|

市場調查報告書

商品編碼

1687783

北美暖通空調設備:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)North America HVAC Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

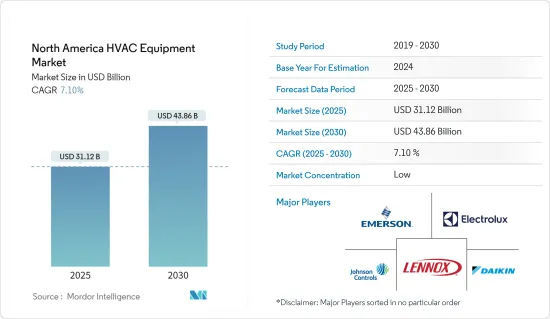

北美 HVAC 設備市場規模預計在 2025 年為 311.2 億美元,預計到 2030 年將達到 438.6 億美元,預測期內(2025-2030 年)的複合年成長率為 7.1%。

可支配收入的增加、建設活動的快速擴張以及天氣模式的變化正在推動所研究市場的成長。北美智慧家庭和智慧城市項目的採用正在顯著增加,推動了市場的成長。

主要亮點

- 政府以增加預算撥款的形式加大對永續社區發展的支持,可能會促進商業和工業建築業的持續成長。此外,建設活動的增加、快速的都市化和基礎設施改革導致暖通空調機組更換量激增,推動了暖通空調設備市場的發展。

- 北美 HVAC 設備市場的成長受到對智慧系統不斷成長的需求以及物聯網 (IoT)、工業自動化系統、智慧製造和工業 4.0 的整合的推動。預計市場高於平均水準的成長很大一部分將來自於綠色建設活動的活性化。快速擴張的智慧家庭市場預計將推動 HVAC 系統市場的成長。

- 綠色建築施工計劃將進一步推動該地區暖通空調設備市場的擴張。例如,2022年2月,加拿大綠建築委員會(CAGBC)宣布,該國在其2021年LEED(能源與環境設計先鋒)十大國家和地區年度榜單中名列世界第二,LEED是全球使用的綠色建築認證計劃。由於居住者和能源消耗的認知不斷提高,安裝符合政府機構標準的空調設備正成為綠色建築設計的重要標準。

- 然而,根據國際能源總署和美國能源局的數據,大約 25-35% 的電力消耗來自 HVAC 系統。根據同一來源,這部分能源消耗的很大一部分(20%至60%)是由寄生能源使用造成的(用於為加熱和冷卻運輸中使用的風扇和泵提供動力來源的能源)。因此,儘管集中式空調系統比模組化系統更有效率(就單位面積空調空間的消費量而言),但它們仍然會增加能源費用。

- 製造業崗位全面短缺。可悲的是, 冷暖氣空調產業也不例外。無論當前的勞動力短缺是否是由於這些因素造成的,它都可能成為阻礙市場成長的因素。

北美暖通空調設備市場趨勢

熱泵正在快速成長

- 預計熱泵將佔據很大的市場佔有率。由於氣候條件、設備便利性、政府稅額扣抵和法規等多種因素,北美熱泵的使用正在穩步增加。

- 由於人們轉向採用節能產品和增加消費者支出的模式轉移,美國住宅熱泵市場預計將繼續保持健康成長。走向脫碳經濟的進程將刺激商業環境,並透過立法能源政策和獎勵提供支持。隨著老化建築的維修,對靈活性和舒適度的需求可能會成長。這可能會使該行業更加充滿活力。

- 熱泵分為水源、空氣源、地源等類型。空氣源熱泵(ASHP)吸收電能並從周圍空氣中提取熱量,產生高達 90 攝氏度的熱水。它從周圍的空氣中提取熱量,使其變得更冷。因此,對熱水和冷空氣的需求正在推動空氣源熱泵的成長。

- 此外,寒冷氣候熱泵在北美許多地區越來越受歡迎,這推動了該領域的重大創新。寒冷氣候熱泵已被開發為在低至 -25°C 的條件下有效運行,有些系統在 -18°C 的條件下仍能保持 200% 以上的效率。

- 2022年6月,美國(DOE)宣布,Lennox International成為美國能源局(DOE)住宅寒冷地區熱泵技術的首個合作夥伴。

美國佔有較大的市場佔有率

- 美國是重要的設備市場之一,一直呈現穩定的成長率。建設活動的活性化、高效系統的可用性以及極端天氣條件有利於整個設施的系統安裝。此外,開利、艾默生電氣等主要製造商的存在也為北美市場的未來成長提供了助力。

- 此外,隨著物聯網 (IoT) 的整合,一些製造商已經開始提供智慧暖氣、空調和通風系統,幫助推動整個美國的市場成長。

- 為了確保永續的未來,美國能源局(DOE) 正在大力投資提高全國的能源效率標準。美國能源部希望透過尋找應對環境、能源和核能挑戰的科學技術解決方案來確保美國的安全和繁榮。

- 此外,根據美國能源資訊署 (EIA) 的住宅能源消耗調查 (RECS),估計美國居住7,600 萬戶住宅(佔總數的 64%)使用中央空調。約有 1,300 萬戶家庭(11%)使用熱泵進行暖氣和冷氣。到2023年,在美國銷售的所有新住宅空調和空氣源熱泵系統都必須符合現代能源效率標準,從而刺激暖通空調設備的成長。

- 此外,根據美國人口普查局的數據,2022年6月美國住宅數約為136萬套。 2022年6月,美國新建私人住宅數量約155萬套。預計在預測期內,這將進一步在該國產生對熱泵的大量新需求。

北美暖通空調設備產業概況

北美暖通空調設備市場競爭激烈,大金、開利、倫諾克斯等知名供應商在各自的領域佔據主要市場佔有率,並擁有完善的分銷網路。由於 HVAC 設備行業是最大的市場之一,因此如此眾多的主要供應商的存在是永續的,而不會影響市場佔有率。然而,供應商之間展開了激烈的競爭,以搶佔更大的市場佔有率,特別是在供暖和製冷領域。

- 2023 年 2 月 - Lennox 推出 Enlight 和 Xion 產品線,增強了其全面的屋頂機組系列。該公司的 Enlight 產品系列旨在最大限度地減少對環境的影響並最大限度地提高效率。

- 2022 年 10 月-開利公司宣佈在北美擴大其 AquaEdge19DV 水冷渦輪冷凍的產能。 AquaEdge19DV 的容量高達 1,150 噸,可滿足更大的容量需求,例如商業高層建築和混合用途建築、大型製造設施和醫療保健設施。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭強度

- 評估宏觀經濟趨勢對市場的影響

第5章 市場動態

- 市場促進因素

- 住宅和非住宅用戶增加

- 市場限制

- 暖通空調設備消費量高

第6章 市場細分

- 按設備

- 空調設備

- 加熱設備

- 熱泵

- 除濕機和加濕器

- 按最終用戶

- 住宅

- 產業

- 商業的

- 按國家

- 美國

- 加拿大

第7章 競爭格局

- 公司簡介

- Johnson Controls International PLC

- Daikin Industries Ltd

- Lennox International Inc.

- Electrolux AB

- Emerson Electric Co.

- Carrier Corporation

- Rheem Manufacturing Company Inc.

- Uponor Corp.

- Ingersoll Rand Inc.(Trane Inc.)

- Nortek Global HVAC, LLC

第8章投資分析

第9章:市場的未來

The North America HVAC Equipment Market size is estimated at USD 31.12 billion in 2025, and is expected to reach USD 43.86 billion by 2030, at a CAGR of 7.1% during the forecast period (2025-2030).

Increasing disposable income, rapidly expanding construction activity, and changing weather patterns are driving the growth of the market studied. North America is witnessing a significant increase in the implementation of smart home and smart city programs, driving the market's growth.

Key Highlights

- Growing government support, in the form of higher budget allocations designed to increase sustainable community development, may contribute to the continually growing commercial and industrial construction sectors. Besides, increased construction activities, rapid urbanization, and infrastructural reforms result in an upsurge in HVAC unit replacements, thus driving the HVAC equipment market.

- The growth of the North American HVAC equipment market is driven by an increase in demand for smart systems and the integration of the Internet of Things (IoT), industrial automation systems, smart manufacturing, and industry 4.0. A significant portion of the market's above-average growth is anticipated from the uptick in green building construction activities. The smart home market, which is expanding rapidly, is projected to boost the HVAC system market's growth.

- Green building construction projects further support the empowerment of the HVAC equipment market in the region. For instance, in February 2022, Canada Green Building Council (CAGBC) announced that the country ranked second globally on the annual list of Top 10 Countries and Regions for LEED (Leadership in Energy and Environmental Design), a green building certification program used worldwide, in 2021. Installation of HVAC equipment with standards imposed by the governmental bodies for the rising awareness of occupants' health and energy consumption is becoming a vital criteria in green building designs.

- However, as per IEA and the U.S. Department of Energy, around 25-35% of electricity consumption is due to HVAC systems. According to the same source, a large part (20% - 60%) of this energy consumption is contributed by parasitic energy use (energy used to power fans and pumps used for the transfer of heating and cooling). Thus, centralized HVAC systems have burdened energy bills despite being more efficient (in terms of energy units' consumption per unit area of space conditioned) than unitary systems.

- There is a lack of employment in the whole manufacturing sector. Sadly, there is no exception in the heating and air conditioning industry Whether or not current workforce shortages are caused by these, they will likely be exacerbated might hamper the market gorwth

North America HVAC Equipment Market Trends

Heat Pumps to Witness Significant Growth

- The market share that heat pumps are predicted to command is significant. Due to various factors, including climatic conditions, the convenience provided by the equipment, government tax credit benefits, regulations, etc., the use of heat pumps has steadily increased in the North American region.

- Owing to a paradigm shift toward adopting energy-efficient products and rising consumer spending, the residential heat pump market in the United States would continue to expand steadily. The business environment will be stimulated by the ongoing progress toward a decarbonized economy, which will be supported by legislative energy policies and incentives. As the number of old buildings that are being fixed up goes up, there will be more demand for flexibility and better comfort. This will make the industry more dynamic.

- The heat pumps are been categorized based on types, such as water source, air source, and ground source. The air-source heat pump (ASHP) takes in electricity, extracts heat from the surrounding air, and produces hot water up to 90 degrees Celsius. Due to the extraction of heat from the ambient air, it gets cooler. Thus, the requirement for both hot water and cold air is driving the growth of air-source heat pumps.

- Moreover, Cold climate heat pumps are becoming increasingly popular in many regions across North America, and this has been driving significant innovation in the space. Cold climate heat pumps are developed to work efficiently in conditions down to -25 degrees Celsius, with some systems maintaining an efficiency of over 200% at -18 degrees Celsius.

- In June 2022, the U.S (DOE) announced that Lennox International had became the first partner in the U.S. Department of Energy's (DOE's) Residential Cold Climate Heat Pump Technology has Challenge to develop an next-generation electric heat pump which woyuld that can more effectively heat homes in northern climates relative to current models.

United States Holds Major Market Share

- The United States is one of the essential equipment markets, witnessing a steady growth rate. The growing construction activity, availability of high-efficiency systems, and extreme climatic conditions favour system installation across the facilities. Additionally, the presence of leading manufacturers, such as Carriers, Emerson Electric Co., and others, is complementing the growth of the North American market in the future.

- Additionally, with the Internet of Things (IoT) integration, several manufacturers have initiated smart heating, air conditioning, and ventilation system offers that, in turn, are propelling market growth across the United States.

- To ensure a sustainable future, the U.S. Department of Energy (DOE) is heavily investing in improving energy efficiency standards throughout the country. The DOE wants to make sure that America is safe and doing well by finding science and technology solutions to its environmental, energy, and nuclear problems.

- Moreover, the Energy Information Administration's (EIA) Residential Energy Consumption Survey (RECS) estimates that 76 million primarily occupied US homes (64% of the total) use central air-conditioning equipment. About 13 million households (11%) use heat pumps for heating or cooling. By 2023, all new residential air-conditioning and air-source heat pump systems sold in the United States will require meeting the latest energy efficiency standards, fueling the growth of HVAC equipment.

- Furthermore, according to the US Census Bureau, new home construction in the United States in June 2022 was around 1.36 million. There were approximately 1.55 million new privately owned housing units in the United States in June 2022. This is further expected to create significant new demand for heat pumps in the country over the forecast period.

North America HVAC Equipment Industry Overview

The competitive rivalry in the North American HVAC equipment market is high, as the market studied is home to prominent vendors like Daikin, Carrier, and Lennox that command a major market share in different segments and have access to well-established distribution networks. Owing to the HVAC equipment industry being one of the largest markets, the existence of such a high number of major vendors without compromising on their market shares is sustainable. However, each vendor, especially in the heating and cooling segments, is fiercely competing to gain a larger share of the market studied.

- February 2023 - Lennox enhanced its comprehensive selection of With the introduction of the Enlight and Xion product lines, packaged rooftop units have been introduced. The company's Enlight product family aims to minimize environmental impact and maximize efficiency.

- October 2022 - Carrier Corporation declared that it had increased In North America, the AquaEdge 19DV watercooled Centrifugal chiller offers a range of capacities. The AquaEdge19DV is capable of supplying the customer with up to 1150 tonnes in order to meet their demand for larger capacities, as regards Commercial Highrise and mixed Use Building Applications, Large Manufacturing Establishments or Health Institutions.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Defnition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 An Assessment of Impact of Macro Economic Trends on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rise in Residential and Non-residential Users

- 5.2 Market Restraints

- 5.2.1 High Energy Consumption of HVAC Equipment

6 MARKET SEGMENTATION

- 6.1 By Equipment

- 6.1.1 Air Conditioning Equipment

- 6.1.2 Heating Equipment

- 6.1.3 Heat Pumps

- 6.1.4 Dehumidifiers and Humidifiers

- 6.2 By End User

- 6.2.1 Residential

- 6.2.2 Industrial

- 6.2.3 Commercial

- 6.3 By Country

- 6.3.1 United States

- 6.3.2 Canada

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Johnson Controls International PLC

- 7.1.2 Daikin Industries Ltd

- 7.1.3 Lennox International Inc.

- 7.1.4 Electrolux AB

- 7.1.5 Emerson Electric Co.

- 7.1.6 Carrier Corporation

- 7.1.7 Rheem Manufacturing Company Inc.

- 7.1.8 Uponor Corp.

- 7.1.9 Ingersoll Rand Inc. (Trane Inc.)

- 7.1.10 Nortek Global HVAC, LLC

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

2025 年至 2033 年 HVAC 設備市場報告,按類型(暖氣、空調、通風等)、系統類型(中央、分散)、最終用戶(住宅、商業、工業)和地區分類

2025 年至 2033 年 HVAC 設備市場報告,按類型(暖氣、空調、通風等)、系統類型(中央、分散)、最終用戶(住宅、商業、工業)和地區分類 全球暖通空調設備市場研究報告 - 產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年

全球暖通空調設備市場研究報告 - 產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年 HVAC 設備市場:按類型、設備類型、最終用戶分類 - 2025-2030 年全球預測

HVAC 設備市場:按類型、設備類型、最終用戶分類 - 2025-2030 年全球預測 HVAC 設備市場規模、佔有率和成長分析:按冷卻設備自控、按實施類型、按服務類型、按應用、按地區 - 行業預測,2024-2031 年

HVAC 設備市場規模、佔有率和成長分析:按冷卻設備自控、按實施類型、按服務類型、按應用、按地區 - 行業預測,2024-2031 年 HVAC 設備市場 – 2024 年至 2029 年預測

HVAC 設備市場 – 2024 年至 2029 年預測 全球攜帶式 HVAC 設備市場 2024-2031

全球攜帶式 HVAC 設備市場 2024-2031 2024-2028年全球暖通空調設備市場

2024-2028年全球暖通空調設備市場 全球暖通空調設備市場研究報告 - 2024 年至 2032 年產業分析、規模、佔有率、成長、趨勢與預測

全球暖通空調設備市場研究報告 - 2024 年至 2032 年產業分析、規模、佔有率、成長、趨勢與預測 全球暖通空調設備產業的成長機會

全球暖通空調設備產業的成長機會 2024-2032 年按類型(暖氣、空調、通風等)、系統類型(集中式、分散式)、最終用戶(住宅、商業、工業)和地區分類的 HVAC 設備市場報告

2024-2032 年按類型(暖氣、空調、通風等)、系統類型(集中式、分散式)、最終用戶(住宅、商業、工業)和地區分類的 HVAC 設備市場報告