|

市場調查報告書

商品編碼

1687401

模擬軟體:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)Simulation Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

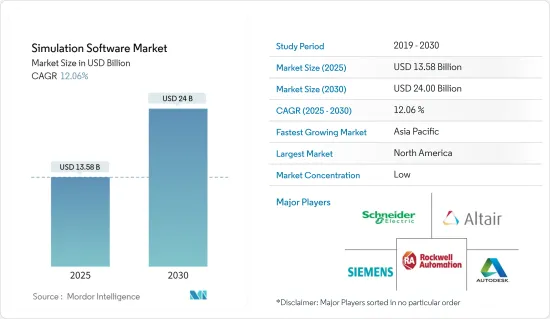

模擬軟體市場規模預計在 2025 年為 135.8 億美元,預計到 2030 年將達到 240 億美元,預測期內(2025-2030 年)的複合年成長率為 12.06%。

對於依賴先進設計、測試和建模環境的產業來說,模擬軟體至關重要。該技術廣泛應用於汽車、航太、國防、能源、通訊和教育等關鍵領域。該軟體使用戶能夠創建數位原型、模擬真實世界的應用程式並測試複雜系統,而無需進行物理實驗。這可以降低成本、提高效率並加快創新週期。

主要亮點

- 關鍵促進因素:汽車產業對成長的影響汽車產業是模擬軟體市場擴張的主要貢獻者。對電動車 (EV) 和自動駕駛技術的需求日益成長,需要先進的模擬工具來設計、測試和改進複雜的車輛系統。這些工具對於開發和最佳化動力傳動系統、電池系統和車載資訊娛樂技術至關重要。同樣,在航太和國防工業中,模擬軟體對於模擬高風險環境、提高飛機設計的安全性和性能以及增強國防系統和關鍵任務操作至關重要。在能源領域,模擬軟體擴大被應用於最佳化風能和太陽能等可再生能源系統,並減少可變性和不可預測性。

- 雲端基礎的模擬軟體:成長趨勢雲端基礎的模擬軟體市場正在經歷顯著成長。與傳統的內部部署解決方案相比,雲端平台具有擴充性、靈活性和成本優勢。雲端基礎的系統允許使用者透過網路存取強大的模擬工具,促進協作並減少前期投資的需要。這一趨勢與整個產業向數位轉型的轉變相吻合。雲端基礎的解決方案還支援人工智慧 (AI) 和機器學習 (ML) 的整合,以實現更有效率的模擬和工作流程最佳化。

汽車產業需求不斷成長

主要亮點

- 對電動車模擬的需求日益增加:電動車 (EV) 發展的激增推動了對先進模擬工具的需求。汽車製造商使用模擬軟體來設計和測試電動車組件,包括電池系統和充電基礎設施。透過模擬真實世界的性能,製造商可以在開發早期發現潛在問題,從而降低成本並縮短上市時間。

- 模擬自動駕駛技術:自動駕駛汽車需要在各種條件下進行大量測試,而這些條件在現實世界中很難複製。模擬軟體使自動駕駛系統能夠在多種道路和天氣條件下進行虛擬測試,以確保在複雜環境中安全運作。主要汽車製造商和科技公司正在採用這些工具來加速自動駕駛汽車的發展。

- 數位孿生增強汽車開發:數位雙胞胎(實體產品的虛擬複製品)擴大被用於汽車模擬,以模擬車載技術,從資訊娛樂系統到安全功能。利用數位雙胞胎,汽車製造商可以模擬不同條件下的性能,以改善使用者體驗和車輛安全性。

向雲端基礎的模擬解決方案的轉變仍在繼續

主要亮點

- 雲端平台的靈活性和擴充性:雲端基礎的模擬軟體由於其固有的靈活性和擴充性而越來越受歡迎。這些解決方案使各種規模的公司無需進行大量的基礎設施投資即可使用先進的模擬工具。該雲端平台支援全球協作,使工程師和設計師能夠即時存取和分析模擬資料。

- 對於中小企業來說具有成本效益:雲端基礎的模擬解決方案的訂閱模式可降低資本支出,並使中小企業也能使用先進的工具。這種可擴展性允許使用者根據計劃需求調整計算資源,從而提高成本效益。

- 整合人工智慧和機器學習:人工智慧驅動的模擬工作流程可以透過並行運行多個場景來確定最有效的配置,從而最佳化設計過程。此功能在製造業中尤其有用,即使效率稍微提高一點也可以節省大量成本。

模擬軟體市場趨勢

汽車產業成長可望加速

- 汽車領域的加速成長:虛擬原型製作、碰撞測試和系統操作的需求持續推動汽車產業對模擬軟體的依賴。這些工具可協助製造商無需建立實體原型即可提高車輛安全性和性能。此外,汽車零件製造商正在採用模擬技術來降低研發成本。

- 汽車性能監控中的數位雙胞胎:數位雙胞胎在汽車行業的整合使製造商能夠模擬即時車輛性能資料,有助於在維護問題變得嚴重之前發現它們。這種積極主動的方法提高了車輛的可靠性,同時有助於滿足監管排放氣體和安全標準。模擬工具對於開發和測試電動車電池至關重要,市場機會正在擴大。

- 即時模擬工具的興起:即時模擬軟體正成為汽車製造商的重要工具。工程師使用這些系統不斷測試車輛零件,以最佳化其在不同駕駛條件下的性能。例如,BMW等公司正在開發自動駕駛技術模擬中心,以加速電動和自動駕駛汽車的創新。

- 雲端平台推動市場效率:雲端基礎的模擬平台為汽車公司提供經濟高效且擴充性的解決方案。減少測試時間、增加協作和提高產品品質的能力正在推動中小企業採用該技術,進一步促進模擬軟體市場這一領域的成長。

北美引領類比模擬軟體市場

- 技術創新的市場領導地位:在強大的技術進步和強勁的研發投資的推動下,北美佔據全球模擬軟體市場的最大佔有率。航太、汽車和醫療保健領域處於模擬軟體採用的前沿。 Ansys、達梭系統和西門子等領先公司正在推動技術創新,幫助產業最佳化業務、降低成本並提高安全性。

- 政府措施推動市場成長永續性和效率的監管壓力正在刺激各行各業採用模擬軟體。例如,汽車製造商正在投資模擬工具以滿足符合政府綠色經濟目標的嚴格排放標準。在國防部門,政府資助的計劃使用模擬軟體進行任務規劃和系統開發。

- 北美醫療保健產業正在採用模擬工具。模擬軟體在醫療訓練、手術規劃和醫療設備開發的應用正在加速發展。這些應用的複雜性要求先進的模擬技術,進一步加速這些市場超越傳統工程學科的擴張。

- 透過雲端平台實現擴充性:雲端基礎的模擬軟體在北美的採用持續成長,從而大大節省了成本,並實現了從遠端位置進行即時模擬。擴充性可適應所有組織,包括小型、中型和大型企業,這有助於其在該地區的模擬軟體市場佔有率擴大,並鞏固其在全球行業領域的領導地位。

模擬軟體產業概況

分散的市場,全球參與者眾多模擬軟體市場高度分散,由跨國公司和利基解決方案供應商組成。雖然西門子股份公司、歐特克公司和羅克韋爾自動化公司等公司繼續佔據主導地位,但規模較小的公司也在為特定的工業應用貢獻創新。此類比賽推動了從汽車到學術研究等領域的進步。

推動創新的主要企業:西門子、羅克韋爾自動化、Schneider電氣、歐特克和 Ansys 等全球公司正在推動航太、汽車和製造等行業的技術邊界。各公司憑藉強大的研發和市場拓展能力,在滿足不斷變化的客戶需求的同時,推動全球模擬軟體市場的成長。

主要趨勢:雲端、人工智慧、數位雙胞胎:雲端基礎的解決方案、人工智慧數位雙胞胎的融合正在改變市場。採用這些技術的公司將會獲得成功。為了保持競爭力,企業,尤其是中小型企業,必須優先考慮軟體的易用性、跨平台功能和具有成本效益的解決方案。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 市場概況

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 購買者/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭強度

- COVID-19 市場影響

- 市場促進因素

- 汽車產業需求不斷成長

- 日益轉向雲端基礎的模擬解決方案

- 市場限制

第5章 市場區隔

- 部署類型

- 本地

- 雲

- 最終用戶產業

- 車

- 資訊科技/通訊

- 航太和國防

- 能源與採礦

- 教育與研究

- 電氣和電子

- 其他最終用戶產業

- 地區

- 北美洲

- 歐洲

- 亞洲

- 澳洲和紐西蘭

- 拉丁美洲

- 中東和非洲

第6章 競爭格局

- 供應商市場佔有率

- 公司簡介

- Altair Engineering Inc.

- The MathWorks Inc.

- Autodesk Inc.

- Cybernet Systems Corp.

- Bentley Systems Incorporated

- PTC Inc.

- CPFD Software LLC

- Design Simulation Technologies Inc.

- Synopsys Inc.

- Siemens AG

- Ansys Inc.

- Dassault Systeemes SE

- Simio LLC

- Lanner Group Ltd

- SIMUL8 Corporation

- CONSELF Srl

- SolidWorks Corporation

- Rockwell Automation Inc.

- The COMSOL Group

- Schneider Electric SE

第7章市場投資分析

第8章 市場機會與未來趨勢

The Simulation Software Market size is estimated at USD 13.58 billion in 2025, and is expected to reach USD 24.00 billion by 2030, at a CAGR of 12.06% during the forecast period (2025-2030).

Simulation software is integral to industries that depend on advanced design, testing, and modeling environments. This technology is widely utilized across key sectors such as automotive, aerospace, defense, energy, telecommunications, and education. The software enables users to create digital prototypes, simulate real-world applications, and test complex systems without the need for physical experimentation. This leads to cost reduction, increased efficiency, and faster innovation cycles.

Key Highlights

- Key Drivers: Automotive Industry's Impact on Growth The automotive sector is a significant contributor to the expansion of the simulation software market. The rising demand for electric vehicles (EVs) and autonomous driving technologies necessitates sophisticated simulation tools to design, test, and refine complex vehicle systems. These tools are essential for developing and optimizing powertrains, battery systems, and in-vehicle infotainment technologies. Similarly, in the aerospace and defense industries, simulation software is critical for modeling high-risk environments, improving safety and performance in aircraft design, and enhancing defense systems and mission-critical operations. In the energy sector, simulation software is increasingly adopted to optimize renewable energy systems such as wind and solar power, mitigating variability and unpredictability.

- Cloud-Based Simulation Software: A Growing Trend The market for cloud-based simulation software has experienced notable growth. Cloud platforms offer scalability, flexibility, and cost advantages over traditional on-premise solutions. With cloud-based systems, users can access powerful simulation tools over the internet, fostering collaboration and reducing the need for significant upfront infrastructure investments. This trend aligns with the broader industry shift toward digital transformation. Cloud-based solutions also support artificial intelligence (AI) and machine learning (ML) integration, enabling more efficient simulations and optimized workflows.

Rising Demand from the Automotive Sector

Key Highlights

- Increased Need for EV Simulation: The surge in electric vehicle (EV) development has amplified the need for advanced simulation tools. Automakers leverage simulation software to design and test EV components, such as battery systems and charging infrastructure. By simulating real-world performance, manufacturers can identify potential issues during the early stages of development, reducing costs and time-to-market.

- Simulation for Autonomous Driving Technologies: Autonomous vehicles require extensive testing under various conditions, which can be difficult to replicate in the real world. Simulation software allows for the virtual testing of autonomous driving systems across multiple road and weather conditions, ensuring their safe operation in complex environments. Major automakers and technology firms have embraced these tools to accelerate the development of autonomous vehicles.

- Digital Twins Enhance Vehicle Development: Digital twins-virtual replicas of physical products-are increasingly used in automotive simulation to model in-vehicle technologies, from infotainment systems to safety features. By using digital twins, automakers can simulate performance under diverse conditions, improving user experience and vehicle safety.

The Growing Shift to Cloud-Based Simulation Solutions

Key Highlights

- Flexibility and Scalability of Cloud Platforms: Cloud-based simulation software is gaining traction due to its inherent flexibility and scalability. These solutions allow companies of all sizes to access advanced simulation tools without heavy infrastructure investments. Cloud platforms support global collaboration, enabling engineers and designers to access and analyze simulation data in real-time.

- Cost-Effectiveness for SMEs: The subscription model of cloud-based simulation solutions reduces capital expenditure, making advanced tools accessible to small and medium enterprises (SMEs). This scalability allows users to adjust computational resources according to project needs, enhancing cost efficiency.

- AI and Machine Learning Integration: AI-driven simulation workflows can optimize design processes by running multiple scenarios in parallel, identifying the most efficient configurations. This capability is particularly valuable in manufacturing, where even minor gains in efficiency can result in significant cost savings.

Simulation Software Market Trends

Automotive Segment is Expected to Grow at a Faster Pace

- Automotive Segment Growth Accelerates:The automotive sector's reliance on simulation software continues to grow, driven by the need for virtual prototyping, crash testing, and system op mization. These tools help manufacturers improve vehicle safety and performance without the need for physical prototypes. Automotive suppliers are also adopting simulation technologies to reduce research and development (R&D) costs.

- Digital Twins in Automotive Performance Monitoring: The integration of digital twins in the automotive industry allows manufacturers to simulate real-time vehicle performance data, helping detect maintenance issues before they escalate. This proactive approach improves vehicle reliability while aligning with regulatory standards on emissions and safety. Simulation tools are vital in the development of EV batteries and testing, further expanding market opportunities.

- Real-Time Simulation Tools Gain Popularity: Real-time simulation software is becoming a pivotal tool for automotive manufacturers. Engineers use these systems to continuously test vehicle components, optimizing performance under various driving conditions. For instance, companies like BMW are developing simulation centers for autonomous driving technologies, helping accelerate the innovation of electric and autonomous vehicles.

- Cloud Platforms Enhance Market Efficiency: Cloud-based simulation platforms are providing cost-effective, scalable solutions for automotive companies. The ability to reduce testing times, enhance collaboration, and improve product quality is driving adoption among SMEs, further contributing to the sector's growth within the simulation software market.

North America Leads the Simulation Software Market

- Market Leadership in Technological Innovation: North America holds the largest share in the global simulation software market, underpinned by strong technological advancements and substantial R&D investments. The aerospace, automotive, and healthcare sectors are at the forefront of simulation software adoption. Major players, including Ansys, Dassault Systemes, and Siemens, are driving innovation, helping industries optimize operations, reduce costs, and improve safety.

- Government Initiatives Fuel Market Growth: Regulatory pressures regarding sustainability and efficiency are spurring the adoption of simulation software across industries. For example, automotive manufacturers are investing in simulation tools to meet stringent emissions standards, aligning with governmental green economy goals. In the defense sector, government-backed projects depend on simulation software for mission planning and system development.

- Healthcare Sector Embraces Simulation Tools: In North America, the healthcare sector is increasingly utilizing simulation software for medical training, surgical planning, and medical device development. The complexity of these applications demands sophisticated simulation technologies, further driving market expansion beyond traditional engineering fields.

- Scalability with Cloud Platforms: The adoption of cloud-based simulation software continues to grow in North America, providing significant cost savings and enabling remote, real-time simulations. The ability to scale across organizations, from SMEs to large enterprises, is broadening the market share of simulation software in the region, cementing its leadership in the global industry outlook.

Simulation Software Industry Overview

Fragmented Market with Global Players: The simulation software market is highly fragmented, with a mix of multinational corporations and niche solution providers. Companies like Siemens AG, Autodesk Inc., and Rockwell Automation Inc. maintain dominant positions, while smaller entities contribute to innovation in specific industry applications. This competition fosters diverse advancements across sectors ranging from automotive to academic research.

Leading Companies Drive Innovation: Global players such as Siemens, Rockwell Automation, Schneider Electric, Autodesk, and Ansys are pushing technological boundaries in industries like aerospace, automotive, and manufacturing. Their strong R&D capabilities and market reach enable them to meet evolving customer needs while driving global growth in the simulation software market.

Key Trends: Cloud, AI, and Digital Twins: The integration of cloud-based solutions, AI, and digital twins is transforming the market. Companies that embrace these technologies are poised for success. To remain competitive, firms must prioritize software usability, cross-platform functionality, and cost-effective solutions, particularly for SMEs.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Impact of the COVID-19 on the Market

- 4.4 Market Drivers

- 4.4.1 Rising Demand from the Automotive Sector

- 4.4.2 The Growing Shift to Cloud-Based Simulation Solutions

- 4.5 Market Restraints

5 MARKET SEGMENTATION

- 5.1 Deployment Type

- 5.1.1 On-premise

- 5.1.2 Cloud

- 5.2 End-user Industry

- 5.2.1 Automotive

- 5.2.2 IT and Telecommunication

- 5.2.3 Aerospace and Defense

- 5.2.4 Energy and Mining

- 5.2.5 Education and Research

- 5.2.6 Electrical and Electronics

- 5.2.7 Other End-user Industries

- 5.3 Geography

- 5.3.1 North America

- 5.3.2 Europe

- 5.3.3 Asia

- 5.3.4 Australia and New Zealand

- 5.3.5 Latin America

- 5.3.6 Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Altair Engineering Inc.

- 6.2.2 The MathWorks Inc.

- 6.2.3 Autodesk Inc.

- 6.2.4 Cybernet Systems Corp.

- 6.2.5 Bentley Systems Incorporated

- 6.2.6 PTC Inc.

- 6.2.7 CPFD Software LLC

- 6.2.8 Design Simulation Technologies Inc.

- 6.2.9 Synopsys Inc.

- 6.2.10 Siemens AG

- 6.2.11 Ansys Inc.

- 6.2.12 Dassault Systeemes SE

- 6.2.13 Simio LLC

- 6.2.14 Lanner Group Ltd

- 6.2.15 SIMUL8 Corporation

- 6.2.16 CONSELF Srl

- 6.2.17 SolidWorks Corporation

- 6.2.18 Rockwell Automation Inc.

- 6.2.19 The COMSOL Group

- 6.2.20 Schneider Electric SE

7 MARKET INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

2025-2029年全球模擬軟體市場

2025-2029年全球模擬軟體市場 2025年雲端基礎的模擬應用全球市場報告2025年模擬軟體全球市場報告

2025年雲端基礎的模擬應用全球市場報告2025年模擬軟體全球市場報告 電磁模擬軟體:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)

電磁模擬軟體:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030) 模擬軟體市場規模、佔有率、成長分析,按組件、按部署、按應用、按最終用戶、按地區 - 行業預測,2024-2031 年

模擬軟體市場規模、佔有率、成長分析,按組件、按部署、按應用、按最終用戶、按地區 - 行業預測,2024-2031 年 模擬軟體市場:按組件、按部署、按應用、按行業 - 2025-2030 年全球預測2024 年 3D模擬軟體全球市場報告2033 年模擬和分析軟體的全球市場、機會和策略

模擬軟體市場:按組件、按部署、按應用、按行業 - 2025-2030 年全球預測2024 年 3D模擬軟體全球市場報告2033 年模擬和分析軟體的全球市場、機會和策略 全球模擬軟體市場:按產品、軟體類型、部署模式、組織規模、應用、產業、地區分類 - 到 2030 年的預測

全球模擬軟體市場:按產品、軟體類型、部署模式、組織規模、應用、產業、地區分類 - 到 2030 年的預測 MBSE 解決方案和軟體/系統建模工具:2024

MBSE 解決方案和軟體/系統建模工具:2024