|

市場調查報告書

商品編碼

1687387

水泥板-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)Cement Board - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

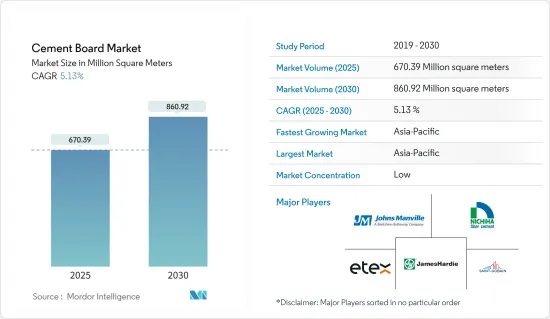

預計2025年水泥板市場規模為6.7039億平方公尺,至2030年將達到8.6092億平方公尺,預測期間(2025-2030年)的複合年成長率為5.13%。

主要亮點

- 預計其在住宅和商業建築中的應用日益廣泛,其抗衝擊性和耐用性等優良特性將在預測期內推動水泥板市場的發展。

- 然而,與傳統產品相比,較高的初始成本預計會阻礙市場成長。

- 然而,人們對美觀度的追求日益成長,預計將為市場創造新的機會。

- 預計亞太地區將主導市場,大部分需求來自中國和印度。

水泥板市場趨勢

在住宅和商業建築的應用日益增多

- 水泥板經常用於住宅建築,因為它們具有獨特的耐用性、耐火性、防潮性和成本效益的組合。

- 商業領域在水泥板市場中佔據重要地位,其中辦公領域佔據領先地位。隨著全球商業活動的激增,該領域對水泥板的需求也在增加。

- 亞太地區是辦公空間快速成長的中心,也是商業建築的頂級市場。在科技、電子商務和銀行等行業的推動下,印度和中國等國家對辦公空間的需求持續成長,導致新辦公大樓建設激增。

- 印度擁有蓬勃發展的新興企業生態系統,對辦公空間的需求不斷增加。政府舉措也起到了推動作用,工業和內部貿易促進部 (DPIIT) 預測,到 2023 年 12 月將成立 117,254 家新興企業。

- 美國也是建設產業的一個巨大的市場。根據美國人口普查局的資料,美國將在 2023 年花費超過 7,061 億美元用於新的私人住宅建築,較 2022 年的 5,965 億美元大幅增加。此外,2023 年的住宅建築成本估計僅為 8,649 億美元。

- 預計 2023 年將允許建造 1,469,800 套住宅,比 2022 年的 1,665,100 套下降 11.7%。此外,2023 年開工住宅數量預計為 1,413,100 套,比 2022 年的 1,552,600 套下降 9%(+2.5%)。

- 2024 年 7 月經季節性已調整的私人住宅開工年率為 1,396,000 套。這一數字比 6 月修訂後的 145.4 萬輛下降了 4%,比 2023 年 7 月的 151.1 萬輛下降了 7%。

- 德國強勁的經濟正在推動對商業空間的需求,特別是高品質、符合 ESG 標準的辦公大樓,優質租金的上漲就是明證。預計 2023 年第三季將有 246,000平方公尺的辦公空間竣工,到 2024 年將達到 180 萬平方公尺。零售空間開發,尤其是購物中心,在 2023 年也實現了持續成長。

- 在快速都市化的推動下,巴西的住宅產業正在吸引大量私人投資。為了滿足日益成長的需求,政府於 2023 年 2 月重新推出了「Minha Casa, Minha Vida」(家,我的生活)計劃,雄心勃勃的目標是到 2026 年建成 200 萬個新計畫。

- 沙烏地阿拉伯正在經歷建築熱潮,吉達中央計劃就是一個縮影。這個雄心勃勃的計劃由公共投資基金(PIF)的子公司吉達中央開發公司(JCDC)主導,耗資 200 億美元,將包括博物館、歌劇院和體育場等地標建築,以及 17,000 套住宅和 3,000 多家酒店。第一階段預計將於 2027 年完成,進一步的開發將持續到 2030 年及以後。

- 這些發展支撐了全球住宅和商業建築對水泥板的強勁需求,預計在預測期內這項需求也將成長。

亞太地區可望主導市場

- 亞太地區在全球水泥板市場佔據主導地位,其中中國是主導。水泥板在中國住宅和商業領域的各種建設活動中得到了廣泛的應用。

- 中國正大力都市化,目標是2030年實現70%的都市化。都市化推動了對更多生活空間的需求,反映了中階對更好生活條件的渴望。這些動態可能會促進住宅市場和住宅建設,對水泥板市場產生正面影響。

- 在中國香港,住宅委員會已推出多項措施來啟動經濟適用住宅建設。當局已設定目標,在 2030 年提供 301,000 套公共住宅。

- 中國政府雄心勃勃的建設計劃,包括到2025年將2.5億農村居民遷移到新興大城市的計劃,可能會促進水泥板市場的發展。

- 為因應經濟困境,中國各省將重大建設計劃預算增加了近20%。中國超過三分之二的地區正在實施重大計劃,包括交通基礎設施和工業園區,2024年總預算將超過12.2兆元(1.8兆美元)。

- 中國可支配收入的增加推動了對購物中心和酒店等高階商業空間的需求。中國處於購物中心發展的前沿,現有購物中心近 4,000 個,預計到 2025 年將新增 7,000 個。武漢復星外灘中心 T1 等計劃計畫於 2021 年第三季破土動工,2025 年第四季完工,將進一步加強市場發展。

- 印度經濟適用住宅預計增加70%。據投資印度 (Invest India) 稱,預計到 2025 年,建築業的估值將達到 1.4 兆美元。預計到 2030 年,超過 30% 的人口將成為居住者,因此迫切需要超過 2,500 萬套中型和經濟適用住宅。近期推出的《房地產法》、《商品及服務稅》和《房地產投資信託》等旨在加快核准速度和加強建設產業的改革正在推動市場成長。

- 韓國正在進行大規模工業建設工程。一個顯著的例子是 S-Oil Corp. 正在蔚山建設的雄心勃勃的沙欣煉油廠綜合石化工廠,目標是於 2026 年竣工。該工廠將配備世界上最大的石腦油蒸汽裂解裝置,年生產能力為 180 萬噸乙烯。

- 由於這些趨勢,預計預測期內亞太地區對水泥板的需求將大幅成長。

水泥板產業細分

水泥板市場部分分散。主要公司(排名不分先後)包括 James Hardie Industries PLC、Etex Group、Saint-Gobain、Johns Manville 和 NICHIHA。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 市場促進因素

- 在住宅和商業建築的應用日益增多

- 理想特性:抗衝擊性和耐用性

- 其他促進因素

- 市場限制

- 與傳統競爭對手相比初始成本更高

- 其他阻礙因素

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場區隔

- 依產品類型

- 纖維水泥板(FCB)

- 木絲水泥板(WWCB)

- 木絲水泥板(WSCB)

- 水泥塑合板(CBPB)

- 按應用

- 地板

- 外牆與隔牆

- 屋頂材料

- 柱和樑

- 建築幕牆、擋風板和覆層

- 隔音、隔熱材料

- 其他用途(預製住宅、永久性百葉窗、防火建築等)

- 按最終用戶產業

- 住宅

- 商業

- 工業/設施

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 馬來西亞

- 泰國

- 印尼

- 越南

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐國家

- 土耳其

- 俄羅斯

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 卡達

- 阿拉伯聯合大公國

- 奈及利亞

- 埃及

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章競爭格局

- 併購、合資、合作與協議

- 市場佔有率(%)**/排名分析

- 主要企業策略

- 公司簡介

- Etex Group

- Elementia Materials

- Everest Industries Limited

- James Hardie Industries PLC

- Johns Manville

- Knauf Gips KG

- Saint-Gobain

- BetonWood SRL

- Cembrit Holding A/S

- HIL Limited

- GAF

- NICHIHA Co. Ltd

第7章 市場機會與未來趨勢

- 追求美觀的趨勢日益成長

- 其他機會

簡介目錄

Product Code: 62218

The Cement Board Market size is estimated at 670.39 million square meters in 2025, and is expected to reach 860.92 million square meters by 2030, at a CAGR of 5.13% during the forecast period (2025-2030).

Key Highlights

- The increasing adoption in residential and commercial construction and desirable properties of impact resistance and durability are expected to drive the cement board market during the forecast period.

- However, the high initial cost compared to its traditional counterparts is expected to hinder market growth.

- Nevertheless, the rising trends for aesthetic improvement are expected to create new opportunities for the market.

- Asia-Pacific is expected to dominate the market, with the majority of demand coming from China and India.

Cement Board Market Trends

Increasing Adoption in Residential and Commercial Construction

- Cement boards offer a unique combination of durability, fire resistance, moisture resistance, and cost-effectiveness, making them a popular choice for residential construction.

- The commercial segment stands out as a pivotal player in the cement board market, with the office sector leading the way. As global commercial activities surge, so does the demand for cement boards in this segment.

- Asia-Pacific, a burgeoning hub for office spaces, ranks among the top markets in commercial construction. Countries like India and China have seen a consistent uptick in demand for office spaces, driven by sectors such as technology, e-commerce, and banking, leading to a flurry of new office constructions.

- India's burgeoning startup ecosystem highlights an increasing appetite for office spaces. Bolstered by government initiatives, the Department for Promotion of Industry and Internal Trade (DPIIT) recognized a remarkable 1,17,254 startups by December 2023.

- The United States is also a huge market for the building and construction industry. As per the data from the US Census Bureau, in 2023, the United States spent over USD 706.1 billion on new private non-residential buildings, a significant increase from USD 596.5 billion in 2022. Moreover, the residential construction in 2023 was only USD 864.9 billion.

- In 2023, an estimated 1,469,800 housing units were authorized by building permits, 11.7% below the 2022 figure of 1,665,100. Moreover, an estimated 1,413,100 housing units were started in 2023, 9% (+-2.5%) below the 2022 figure of 1,552,600.

- In July 2024, the seasonally adjusted annual rate for privately-owned housing units authorized by building permits stood at 1,396,000. This figure represents a 4% decline from the revised June rate of 1,454,000 and a 7% drop compared to the July 2023 rate of 1,501,000.

- Germany's robust economy is fueling a demand for commercial spaces, especially high-quality, ESG-compliant office buildings, which is evident from rising prime rents. In Q3 2023, 246,000 square meters of office space were completed, with projections reaching 1.8 million sq. m by 2024. Retail space development, particularly in shopping centers, also saw consistent growth in 2023.

- Brazil's residential sector is drawing substantial private investments fueled by swift urbanization. In response to this burgeoning demand, the government reintroduced the "Minha Casa, Minha Vida" (My Home, My Life) program in February 2023, setting an ambitious goal of 2 million new projects by 2026.

- Saudi Arabia is witnessing a construction boom, highlighted by the Jeddah Central megaproject. Spearheaded by the Jeddah Central Development Company (JCDC), a subsidiary of the Public Investment Fund (PIF), this ambitious USD 20 billion project includes landmarks like a museum, opera house, and sports stadium, alongside 17,000 residential units and over 3,000 hotels. The first phase is set for completion in 2027, with further developments extending to 2030 and beyond.

- These dynamics underscore a robust demand for cement boards in both residential and commercial construction globally, with promising growth during the forecast period.

Asia-Pacific Expected to Dominate the Market

- Asia-Pacific holds a dominant position in the global cement board market, led by China. Cement boards find extensive applications in China's diverse construction activities, spanning both residential and commercial sectors.

- China is actively pursuing urbanization, aiming for a 70% urban rate by 2030. This urbanization drives a demand for more living spaces and reflects the middle class's aspirations for better living conditions. Such dynamics are set to boost the housing market and residential construction, positively influencing the cement board market.

- In Hong Kong, China, housing authorities have initiated multiple measures to kickstart the construction of affordable housing. Officials have set a target to deliver 301,000 public housing units by 2030.

- With plans to relocate 250 million rural residents to new megacities by 2025, the Chinese government's ambitious construction initiatives are set to boost the cement board market.

- In response to a struggling economy, Chinese governors are ramping up budgets for major building projects by nearly 20%. Over two-thirds of China's regions have committed to significant projects, including transportation infrastructure and industrial zones, with a combined budget exceeding CNY 12.2 trillion (USD 1.8 trillion) for 2024.

- Rising disposable incomes in China are fueling the demand for upscale commercial spaces, including malls and hotels. China stands at the forefront of shopping center development, boasting nearly 4,000 existing centers and an estimated 7,000 more by 2025. Projects like the Wuhan Fosun Bund Center T1, with construction starting in Q3 2021 and completion slated for Q4 2025, further bolster the market.

- India is set to witness a 70% surge in the availability of affordable housing. According to Invest India, the construction sector is projected to attain a valuation of USD 1.4 trillion by 2025. With forecasts suggesting that over 30% of the population will be urban dwellers by 2030, there is a pressing need for 25 million more mid-end and affordable housing units. Recent reforms, such as the Real Estate Act, GST (goods and services tax), and REITs (real estate investment trusts), aim to expedite approvals and strengthen the construction industry, driving market growth.

- South Korea is undertaking significant industrial construction ventures. A notable example is S-Oil Corp.'s ambitious Shaheen refinery-integrated petrochemical plant in Ulsan, set to finish by 2026. This facility will house the world's largest naphtha-fed steam cracker, capable of producing 1.8 million mt/year of ethylene, underscoring the project's potential to elevate industrial demand and support market growth.

- Given these dynamics, the demand for cement boards in Asia-Pacific is poised for significant growth during the forecast period.

Cement Board Industry Segmentation

The cement board market is partially fragmented in nature. The major players (not in any particular order) include James Hardie Industries PLC, Etex Group, Saint-Gobain, Johns Manville, and NICHIHA Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Increasing Adoption in Residential and Commercial Construction

- 4.1.2 Desirable Properties of Impact Resistance and Durability

- 4.1.3 Other Drivers

- 4.2 Market Restraints

- 4.2.1 High Initial Cost in Comparison to Traditional Counterparts

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 By Product Type

- 5.1.1 Fiber Cement Board (FCB)

- 5.1.2 Wood Wool Cement Board (WWCB)

- 5.1.3 Wood Strand Cement Board (WSCB)

- 5.1.4 Cement Bonded Particle Board (CBPB)

- 5.2 By Application

- 5.2.1 Flooring

- 5.2.2 Exterior and Partition Walls

- 5.2.3 Roofing

- 5.2.4 Columns and Beams

- 5.2.5 Facades, Weatherboard, and Cladding

- 5.2.6 Acoustic and Thermal Insulation

- 5.2.7 Other Applications (Prefabricated Houses, Permanent Shuttering, Fire-resistant Construction, etc.)

- 5.3 By End-user Industry

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Industrial and Institutional

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Thailand

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 NORDIC Countries

- 5.4.3.7 Turkey

- 5.4.3.8 Russia

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 Qatar

- 5.4.5.3 United Arab Emirates

- 5.4.5.4 Nigeria

- 5.4.5.5 Egypt

- 5.4.5.6 South Africa

- 5.4.5.7 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/ Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Etex Group

- 6.4.2 Elementia Materials

- 6.4.3 Everest Industries Limited

- 6.4.4 James Hardie Industries PLC

- 6.4.5 Johns Manville

- 6.4.6 Knauf Gips KG

- 6.4.7 Saint-Gobain

- 6.4.8 BetonWood SRL

- 6.4.9 Cembrit Holding A/S

- 6.4.10 HIL Limited

- 6.4.11 GAF

- 6.4.12 NICHIHA Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Rising Trends for Aesthetic Improvement

- 7.2 Other Opportunities

02-2729-4219

+886-2-2729-4219

2025 年全球水泥板市場報告

2025 年全球水泥板市場報告 夯土市場機會、成長動力、產業趨勢分析與 2024 - 2032 年預測

夯土市場機會、成長動力、產業趨勢分析與 2024 - 2032 年預測 水泥板市場:按類型、應用、最終用戶、產品類型、厚度、製造程序、飾面類型 - 2025-2030 年全球預測纖維水泥板和板材市場 - 全球行業規模、佔有率、趨勢、機會和預測,按原料、應用、最終用戶、地區和競爭細分,2019-2029F

水泥板市場:按類型、應用、最終用戶、產品類型、厚度、製造程序、飾面類型 - 2025-2030 年全球預測纖維水泥板和板材市場 - 全球行業規模、佔有率、趨勢、機會和預測,按原料、應用、最終用戶、地區和競爭細分,2019-2029F 全球水泥板市場-2024年至2029年預測

全球水泥板市場-2024年至2029年預測 南美洲和中美洲水泥板市場預測至 2028 年 - 按產品類型、應用和最終用途進行區域分析

南美洲和中美洲水泥板市場預測至 2028 年 - 按產品類型、應用和最終用途進行區域分析 板岩市場:依產品類型、依用途、依最終用戶、依地區

板岩市場:依產品類型、依用途、依最終用戶、依地區 水泥面板的全球市場:2023年

水泥面板的全球市場:2023年 亞太地區水泥板市場預測至 2028 年 - 區域分析 - 按產品類型(纖維水泥板和水泥粘合塑合板)、應用(屋頂、外牆板或外牆等)和最終用途(住宅和非住宅)

亞太地區水泥板市場預測至 2028 年 - 區域分析 - 按產品類型(纖維水泥板和水泥粘合塑合板)、應用(屋頂、外牆板或外牆等)和最終用途(住宅和非住宅) 北美水泥板市場預測至 2028 年-區域分析-按產品類型(纖維水泥板和水泥粘合塑合板)、應用(屋頂、外牆板或外牆等)和最終用途(住宅和非住宅)

北美水泥板市場預測至 2028 年-區域分析-按產品類型(纖維水泥板和水泥粘合塑合板)、應用(屋頂、外牆板或外牆等)和最終用途(住宅和非住宅)

▼