|

市場調查報告書

商品編碼

1562736

儘管缺乏收入機會和法律挑戰,生成式人工智慧席捲了世界:資料中心淘金熱會結束嗎?這股熱情將走向何方?資料中心需求將會發生什麼變化?Will the Data Center Gold Rush Come to an End? Generative AI has Taken the World by Storm, despite the Lack of Proven Revenue Opportunities and Huge Legal Challenges, Where Does the Hype Head Next, and What Happens to Data Center Demand? |

|||||||

本報告為我們的資本支出預測提供了支援數據,重點關注資料中心需求以及生成式人工智慧在刺激投資增加方面的作用,特別是在網路規模領域。

視覺

生成式人工智慧的所有演變都吸引了投資界的注意。人們認為,生成式人工智慧是千載難逢的機會,早期的獲勝者有可能在數十年中佔據主導地位。這種情況以前在其他創新中也曾發生過,興奮感通常會消失。生成式人工智慧現在走向何方?生成式人工智慧是一個泡沫,我們正面臨著一場艱苦的戰鬥來普及它。生成式人工智慧工具很有趣,而且有多種應用,但它們面臨嚴峻的法律挑戰,而且還沒有殺手級應用。

上週,宣佈設立一支基金,將籌集和管理高達 1000 億美元的人工智慧資料中心和相關能源投資。新基金GAIIP(全球人工智慧基礎設施投資合作夥伴關係)是微軟與三個專注於人工智慧基礎設施的金融機構之間的合作夥伴關係:貝萊德、全球基礎設施合作夥伴(GIP)和總部位於阿布達比的MGX。 這項新的合作關係增加了近年來宣布的一系列由私募股權主導的資料中心投資。自 2022 年底 ChatGPT 發布以來,這些投資激增。甚至在 2022 年底/2023 年初推出生成式人工智慧之前,旨在籌集資金和管理數位基礎設施投資的新投資工具就已經出現。生成式人工智慧將於 2024 年開始流行,並且正在加速發展。

由於生成式人工智慧熱潮導致資料中心支出激增並不是什麼新聞。即將推出的新資料中心更大、更好、能耗更高。新的金融工具不斷湧現,為這些新的基礎設施提供融資。這使得人們更加意識到計算機,尤其是現在 GPU 伺服器占主導地位的網路規模資料中心中普遍存在的巨大計算機集群,實際上消耗了多少電力。自 2019 年以來,網路規模產業的能源消耗翻了一番,過去兩年每年增長 15%。更重要的是,自從新冠疫情以來,網路規模產業的能源密集度變得更高,而不是更少。 2021年,每百萬美元收入消耗59兆瓦時的能源,這一數字到2022年將增加到65兆瓦時,到2023年將增加到70兆瓦時。這是值得注意的,因為網路擴展者應該能夠利用其規模並從規模中獲得效率。由於對生成式人工智慧的大力投入,能源強度將持續上升。無法獲得足夠的可負擔的可再生能源是產生人工智慧市場面臨的眾多挑戰之一,但儘管存在這些挑戰,資料中心支出仍將繼續推動網路規模市場在幾個季度內保持高位。推進這些新人工智慧模型的競賽正在進行中,並且有一種觀點認為,早期的獲勝者將擁有多年的優勢。因此,存在著對熟練開發商、工具、能源能力和土地的競爭。

目標範圍

提及的組織

|

|

目錄

摘要

簡介

分析

- 2024 年上半年網路規模資本支出激增,生成式人工智慧推動強勁前景

- 四大網路縮放器引領資料中心發展

- 雲端現已成為主要收入來源

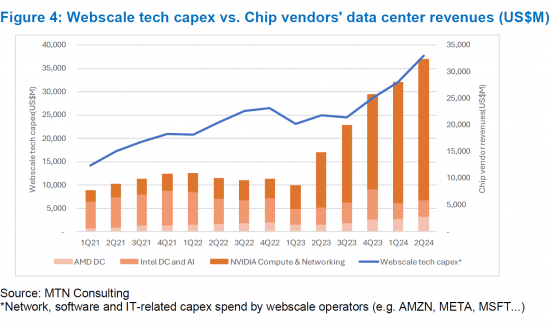

- 網路規模技術的資本支出與晶片供應商的資料中心收入密切相關

- 人們對網路規模市場的能源消耗趨勢感到擔憂。

- 世界政治與中美貿易戰的干預

展望

附錄

This short brief is focused on data center demand and the role of generative AI in spurring an uptick in investments, particularly in the webscale sector. This brief supports our pending capex forecast update.

VISUALS

Generative AI (GenAI) in all its evolving flavors has captured the attention of the 'investment community' - there is a feeling that GenAI is a once in a lifetime opportunity where the early winners have the potential to dominate for decades. This has happened before with other technology breakthroughs and the hype usually dies down. Where is it going now? There is a strong argument that GenAI is a bubble which faces an uphill battle towards widespread adoption. The tools are interesting and do have a range of applications, but they also face serious legal challenges and lack a killer app. There's also support for the idea that the "smart money" already believes this but doesn't care, due to confidence in being able to sell others on the hype.

Last week a fund was announced to raise and manage up to $100 billion (B) in funding for AI data centers and related energy investments. The new fund, Global AI Infrastructure Investment Partnership (GAIIP), is a partnership between Microsoft and three financial institutions betting big on AI infrastructure: BlackRock, Global Infrastructure Partners (GIP), and Abu Dhabi-based MGX. The new partnership adds to a long list of private equity-driven investments in data centers announced over the last few years. These investments have spiked since late 2022, when ChatGPT was released. Even prior to GenAI rolling out in late 2022/early 2023, new investment vehicles were emerging to raise capital and manage investments in digital infrastructure. With GenAI gaining steam in 2024, that has accelerated.

It's not news that data center spending is surging thanks to widespread enthusiasm for GenAI. The announcements keep on coming: new data centers, bigger and better, consuming more power. New financial vehicles arising to fund all this new infrastructure. With this, a more widespread appreciation of how power-hungry computers actually are - especially the massive clusters of computers prevailing in webscale data centers, now dominated by GPU servers. Energy consumption has doubled in the webscale sector since 2019, growing 15% per year in each of the last two years. More important, since COVID, the webscale sector has become more energy intensive, not less; in 2021, 59 MWh of energy was consumed per US$1M in revenues. That figure grew to 65 in 2022 and 70 in 2023. This is notable, as webscalers are supposed to be able to exploit their size in order to get efficiencies from scale; it's going the opposite direction with data center power consumption. And energy intensity is likely to keep rising with big commitments to GenAI. Inadequate access to affordable, renewable power is one of many challenges faced by the GenAI market. Despite these challenges, data center spend is likely to remain elevated for a few quarters, driven by the webscale market. There is a race underway to train and evolve these new AI models. There is a feeling that the early winners will be able to preserve their advantage for many years. Hence there is a land grab underway: for skilled developers, for tools, for energy capacity, and for land.

Coverage

Organizations mentioned:

|

|

Table of Contents

Summary

Introduction

Analysis

- Webscale capex surged in 1H24 and GenAI is driving strong outlook

- Top four webscalers drive data center developments

- Cloud may have started as a side business but it's now big money

- Webscale tech capex closely tied to chip vendors' data center revenues

- Energy consumption trends in webscale market are concerning

- Global politics and the US-China trade war will intervene

Outlook

Appendix

Figures:

- Figure 1: Webscale sector capex and free cash flow margin trends through 2Q24

- Figure 2: Big data center spenders (webscale and CNNO) - annualized capex and YoY % change

- Figure 3: Cloud service revenues as a percent of total for key webscalers, 2018-24

- Figure 4: Webscale tech capex vs. Chip vendors' data center revenues (US$M)

- Figure 5: Energy intensity (MWh of energy consumption per $M in revenue)

全球配電中心市場:依類型、應用和地區劃分 - 市場規模、行業趨勢、機會分析和預測(2025-2033 年)

全球配電中心市場:依類型、應用和地區劃分 - 市場規模、行業趨勢、機會分析和預測(2025-2033 年) 資料中心設備及基礎設施市場:2025-2030

資料中心設備及基礎設施市場:2025-2030 高階主管簡報:2025 年第四季

高階主管簡報:2025 年第四季 AI資料中心的設備投資的明細和未來預測

AI資料中心的設備投資的明細和未來預測 全球資料中心服務市場按服務類型、設施服務、IT 服務、專業諮詢與認證、層級類型、資料中心規模與容量、資料中心類型、企業資料中心和地區分類 - 預測至 2030 年

全球資料中心服務市場按服務類型、設施服務、IT 服務、專業諮詢與認證、層級類型、資料中心規模與容量、資料中心類型、企業資料中心和地區分類 - 預測至 2030 年 資料中心資產管理市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)

資料中心資產管理市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年) 全球企業 IT 資產處置市場規模、佔有率和行業分析報告:2025 年至 2032 年按資產類型、服務、行業和地區分類的展望和預測

全球企業 IT 資產處置市場規模、佔有率和行業分析報告:2025 年至 2032 年按資產類型、服務、行業和地區分類的展望和預測 資料中心市場:按組件、資料中心類型、層級、冷卻類型、電源、最終用戶和組織規模分類 - 全球預測,2025-2032 年

資料中心市場:按組件、資料中心類型、層級、冷卻類型、電源、最終用戶和組織規模分類 - 全球預測,2025-2032 年 2025年全球託管資料中心服務市場報告2025年全球資料中心IT資產處置市場報告

2025年全球託管資料中心服務市場報告2025年全球資料中心IT資產處置市場報告