|

市場調查報告書

商品編碼

1690783

表面黏著技術:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Surface Mount Technology - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

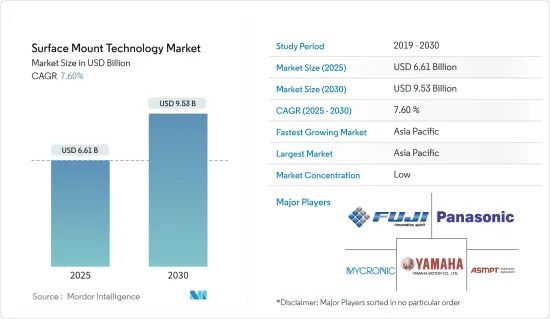

表面黏著技術市場規模預計在 2025 年為 66.1 億美元,預計到 2030 年將達到 95.3 億美元,預測期內(2025-2030 年)的複合年成長率為 7.6%。

表面黏著技術(SMT) 是一種建構電子電路的方法,其中組件直接安裝到印刷基板(PCB) 的表面上。這與舊的通孔技術形成對比,舊的通孔技術是將元件插入 PCB 上鑽孔中。 SMT 中使用的組件稱為 SMD,具有可直接焊接到 PCB 表面的小金屬片或端蓋。這使得單一 PCB 上可以使用更小、更輕以及更多的組件。

疫情爆發後,筆記型電腦和伺服器市場需求激增。據印度電子和半導體協會 (IESA) 稱,隨著在家工作和協作工具的採用,越來越多的資料被儲存在雲端。伺服器、資料中心和運算領域的需求正在激增。美國美光科技公司也報告稱,由於遠距工作經濟、遊戲和電子商務的活性化,資料中心的需求增加。此外,根據 Cloudscene 的數據,截至 2024 年 3 月,美國擁有 5,381 個資料中心,比世界上任何其他國家都多。另外有 521 家在德國,514 家在英國。

電子元件的小型化使得生產可以隨身攜帶的小型、攜帶式、手持式可攜式成為可能。因此,現在市場上出現了更小、更輕且處理能力更強大的設備。由於組件可以輕鬆嵌入(例如,放入衣服袋中)並可長時間攜帶,因此它們變得越來越容易穿戴。元件變得越來越小,對安裝它們的印刷電路基板的設計提出了新的要求。 NCAB集團堅定地致力於IPC制定超高密度Ultra HDI印刷電路基板標準的努力,並預計能夠在2023年向客戶交付。

表面黏著技術(SMT) 已成為現代電子製造的重要組成部分,與傳統通孔方法相比具有無數優勢。 SMT 的一個明顯優勢是顯著減少所需的 PCB 鑽孔量。透過省去鑽孔步驟,製造商可以節省時間和金錢,這對於複雜的高密度基板尤其有利。這項轉變將簡化生產,降低人事費用和材料成本,並提高製造過程的整體成本效益。

表面黏著技術能夠生產更小、更有效率、更具成本效益的電子設備,從而徹底改變了電子製造業。然而,儘管 SMT 具有許多優點,但它並不適合所有應用。 SMT不適用於變壓器、電源電路等高功率、高壓元件。這些組件會產生熱量並具有高電負荷,而 SMT 的設計無法有效處理。

根據美國預算辦公室預測,到2033年,美國國防支出將逐年增加。到2023年,美國國防支出將達到7,460億美元。同一項預測也預測,到2033年,國防支出將增加至1.1兆美元。

表面黏著技術(SMT) 市場趨勢

消費性電子終端用戶產業預計將佔據相當大的市場佔有率

- 在汽車產業,SMT 用於電控系統(ECU)、儀表板顯示器、雷達和相機模組、電池管理系統(BMS)、安全輔助系統等。 SMT 已成為汽車應用中的關鍵製造流程。 SMT 以其高效、精確和可靠而聞名,對於驅動各種車載電子產品至關重要,包括 ADAS(高級駕駛輔助系統)、資訊娛樂系統和車輛控制系統。

- 在現代汽車中,車載控制系統充當汽車的“大腦”,監督和協調所有電子元件的功能。車載控制系統對於導航、音訊、空調等一切設備的無縫運作至關重要。這些控制系統可靠性的核心是 SMT 技術。此技術可將微小的電子元件精確地放置在電路基板,確保系統有效率且可靠的運作。

- 引擎控制單元 (ECU) 是汽車電子系統的核心,監督引擎性能、傳動和煞車等重要操作。表面黏著技術(SMT) 對於將微晶片、電阻器、電容器和其他表面黏著技術組件組裝到 ECU 中至關重要。

- 此外,人工智慧技術預計將在汽車領域得到更廣泛的應用。電子組裝中表面黏著技術(SMT)的精度和效率為人工智慧晶片和處理器的生產提供了動力。因此,汽車電子產品將具有增強的自主決策能力,促進智慧駕駛和車輛自動化。

- 正如國際能源總署所強調的,全球汽車產業正在經歷深刻的變革時期,這可能對能源產業產生重大影響。預測表明,到 2030 年,電氣化將減少每天 500 萬桶石油的需求。

- IEA報告也顯示,電動車銷量將大幅成長,2023年銷量將與2022年相比成長35%至350萬輛。最值得注意的是,全年每週都有超過 250,000 個新註冊。 2023 年,電動車將佔總銷量的 18% 左右,高於五年前的 2% 和 2022 年的 14%。這些趨勢表明,隨著電動車市場的成熟,強勁成長預計將持續下去。此外,預計到2023年,70%的電動車保有量將由電池電動車組成。

亞太地區預計將經歷最快成長

- 亞太地區,尤其是日本、中國、韓國、台灣和東南亞等國家,是全球電子製造中心。該地區強大的製造業基礎設施、熟練的勞動力和支持性的政府政策正在吸引跨國公司,刺激當地電子產業的成長。平板電腦、智慧型手機和其他電子設備的需求持續成長,需要透過表面黏著技術實現高效、大量的生產能力。該公司預計,透過在本地引進SMT(表面黏著技術),附加價值將從目前的15%提升至25%。

- 例如,2023年8月,印度政府正積極與全球電子公司合作,提昇在印度組裝的產品的本地附加價值,目標在未來5-10年內大幅成長60-80%。為實現此目標,政府鼓勵印度工業採用表面黏著技術(SMT)生產線等先進的生產方法。

- 碳化矽(SiC)因具有耐高溫、優異的電導性、優異的能源效率等特點,受到越來越多的關注。隨著工業 4.0 推動對電動車 (EV)、太陽能板和先進電源管理的需求,SiC 製造變得越來越重要。鑑於需要盡量減少這些區域的電力消耗,寬能能隙導體是自然的選擇。

- 2024 年 2 月,大陸設備印度有限公司 (CDIL) 邁出了重要一步,運作了一條專用於 SiC表面黏著技術(SMT) 組件的新組裝。這確立了 CDIL 作為印度 SiC 元件製造先驅的地位。透過這項改進,CDIL 現在能夠生產各種汽車級設備,如 SiC 肖特基二極體、SiC MOSFET、齊納二極體、整流器和 TVS 二極體,以滿足全球和國內市場的需求。

- 2024 年 4 月,TDK 公司宣布推出 B40910 系列,這是一系列混合聚合物電容器,最大電流可達 4.6 A(100 kHz、+125 度C時)。這些表面黏著技術元件在室溫下具有驚人的低 ESR 值 17mΩ 和 22mΩ。

- 與使用液體電解質的標準電解電容器不同,TDK 電容器的 ESR 隨溫度的變化很小。這些緊湊型元件的尺寸為 10 x 10.2 毫米或 10 x 12.5 毫米(深 x 高),額定電壓為 63 V,電容範圍為 82 μF 至 120 μF。因此,SMT 製造商正在透過技術整合和創新來推動對該技術的需求。這些努力促進了表面黏著技術(SMT) 在各行業的廣泛應用和發展。

表面黏著技術(SMT) 產業概覽

表面黏著技術市場高度分散,既有全球參與者,也有中小型企業。市場的主要企業包括FUJIFILM、Yamaha Motor Co, Ltd.、Mycronic AB、ASMPT 和Panasonic。市場參與者正在採用合作和收購的方式,以加強其產品供應並獲得競爭優勢。

2024 年 3 月 - 諾信公司在墨西哥克雷塔羅設立了新的拉丁美洲技術中心,以幫助該地區的製造商及時獲得反饋,了解哪種流體分配設備最適合他們的裝配流體、零件、基板和生產要求。實驗室配備了 3D 列印機、秤和其他測量設備,使我們能夠根據每個客戶的特定應用要求確定合適的流體分配設備。

2024年1月-Yamaha Motor Co, Ltd.株式會社宣布推出YRM10表面黏著技術,該貼片機在貼片性能方面被譽為同類產品中最快的。其速度高達 52,000 CPH,在 1 光束 1 頭類別中遠遠超過其他競爭對手。該機器結構緊湊,節省空間,提供廣泛的組件相容性和多功能性,使其成為高速模組組裝的下一代解決方案。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況

- 產業價值鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- COVID-19 對表面黏著技術市場的影響

第5章 市場動態

- 對技術小型化的需求日益增加

- 與其他技術相比, 基板上需要的孔更少

- 市場挑戰

- SMT 不適用於大型、高功率、高壓元件或經常受到機械應力的元件。

- 初始成本高且返工問題

第6章 市場細分

- 按組件

- 被動元件

- 電阻器

- 冷凝器

- 主動元件

- 電晶體

- 積體電路

- 被動元件

- 按最終用戶產業

- 消費性電子產品

- 車

- 工業電子

- 航太和國防

- 衛生保健

- 其他最終用戶產業

- 按地區

- 北美洲

- 歐洲

- 亞洲

- 澳洲和紐西蘭

- 拉丁美洲

- 中東和非洲

第7章 競爭格局

- 公司簡介

- Fuji Corporation

- Yamaha Motor Co. Ltd

- Mycronic AB

- ASMPT

- Panasonic Corporation

- Nordson Corporation

- Juki Corporation

- Hanwa Precision Machinery Co. Ltd

- Zhejiang Neoden Technology Co. Ltd

- Europlacer Limited

- Viscom SE

第8章投資分析

第9章 市場機會與未來趨勢

The Surface Mount Technology Market size is estimated at USD 6.61 billion in 2025, and is expected to reach USD 9.53 billion by 2030, at a CAGR of 7.6% during the forecast period (2025-2030).

Surface mount technology (SMT) is a method for constructing electronic circuits in which the components are mounted directly onto the surface of printed circuit boards (PCBs). This contrasts with older through-hole technology, where components are inserted into holes drilled into the PCB. Components used in SMT, known as SMDs, have small metal tabs or end caps that can be soldered directly onto the PCB surface. This allows for using smaller, lighter, and more components on a single PCB.

After the effect of the pandemic, the market for laptops and servers is witnessing a surge in demand. According to the India Electronics and Semiconductor Association (IESA), more data is stored on the cloud as work-from-home increases and more collaboration tools are deployed. A surge in demand is witnessed in the server, data centers, and computing segments. US-based Micron Technology also reported a more robust demand from data centers due to the remote-work economy, increased gaming, and e-commerce activity. Additionally, as per Cloudscene, as of March 2024, there are 5,381 data centers in the United States, the most of any country worldwide. A further 521 are in Germany, while 514 are in the United Kingdom.

Miniaturization of electronic components has made it possible to build small portable and handheld computer devices that can be carried anywhere. As a result, smaller, lighter devices with high processing capacity are available on the market. They are becoming more wearable since components can be easily embedded (for example, in clothing bags) and carried for long periods. Components are shrinking, putting new demands on the design of the PCBs they are mounted on. NCAB Group is firmly committed to IPC's efforts in defining standards for ultra-dense Ultra HDI PCBs and anticipates being able to provide them to clients in 2023.

Surface mount technology (SMT) has emerged as a pivotal element in modern electronics manufacturing, eclipsing traditional through-hole methods with its myriad benefits. A standout advantage of SMT lies in its drastic reduction of necessary PCB drilling. Manufacturers slash both time and costs by sidestepping the drilling process, a notable boon for intricate, high-density boards. This shift streamlines production and trims labor and material expenses, bolstering the overall cost-effectiveness of the manufacturing process.

Surface mount technology has revolutionized the electronics manufacturing industry by enabling the production of smaller, more efficient, and cost-effective electronic devices. However, despite its numerous advantages, SMT is unsuitable for all applications. SMT is unsuitable for high-power and high-voltage components, such as transformers and power circuitry. These components generate heat and carry high electric loads, which SMT is not designed to handle effectively.

According to the US Congressional Budget Office, defense spending in the United States is predicted to increase yearly until 2033. Defense outlays in the United States amounted to USD 746 billion in 2023. The forecast predicts an increase in defense outlays up to USD 1.1 trillion in 2033.

Surface Mount Technology (SMT) Market Trends

Consumer Electronics End-user Industry Segment is Expected to Hold Significant Market Share

- In the automotive industry, SMT is used in Electronic Control Units (ECU), dashboard displays, radar and camera modules, Battery Management Systems (BMS), safety assistance systems, and more. SMT has emerged as a pivotal manufacturing process in the automotive application. Renowned for its efficiency, precision, and reliability, SMT is crucial in bolstering various automotive electronic products, including advanced driver-assistance systems (ADAS), infotainment systems, and vehicle control systems.

- In modern cars, the on-board control system acts as the vehicle's 'brain,' overseeing and harmonizing the functions of its electronic components. The on-board control system is crucial in their seamless operation, from navigation to audio and air conditioning. Central to the reliability of these control systems is SMT technology. This technology enables the precise mounting of minuscule electronic components on circuit boards, ensuring the systems operate efficiently and reliably.

- The Engine Control Unit (ECU) is the automotive electronic system's nucleus, overseeing critical operations like engine performance, transmission, and braking. Surface-mount technology (SMT) is essential in assembling microchips, resistors, capacitors, and other surface-mounted components onto the ECU.

- Furthermore, Artificial Intelligence technology is poised to see increased adoption in the automotive sector. The precision and efficiency of Surface Mount Technology (SMT) in electronic assembly are set to bolster the production of AI chips and processors. Consequently, automotive electronic products will have enhanced autonomous decision-making abilities, advancing intelligent driving and vehicle automation.

- As highlighted by the IEA, the global automotive industry is undergoing a significant transformation, with potentially far-reaching implications for the energy sector. According to projections, the rise of electrification is anticipated to result in a daily elimination of the need for 5 million barrels of oil by 2030.

- The IEA's report also revealed a substantial increase in electric vehicle sales, with 3.5 million units sold in 2023 compared to 2022, marking a 35% growth. Notably, over 250,000 new registrations were recorded weekly, and over 250,000 new registrations were recorded weekly throughout the year. In 2023, electric vehicles accounted for approximately 18% of all vehicles sold, a significant increase from 2% five years ago and 14% in 2022. These trends indicate that solid growth is expected to persist as the electric vehicle market matures. Additionally, it was projected that 70% of the electric vehicle stock in 2023 would consist of battery electric vehicles.

Asia Pacific is Expected to Witness Fastest Growth

- Asia-Pacific, particularly countries like Japan, China, South Korea, Taiwan, and Southeast Asia, has become a global hub for electronics manufacturing. The region's robust manufacturing infrastructure, skilled labor force, and supportive government policies attract multinational corporations and promote the growth of local electronics industries. Demand for tablets, smartphones, and other electronic devices continues to grow, necessitating efficient and high-volume production capabilities by surface mount technology. The company projects that by implementing SMT (Surface Mount Technology) locally, the value addition will increase to 25% from the current 15%.

- For instance, in August 2023, the Indian government is actively engaging with global electronics firms to ramp up local value addition in products assembled in India, targeting a significant increase of 60-80% over the next five to ten years. To achieve this, the government is urging industries in India to adopt advanced production methods, like surface-mount technology (SMT) lines.

- Silicon Carbide (SiC) is increasingly in the spotlight for its high-temperature resilience, superior electrical conductivity, and remarkable energy efficiency. As the demand for electric vehicles (EVs), solar panels, and advanced power management rises with Industry 4.0, SiC manufacturing's significance has heightened. Wide Band Gap conductors are a natural fit given the imperative for minimal power consumption in these sectors.

- In February 2024, Continental Device India Limited (CDIL) took a significant step by inaugurating a new assembly line specifically for SiC Surface Mount Technology (SMT) components. This move positions CDIL as India's pioneer in SiC component manufacturing. With this enhancement, CDIL can now produce a range of auto-grade devices, such as SiC Schottky Diodes, SiC MOSFETs, Zeners, Rectifiers, and TVS Diodes, catering to both global and domestic markets.

- In April 2024, TDK Corporation introduced the B40910 series, a line of hybrid polymer capacitors designed to handle up to 4.6 A (at 100 kHz and +125 °C). These surface mount components boast impressively low ESR values of 17 mΩ and 22 mΩ at room temperature.

- Notably, unlike standard electrolytic capacitors with liquid electrolytes, the ESR of TDK's capacitors shows minimal variation with temperature. These compact components, measuring 10 x 10.2 mm or 10 x 12.5 mm (D x H), feature a rated voltage of 63 V and offer capacitances ranging from 82 µF to 120 µF. Thus, SMT manufacturers drive the need for the technology by integrating and innovating technologies. These efforts contribute to the widespread adoption and growth of surface mount technology (SMT) in various industries.

Surface Mount Technology (SMT) Industry Overview

Surface Mount Technology market is highly fragmented due to the presence of both global players and small and medium-sized enterprises. Some of the major players in the market are Fuji Corporation, Yamaha Motor Co. Ltd, Mycronic AB, ASMPT, and Panasonic Corporation. Players in the market are adopting partnerships and acquisitions to enhance their product offerings and gain competitive advantage.

March 2024 - Nordson Corporation introduced a new Latin America Tech Center based in Queretaro, Mexico, to allow manufacturers in the region to get timely feedback on the best fluid dispensing equipment for their assembly fluid, parts, substrates, and production requirements. The lab has a 3D printer, scales, and other measurement equipment to determine the correct fluid dispensing equipment for each customer's unique application requirements.

January 2024 - Yamaha Motor Co. Ltd announced the launch of YRM10, a surface mounter with the title of being the fastest in its class regarding mounting performance. With an impressive speed of 52,000 CPH, it outshines its competitors in the 1-Beam/1-Head category. This device is compact and space-saving and offers a range of component compatibility and versatility, making it a next-generation solution for high-speed modular assembly.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact of COVID-19 on the Surface Mount Technology Market

5 MARKET DYNAMICS

- 5.1 Rising Demand For Miniaturization of Technology

- 5.1.1 Fewer Holes Required to Drill on PCBs Compared to Other Technologies

- 5.2 Market Challenges

- 5.2.1 SMT is Unsuitable for Any Large, High-Power and High-Voltage Parts and Parts Undergoing Frequent Mechanical Stress

- 5.2.2 High Initial Cost and Rework Issues

6 MARKET SEGMENTATION

- 6.1 By Component

- 6.1.1 Passive Components

- 6.1.1.1 Resistors

- 6.1.1.2 Capacitors

- 6.1.2 Active Components

- 6.1.2.1 Transistors

- 6.1.2.2 Integrated Circuits

- 6.1.1 Passive Components

- 6.2 By End-user Industry

- 6.2.1 Consumer Electronics

- 6.2.2 Automotive

- 6.2.3 Industrial Electronics

- 6.2.4 Aerospace and Defense

- 6.2.5 Healthcare

- 6.2.6 Other End-user Industries

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Fuji Corporation

- 7.1.2 Yamaha Motor Co. Ltd

- 7.1.3 Mycronic AB

- 7.1.4 ASMPT

- 7.1.5 Panasonic Corporation

- 7.1.6 Nordson Corporation

- 7.1.7 Juki Corporation

- 7.1.8 Hanwa Precision Machinery Co. Ltd

- 7.1.9 Zhejiang Neoden Technology Co. Ltd

- 7.1.10 Europlacer Limited

- 7.1.11 Viscom SE

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

2025年表面黏著技術全球市場報告

2025年表面黏著技術全球市場報告 2025-2029年全球表面黏著技術(SMT)設備市場

2025-2029年全球表面黏著技術(SMT)設備市場 全球表面黏著技術(SMT) 設備市場:預測(2025-2030 年)

全球表面黏著技術(SMT) 設備市場:預測(2025-2030 年) 表面黏著技術市場規模、佔有率、成長分析,按設備、按組件、按服務、按最終用戶行業、按地區 - 行業預測,2024-2031 年

表面黏著技術市場規模、佔有率、成長分析,按設備、按組件、按服務、按最終用戶行業、按地區 - 行業預測,2024-2031 年 PCB 焊膏模板的全球市場 (2024-2028)

PCB 焊膏模板的全球市場 (2024-2028) 亞太地區 SMT 設備市場預測至 2031 年 - 區域分析 - 按組件、設備類型和最終用戶

亞太地區 SMT 設備市場預測至 2031 年 - 區域分析 - 按組件、設備類型和最終用戶 北美 SMT 設備市場預測至 2031 年 - 區域分析 - 按組件、設備類型和最終用戶

北美 SMT 設備市場預測至 2031 年 - 區域分析 - 按組件、設備類型和最終用戶 歐洲 SMT 設備市場預測至 2031 年 - 區域分析 - 按組件、設備類型和最終用戶

歐洲 SMT 設備市場預測至 2031 年 - 區域分析 - 按組件、設備類型和最終用戶 表面黏著技術市場:按設備、組件和最終用戶分類 - 全球預測 2025-2030 年

表面黏著技術市場:按設備、組件和最終用戶分類 - 全球預測 2025-2030 年 表面黏著技術開關市場:按類型、最終用戶分類 - 2025-2030 年全球預測

表面黏著技術開關市場:按類型、最終用戶分類 - 2025-2030 年全球預測