|

市場調查報告書

商品編碼

1690079

自動化 3D 列印:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Automated 3D Printing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

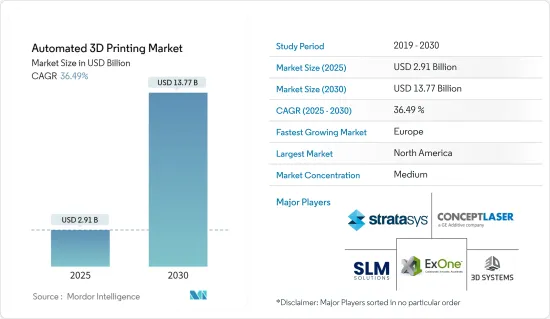

自動化 3D 列印市場規模預計在 2025 年為 29.1 億美元,預計到 2030 年將達到 137.7 億美元,預測期內(2025-2030 年)的複合年成長率為 36.49%。

預計研發投入的增加和工業自動化中機器人的應用增加將推動市場成長。

主要亮點

- 在過去的幾年裡,3D 列印經歷了從原型製作和小批量生產到大規模生產技術的穩定轉變,產業和非列印機供應商將重點轉向自動化。此外,隨著積層製造趨勢的發展,硬體正從用作原型製作、工具和單一零件生產的獨立系統,發展成為整合數位量產線中的核心系統,從而增加了新興無人工廠的機會。

- 人工智慧和機器學習技術正在積層製造業的各種應用中尋找自己的位置。例如,麻省理工學院(MIT)的研究人員應用機器學習的資料驅動特性來自動化發現新 3D 列印材料的流程。利用機器學習,對韌性、抗壓強度等材料性能因素進行演算法最佳化,迅速超越了傳統的3D列印材料配方方法。研發部門開發了一個名為 AutoOED 的免費開放原始碼材料最佳化平台,以便其他研究人員可以進行材料最佳化。

- 同樣,2022 年 1 月,來自德國和加拿大的一組組織啟動了一項新的合作,利用 3D 列印和人工智慧實現零件夾持流程的自動化。自適應雷射積層製造過程感測的人工智慧增強 (AI-SLAM)計劃旨在創建強大的基於 AI 的軟體,可自主操作指向性能量沉積技術(DED) 3D 列印機。該軟體透過演算法控制列印過程,以更好地修復受損部件的表面不規則。弗勞恩霍夫雷射技術研究所 (ILT) 和軟體公司 BCT 是該德國財團的成員。在加拿大,該研究將由加拿大國家研究委員會 (NRC)監督。麥吉爾大學將協調這項研究,機器學習公司 Braintoy 將協助編程 AI 模型。

- 此外,參與者正在採取各種市場開發措施來鞏固其在市場中的地位。例如,2021年4月,Mosaic宣布了其自動化3D列印平台Array。該平台為四台 Element HT 印表機裝載和卸載材料、開始列印、移除列印件並儲存它們以準備開始下一次列印。 Array 的設計具有最大的靈活性,它採用自動販賣機式的機械臂,透過取出列印件、將其放在一邊並為下一次列印裝載乾淨的床來確保最大的產量。

- 2021 年 10 月,總部位於溫哥華的 3D 列印產業自動化技術開發商 3DQue 宣布推出適用於 Creality CR-10 和 CR-6 SE 的兩款全新 Quinly 自動化套件。 Quinly 是虛擬3D 列印機操作員,由 Raspberry Pi 驅動,Raspberry Pi 是一套可自行運作桌上型 3D 列印機的硬體和軟體套件。該技術旨在透過消除手工勞動,使 3D 列印更具可擴展性。它主要針對印刷實驗室、按需製造商、教育機構以及任何尋求自動化、大量零件生產的人。

- 此外,由於供應鏈中斷以及對治療和材料的新需求,COVID-19 疫情大大加速了製藥、醫療設備和製造業的技術進步。供應鏈的缺陷導致醫護人員難以獲得所需的物資,醫院也缺乏個人防護工具(PPE)和對抗病毒的醫療設備。因此,積層製造(AM)——自動化 3D 列印——因其在快速生產複雜整體零件甚至機械系統方面的可近性和靈活性而成為值得關注的製造流程之一。

自動化 3D 列印市場趨勢

汽車產業可望推動市場成長

- 汽車作為當今的主要交通途徑,是人類生活中不可或缺的一部分。目前,全球道路上行駛的汽車超過 13 億輛,預計到 2035 年將成長到 18 億輛。其中,乘用車約佔 74%,輕型商用車、卡車、巴士、長途客車和小型巴士佔剩餘的 26%。

- 3D 列印可用於製造模具和熱成型工具,以快速生產夾具、夾具和固定裝置。這使得汽車製造商能夠以低成本生產樣品和工具,從而消除了投資高成本模具時未來生產損失。 2014 年,Local Motors 推出了首款 3D 列印電動車。此後,寶馬集團等其他老字型大小企業也紛紛效仿,採用自動化 3D 列印技術。在美國幾家大型汽車製造商中,大約 80% 至 90% 的初始原型組裝都是透過 3D 列印完成的,而且自動化趨勢還在持續成長。最受歡迎的部件包括排氣部件、進氣部件和管道部件。這些部件經過數位化設計、3D 列印、快速安裝到汽車上,然後反覆測試。

- 自動化 3D 列印在汽車行業最常見的應用可能是創建夾具和固定裝置等製造輔助工具。使用傳統方法創建製造工具非常昂貴且耗時,且幾何限制會降低製造過程的效率並限制最終用途零件的幾何形狀。 3D 列印製造工具更輕、更符合人體工學,使工廠工人能夠更輕鬆、更安全地完成工作。

- 此外,汽車製造所涉及的生產量非常巨大,每個零件的運行次數高達數十萬次。這是目前大多數 3D 列印技術難以企及的。然而,許多高階汽車製造商將汽車產量限制在數千輛,因此自動化 3D 列印成為可行的選擇。

- 根據世界經濟論壇預測,到2035年,全自動駕駛汽車的銷售量將佔全球汽車市場的25%,高於與前一年同期比較。此外,馬達製造商的多項措施也促進了市場的成長。 2020年3月,英國工程公司Equipmake開發出功率密集型永磁馬達。該馬達是與 3D 列印專家 Hieta 合作設計的。 Equipmake 的 Ampere馬達重量接近 10 公斤,但可提供 295 匹馬力的功率。

- 此外,支架是一種常見的小型部件,當工程師受到傳統製造方法的限制時,以前很難對其進行最佳化。現在,工程師可以設計最佳化的支架,並藉助3D列印實現這些設計。勞斯萊斯最近展示了其支架的 3D 列印功能。該公司展示了大量經過 DfAM 最佳化和 3D 列印的金屬汽車零件,其中許多看起來像支架。雖然原型製作仍然是 3D 列印在汽車行業的主要應用,但該技術在工具方面的應用正在迅速擴大。大眾汽車內部已使用 3D 列印多年。該公司的黏著劑噴塗成型技術也用於製造這些組件。福斯汽車也於2021年7月宣布,將與西門子、惠普合作,實現結構件3D列印工業化。

預計北美將佔據較大的市場佔有率

- 北美是全球自動化 3D 列印的主要市場之一,其中美國佔據該地區的大部分佔有率。該國不斷成長的需求歸因於大大小小的眾多供應商的存在。例如,總部位於加州卡爾斯巴德的 Forecast 3D 公司為醫療保健、汽車、航太、消費品和設計產業提供多種材料的 3D 列印服務。

- 在強大的人工智慧應用快速發展的推動下,閉合迴路控制系統長期以來一直是積層製造工程師的基本目標。例如,通用電氣紐約尼斯卡尤納增材研究實驗室的調查團隊開發了一個專有的機器學習平台,該平台使用高解析度攝影機逐層監控列印過程,檢測出肉眼通常看不到的條紋、凹坑、孔洞和其他問題。此外,還可以使用電腦斷層掃描 (CT) 影像將這些資料與預先記錄的缺陷資料庫即時進行比較。利用高解析度影像和電腦斷層掃描資料,訓練 AI 系統預測整個列印過程中的困難並檢測缺陷。

- 此外,市場正見證各種與聚合物3D列印相關的技術專利。例如,2020年8月,工業3D列印自動化和智慧後列印解決方案提供商之一PostProcess Technologies Inc.獲得了聚合物3D列印自動化後列印技術的專利。 SVC 技術是 PostProcess 積層製造系列 3D 列印聚合物支撐去除和樹脂去除解決方案的一部分。此取得專利的方法使用正在申請專利的清洗劑和專有演算法,確保 3D 列印組件在列印後均勻、一致且可靠地暴露於清洗劑和空化中。

- 此外,各種供應商都在該地區擴建設施,主要是為了應對供應鏈挑戰和各個終端用戶垂直領域日益成長的需求。例如,2021年2月,Roboze宣布將在德克薩斯州休士頓開設美國總部,以促進國內生產回流並解決供應鏈問題。 Roboze 計劃在未來兩年內招聘 100 多名員工,擴大其在美國工程和製造能力,以滿足航太、石油天然氣和移動等行業對 3D 列印技術日益成長的需求。

- 同樣,2021 年 4 月,Roboze 宣布推出 Roboze Automate,這是一套工業自動化系統,它將採用超級聚合物和複合材料的客製化 3D 列印引入到極端終端用戶應用的生產工作流程中。隨著美國開始大力推動基礎建設,該國正面臨金屬短缺的問題,影響能源、交通、製造業等各產業。 Roboze 將 PEEK(一種理想的金屬替代品的新型聚合物平台技術)與與 B&R 合作開發的 PLC 工業自動化系統相結合。

自動化 3D 列印產業概覽

自動化 3D 列印市場競爭激烈,幾家主要參與者競相搶佔更大的市場佔有率,然而,主要參與者已經佔據了很大比例的消費者,並且正在投資研發並與硬體供應商合作以進一步開發和創新。主要企業包括 Stratasys Ltd、3D Systems Corporation、The ExOne Company 等。

- 2022 年 2 月 - Viaccess-Orca、ShipParts.com 和 SLM Solutions 宣布了一項新技術解決方案,可實現積層製造(AM) 的直接雲端列印。這種全自動軟體執行透過控制允許列印的數量、持續時間和參數來保護與零件資料相關的製造商的智慧財產權 (IP)。基於 VO 的 SMP 軟體庫和 SLM Solutions 的韌體韌體的本地整合,該 Cloud-to-Print 解決方案讓製造商充滿信心,在獲得列印許可時他們的 IP 受到保護。

- 2022 年 1 月 - 著名的積層製造 (AM) 軟體和服務供應商 Materialise NV、品質保證軟體供應商 Sigma Labs, Inc. 和 Materialise 合作開發了可增強金屬 AM 應用可擴展性的技術。新平台將 Sigma Labs 的 PrintRite3D 感測器技術與 Materialise 控制平台結合,使用戶能夠即時識別和糾正金屬建構問題。

- 2022 年 1 月-PostProcess Technologies 宣布增加一條新的自動化、智慧印後解決方案系列。新款 VORSA 500 利用 PostProcess 技術為 3D 列印的 FDM 零件提供一致、免持的支撐結構拆除。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況

- 產業價值鏈分析

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 買家的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭強度

- COVID-19 產業影響評估

第5章 市場動態

- 市場促進因素

- 增加研發投入

- 機器人在工業自動化的應用日益廣泛

- 市場挑戰

- 營運挑戰

第6章 市場細分

- 奉獻

- 硬體

- 軟體

- 服務

- 流程

- 自動化生產

- 物料輸送

- 零件處理

- 後製處理

- 多處理

- 按最終用戶產業

- 工業生產

- 車

- 航太和國防

- 消費性產品

- 衛生保健

- 能源

- 其他最終用戶產業

- 地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

第7章 競爭格局

- 公司簡介

- Stratasys Ltd

- Concept Laser Inc.(GE Additive)

- The ExOne Company

- SLM Solutions Group AG

- 3D Systems Corporation

- Universal Robots AS

- Formlabs

- PostProcess Technologies Inc.

- Materialise NV

- Authentise Inc.

- DWS Systems

- Coobx AG

- ABB Group

第8章投資分析

第9章 市場機會與未來趨勢

The Automated 3D Printing Market size is estimated at USD 2.91 billion in 2025, and is expected to reach USD 13.77 billion by 2030, at a CAGR of 36.49% during the forecast period (2025-2030).

The increasing investments in R&D and growth in the adoption of robotics for industrial automation are expected to propel market growth.

Key Highlights

- Over the last few years, 3D printing has constantly experienced a shift from the prototyping and small batches phase to mass production technology with a growing adoption rate across the industries, where the industrial and non-printer vendors have shifted their focus toward automation. Also, with the evolutionary trend for additive manufacturing, hardware growing beyond stand-alone systems that are used for prototyping, tooling, and single-part production to be used as core systems within integrated digital mass production lines is driving the number of opportunities in the emerging lights-out factories.

- Artificial Intelligence and machine learning technologies are finding their way through various applications in the additive manufacturing industry. For instance, researchers from MIT have applied the data-driven nature of machine learning to automate the process of discovering new 3D printing materials. With machine learning, material performance factors, such as toughness and compression strength, were optimized using an algorithm that quickly outperformed conventional methods of 3D printing material formulation. The researchers developed a free, open-source materials optimization platform called AutoOED, allowing other researchers to conduct their material optimization.

- Similarly, in January 2022, a group of organizations from Germany and Canada formed a new collaboration to use 3D printing and AI to automate the process of fixing parts. The Artificial Intelligence Enhancement of Process Sensing for Adaptive Laser Additive Manufacturing (AI-SLAM) project aims to create powerful AI-based software that can run directed energy deposition (DED) 3D printers automatically. To more successfully repair uneven surfaces on damaged components, the software will algorithmically regulate the printing process. The Fraunhofer Institute for Laser Technology (ILT) and a software company BCT are part of the German consortium. In Canada, the work will be overseen by the National Research Council of Canada (NRC). McGill University will coordinate the research, and machine learning firm Braintoy will help program the AI models.

- Furthermore, there have been various developments in the market by players to enhance their position in the market. For instance, in April 2021, Mosaic launched Array, an automated 3D printing platform, which loads and unloads materials for its four Element HT printers, starts prints, removes prints, and stores them so that the next prints can begin. The Array is designed for maximum flexibility with its vending machine-style robotic arm that removes prints, places them to the side, and loads a clean bed for the next print, ensuring maximum output.

- In October 2021, 3DQue, a Vancouver-based developer of automation technology for the 3D printing industry, announced the launch of two new Quinly automation kits for the Creality CR-10 and CR-6 SE. Quinly is a virtual 3D printer operator served by a Raspberry Pi, a hardware and software kit capable of running desktop 3D printers on its own. The technology is designed to make 3D printing more scalable by taking manual labor out of the equation. It is primarily aimed at print labs, on-demand manufacturers, educational institutions, and anyone else seeking automated mass part production.

- Additionally, due to the disruption of supply chains and new demands for treatments and materials, the COVID-19 pandemic has significantly accelerated technological advancements in the pharmaceutical, medical device, and manufacturing sectors. The supply chain shortages have made it hard for medical personnel to get the supplies they need, generating a shortage of personal protection equipment (PPE) and medical devices in hospitals for fighting off the virus. Owing to this, additive manufacturing (AM) (automated 3D printing) has emerged as one remarkable fabrication process because of its accessibility and flexibility to produce complex and monolithic parts or even mechanical systems quickly.

Automated 3D Printing Market Trends

The Automotive Segment is Expected to Drive the Market's Growth

- Automobiles are an essential part of human lives as the main mode of transportation today. Currently, there are over 1.3 billion motor vehicles on the road globally, with that number expected to rise to 1.8 billion by the year 2035. Passenger cars comprise roughly 74% of these statistics, while light commercial vehicles and heavy trucks, buses, coaches, and minibusses make up the remaining 26%.

- 3D printing can be used in making molds and thermoforming tools for the rapid manufacturing of grips, jigs, and fixtures. This allows automakers to produce samples and tools at low costs and eliminate future production losses when investing in high-cost tooling. The first-ever 3D-printed electric car was launched in 2014 by Local Motors. Subsequently, other established firms, like the BMW group, have also followed suit in terms of adopting automated 3D printing techniques. In several major US auto manufacturers, around 80%-90% of each initial prototype assembly has been 3D printed, with an increasing trend toward automation. Some of the popular components are parts of the exhaust, air intake, and ducting. These parts are designed digitally, 3D printed, and fitted on a car in short order, then tested through multiple iterations.

- Perhaps the most popular use of automated 3D printing in the automotive space is fabricating manufacturing aids like jigs and fixtures. Making manufacturing tools using traditional means is rather costly and time-consuming, and geometry limitations translate into less efficient manufacturing processes and more constraints on the geometry of end-use parts. Manufacturing tools that are 3D printed are lighter and more ergonomic, making it easier and safer for factory workers to perform their duties.

- Furthermore, the production volumes associated with automotive manufacturing are very high, tallying to hundreds of thousands of runs for every part. That would be difficult for most 3D printing technologies to keep up with (for now). But many high-end automobile manufacturers limit the production runs of their cars to only a few thousand units, which makes automated 3d printing a viable option.

- According to the World Economic Forum, more than 12 million fully autonomous cars are expected to be sold per year-on-year 2035, covering 25% of the global automotive market. Also, several initiatives taken by the electric motor manufacturers are leading to the growth of the market. In March 2020, UK-based engineering company Equipmake developed a power-dense permanent magnet electric motor. The motor was designed in collaboration with Hieta, a 3D printing specialist. Equipmake's Ampere motor will weigh near to 10kg but provide an output of 295bhp.

- Furthermore, Brackets are small and rather mundane parts, which were very difficult to optimize in the past time when engineers were constrained by the traditional manufacturing methods. Currently, engineers can design optimized brackets and bring these designs to life with the help of 3D printing. Rolls Royce recently showcased the capabilities of 3D printing for brackets. The company showed off a large batch of DfAM-optimized and 3D-printed automotive metal parts, many of which look to be bracketed. While prototyping remains the primary application of 3D printing within the automotive industry, using the technology for tooling is rapidly catching on. One major example of this is Volkswagen, which has been using 3D printing in-house for a number of years. Their binder jetting technology is also in use to construct the component. Also, in July 2021, Volkswagen stated that it is partnering with Siemens and HP to industrialize 3D printing of structural parts, which can be significantly lighter than equivalent components made of sheet steel.

North America is Expected to Hold a Major Market Share

- North America is one of the significant markets for Automated 3D printing globally, with the United States accounting for a significant share in the region. The country's rising demand can be attributed to the vast presence of small and big vendors. For instance, Forecast 3D in Carlsbad, CA, offers 3D printing services in a variety of materials to the healthcare, automotive, aerospace, consumer products, and design industries.

- Closed-loop control systems have long been a fundamental aim for additive manufacturing engineers due to the rapid development of powerful AI applications. For instance, Researchers at GE's Niskayuna Additive Research Lab, New York, created a proprietary machine-learning platform that uses high-resolution cameras to monitor the printing process layer by layer and detect streaks, pits, holes, and other problems that are typically invisible to the naked eye. Further, The data is compared in real-time to a pre-recorded flaws database utilizing computer tomography (CT) imaging. The AI system will be trained to forecast difficulties and detect flaws throughout the printing process using the high-resolution image and CT scan data.

- Furthermore, the market is witnessed with various technology patents for polymer 3D printing. For instance, in August 2020, PostProcess Technologies Inc., one of the providers of automated and intelligent post-printing solutions for industrial 3D printing, received a patent for automated post-printing technology for polymer 3D printing. The SVC technology is part of PostProcess's additive manufacturing family of 3D printed polymer support removal and resin removal solutions. This patented method uses patent-pending detergents and proprietary algorithms to ensure that 3D printed components are exposed to detergent and cavitation uniformly, consistently, and reliably during post-printing.

- Also, various vendors are expanding facilities into the region, primarily to address the supply chain challenges and growing demand in various end-user verticals. For instance, in February 2021, Roboze announced the opening of its US headquarters in Houston, Texas, to facilitate the reshoring of domestic production and address supply chain issues. Roboze will be able to increase its engineering and production capacity in the United States with plans to hire over 100 employees in the next two years and address a growing demand for 3D printing technology in industries such as aerospace, oil and gas, and mobility.

- Similarly, in April 2021, Roboze announced the launch of Roboze Automate, the industrial automation system to bring customized 3D printing with super polymers and composites into the production workflow for extreme end-user applications. The United States is experiencing a metals deficit that is affecting each of the industry areas as it begins an infrastructure push that spans from energy to transportation to manufacturing. Roboze combined its novel polymer platform technology, PEEK, an ideal metals replacement technology, with a PLC industrial automation system developed in partnership with B&R.

Automated 3D Printing Industry Overview

The automated 3D printing market is competitive and consists of several major players who are trying to gain a larger share, but top players have gained a major proportion of consumers and also investing in R&D and partnerships with hardware vendors for more developments and innovations. Some of the key players include Stratasys Ltd, 3D Systems Corporation, and The ExOne Company, among others.

- February 2022 - Viaccess-Orca, ShipParts.com, along with SLM Solutions, announced a new technology solution that enables direct Cloud-to-Print for additive manufacturing (AM). This fully automated software execution protects the manufacturer's intellectual property (IP) associated with part data by controlling the quantity, duration, and parameters of acceptable prints. Based on the native integration of VO's SMP software library and SLM Solutions machine firmware, this Cloud-to-Print solution allows manufacturers to be fully confident that their IP will be protected when printing is licensed.

- January 2022 - Materialise NV, a renowned provider of additive manufacturing (AM) software and services, Sigma Labs, Inc., a provider of quality assurance software, and Materialise, together have developed a technology to enhance the scalability of metal AM applications. The new platform combines Sigma Labs' PrintRite3D sensor technology to Materialise Control Platform to enable the users to identify and correct metal build issues in real-time.

- January 2022 - PostProcess Technologies announced the addition of a new solution lineup of automated, intelligent post-printing solutions for additive manufacturing (AM) to its portfolio. The new VORSA 500 leverages PostProcess technology for consistent, hands-free support structure removal on 3D printed FDM parts.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assestment of the Impact of COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Investments in R&D

- 5.1.2 Growth in Adoption of Robotics for Industrial Automation

- 5.2 Market Challenges

- 5.2.1 Operational Challenges

6 MARKET SEGMENTATION

- 6.1 Offering

- 6.1.1 Hardware

- 6.1.2 Software

- 6.1.3 Services

- 6.2 Process

- 6.2.1 Automated Production

- 6.2.2 Material Handling

- 6.2.3 Part Handling

- 6.2.4 Post-Processing

- 6.2.5 Multiprocessing

- 6.3 End-user Vertical

- 6.3.1 Industrial Manufacturing

- 6.3.2 Automotive

- 6.3.3 Aerospace and Defense

- 6.3.4 Consumer Products

- 6.3.5 Healthcare

- 6.3.6 Energy

- 6.3.7 Other End-user Verticals

- 6.4 Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia Pacific

- 6.4.4 Latin America

- 6.4.5 Middle-East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Stratasys Ltd

- 7.1.2 Concept Laser Inc. (GE Additive)

- 7.1.3 The ExOne Company

- 7.1.4 SLM Solutions Group AG

- 7.1.5 3D Systems Corporation

- 7.1.6 Universal Robots AS

- 7.1.7 Formlabs

- 7.1.8 PostProcess Technologies Inc.

- 7.1.9 Materialise NV

- 7.1.10 Authentise Inc.

- 7.1.11 DWS Systems

- 7.1.12 Coobx AG

- 7.1.13 ABB Group

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

工業用小型台秤市場:2025 年全球市場

工業用小型台秤市場:2025 年全球市場 全球 3D 列印服務局市場:產業分析、規模、佔有率、成長、趨勢和預測(2025-2032 年)

全球 3D 列印服務局市場:產業分析、規模、佔有率、成長、趨勢和預測(2025-2032 年) 輪胎模具 3D 列印機市場按印表機技術類型、應用、最終用戶和應用分類 - 2025-2030 年全球預測

輪胎模具 3D 列印機市場按印表機技術類型、應用、最終用戶和應用分類 - 2025-2030 年全球預測 2025-2029年全球3D列印市場

2025-2029年全球3D列印市場 2025年3D列印機全球市場報告

2025年3D列印機全球市場報告 顆粒3D印表機的全球市場:2030年為止的預測

顆粒3D印表機的全球市場:2030年為止的預測 全球自動化 3D 列印市場規模:按產品、按流程、按最終用戶、按地區、範圍和預測

全球自動化 3D 列印市場規模:按產品、按流程、按最終用戶、按地區、範圍和預測 全球 3D 列印機市場規模、佔有率和成長分析:按產品、技術、應用、流程、產業和地區分類 - 產業預測,2024-2031 年

全球 3D 列印機市場規模、佔有率和成長分析:按產品、技術、應用、流程、產業和地區分類 - 產業預測,2024-2031 年 到 2030 年自動化 3D 列印市場預測:按組件、工藝、技術、應用、最終用戶和地區進行的全球分析

到 2030 年自動化 3D 列印市場預測:按組件、工藝、技術、應用、最終用戶和地區進行的全球分析 全球 3D 列印機市場:2025-2030 年預測

全球 3D 列印機市場:2025-2030 年預測