|

市場調查報告書

商品編碼

1687722

中國生物肥料市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)China Biofertilizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

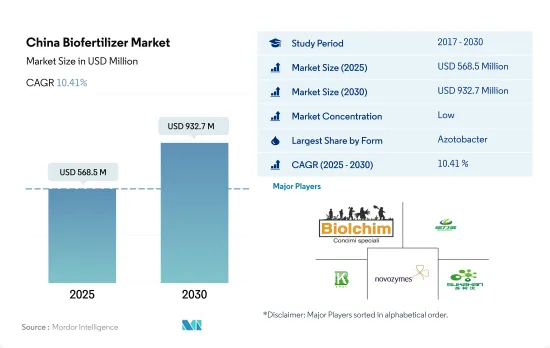

預計 2025 年中國生物肥料市場規模將達到 5.685 億美元,到 2030 年將達到 9.327 億美元,預測期內(2025-2030 年)的複合年成長率為 10.41%。

- 生物肥料是活的微生物,透過調動和增加土壤中養分的可用性來改善植物的營養狀況。生物肥料是有機農業的重要組成部分,透過固定大氣中的氮、調動固定的大量和微量營養素以及將土壤中的不溶性磷轉化為植物可利用的形式,在長期土壤肥力和永續性中發揮關鍵作用。

- 在中國生物肥料市場中,固氮菌是消耗量最大的生物肥料,佔據市場主導地位,佔有31.3%的佔有率,2022年的市場規模為1.371億美元,其次是菌根真菌、固氮螺菌、根瘤菌和解磷菌,佔有率分別為22%、22.0%、11.6%和11.2%。

- 截至2021年,中國已實現「連續18年糧食豐收」。然而,這項成就的取得卻面臨農業化肥長期過量使用等問題。中國農業化肥單位面積使用量已超過國際公認的上限。作為世界農業生產大國,中國於2015年提案了化肥減量增效舉措,到2020年實現「化肥零增量、化肥零減量」。中國在2015年至2020年期間已實現化肥減量12.8%,並將帶動2017年至2022年期間中國農業領域的生物肥料消費量增加7.0%。

- 隨著中國對有機食品的需求不斷成長,有機農業也呈現上升趨勢。從 2017 年到 2022 年,有機種植面積將增加 29.6%。在有機種植面積增加和政府措施的推動下,中國生物肥料市場的價值預計將在 2023 年至 2029 年間成長 78.8%。

中國生物肥料市場趨勢

農藥使用量降至零,有機產品出口增加,有機農業推廣。

- 根據FiBL和IFOAM的最新報告,中國有機食品市場正以每年25.0%的速度成長。鑑於中國每年出口29.1億美元的農產品,從傳統農業向有機農業的轉變意味著中國轉向更永續的食品體系的轉變。

- 隨著收入的提高和食品安全重要性的提高導致越來越多的人購買有機產品,中國的有機農場面積迅速成長。過去3年,中國有機種植面積增加了10%,2020年達到240萬公頃。此外,國家推出政策推動有機生產,提出「綠水青山是金山銀山」、「綠色發展」等口號。

- 中國的有機農業主要以出口為主。出口和進口商品包括穀物、大豆、水果和蔬菜。中國東北三省(遼寧、吉林、黑龍江)是全國有機農產品產量、產值、面積最大的省區。中國北方地區(如山東省、遼寧省)的大多數有機農場都向周邊城市供應有機蔬菜和水果。此外部分產品也出口到日本、韓國、歐美等美國。

- 由於過度使用合成肥料和殺蟲劑導致土壤污染,人們越來越擔心土壤毒性,中國對永續農業實踐和有機食品生產的需求日益成長。這種農業實踐的改變雖然緩慢但趨勢日益增強,並且對作物營養和保護產品的需求也日益增加。

隨著有機產品需求的不斷成長,約73%的中國消費者希望食用有機食品。

- 中國的有機食品市場發展迅速,中國消費者對有機食品的潛在需求龐大。更富裕的中階的崛起和對健康影響的認知不斷提高是這一現象背後的驅動力。 2021年,中國有機食品銷售額約達775.4億美元。

- 由於各種政府法律偏向有機食品而非食品安全,且消費者偏好有機食品而不是傳統食品,因此對有機食品的需求大幅增加。我國有機蔬菜價格一般是常規蔬菜的5至10倍,而有機蔬菜價格則是常規蔬菜的3至15倍。然而,儘管價格因素是一個障礙,富裕家庭和有健康問題的個人仍然願意擴大預算,約 73% 的中國消費者願意為有機食品支付額外費用。

- 中國政府正逐步實現有機食品領域的自力更生。例如,透過鼓勵農民減少化學肥料的使用、轉用生物替代品,經濟正逐步走向綠色農業。中國連鎖專利權協會2020年的調查顯示,中國發達城市中了解永續食品生產概念的人的有機認知度已達83%。儘管中國的有機食品產業仍相當小,遠遠無法滿足國內外消費者的需求,但考慮到2021年國內銷售額預計將成長4.01%,可以說中國有機食品在國內和海外市場都具有巨大的潛力。

中國生物肥料產業概況

中國生物肥料市場較為分散,前五大企業市佔率合計為3.08%。該市場的主要企業是:Biolchim SpA、Genliduo Bio-tech Corporation Ltd、Kiwa Bio-Tech、Novozymes 和山東蘇卡漢生物科技有限公司(按字母順序排列)。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章執行摘要和主要發現

第2章 報告要約

第 3 章 簡介

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 有機栽培面積

- 有機產品人均支出

- 法律規範

- 中國

- 價值鏈與通路分析

第5章 市場區隔

- 形式

- 固氮螺菌

- 固氮菌

- 菌根真菌

- 磷酸鹽溶解細菌

- 根瘤菌

- 其他生物肥料

- 作物類型

- 經濟作物

- 園藝作物

- 田間作物

第6章 競爭格局

- 重大策略舉措

- 市場佔有率分析

- 業務狀況

- 公司簡介.

- Atlantica Agricola

- Binzhou Jingyang Biological Fertilizer Co. Ltd

- Biolchim SpA

- Dora Agri-Tech

- Genliduo Bio-tech Corporation Ltd

- Kiwa Bio-Tech

- Novozymes

- Shandong Sukahan Bio-Technology Co. Ltd

- Sustane Natural Fertilizer Inc.

- Symborg Inc.

第7章:執行長的關鍵策略問題

第 8 章 附錄

- 世界概況

- 概述

- 五力分析框架

- 全球價值鏈分析

- 市場動態(DRO)

- 資訊來源和進一步閱讀

- 圖片列表

- 關鍵見解

- 資料包

- 詞彙表

簡介目錄

Product Code: 64594

The China Biofertilizer Market size is estimated at 568.5 million USD in 2025, and is expected to reach 932.7 million USD by 2030, growing at a CAGR of 10.41% during the forecast period (2025-2030).

- Biofertilizers are living microorganisms that improve plant nutrition by mobilizing or increasing nutrient availability in soils. Biofertilizers are essential components of organic farming that play an important role in long-term soil fertility and sustainability by fixing atmospheric nitrogen, mobilizing fixed macro and micronutrients, or converting insoluble phosphorous in the soil into forms available to plants.

- In the Chinese biofertilizer market, Azotobacter is the most consumed biofertilizer, dominating the market with a share of 31.3%, valued at USD 137.1 million, followed by Mycorrhiza, Azospirillum, Rhizobium, and phosphate-solubilizing bacteria with shares of 22%, 22.0%, 11.6%, and 11.2%, respectively, in 2022.

- As of 2021, China achieved its "eighteenth consecutive bumper grain harvest." However, this achievement was accomplished by problems such as the chronic overuse of agricultural fertilizers. China exceeds the internationally accepted upper limit of agricultural fertilizer per unit area. As a major global agricultural producer, China proposed a fertilizer reduction and efficiency initiative in 2015 to achieve "zero fertilizer growth rate and zero fertilizer use reduction" by 2020. China achieved a fertilizer reduction of 12.8% from 2015 to 2020. This initiative increased the consumption value of biofertilizers in the Chinese agricultural sector by 7.0% during 2017-2022.

- Organic farming is also increasing in China as the demand for organic food continues to rise. From 2017 to 2022, 29.6% of organic acreage increased. Increasing organic acreage and government initiatives are expected to boost the value of the Chinese biofertilizers market by 78.8% between 2023 and 2029.

China Biofertilizer Market Trends

Country's zero growth in pesticides use and increasing exports under organic products driving the organic cultivation.

- According to the latest reports by FiBL and the IFOAM, the market for organic food in China is growing at an annual rate of 25.0%. The shift from conventional to organic is a transformation toward a more sustainable food system within China, given the USD 2.91 billion of agri-food commodities exported from China each year.

- The size of organic farmland increased rapidly in China because more people started buying organic products due to increased incomes and the increasing importance of food safety. In the last three years, China's organic planting area increased by 10%, reaching 2.4 million ha in 2020. In addition, national policies have been adopted to promote organic production, advocating the slogans that state, "lucid waters and lush mountains are invaluable assets" and "green development".

- Organic farming in China is majorly export-oriented. The products that are both exported and imported include cereals, soybeans, fruits, and vegetables. China's three northeastern provinces (Liaoning, Jilin, and Heilongjiang) support the largest organic production nationally in terms of output, volume, and area. Most organic farms located in the northern part of China (e.g., Shandong and Liaoning) supply organic vegetables and fruits to nearby cities. In addition, they export some products to Japan, South Korea, Europe, and the United States.

- With the increasing concerns of soil toxicity due to the overuse of synthetic fertilizers and pesticides that lead to soil contamination, the demand for sustainable agriculture practices and organic food production is on the rise in China. This moderately slow yet increasing shift in cultivation practices has also subsequently increased the demand for crop nutrition and protection products.

The growing demand for organic products, approximately 73% of Chinese consumers are willing to have organic food

- China's organic food market is developing rapidly, and the potential demand for organic food among Chinese consumers is enormous. This is due to the growth of the wealthier middle classes and a greater awareness of the health implications. In 2021, organic food sales in China amounted to about USD 77.54 billion.

- Due to various government laws that favor organic food over food safety and customer preferences for organic food over conventional food, the demand for organic food items has considerably expanded. While prices of organic vegetables in China range from 3 to 15 times the cost of conventional produce, prices for organic vegetables are generally between 5 and 10 times that of their conventional counterparts. However, despite the price factor being a barrier, wealthy families and individuals with health problems are eager to increase their budget, with approximately 73% of Chinese consumers willing to pay extra for organic foods.

- The Chinese government is slowly aiming to become self-reliant in the organic food sector. For instance, the economy is slowly moving toward a green agriculture practice by encouraging farmers to scale back the use of chemical fertilizers and switch to bio-based alternatives. The China Chain Store and Franchise Association (CCFA) research in 2020 declared that organic awareness among the Chinese population in developed cities was at 83% when it came to an understanding of the concept of sustainable food production. Although China's organic food sector is still quite small and falls far short of satisfying domestic and international consumer demand, it can be stated that organic food in China has enormous potential in both the domestic and foreign markets, considering the rise in domestic sales by 4.01% in 2021.

China Biofertilizer Industry Overview

The China Biofertilizer Market is fragmented, with the top five companies occupying 3.08%. The major players in this market are Biolchim SpA, Genliduo Bio-tech Corporation Ltd, Kiwa Bio-Tech, Novozymes and Shandong Sukahan Bio-Technology Co. Ltd (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Organic Cultivation

- 4.2 Per Capita Spending On Organic Products

- 4.3 Regulatory Framework

- 4.3.1 China

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Form

- 5.1.1 Azospirillum

- 5.1.2 Azotobacter

- 5.1.3 Mycorrhiza

- 5.1.4 Phosphate Solubilizing Bacteria

- 5.1.5 Rhizobium

- 5.1.6 Other Biofertilizers

- 5.2 Crop Type

- 5.2.1 Cash Crops

- 5.2.2 Horticultural Crops

- 5.2.3 Row Crops

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Atlantica Agricola

- 6.4.2 Binzhou Jingyang Biological Fertilizer Co. Ltd

- 6.4.3 Biolchim SpA

- 6.4.4 Dora Agri-Tech

- 6.4.5 Genliduo Bio-tech Corporation Ltd

- 6.4.6 Kiwa Bio-Tech

- 6.4.7 Novozymes

- 6.4.8 Shandong Sukahan Bio-Technology Co. Ltd

- 6.4.9 Sustane Natural Fertilizer Inc.

- 6.4.10 Symborg Inc.

7 KEY STRATEGIC QUESTIONS FOR AGRICULTURAL BIOLOGICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

生物肥料市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、形態、作物類型、應用、微生物類型、地區和競爭格局分類,2020-2030年預測

生物肥料市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、形態、作物類型、應用、微生物類型、地區和競爭格局分類,2020-2030年預測 基於固氮菌的生物肥料市場—按產品類型、作物類型、應用方法、分銷管道、最終用戶和配方類型分類—2025-2032年全球預測生物肥料市場按類型、形態、應用方法、作物類型和分銷管道分類-2025-2032年全球預測

基於固氮菌的生物肥料市場—按產品類型、作物類型、應用方法、分銷管道、最終用戶和配方類型分類—2025-2032年全球預測生物肥料市場按類型、形態、應用方法、作物類型和分銷管道分類-2025-2032年全球預測 2032年生物肥料市場預測:按產品類型、微生物、作物類型、形態、應用和地區進行的全球分析

2032年生物肥料市場預測:按產品類型、微生物、作物類型、形態、應用和地區進行的全球分析 2025年全球生物肥料市場報告

2025年全球生物肥料市場報告 生物肥料市場機會、成長動力、產業趨勢分析及2025-2034年預測固氮菌生物肥料市場機會、成長動力、產業趨勢分析及2025-2034年預測全球固氮菌生物肥料市場2025年全球根瘤菌肥料市場報告

生物肥料市場機會、成長動力、產業趨勢分析及2025-2034年預測固氮菌生物肥料市場機會、成長動力、產業趨勢分析及2025-2034年預測全球固氮菌生物肥料市場2025年全球根瘤菌肥料市場報告 日本生物肥料市場報告(按類型、作物、微生物、應用方式和地區)2025-2033

日本生物肥料市場報告(按類型、作物、微生物、應用方式和地區)2025-2033

▼