type of Food

- 7.3.1 Dry Food

- 7.3.2 Wet Food

- 7.3.3 Chilled and Frozen

- 7.4 By Animal

- 7.4.1 Dog Food

- 7.4.2 Cat Food

- 7.4.3 Other Animal

- 7.5 By Geography

- 7.5.1 North America

- 7.5.2 Europe

- 7.5.3 Asia-Pacific

- 7.5.4 Latin America

- 7.5.5 Middle East and Africa

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 American Packaging Corporation

- 8.1.2 ProAmpac LLC

- 8.1.3 Constantia Flexibles Group GmbH

- 8.1.4 Amcor Group GmbH

- 8.1.5 Crown Holdings Inc.

- 8.1.6 Coveris Holdings

- 8.1.7 Polymerall LLC

- 8.1.8 Mondi PLC

- 8.1.9 Sonoco Products Company

- 8.1.10 Berry Global Inc.

- 8.1.11 Ardagh Group SA

- 8.1.12 Wipak

- 8.1.13 Silgan Holdings Inc.

9 INVESTMENT ANALYSIS

10 FUTURE OF THE MARKET

寵物食品包裝市場規模、佔有率及成長分析(依材料、產品、食品、動物及地區)-2025-2032 年產業預測

寵物食品包裝市場規模、佔有率及成長分析(依材料、產品、食品、動物及地區)-2025-2032 年產業預測 美國寵物食品包裝:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

美國寵物食品包裝:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 2025年寵物食品包裝全球市場報告

2025年寵物食品包裝全球市場報告 寵物食品包裝市場報告:2030 年趨勢、預測與競爭分析

寵物食品包裝市場報告:2030 年趨勢、預測與競爭分析 寵物食品包裝市場:按材料、產品、應用和最終用途分類 - 全球預測 2025-20302024-2032 年按材料、食品類型、動物類型、包裝形式和地區分類的寵物食品包裝市場報告寵物食品包裝市場(包裝形式:袋、袋、折疊紙盒、桶和杯、罐、瓶和罐;材料:紙和紙板、塑膠和金屬)-全球產業分析、規模、佔有率、成長、趨勢,以及預測,2024-2032

寵物食品包裝市場:按材料、產品、應用和最終用途分類 - 全球預測 2025-20302024-2032 年按材料、食品類型、動物類型、包裝形式和地區分類的寵物食品包裝市場報告寵物食品包裝市場(包裝形式:袋、袋、折疊紙盒、桶和杯、罐、瓶和罐;材料:紙和紙板、塑膠和金屬)-全球產業分析、規模、佔有率、成長、趨勢,以及預測,2024-2032 全球寵物食品包裝市場研究報告 - 2024 年至 2032 年產業分析、規模、佔有率、成長、趨勢與預測

全球寵物食品包裝市場研究報告 - 2024 年至 2032 年產業分析、規模、佔有率、成長、趨勢與預測 2023年至2028年寵物食品包裝市場預測

2023年至2028年寵物食品包裝市場預測 寵物食品包裝市場 - 按包裝類型(袋、罐、小袋、盒子/紙箱)、按材料類型(塑膠、紙和紙板、金屬)、按食品類型、按寵物類型、按配銷通路和預測,2024 年至2032 年

寵物食品包裝市場 - 按包裝類型(袋、罐、小袋、盒子/紙箱)、按材料類型(塑膠、紙和紙板、金屬)、按食品類型、按寵物類型、按配銷通路和預測,2024 年至2032 年