|

市場調查報告書

商品編碼

1555073

回顧2024年第二季資本支出及各細分領域展望:催生AI泡沫-企業獲利穩定,Webscale及業者中性資本支出分別較去年同期成長51%及19% 同時,電信企業的資本投資持續下降。Review of 2Q24 Capex and Outlook for all Segments - GenAI Bubble: Capex for Webscale and Carrier-neutral Sectors Climbs by 51% and 19% YoY in 2Q24, respectively, Telco Capex is still on the Decline as Companies Stabilize Profitability |

||||||

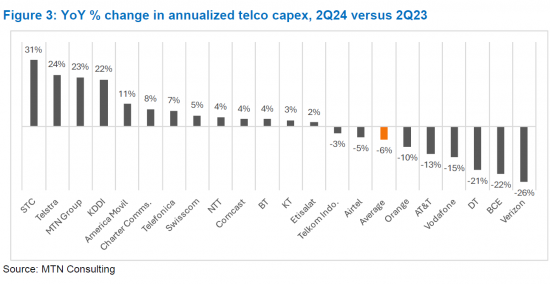

2024年第二季網路規模業者的資本投資年增超過50%,業者中立業者的資本投資年增約20%;正在下降。電信業者的資本支出連續幾季較去年同期下降5-10%。考慮到 5G 推出後需要減少支出以及電信業的扁平化性質,營運商的低迷並不令人震驚。人們早就預測AWS、Azure和GCP等雲端供應商最終將在營運商網路中發揮更大的作用。隨著雲端供應商將其解決方案與 Amdocs 和愛立信等傳統通訊供應商合併,這一點開始成為現實。兩年前,AWS、Azure 和 GCP 向營運商的銷售額合計約為 10 億美元,但現在已超過 20 億美元,有助於減少資本支出。

本報告概述了截至 2024 年 6 月電信業者、網路規模營運商和營運商中立營運商三個細分市場的資本投資表現,以及主要公司的全年展望。

視覺

調查範圍

刊載組織

|

|

目錄

摘要

主要經營者的設備投資實際成果及預測

- 2024 年第二季 Webscale 資本支出:年增 51%

- 2024 年第二季營運商中性資本支出:年增 19%

- 2024年第二季電信公司資本投資:年減5-10%

附錄

圖表:

This brief report reviews actual capex through June 2024 and the full-year outlook for key companies in three segments of communications network operators: telco, webscale and carrier-neutral.

VISUALS

MTN Consulting tracks communications network operator spending (capex) closely. Each quarter, we publish detailed Excel reviews for the telco & webscale markets. For carrier-neutral, we update our database informally each quarter and publish a detailed review once a year. For all three, we usually publish a market forecast twice a year: around December and around July. This year, our July update was postponed as we believed the market was too volatile to make publication of a new forecast feasible. That turned out to be a good decision. For example, interest rates now appear to be set to fall, which will support more telco capex and also entice some market consolidation (e.g. Verizon-Frontier). That gives more support to the presumption that telco spending will change directions after 2H24. Also, there is more support now for our thesis that GenAI is overly hyped and cannot sustain continued capex spikes.

We now plan to release an update around the end of 3Q24. As part of the update process, we expect to publish a number of shorter reports reviewing various aspects of the forecast. The starting point is a review of actual capex through 2Q24 and the latest guidance from key operators. That is the purpose of this report. As discussed below, webscale capex surged by over 50% YoY in 2Q24, carrier-neutral capex grew by about 20% YoY, but telco capex remains on the decline. That's where it has been for several straight quarters, recording YoY declines in the 5-10% range. The telco weakness is not a shock given the need to ramp down spending post 5G rollouts, and given the flat nature of the telecom industry. Moreover, we have long expected the cloud providers AWS, Azure and GCP to play a much larger role in telco networks, eventually. That is starting to happen as the cloud providers blend their solutions with more traditional telco vendors like Amdocs and Ericsson. For AWS, Azure and GCP, their combined sales to telcos now exceed $2B per quarter, from about $1B per quarter two years ago. This enables capex reductions.

Other topics we plan to address in the coming weeks include: labor costs & automation; data center spending & supply chain dynamics; shifting vendor landscape & implications for spending patterns; and wildcard topics, such as China starting a war, Trump winning, and India emerging as real player in tech supply chains.

COVERAGE:

Organizations mentioned:

|

|

Table of Contents

Summary

Capex results & outlook for key operators

- Webscale capex climbs 51% YoY in 2Q24

- Carrier-neutral capex up by 19% YoY in 2Q24

- Telco capex continued declining at a 5-10% YoY rate in 2Q24

Appendix

Figures:

- Figure 1: YoY % change in annualized capex for key webscalers, 2Q24

- Figure 2: Annualized capex for key CNNOs in 2Q24, YoY % change

- Figure 3: YoY % change in annualized telco capex, 2Q24 versus 2Q23

2026年全球媒體生成式人工智慧市場報告2026年全球採購領域生成式人工智慧市場報告2026年擴增實境生成式人工智慧全球市場報告2026年生成式人工智慧全球市場報告2026年人力資源領域生成式人工智慧(AI)全球市場報告2026年全球生成式人工智慧媒體軟體市場報告

2026年全球媒體生成式人工智慧市場報告2026年全球採購領域生成式人工智慧市場報告2026年擴增實境生成式人工智慧全球市場報告2026年生成式人工智慧全球市場報告2026年人力資源領域生成式人工智慧(AI)全球市場報告2026年全球生成式人工智慧媒體軟體市場報告 3D建模類型AIGC市場:按組件、技術、輸入方法、應用和部署方式分類,全球預測,2026-2032年基於影像的AIGC市場:按影像類型、模型類型、部署方式、應用領域和最終用戶分類,全球預測,2026-2032年

3D建模類型AIGC市場:按組件、技術、輸入方法、應用和部署方式分類,全球預測,2026-2032年基於影像的AIGC市場:按影像類型、模型類型、部署方式、應用領域和最終用戶分類,全球預測,2026-2032年 生成式人工智慧市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、最終用戶、部署類型和功能分類

生成式人工智慧市場分析及預測(至2035年):按類型、產品類型、服務、技術、組件、應用、最終用戶、部署類型和功能分類 AI在3D資產生成和紋理繪製領域的市場規模、佔有率和預測:依資產類型、AI模型、整合方式和最終用戶(遊戲、元宇宙、視覺特效)劃分 - 全球預測(2026-2036)

AI在3D資產生成和紋理繪製領域的市場規模、佔有率和預測:依資產類型、AI模型、整合方式和最終用戶(遊戲、元宇宙、視覺特效)劃分 - 全球預測(2026-2036)