|

市場調查報告書

商品編碼

1692159

加速度和偏航率感測器:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)Acceleration And Yaw Rate Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

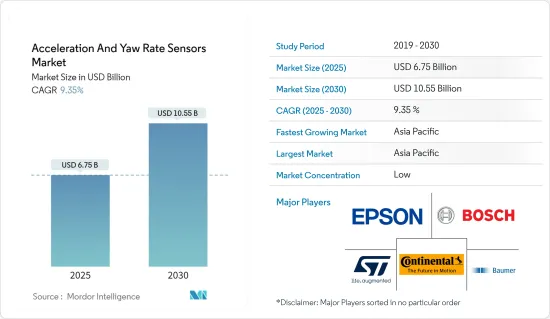

加速度和偏航率感測器市場規模預計在 2025 年為 67.5 億美元,預計到 2030 年將達到 105.5 億美元,預測期內(2025-2030 年)的複合年成長率為 9.35%。

偏航率感知器測量車輛繞其垂直軸的旋轉,同時測量垂直於行駛方向的加速度。偏航率以度/秒為單位進行測量。如果車輛在 2 秒內旋轉 900 次,則偏航率為 450。透過以電子方式評估測量值,感測器能夠區分正常轉彎和車輛的打滑運動。

主要亮點

- 偏航率感測器是一種陀螺儀裝置,可偵測車輛繞其垂直軸的角運動。輸出通常以度/秒或弧度/秒錶示。滑移角與偏航角速度有關,是車輛行駛方向與自然方向之間所形成的夾角。利用科氏效應來計算該值。科氏效應提供了精確的測量和結果。因此,預計它將保持其在市場上的主導地位。科氏加速度是透過微機械型振動元件上的微機械捕獲加速感應器測的。加速度與偏航率和振動速度的乘積成比例,並由電子方式維持。

- ADAS(進階駕駛輔助系統)和網路連線汽車技術日益普及,其動力源自於消費者對提高車輛安全性、保障性和舒適性的需求日益成長。 ADAS(高級駕駛輔助系統)透過整合感測器、攝影機和通訊系統來幫助改變駕駛體驗,以在各種情況下為駕駛員提供協助。

- 需求激增反映了人們對車輛的集體渴望,這些車輛優先考慮安全性,具有防撞和車道維持輔助等功能,並提供連接性以改善導航、提供即時資訊和個性化的舒適設定。這一趨勢凸顯了消費者對更聰明、更安全的駕駛體驗不斷變化的期望。

- 近年來,由於消費者應對氣候變遷和減少溫室氣體排放的願望,對替代燃料汽車的興趣和偏好顯著增加。這項轉變是朝著更永續和環保的交通途徑邁出的一大步。

- 在汽車產業,對先進感測器技術的需求正在激增,將汽車轉變為智慧系統。雖然已開發經濟體已經接受了這一發展,但新興經濟體的汽車感測器售後市場面臨獨特的挑戰,可能會阻礙加速度和偏航率感測器的成長。其中一個主要障礙是新興國家售後市場基礎設施不發達。與已開發市場不同,新興市場往往缺乏強大的專業感測器服務提供者網路,阻礙了提供優質的感測器更換和及時的維護服務。

加速度和偏航率感測器市場趨勢

乘用車佔很大市場佔有率

- 乘用車的不斷發展和對汽車安全功能的需求不斷成長,推動了對加速度和偏航率感測器的需求。這些感測器是汽車穩定控制的關鍵部件,即使在最具挑戰性的駕駛條件下也能提高安全性、安全性和控制力。這些感測器用於許多安全功能,例如安全氣囊、牽引力控制、ADAS(高級駕駛輔助系統)和防撞系統。

- 乘用車中的偏航率感知器用於測量車輛的轉速,通常稱為偏航率。這些資料對於電子穩定控制 (ESC) 和牽引力控制等穩定控制系統至關重要,並構成其基礎。它還可以幫助診斷車輛性能問題並向駕駛輔助系統提供資料。

- 特別是小型乘用車,由於自動駕駛和汽車電氣化等趨勢的引入,市場預計將經歷高速成長。為了滿足日益成長的需求,汽車製造商正集中投資並推出新車型,以擴大其影響力並提高市場競爭力。根據加拿大豐業銀行預測,2023年亞洲乘用車銷售量將達到約3,650萬輛,北美乘用車銷售量將達1,830萬輛。

- 2023年5月,比亞迪宣佈在歐洲建立新的乘用車工廠。作為其成長策略的一部分,該公司還計劃在泰國建立一家乘用車廠。

- 同樣,鈴木汽車公司在2023年10月表示,其目標是到2030年在其最大的單一市場印度銷售300萬輛乘用車,並重申未來十年將其在印度的產能增加一倍至400萬輛的計劃。

- 此外,世界各國政府和消費者都在增加對電動車的支出,地方政府也提供購買補貼和免稅以鼓勵人們使用電動車。此外,各國政府也正在加速推動電氣化計劃,加大對充電基礎設施的投入,邁向全電動化未來,進而支持市場成長。

亞太地區可望佔據主要市場佔有率

- 近年來,中國汽車工業取得了長足的成長和發展。中國汽車產業擁有全球最大的電動車市場和產業,擁有強大的供應鏈和大量的研發活動。中國政府將汽車產業,包括汽車零件產業,視為國家重點產業之一。中央政府預計,到 2025 年,中國的汽車產量將達到 3,500 萬輛。中國最近指示汽車製造商到 2030 年,電動車 (EV) 的銷量比傳統汽車多 40%。隨著汽車產業的這些進步,研究市場預計將會成長。

- 此外,隨著工業 4.0 和物聯網的到來,製造業發生了巨大轉變,要求企業採用敏捷、智慧和創新的方式來推動生產,利用技術透過自動化補充和增強人力,並減少因製程故障而導致的工業事故。中國汽車產業大力採用先進製造技術,以提高產量、改善產品組裝和成品水準並降低整體成本。預計中國汽車行業的成長將支持該市場的成長。

- 此外,根據中國工業協會(CAAM)的數據,2022年中國將生產約2,384萬輛乘用車和319萬輛商用車。

- 根據 IBEF 的汽車產業報告,印度的中產階級正在不斷壯大,而且年輕人口占很大比例,這意味著二輪車在數量上佔據市場主導地位。此外,企業對開拓農村市場的興趣日益濃厚,進一步推動了該產業的成長。物流和客運行業的成長正在推動商用車的需求。預計未來市場的成長將受到汽車電氣化等新興趨勢的推動,尤其是小型車和三輪車的電氣化。

- 印度是世界上最大的曳引機製造商、第二大客車製造商和第三大重型卡車製造商,在全球重型汽車市場佔有重要地位。印度22會計年度的汽車產量約為2,293萬輛。

- 印度也是一個主要的汽車出口國,預計預測期內出口將大幅成長。此外,印度政府推出的多項舉措,如報廢政策、2026汽車任務計畫、與生產掛鉤的獎勵計畫等,可能會使印度成為二輪車和四輪車市場的領導者。

加速度和偏航率感測器市場概況

加速和偏航率感測器市場高度分散,主要企業包括 Epson Europe Electronics Gmbh(Seiko Epson Corp.)、Bosch Sensortec Gmbh(羅伯特博世公司)、義法半導體公司、大陸集團和堡盟集團。市場參與者正在採取合作和收購等策略來加強其產品供應並獲得永續的競爭優勢。

- 2023 年 9 月 - 在 Intergeo 2023 上,Silicon Sensing 團隊將展示其最新系列基於堅固、高性能慣性和電子機械系統 (MEMS) 的感測器。此外,我們也討論了即將推向市場的新一代技術。這些基於 MEMS 的尖端系統和感測器提供的性能等級可與關鍵領域的更大、更重、更昂貴的光纖陀螺儀 (FOG) 裝置相媲美。

- 2023 年 8 月 - DTS 將被獎勵南加州最佳職場場所。這項享有盛譽的獎項認可了 DTS 為營造每個人都發揮重要作用的協作環境所做的不懈奉獻和努力。此外,這項成就強化了 DTS 的核心價值觀,即開發為社會帶來價值的突破性產品、培養團隊成員之間的友愛精神、促進個人成長並營造積極的氛圍。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

- 產業供應鏈分析

第5章 市場動態

- 市場促進因素

- 消費者對車輛安全性、保障性和舒適性的需求不斷成長

- 消費者越來越傾向於使用替代燃料汽車以減少溫室排放

- 市場限制

- 新興國家汽車感測器售後市場尚未開發

第6章 市場細分

- 按類型

- 壓電型

- 微機械型

- 按應用

- 航太

- 車

- 搭乘用車

- 輕型商用車

- 重型商用車

- 按地區

- 北美洲

- 歐洲

- 亞洲

- 澳洲和紐西蘭

- 拉丁美洲

- 中東和非洲

第7章 競爭格局

- 公司簡介

- Epson Europe Electronics GmbH(Seiko Epson Corporation)

- Bosch Sensortec GmbH(Robert Bosch GmbH)

- STMicroelectronics NV

- Continental AG

- Baumer Holding AG

- DIS Sensors BV

- Silicon Sensing Systems Ltd

- Xsens Technologies BV

- Diversified Technical Systems Inc.

- MEMSIC Semiconductor(Tianjin)Co. Ltd

- CTS Corporation

第8章投資分析

第9章:市場的未來

The Acceleration And Yaw Rate Sensors Market size is estimated at USD 6.75 billion in 2025, and is expected to reach USD 10.55 billion by 2030, at a CAGR of 9.35% during the forecast period (2025-2030).

A yaw rate sensor measures the vehicle's rotation around its vertical axis while measuring the acceleration at right angles to the driving direction at the same time. The yaw rate is measured in degrees per second. If a vehicle makes a 900 turn in two seconds, it will have a yaw rate of 450. The sensor can differentiate between normal cornering and vehicle skidding movements by electronically evaluating the measured values.

Key Highlights

- A yaw rate sensor is a gyroscope gadget that detects a vehicle's angular motion around its vertical axis. The output is usually expressed in degrees per second or radians per second. The slip angle, related to the yaw rate, is the angle formed between the vehicle's driving and natural direction. The Coriolis effect is used to calculate this value. The Coriolis effect provides precise readings and results. Thus, it is projected to maintain its market dominance. Coriolis acceleration is sensed through a micromechanical capture acceleration sensor on the oscillating element in the micromechanical type. The acceleration is proportional to the product of the yaw rate and the oscillation speed, which is maintained electronically.

- The growing popularity of advanced driver assistance systems (ADAS) and connected vehicle technology is propelled by heightened consumer demand for enhanced safety, security, and comfort in automobiles. As these technologies advance, they contribute to a transformative driving experience by integrating sensors, cameras, and communication systems to assist drivers in various situations.

- The surge in demand reflects a collective desire for vehicles that prioritize safety with features like collision avoidance and lane-keeping assistance and offer connectivity for improved navigation, real-time information, and personalized comfort settings. This trend underscores the evolving expectations of consumers who seek a more smart and secure driving environment.

- In recent years, there has been a notable surge in consumer interest and preference for alternative fuel vehicles, driven by a collective desire to combat climate change and reduce greenhouse gas (GHG) emissions. The shift marks a significant step toward a more sustainable and eco-friendly transportation landscape.

- The automotive industry has witnessed a surge in the demand for advanced sensor technologies, transforming vehicles into smart systems. While developed economies have embraced this evolution, the aftermarket for automotive sensors in emerging economies faces unique challenges that may impede the growth of acceleration and yaw rate sensors. One of the primary hurdles lies in the underdeveloped nature of the aftermarket infrastructure in emerging economies. Unlike their developed counterparts, these markets often lack a robust network of specialized sensor service providers, hindering the availability of quality sensor replacements and timely maintenance services.

Acceleration And Yaw Rate Sensors Market Trends

Passenger Cars to Hold Major Market Share

- The growing developments of passenger vehicles and rising demand for safety features in cars have fueled the demand for acceleration and yaw rate sensors. These sensors are key components in a vehicle's stability control to provide increased security, safety, and control even in the most difficult driving conditions. These sensors are used in numerous safety features such as airbags, traction control, advanced driver assistance systems (ADAS), collision avoidance systems, and others.

- The yaw rate sensor in passenger cars is used to measure the rotational speed of a vehicle, often referred to as the yaw rate. This data is essential for stability control systems, such as electronic stability control (ESC) and traction control, as it provides the basis for their operation. They are also helpful in diagnosing vehicle performance issues and providing data for driver assistance systems.

- The market is expected to witness high growth due to the introduction of trends such as autonomous driving and the electrification of vehicles, particularly in small passenger automobiles. To meet this growing demand, various automaker players focus on investing and introducing new vehicle models to expand their footprint and gain a competitive edge in the market. According to Scotiabank, in Asia, passenger car sales reached around 36.5 million units in 2023, and in North America, it reached 18.3 million units.

- In May 2023, BYD announced the establishment of a new passenger vehicle plant in Europe. The company is also planning to construct a vehicle plant in Thailand as a part of its growth strategy.

- Similarly, in October 2023, Suzuki Motor Corporation announced that it is targeting the sales of 3 million passenger vehicles in India, its single-largest market, by 2030, reiterating its plans to double its manufacturing capacity in the country to 4 million units over the next decade.

- Furthermore, governments and consumers around the globe are increasing their spending on electric cars, and regional governments are also providing purchase subsidies and tax waivers to promote the adoption of electric vehicles. Various governments are also spending on charging infrastructure to accelerate electrification plans and aiming for a fully electric future, thus supporting the market's growth.

Asia-Pacific is Expected to Hold Significant Market Share

- The automotive industry in China has experienced significant growth and development in recent years. The Chinese industry has the largest EV market and industry in the world, with a robust supply chain and significant research and development activities. The Chinese government views its automotive industry, including the auto parts sector, as one of the prominent industries. The central government expects China's automobile output to reach 35 million units by 2025. China recently instructed automakers to sell 40% more electric vehicles (EVs) than conventional vehicles by 2030. As a result of these advancements in the automotive industry, there is likely to be growth in the market studied.

- Moreover, massive shifts in manufacturing due to Industry 4.0 and the acceptance of IoT require enterprises to adopt agile, smarter, and innovative ways to advance production, with technologies that complement and augment human labor with automation and reduce industrial accidents caused by process failure. The automotive sector in China has been a significant adopter of advanced manufacturing techniques for increasing their production output, achieving higher levels of fit and finish for their products, and reducing overall costs. The growing automotive sector in China is anticipated to support the growth of the market studied.

- Further, according to the China Association of Automobile Manufacturers(CAAM), in 2022, approximately 23.84 million passenger cars and 3.19 million commercial vehicles were produced in China.

- According to the IBEF automobile industry report, the two-wheelers segment dominates the market in terms of volume due to a growing middle-class population, and a considerable percentage of India's population is young. Moreover, the rising interest of companies in examining the rural markets is further aiding the sector's growth. The growing logistics and passenger transportation industries are driving the demand for commercial vehicles. Future market growth is expected to be fueled by new trends, including the electrification of vehicles, particularly small passenger automobiles and three-wheelers.

- India also enjoys a powerful position in the global heavy vehicles market as it is the largest tractor manufacturer, second-largest bus producer, and third-largest heavy truck manufacturer globally. India's annual production of automobiles in FY22 was approximately 22.93 million vehicles.

- India is also a major auto exporter and has substantial export growth expectations for the forecast period. Additionally, several initiatives by the Government of India, like the scrappage policy, Automotive Mission Plan 2026, and production-linked incentive schemes in the Indian market, are likely to make India a prominent player in the two-wheeler and four-wheeler markets.

Acceleration And Yaw Rate Sensors Market Overview

The acceleration and yaw rate sensors market is highly fragmented, with the presence of major players like Epson Europe Electronics Gmbh (Seiko Epson Corporation), Bosch Sensortec Gmbh (Robert Bosch Gmbh), STMicroelectronics NV, Continental AG, and Baumer Group. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- September 2023 - During Intergeo 2023, the Silicon Sensing team showcased the latest lineup of robust and high-performing inertial systems and a variety of sensors based on micro-electro-mechanical systems (MEMS). Additionally, they engaged in discussions regarding the imminent market-ready technology of a new generation. These cutting-edge MEMS-based systems and sensors provide comparable performance levels to larger, heavier, and more expensive fiber optic gyroscope (FOG) units in crucial domains.

- August 2023 - DTS received the accolade of being acknowledged as one of the top workplaces in Southern California. This acknowledgment serves as a testament to DTS's unwavering dedication to fostering a collaborative environment where every individual has played a significant role in achieving this esteemed recognition. Furthermore, this achievement reinforces DTS's core principles of developing groundbreaking products that bring value to society, nurturing a sense of camaraderie among team members, promoting personal growth, and cultivating a positive atmosphere.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Degree of Competition

- 4.3 Industry Supply Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Surging Consumer Demand for Vehicle Safety, Security, and Comfort

- 5.1.2 Growing Inclination of Consumers Toward Alternative Fuel Vehicles to Reduce GHG Emissions

- 5.2 Market Restraints

- 5.2.1 Underdeveloped Aftermarket for Automotive Sensors in Emerging Economies

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Piezoelectric Type

- 6.1.2 Micromechanical Type

- 6.2 By Application

- 6.2.1 Aerospace

- 6.2.2 Automotive

- 6.2.2.1 Passenger Cars

- 6.2.2.2 Light Commercial Vehicles

- 6.2.2.3 Heavy Commercial Vehicles

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Epson Europe Electronics GmbH (Seiko Epson Corporation)

- 7.1.2 Bosch Sensortec GmbH (Robert Bosch GmbH)

- 7.1.3 STMicroelectronics NV

- 7.1.4 Continental AG

- 7.1.5 Baumer Holding AG

- 7.1.6 DIS Sensors BV

- 7.1.7 Silicon Sensing Systems Ltd

- 7.1.8 Xsens Technologies BV

- 7.1.9 Diversified Technical Systems Inc.

- 7.1.10 MEMSIC Semiconductor (Tianjin) Co. Ltd

- 7.1.11 CTS Corporation

8 INVESTMENTS ANALYSIS

9 FUTURE OF THE MARKET

加速計市場:按類型、尺寸、產業分類 - 2025-2030 年全球預測

加速計市場:按類型、尺寸、產業分類 - 2025-2030 年全球預測 加速計市場規模、佔有率、成長分析、按產品、按尺寸、按最終用途行業、按地區 - 行業預測,2024-2031 年

加速計市場規模、佔有率、成長分析、按產品、按尺寸、按最終用途行業、按地區 - 行業預測,2024-2031 年 2024-2028年全球加速計市場2024-2032 年按類型、軸類型、應用和地區分類的高階加速度計市場報告

2024-2028年全球加速計市場2024-2032 年按類型、軸類型、應用和地區分類的高階加速度計市場報告 全球加速度計市場規模:按類型、軸、最終用戶產業、地區、範圍和預測

全球加速度計市場規模:按類型、軸、最終用戶產業、地區、範圍和預測 鐵路用MEMS加速感應器的全球市場:2024年

鐵路用MEMS加速感應器的全球市場:2024年 高階加速度計 - 市場佔有率分析、產業趨勢與統計、成長預測(2024 - 2029)

高階加速度計 - 市場佔有率分析、產業趨勢與統計、成長預測(2024 - 2029) 加速度計市場(類型:交流響應和直流響應;軸:1 軸、2 軸和 3 軸)- 2023-2031 年全球行業分析、規模、佔有率、成長、趨勢和預測

加速度計市場(類型:交流響應和直流響應;軸:1 軸、2 軸和 3 軸)- 2023-2031 年全球行業分析、規模、佔有率、成長、趨勢和預測