|

市場調查報告書

商品編碼

1689931

聚乙烯丁醛(PVB):市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Polyvinyl Butyral (PVB) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

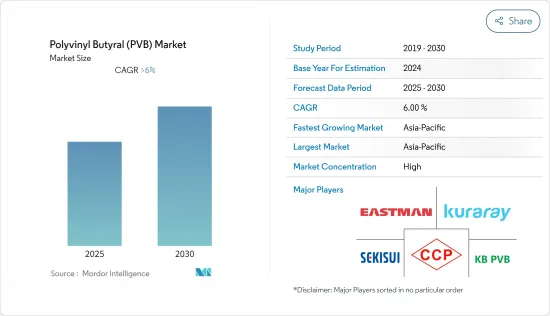

預計預測期內聚乙烯丁醛(PVB) 市場複合年成長率將超過 6%。

市場受到了 COVID-19 的負面影響。鑑於疫情情勢,汽車製造廠暫時關閉以防止感染蔓延,限制了用於生產安全、抗衝擊的汽車擋風玻璃的 PVB 材料的需求。然而,自 2021 年以來,該行業已恢復發展勢頭,預計市場在預測期內將遵循類似的軌跡。

主要亮點

- 短期內,全球夾層玻璃使用量的增加以及建築和基礎設施活動的活性化可能會推動市場成長。

- 然而,市場上替代品的存在預計會阻礙市場成長。此外,新興經濟體中大量的聚乙烯丁醛回收可能會損害市場,因為它會帶來環境問題。

- 由於太陽能產業的需求不斷成長以及購買電動車的人數不斷增加,預計未來幾年市場將會成長。

- 預計亞太地區將引領這一趨勢,在預測期內實現最高的複合年成長率。

聚乙烯丁醛(PVB) 市場趨勢

汽車領域佔據市場主導地位

- 聚乙烯丁醛是一種機械性質優異的聚合物,常用作夾層玻璃的中間層材料。 PVB 片材附著在兩層玻璃上,即使受到撞擊也不會破裂。 PVB 片材和玻璃之間的黏合是化學黏合,因此不會輕易剝落。

- PVB 主要用於汽車擋風玻璃的夾層安全玻璃。由於 PVB 能為汽車擋風玻璃提供安全保障,因此作為夾層玻璃中間層的材料需求正在迅速增加。此外,隔音、防紫外線也是PVB的重要優點,增加了PVB在汽車產業的應用。

- 國際汽車製造商協會(OICA)預測,2021年全球汽車產量將達到8,000萬輛,比2020年的7,800萬輛成長約3%。

- 知名汽車公司豐田汽車2022年11月的汽車銷售量和產量與前一年同期比較成長了約4%。豐田2022年1-11月汽車總銷量約950萬輛,產量約970萬輛。雖然銷售量與上年基本持平,但產量與前一年同期比較增加了約7%。

- 歐洲汽車工業協會在最新報告中稱,美國總合194家汽車製造廠。此外,預計2021年歐洲汽車產量將達總合萬輛左右。

- ACEA 也觀察到,2022 年 12 月的乘用車註冊量與 2021 年 12 月相比環比成長了約 13%。註冊量成長率最高的是德國(+38%),其次是義大利(+21.0%)。隨著乘用車註冊量的增加,產業的生產需求也在增加,這對PVB市場產生了重大影響。

- 受以上因素影響,未來聚乙烯丁醛市場可望保持強勁。

亞太地區佔市場主導地位

- 亞太地區有望成為全球最大的市場,因為中國、印度、日本和新加坡正在建造更多的建築物、銷售和製造更多的汽車,而且該地區正在進行投資以幫助生產太陽能。

- 根據中國工業協會預測,2022年中國汽車產量預計將年增與前一年同期比較%左右。 2014年美國汽車銷量約2,686萬輛。中國預計2022與前一年同期比較的汽車產量也將年增2.1%左右。 2021年汽車銷量為2627萬輛,而2022年銷量約2686萬輛。

- 根據印度品牌股權基金會預測,到2026年,印度汽車產業規模將達到3,000億美元左右。此外,2022會計年度國內乘用車銷量達約300萬輛。

- 2000年4月至2022年6月期間,汽車產業累計獲得直接股權投資約335.3億美元。印度政府預計到2023年印度和其他國家將向汽車業額外投資80億至100億美元。

- 隨著該展會在日本舉辦,日本的建設產業也有望蓬勃發展。例如,大阪將於2025年舉辦世博會。建設將主要由重建和自然災害後的恢復所推動。東京車站有兩棟高層建築:一棟 37 層樓、230 公尺高的辦公大樓,原計劃於 2021 年竣工;一棟 61 層樓、390 公尺高的辦公大樓,計劃於 2027 年竣工。

- 據日本國土交通省稱,2022年建築業總投資預計約為66.99兆日圓(5,081.6億美元),與前一年同期比較成長0.6%。

- 由於汽車、建築和其他行業的投資不斷增加,聚乙烯丁醛(PVB) 的需求預計會增加,這將為這些行業提供服務。這對未來幾年的市場來說似乎是件好事。

聚乙烯丁醛(PVB) 產業概覽

聚乙烯丁醛(PVB) 市場部分合併,少數大公司控制很大一部分市場。市場的主要企業包括(不分先後順序):伊士曼化學公司、可樂麗、積水化學、建滔(佛岡)特種樹脂(KB PVB)、長春集團等。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 驅動程式

- 不斷擴大的全球建築和基礎設施活動

- 擴大夾層玻璃的應用範圍

- 限制因素

- 市場上存在替代品

- 新興經濟體聚乙烯丁醛回收率高

- 價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場區隔

- 類型

- 黏合膜

- 油漆和塗料(包括耐洗底漆)

- 印刷油墨和清漆

- 其他類型(陶瓷黏合劑、複合纖維黏合劑)

- 最終用戶產業

- 車

- 建造

- 發電

- 其他終端用戶產業(航太和國防)

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭格局

- 併購、合資、合作、協議

- 市場排名分析

- 主要企業策略

- 公司簡介

- Chang Chun Group

- Everlam

- Genau Manufacturing Company LLP

- Huakai plastic(Chongqing)Co., Ltd.

- Kingboard FoGang Specialty Resins Co. Ltd

- KURARAY CO. LTD

- Eastman Chemical Company

- Sekisui Chemical Co. Ltd.

- WMC GLASS

第7章 市場機會與未來趨勢

- 太陽能發電產業的需求不斷成長

- 擴大電動車的使用

The Polyvinyl Butyral Market is expected to register a CAGR of greater than 6% during the forecast period.

The market was negatively impacted by COVID-19. Given the pandemic situation, car manufacturing plants were temporarily halted to prevent the spread, limiting demand for PVB materials used to manufacture safe, impact-resistant automotive windscreens. However, the industry has picked up speed since 2021, and the market is expected to follow a similar trajectory throughout the projection period as well.

Key Highlights

- Over the short term, the growing number of laminated glass applications and the ever-increasing construction and infrastructure activities across the world are likely to boost market growth.

- On the flip side, the availability of product substitutes in the market is expected to hinder the market's growth. The high amount of polyvinyl butyral recycling in developed economies could also hurt the market because it would cause environmental problems.

- In the coming years, the market is likely to grow thanks to growing demand from the photovoltaic industry and more people buying electric cars.

- During the period of the forecast, the Asia-Pacific region is expected to lead and have the highest CAGR.

Polyvinyl Butyral (PVB) Market Trends

The Automotive Segment to Dominate the Market

- Polyvinyl butyral is a polymer with good mechanical properties that are commonly used as an interlayer material in laminated glass. The PVB sheet adheres to both layers of glass, keeping them unbroken even after impact. Because the bond between the PVB sheet and the glass is chemical, it does not delaminate easily.

- PVB is mostly found in laminated safety glass for car windshields. Because of the safety and security it provides in automotive windscreens, the demand for PVB as an interlayer in sandwich laminated glass has skyrocketed. Furthermore, acoustic insulation and UV protection are important advantages of PVB that increase its use in the automotive industry.

- The Organization Internationale des Constructeurs d'Automobiles (OICA) predicts that 80 million vehicles will be made around the world in 2021, which is about 3% more than the 78 million vehicles that will be made in 2020.

- Toyota, a renowned automobile company, increased vehicle sales and manufacturing by around 4% in November 2022 compared to the previous year. Toyota's total vehicle sales and production from January to November 2022 were around 9.5 million and 9.7 million, respectively. Even though sales didn't change much from the year before, production did go up by about 7% compared to the year before.

- The European Automobile Manufacturers' Association stated in its latest report that a total of 194 automobile manufacturing units operate on European Union soil. Also, a total of about 12 million vehicles will be made in Europe in 2021.

- The ACEA also saw an increase in passenger automobile registrations in December 2022, which grew by roughly 13% month over month compared to December 2021. Germany gained the highest percentage of registrations (+38%), followed by Italy (+21.0%). With the increased registration of passenger vehicles, demand for production is also increasing in the industry, significantly impacting the PVB market.

- So, the above factors are likely to keep the polyvinyl butyral market going in the years to come.

The Asia-Pacific Region to Dominate the Market

- Asia-Pacific is expected to be the biggest market in the world because China, India, Japan, and Singapore are building more buildings and selling and making more cars, and because investments are being made in the region to help solar energy production.

- According to the China Association of Automobile Manufacturers, China has also seen an increase in automotive production in the country of around 2.1% in the year 2022, compared to the previous year. About 26.86 million units of automobiles were sold in the United States in 2014. China has also seen an increase in automotive production in the country of around 2.1% in the year 2022, compared to the previous year. About 26.86 million units of automobiles were sold in 2022, as compared to 26.27 million units sold in 2021.

- According to the Indian Brand Equity Foundation, the Indian automotive industry is expected to reach around USD 300 billion by 2026. Moreover, in FY 2022, passenger vehicle sales in the country reached about 3 million.

- Between April 2000 and June 2022, the automobile industry received approximately USD 33.53 billion in cumulative equity FDI inflows. The Indian government thought that between USD 8 billion and USD 10 billion more would be invested in the car business from India and other countries by 2023.

- The Japanese construction industry is also expected to bloom due to the events expected to be hosted in the country. For instance, Osaka will host the World Expo in 2025. The construction is mostly driven by redevelopment and recovery from natural disasters. Two high-rise towers for Tokyo Stations, a 37-story, 230-meter-tall office tower initially planned to be completed in 2021, and a 61-story, 390-meter-tall office tower, are due for completion in 2027.

- According to Japan's Ministry of Land, Infrastructure, Transport, and Tourism (MLIT), total investment in the construction sector in 2022 is expected to be around 66,990 billion yen (USD 508.16 billion), which is a 0.6% increase over the previous year.

- Growing investments in the auto, construction, and other industries would lead to a rise in demand for polyvinyl butyral (PVB) because it serves those industries. This would be good for the market over the next few years.

Polyvinyl Butyral (PVB) Industry Overview

The polyvinyl butyral (PVB) market is partially consolidated, with a few major players dominating a significant portion of the market. Some of the key players in the market include (in no particular order): Eastman Chemical Company, Kuraray Co. Ltd., Sekisui Chemical Co. Ltd., Kingboard (Fogang) Specialty Resins Co. Ltd. (KB PVB), and Chang Chun Group.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Construction and Infrastructure Activities Across the World

- 4.1.2 Growing Applications for Laminated Glass

- 4.2 Restraints

- 4.2.1 Availability of Product Substitutes in the Market

- 4.2.2 High Recycling Activities of Polyvinyl Butyral in Developed Economies

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitutes

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 Adhesive Films

- 5.1.2 Paints and Coatings (including Wash Primers)

- 5.1.3 Printing Inks and Lacquers

- 5.1.4 Other Types (Binders for Ceramics and Composite Fibers)

- 5.2 End-user Industry

- 5.2.1 Automotive

- 5.2.2 Construction

- 5.2.3 Power Generation

- 5.2.4 Other End-user Industries (Aerospace, Defense)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Chang Chun Group

- 6.4.2 Everlam

- 6.4.3 Genau Manufacturing Company LLP

- 6.4.4 Huakai plastic(Chongqing) Co., Ltd.

- 6.4.5 Kingboard FoGang Specialty Resins Co. Ltd

- 6.4.6 KURARAY CO. LTD

- 6.4.7 Eastman Chemical Company

- 6.4.8 Sekisui Chemical Co. Ltd.

- 6.4.9 WMC GLASS

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Demand from the Photovoltaic Industry

- 7.2 Increasing Adoption of EVs

聚乙烯丁醛市場規模、佔有率和成長分析(按應用、最終用途行業和地區)- 2025-2032 年行業預測

聚乙烯丁醛市場規模、佔有率和成長分析(按應用、最終用途行業和地區)- 2025-2032 年行業預測 聚乙烯醇縮丁醛(PVB)全球市場(2018-2034)

聚乙烯醇縮丁醛(PVB)全球市場(2018-2034) 聚乙烯醇縮丁醛 (PVB) 市場機會、成長動力、產業趨勢分析及 2025-2034 年預測

聚乙烯醇縮丁醛 (PVB) 市場機會、成長動力、產業趨勢分析及 2025-2034 年預測 聚乙烯丁醛(PVB)市場:未來預測(2025-2030)

聚乙烯丁醛(PVB)市場:未來預測(2025-2030) 聚乙烯丁醛市場:按應用、最終用途分類 - 2025-2030 年全球預測

聚乙烯丁醛市場:按應用、最終用途分類 - 2025-2030 年全球預測 聚乙烯丁醛(PVB) 的全球市場規模、佔有率和趨勢分析:按應用、最終用途和地區分類的展望和預測 (2024-2031)

聚乙烯丁醛(PVB) 的全球市場規模、佔有率和趨勢分析:按應用、最終用途和地區分類的展望和預測 (2024-2031) 2024-2028年全球聚乙烯丁醛市場

2024-2028年全球聚乙烯丁醛市場