|

市場調查報告書

商品編碼

1585175

胰島素幫浦市場:產業趨勢與全球預測(~2035)-按幫浦類型、自動化程度、電池類型、目標糖尿病類型、通路、地區Insulin Pump Market: Industry Trends and Global Forecasts, till 2035 - Distribution by Type of Pump, Degree of Automation, Type of Battery, Type of Diabetes Targeted, Distribution Channel and Key Geography |

||||||

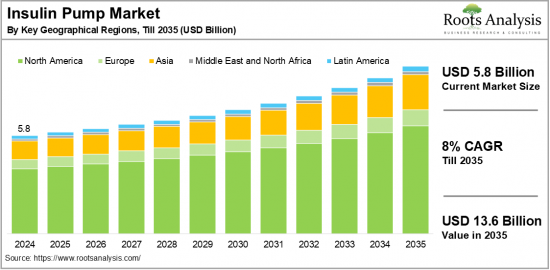

胰島素幫浦市場規模預計到 2024 年將達到 58 億美元,並且預計到 2035 年的預測期間複合年增長率將達到 8%。

根據世界衛生組織 (WHO) 統計,目前全球有超過 4.2 億人患有糖尿病。糖尿病已成為失明、心臟病、腎衰竭、下肢截肢和中風等嚴重健康問題的主要原因。糖尿病的傳統治療方法包括口服藥物、注射胰島素和改變生活方式。然而,涉及每日多次注射的傳統糖尿病管理方法通常不舒服、不方便,且患者治療效果不佳。這引起了有關藥物傳遞的一些擔憂,包括劑量不準確、針刺傷害的風險以及注射部位胰島素吸收的變異性。

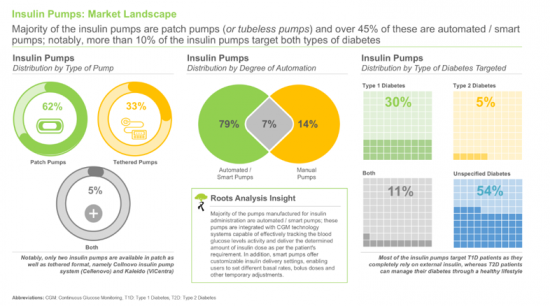

考慮到與糖尿病藥物輸送裝置相關的局限性,胰島素幫浦已成為胰島素給藥的首選。這些緊湊、輕巧的設備旨在根據患者的需求連續或間歇地輸送胰島素,為糖尿病管理提供精確且適應性強的方法。值得注意的是,大多數胰島素幫浦可以戴在腰帶上,並由一根管子組成,該管將幫浦連接到放置在皮下脂肪組織中的輸液器。有些胰島素幫浦可以作為貼片直接戴在皮膚上,讓患者可以自由活動。這些設備具有許多優點,包括精確且可調節的胰島素劑量、可自訂的基礎劑量、進餐時推注、提高舒適度以及降低低血糖和高血糖的風險,有助於提高生活品質。此外,胰島素幫浦由一個簡單的給藥過程組成,已被證明可以改善家庭自我藥療,並減少對醫療保健提供者註射胰島素的依賴。

該報告研究了全球胰島素幫浦市場,並提供了市場概況,包括幫浦類型、自動化程度、電池類型、目標糖尿病類型、分銷管道、地區和市場趨勢的趨勢。

目錄

第1章 前言

第2章 研究方法

第3章市場動態

第4章. 經濟和其他專案特定考慮因素

第5章 執行摘要

第6章 簡介

- 章節概述

- 糖尿病概述

- 胰島素泵

- 未來展望

第7章胰島素幫浦:市場情勢

- 章節概述

- 胰島素幫浦:市場狀況

- 胰島素幫浦:製造商列表

第8章 公司簡介:北美胰島素幫浦製造商

- 章節概述

- Beta Bionics

- Insulet

- MannKind

- Medtronic

- Tandem Diabetes Care

第9章公司簡介:歐洲胰島素幫浦製造商

- 章節概述

- CeQur

- Roche

- ViCentra

- Ypsomed

第10章公司簡介:亞太地區胰島素幫浦製造商

- 章節概述

- EOFlow

- Medtrum Technologies

- MicroPort

- Microtech Medical

- SOOIL Development

- Terumo

第11章 專利分析

第12章市場影響分析

第13章 全球胰島素幫浦市場

第14章胰島素幫浦市場(按幫浦類型)

第15章胰島素幫浦市場(依自動化程度)

第16章胰島素幫浦市場(以電池類型)

第17章胰島素幫浦市場(依目標糖尿病類型)

第18章胰島素幫浦市場(依通路)

第19章胰島素幫浦市場(按地區)

第20章 結論

第21章 高階主管洞察

第22章附錄一:表格數據

第23章 附錄二:公司與組織名單

The Insulin Pump Market is expected to reach USD 5.8 billion in 2024 and is anticipated to grow at a CAGR of 8% during the forecast period till 2035.

According to the World Health Organization, over 420 million people are currently suffering from diabetes worldwide. Diabetes has emerged as a leading cause of serious health issues including blindness, heart attacks, kidney failure, lower limb amputation, and strokes. The traditional treatment options for diabetes include oral medications, insulin injections and lifestyle modifications. However, conventional diabetes management techniques, characterized by multiple daily injections, are often associated with discomfort, inconvenience, and suboptimal patient outcomes. This raises several concerns related to drug delivery, including dosing inaccuracies, the risk of needlestick injuries, and variability in insulin absorption depending on the site of injection.

Given the limitations associated with diabetes drug delivery devices, insulin pumps have become a preferred option for insulin administration. These compact, lightweight devices are designed to deliver continuous or intermittent insulin infusions based on the patient's needs, offering a precise and adaptable approach to diabetes management. Notably, most insulin pumps can be worn on a belt and consist of a tube that connects the pump to an infusion set placed in the subcutaneous fatty tissue. Some insulin pumps can be worn directly on the skin as patches, allowing patients to move freely. These devices offer numerous advantages, including accurate and adjustable insulin delivery, customizable basal rates, bolus dosing during meals, enhanced comfort, and reduced risk of hypoglycemia and hyperglycemia, contributing to the enhanced quality of life. Further, insulin pumps comprise of a simple administration process that has proven to improve self-medication at-home settings, thereby reducing reliance on healthcare providers for insulin administration.

Key Market Segments

Type of Pump

- Tethered Pumps

- Patch Pumps

Degree of Automation

- Manual Pumps

- Automated / Smart Pumps

Type of Battery

- Replaceable Batteries

- Rechargeable Batteries

Type of Diabetes Targeted

- Type 1 Diabetes

- Type 2 Diabetes

Distribution Channel

- Retail Pharmacies

- Hospital Pharmacies

- Online Pharmacies

- Other Pharmacies

Key Geography

- North America (US, Canada)

- Europe (UK, Germany, Spain, France, Italy)

- Asia (China, India, Japan, Pakistan)

- Latin America (Brazil, Argentina, Mexico)

- Middle East and North Africa (Israel, Egypt, Saudi Arabia)

Research Coverage:

- An outline of the systematic research approach used for the study of insulin pump market, featuring an overview of the key assumptions, research methodologies, and quality control measures employed to ensure the accuracy and reliability of our findings.

- An in-depth assessment of the key factors including economic, strategic, technological, and institutional drivers impacting the growth of the insulin pump industry. Further, this section highlights key factors affecting market dynamics and the strong quality control framework implemented to guarantee transparency and credibility in the insights provided to the clients.

- An executive summary of the insights captured during our research, offering an overview of the current insulin pump market. Additionally, this section presents information on the most relevant trends, challenges and opportunities that are shaping the industry's development.

- A brief overview of diabetes, along with information on insulin pumps and their types. The module covers the advantages and drawbacks associated with the use of insulin pumps. In addition, it discusses the anticipated future trends in this domain.

- A detailed assessment of the current market landscape of insulin pumps, along with information on several relevant parameters, such as stage of development (under development and commercialized), launch year, type of pump (tethered pumps and patch pumps), degree of automation (manual pumps and automated / smart pumps), type of diabetes targeted (type 1 diabetes and type 2 diabetes), type of doses administered (basal and bolus), reservoir capacity and type of battery (replaceable batteries and rechargeable batteries). In addition, this section covers a detailed list of players engaged in manufacturing insulin pumps, along with analysis based on various parameters, such as year of establishment, company size (in terms of employee count), location of headquarters (North America, Europe and Asia-Pacific), type of company (public and private), and the most active players in this domain (in terms of number of insulin pumps manufactured).

- Elaborate profiles of prominent players manufacturing insulin pumps, based across different geographies, including North America, Europe and Asia-Pacific. Each profile features a brief overview of the company (including information on its year of establishment, location of headquarters, number of employees, leadership team, business segments and contact details), financial information (if available), insulin pump portfolio, recent developments and an informed future outlook.

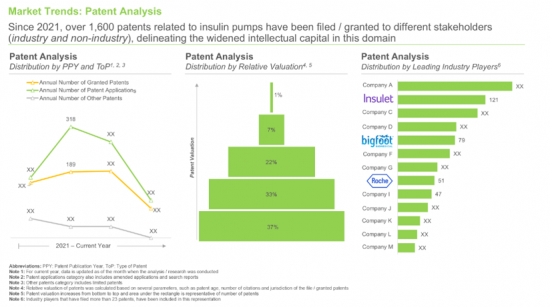

- An in-depth analysis of patents that have been filed / granted in insulin pump domain, since 2021, based on several relevant parameters, such as the type of patent (granted patents, patent applications and others), patent publication year, patent application year, patent jurisdiction, Cooperative Patent Classification (CPC) symbols, type of applicant, and most active industry and non-industry players (in terms of number of patents filed / granted). In addition, it includes patent benchmarking and an insightful patent valuation analysis, highlighting the leading players (in terms of number of citations).

- Detailed analysis of the factors that are likely to impact the growth of the insulin pump market. Further, the report also provides insights on the key drivers, potential restraints, emerging opportunities, and existing challenges in the insulin pump industry.

- A detailed estimate of the current market size, opportunity and the future growth potential of the insulin pump industry over the next decade. Based on multiple parameters, such as likely adoption trends and through primary validations, we have provided an informed estimate on the market evolution, during the forecast period till 2035.

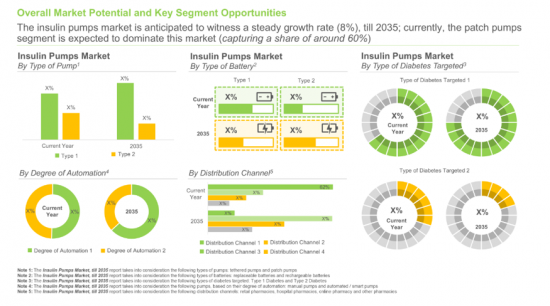

- Detailed projections of the current and future opportunity within the insulin pump market based on different types of pumps, such as tethered pumps and patch pumps.

- Detailed projections of the current and future opportunity within the insulin pump industry based on the degree of automation, such as manual pumps and automated / smart pumps.

- Detailed projections of the current and future opportunity within the insulin pump market, based on various types of batteries, such as replaceable batteries and rechargeable batteries.

- Detailed projections of the current and future opportunity within the insulin pump market across different types of diabetes, such as type 1 diabetes and type 2 diabetes.

- Detailed projections of the current and future opportunity within the insulin pump industry based on various distribution channels, such as retail pharmacies, hospital pharmacies, online pharmacies and other pharmacies.

- Detailed predictions of the current and future opportunity within the insulin pump market across key geographical regions, such as North America, Europe, Asia, Latin America, and Middle East and North Africa.

Key Benefits of Buying this Report

- The report offers valuable insights into revenue estimation for both the overall market and its sub-segments, in order to empower market leaders and newcomers with critical information requisite for establishing their footprint in the industry.

- The report can be utilized by stakeholders to enhance their understanding of the competitive landscape, allowing for improved business positioning and more effective go-to-market strategies.

- The report provides stakeholders with a comprehensive view on the insulin pump market, covering essential information on significant market drivers, barriers, opportunities, and challenges.

Example Companies Profiled

- Beta Bionics

- CeQur

- EOFlow

- Insulet Corporation

- LA Roche

- MannKind

- Medtronic

- Medtrum Technologies

- MicroPort

- Microtech Medical

- SOOIL Development

- Tandem Diabetes Care

- Terumo

- ViCentra

- Ypsomed

TABLE OF CONTENTS

1. PREFACE

- 1.1. Introduction

- 1.2. Market Share Insights

- 1.3. Key Market Insights

- 1.4. Report Coverage

- 1.5. Key Questions Answered

- 1.6. Chapter Outlines

2. RESEARCH METHODOLOGY

- 2.1. Chapter Overview

- 2.2. Research Assumptions

- 2.2.1. Market Landscape and Market Trends

- 2.2.2. Market Forecast and Opportunity Analysis

- 2.2.3. Comparative Analysis

- 2.3. Database Building

- 2.3.1. Data Collection

- 2.3.2. Data Validation

- 2.3.3. Data Analysis

- 2.4. Project Methodology

- 2.4.1. Secondary Research

- 2.4.1.1. Annual Reports

- 2.4.1.2. Academic Research Papers

- 2.4.1.3. Company Websites

- 2.4.1.4. Investor Presentations

- 2.4.1.5. Regulatory Filings

- 2.4.1.6. White Papers

- 2.4.1.7. Industry Publications

- 2.4.1.8. Conferences and Seminars

- 2.4.1.9. Government Portals

- 2.4.1.10. Media and Press Releases

- 2.4.1.11. Newsletters

- 2.4.1.12. Industry Databases

- 2.4.1.13. Roots Proprietary Databases

- 2.4.1.14. Paid Databases and Sources

- 2.4.1.15. Social Media Portals

- 2.4.1.16. Other Secondary Sources

- 2.4.2. Primary Research

- 2.4.2.1. Types of Primary Research

- 2.4.2.1.1. Qualitative Research

- 2.4.2.1.2. Quantitative Research

- 2.4.2.1.3. Hybrid Approach

- 2.4.2.2. Advantages of Primary Research

- 2.4.2.3. Techniques for Primary Research

- 2.4.2.3.1. Interviews

- 2.4.2.3.2. Surveys

- 2.4.2.3.3. Focus Groups

- 2.4.2.3.4. Observational Research

- 2.4.2.3.5. Social Media Interactions

- 2.4.2.4. Key Opinion Leaders Considered in Primary Research

- 2.4.2.4.1. Company Executives (CXOs)

- 2.4.2.4.2. Board of Directors

- 2.4.2.4.3. Company Presidents and Vice Presidents

- 2.4.2.4.4. Research and Development Heads

- 2.4.2.4.5. Technical Experts

- 2.4.2.4.6. Subject Matter Experts

- 2.4.2.4.7. Scientists

- 2.4.2.4.8. Doctors and Other Healthcare Providers

- 2.4.2.5. Ethics and Integrity

- 2.4.2.5.1. Research Ethics

- 2.4.2.5.2. Data Integrity

- 2.4.2.1. Types of Primary Research

- 2.4.3. Analytical Tools and Databases

- 2.4.1. Secondary Research

3. MARKET DYNAMICS

- 3.1. Chapter Overview

- 3.2. Forecast Methodology

- 3.2.1. Top-down Approach

- 3.2.2. Bottom-up Approach

- 3.2.3. Hybrid Approach

- 3.3. Market Assessment Framework

- 3.3.1. Total Addressable Market (TAM)

- 3.3.2. Serviceable Addressable Market (SAM)

- 3.3.3. Serviceable Obtainable Market (SOM)

- 3.3.4. Currently Acquired Market (CAM)

- 3.4. Forecasting Tools and Techniques

- 3.4.1. Qualitative Forecasting

- 3.4.2. Correlation

- 3.4.3. Regression

- 3.4.4. Extrapolation

- 3.4.5. Convergence

- 3.4.6. Sensitivity Analysis

- 3.4.7. Scenario Planning

- 3.4.8. Data Visualization

- 3.4.9. Time Series Analysis

- 3.4.10. Forecast Error Analysis

- 3.5. Key Considerations

- 3.5.1. Demographics

- 3.5.2. Government Regulations

- 3.5.3. Reimbursement Scenarios

- 3.5.4. Market Access

- 3.5.5. Supply Chain

- 3.5.6. Industry Consolidation

- 3.5.7. Pandemic / Unforeseen Disruptions Impact

- 3.6. Key Market Segmentation

- 3.7. Robust Quality Control

- 3.8. Limitations

4. ECONOMIC AND OTHER PROJECT SPECIFIC CONSIDERATIONS

- 4.1. Chapter Overview

- 4.2. Market Dynamics

- 4.2.1. Time Period

- 4.2.1.1. Historical Trends

- 4.2.1.2. Current and Forecasted Estimates

- 4.2.2. Currency Coverage

- 4.2.2.1. Overview of Major Currencies Affecting the Market

- 4.2.2.2. Impact of Currency Fluctuations on the Industry

- 4.2.3. Foreign Exchange Impact

- 4.2.3.1. Evaluation of Foreign Exchange Rates and Their Impact on Market

- 4.2.3.2. Strategies for Mitigating Foreign Exchange Risk

- 4.2.4. Recession

- 4.2.4.1. Historical Analysis of Past Recessions and Lessons Learnt

- 4.2.4.2. Assessment of Current Economic Conditions and Potential Impact on the Market

- 4.2.5. Inflation

- 4.2.5.1. Measurement and Analysis of Inflationary Pressures in the Economy

- 4.2.5.2. Potential Impact of Inflation on the Market Evolution

- 4.2.1. Time Period

5. EXECUTIVE SUMMARY

6. INTRODUCTION

- 6.1. Chapter Overview

- 6.2. Overview of Diabetes

- 6.2.1. Classification of Diabetes

- 6.3. Insulin Pumps

- 6.3.1. Types of Insulin Pumps

- 6.3.2. Advantages of Insulin Pumps

- 6.3.3. Limitations of Insulin Pumps

- 6.4. Future Perspectives

7. INSULIN PUMPS: MARKET LANDSCAPE

- 7.1. Chapter Overview

- 7.2. Insulin Pumps: Overall Market Landscape

- 7.2.1. Analysis by Stage of Development

- 7.2.2. Analysis by Launch Year

- 7.2.3. Analysis by Type of Pump

- 7.2.4. Analysis by Degree of Automation

- 7.2.5. Analysis by Type of Diabetes Targeted

- 7.2.6. Analysis by Type of Dose Administered

- 7.2.7. Analysis by Reservoir Capacity

- 7.2.8. Analysis by Type of Battery

- 7.3. Insulin Pumps: List of Manufacturer

- 7.3.1. Analysis by Year of Establishment

- 7.3.2. Analysis by Company Size

- 7.3.3. Analysis by Location of Headquarters

- 7.3.4. Analysis by Company Size and Location of Headquarters

- 7.3.5. Analysis by Type of Company

- 7.3.6. Most Active Players: Analysis by Number of Insulin Pumps Manufactured

8. COMPANY PROFILES: INSULIN PUMP MANUFACTURERS BASED IN NORTH AMERICA

- 8.1. Chapter Overview

- 8.2. Beta Bionics

- 8.2.1. Company Overview

- 8.2.2. Insulin Pumps Portfolio

- 8.2.3. Recent Developments and Future Outlook

- 8.3. Insulet

- 8.3.1. Company Overview

- 8.3.2. Insulin Pumps Portfolio

- 8.3.3. Recent Developments and Future Outlook

- 8.4. MannKind

- 8.4.1. Company Overview

- 8.4.2. Insulin Pumps Portfolio

- 8.4.3. Recent Developments and Future Outlook

- 8.5. Medtronic

- 8.5.1. Company Overview

- 8.5.2. Insulin Pumps Portfolio

- 8.5.3. Recent Developments and Future Outlook

- 8.6. Tandem Diabetes Care

- 8.6.1. Company Overview

- 8.6.2. Insulin Pumps Portfolio

- 8.6.3. Recent Developments and Future Outlook

9. COMPANY PROFILES: INSULIN PUMP MANUFACTURERS BASED IN EUROPE

- 9.1. Chapter Overview

- 9.2. CeQur

- 9.2.1. Company Overview

- 9.2.2. Insulin Pumps Portfolio

- 9.2.3. Recent Developments and Future Outlook

- 9.3. Roche

- 9.3.1. Company Overview

- 9.3.2. Financial Information

- 9.3.3. Insulin Pumps Portfolio

- 9.3.4. Recent Developments and Future Outlook

- 9.4. ViCentra

- 9.4.1. Company Overview

- 9.4.2. Insulin Pumps Portfolio

- 9.4.3. Recent Developments and Future Outlook

- 9.5. Ypsomed

- 9.5.1. Company Overview

- 9.5.2. Financial Information

- 9.5.3. Insulin Pumps Portfolio

- 9.5.4. Recent Developments and Future Outlook

10. COMPANY PROFILES: INSULIN PUMP MANUFACTURERS BASED IN ASIA-PACIFIC

- 10.1. Chapter Overview

- 10.2. EOFlow

- 10.2.1. Company Overview

- 10.2.2. Financial Information

- 10.2.3. Insulin Pumps Portfolio

- 10.2.4. Recent Developments and Future Outlook

- 10.3. Medtrum Technologies

- 10.3.1. Company Overview

- 10.3.2. Insulin Pumps Portfolio

- 10.3.3. Recent Developments and Future Outlook

- 10.4. MicroPort

- 10.4.1. Company Overview

- 10.4.2. Financial Information

- 10.4.3. Insulin Pumps Portfolio

- 10.4.4. Recent Developments and Future Outlook

- 10.5. Microtech Medical

- 10.5.1. Company Overview

- 10.5.2. Financial Information

- 10.5.3. Insulin Pumps Portfolio

- 10.5.4. Recent Developments and Future Outlook

- 10.6. SOOIL Development

- 10.6.1. Company Overview

- 10.6.2. Financial Information

- 10.6.3. Insulin Pumps Portfolio

- 10.6.4. Recent Developments and Future Outlook

- 10.7. Terumo

- 10.7.1. Company Overview

- 10.7.2. Financial Information

- 10.7.3. Insulin Pumps Portfolio

- 10.7.4. Recent Developments and Future Outlook

11. PATENT ANALYSIS

- 11.1. Chapter Overview

- 11.2. Scope and Methodology

- 11.3. Insulin Pumps: Patent Analysis

- 11.3.1. Analysis by Patent Publication Year

- 11.3.2. Analysis by Patent Application Year

- 11.3.3. Analysis by Type of Patent and Publication Year

- 11.3.4. Analysis by Patent Jurisdiction

- 11.3.5. Analysis by CPC Symbols

- 11.3.6. Analysis by Type of Applicant

- 11.3.7. Leading Industry Players: Analysis by Number of Patents

- 11.3.8. Leading Non-industry Players: Analysis by Number of Patents

- 11.3.9. Leading Patent Assignees: Analysis by Number of Patents

- 11.4. Patent Benchmarking Analysis

- 11.4.1. Analysis of Patent Characteristics (CPC codes) by Leading Industry Players

- 11.4.2. Analysis of Leading Industry Players by Patent Characteristics (CPC codes)

- 11.5. Patent Valuation

- 11.6. Leading Patents by Number of Citations

12. MARKET IMPACT ANALYSIS

- 12.1. Chapter Overview

- 12.2. Market Drivers

- 12.3. Market Restraints

- 12.4. Market Opportunities

- 12.5. Market Challenges

- 12.6. Conclusion

13. GLOBAL INSULIN PUMPS MARKET

- 13.1. Chapter Overview

- 13.2. Key Assumptions and Methodology

- 13.3. Global Insulin Pumps Market, till 2035

- 13.3.1. Scenario Analysis

- 13.3.1.1. Conservative Scenario

- 13.3.1.2. Optimistic Scenario

- 13.3.1. Scenario Analysis

- 13.4. Key Market Segmentations

- 13.5. Leading Industry Players

14. INSULIN PUMPS MARKET, BY TYPE OF PUMP

- 14.1. Chapter Overview

- 14.2. Key Assumptions and Methodology

- 14.3. Insulin Pumps Market: Distribution by Type of Pump, 2017, Current Year and 2035

- 14.3.1. Insulin Pumps Market for Tethered Pumps, till 2035

- 14.3.2. Insulin Pumps Market for Patch Pumps, till 2035

- 14.4. Data Triangulation and Validation

15. INSULIN PUMPS MARKET, BY DEGREE OF AUTOMATION

- 15.1. Chapter Overview

- 15.2. Key Assumptions and Methodology

- 15.3. Insulin Pumps Market: Distribution by Degree of Automation, 2017, Current Year and 2035

- 15.3.1. Insulin Pumps Market for Manual Pumps, till 2035

- 15.3.2. Insulin Pumps Market for Automated / Smart Pumps, till 2035

- 15.4. Data Triangulation and Validation

16. INSULIN PUMPS MARKET, BY TYPE OF BATTERY

- 16.1. Chapter Overview

- 16.2. Key Assumptions and Methodology

- 16.3. Insulin Pumps Market: Distribution by Type of Battery, 2017, Current Year and 2035

- 16.3.1. Insulin Pumps Market for Replaceable Batteries, till 2035

- 16.3.2. Insulin Pumps Market for Rechargeable Batteries, till 2035

- 16.4. Data Triangulation and Validation

17. INSULIN PUMPS MARKET, BY TYPE OF DIABETES TARGETED

- 17.1. Chapter Overview

- 17.2. Key Assumptions and Methodology

- 17.3. Insulin Pumps Market: Distribution by Type of Diabetes Targeted, 2017, Current Year and 2035

- 17.3.1. Insulin Pumps Market for Type 1 Diabetes, till 2035

- 17.3.1.1. Insulin Pumps Market for Type 1 Diabetes in North America, till 2035

- 17.3.1.1.1. Insulin Pumps Market for Type 1 Diabetes in the US, till 2035

- 17.3.1.1.2. Insulin Pumps Market for Type 1 Diabetes in Canada, till 2035

- 17.3.1.2. Insulin Pumps Market for Type 1 Diabetes in Europe, till 2035

- 17.3.1.2.1. Insulin Pumps Market for Type 1 Diabetes in the UK, till 2035

- 17.3.1.2.2. Insulin Pumps Market for Type 1 Diabetes in Germany, till 2035

- 17.3.1.2.3. Insulin Pumps Market for Type 1 Diabetes in Spain, till 2035

- 17.3.1.2.4. Insulin Pumps Market for Type 1 Diabetes in Italy, till 2035

- 17.3.1.2.5. Insulin Pumps Market for Type 1 Diabetes in France, till 2035

- 17.3.1.3. Insulin Pumps Market for Type 1 Diabetes in Asia, till 2035

- 17.3.1.3.1. Insulin Pumps Market for Type 1 Diabetes in China, till 2035

- 17.3.1.3.2. Insulin Pumps Market for Type 1 Diabetes in Japan, till 2035

- 17.3.1.3.3. Insulin Pumps Market for Type 1 Diabetes in India, till 2035

- 17.3.1.3.4. Insulin Pumps Market for Type 1 Diabetes in Pakistan, till 2035

- 17.3.1.4. Insulin Pumps Market for Type 1 Diabetes in Middle East and North Africa, till 2035

- 17.3.1.4.1. Insulin Pumps Market for Type 1 Diabetes in Israel, till 2035

- 17.3.1.4.2. Insulin Pumps Market for Type 1 Diabetes in Egypt, till 2035

- 17.3.1.4.3. Insulin Pumps Market for Type 1 Diabetes in Saudi Arabia, till 2035

- 17.3.1.5. Insulin Pumps Market for Type 1 Diabetes in Latin America, till 2035

- 17.3.1.5.1. Insulin Pumps Market for Type 1 Diabetes in Brazil, till 2035

- 17.3.1.5.2. Insulin Pumps Market for Type 1 Diabetes in Argentina, till 2035

- 17.3.1.5.3. Insulin Pumps Market for Type 1 Diabetes in Mexico, till 2035

- 17.3.1.1. Insulin Pumps Market for Type 1 Diabetes in North America, till 2035

- 17.3.2. Insulin Pumps Market for Type 2 Diabetes, till 2035

- 17.3.2.1. Insulin Pumps Market for Type 2 Diabetes in North America, till 2035

- 17.3.2.1.1. Insulin Pumps Market for Type 2 Diabetes in the US, till 2035

- 17.3.2.1.2. Insulin Pumps Market for Type 2 Diabetes in Canada, till 2035

- 17.3.2.2. Insulin Pumps Market for Type 2 Diabetes in Europe, till 2035

- 17.3.2.2.1. Insulin Pumps Market for Type 2 Diabetes in the UK, till 2035

- 17.3.2.2.2. Insulin Pumps Market for Type 2 Diabetes in Germany, till 2035

- 17.3.2.2.3. Insulin Pumps Market for Type 2 Diabetes in Spain, till 2035

- 17.3.2.2.4. Insulin Pumps Market for Type 2 Diabetes in Italy, till 2035

- 17.3.2.2.5. Insulin Pumps Market for Type 2 Diabetes in France, till 2035

- 17.3.2.3. Insulin Pumps Market for Type 2 Diabetes in Asia, till 2035

- 17.3.2.3.1. Insulin Pumps Market for Type 2 Diabetes in China, till 2035

- 17.3.2.3.2. Insulin Pumps Market for Type 2 Diabetes in Japan, till 2035

- 17.3.2.3.3. Insulin Pumps Market for Type 2 Diabetes in India, till 2035

- 17.3.2.3.4. Insulin Pumps Market for Type 2 Diabetes in Pakistan, till 2035

- 17.3.2.4. Insulin Pumps Market for Type 2 Diabetes in Middle East and North Africa, till 2035

- 17.3.2.4.1. Insulin Pumps Market for Type 2 Diabetes in Israel, till 2035

- 17.3.2.4.2. Insulin Pumps Market for Type 2 Diabetes in Egypt, till 2035

- 17.3.2.4.3. Insulin Pumps Market for Type 2 Diabetes in Saudi Arabia, till 2035

- 17.3.2.5. Insulin Pumps Market for Type 2 Diabetes in Latin America, till 2035

- 17.3.2.5.1. Insulin Pumps Market for Type 2 Diabetes in Brazil, till 2035

- 17.3.2.5.2. Insulin Pumps Market for Type 2 Diabetes in Argentina, till

- 17.3.2.5.3. Insulin Pumps Market for Type 2 Diabetes in Mexico, till 2035

- 17.3.2.1. Insulin Pumps Market for Type 2 Diabetes in North America, till 2035

- 17.3.1. Insulin Pumps Market for Type 1 Diabetes, till 2035

- 17.4. Data Triangulation and Validation

18. INSULIN PUMPS MARKET, BY DISTRIBUTION CHANNEL

- 18.1. Chapter Overview

- 18.2. Key Assumptions and Methodology

- 18.3. Insulin Pumps Market: Distribution by Distribution Channel, 2017, Current Year and 2035

- 18.3.1. Insulin Pumps Market for Retail Pharmacies, till 2035

- 18.3.2. Insulin Pumps Market for Hospital Pharmacies, till 2035

- 18.3.3. Insulin Pumps Market for Online Pharmacies, till 2035

- 18.3.4. Insulin Pumps Market for Other Pharmacies, till 2035

- 18.4. Data Triangulation and Validation

19. INSULIN PUMPS MARKET, BY GEOGRAPHY

- 19.1. Chapter Overview

- 19.2. Assumptions and Methodology

- 19.3. Insulin Pumps Market: Distribution by Geography, 2017, Current Year and 2035

- 19.3.1. Insulin Pumps Market in North America, till 2035

- 19.3.1.1. Insulin Pumps Market in the US, till 2035

- 19.3.1.2. Insulin Pumps Market in Canada, till 2035

- 19.3.2. Insulin Pumps Market in Europe, till 2035

- 19.3.2.1. Insulin Pumps Market in the UK, till 2035

- 19.3.2.2. Insulin Pumps Market in Germany, till 2035

- 19.3.2.3. Insulin Pumps Market in Spain, till 2035

- 19.3.2.4. Insulin Pumps Market in Italy, till 2035

- 19.3.2.5. Insulin Pumps Market in France, till 2035

- 19.3.3. Insulin Pumps Market in Asia, till 2035

- 19.3.3.1. Insulin Pumps Market in China, till 2035

- 19.3.3.2. Insulin Pumps Market in Japan, till 2035

- 19.3.3.3. Insulin Pumps Market in India, till 2035

- 19.3.3.4. Insulin Pumps Market in Pakistan, till 2035

- 19.3.4. Insulin Pumps Market in Middle East and North Africa, till 2035

- 19.3.4.1. Insulin Pumps Market in Israel, till 2035

- 19.3.4.2. Insulin Pumps Market in Egypt, till 2035

- 19.3.4.3. Insulin Pumps Market in Saudi Arabia, till 2035

- 19.3.5. Insulin Pumps Market in Latin America, till 2035

- 19.3.5.1. Insulin Pumps Market in Brazil, till 2035

- 19.3.5.2. Insulin Pumps Market in Argentina, till 2035

- 19.3.5.3. Insulin Pumps Market in Mexico, till 2035

- 19.3.1. Insulin Pumps Market in North America, till 2035

- 19.4. Insulin Pumps Market, By Geography: Market Dynamics Assessment

- 19.4.1. Penetration Growth (P-G) Matrix

- 19.4.2. Market Movement Analysis

- 19.5. Data Triangulation and Validation

20. CONCLUDING REMARKS

21. EXECUTIVE INSIGHTS

22. APPENDIX I: TABULATED DATA

23. APPENDIX II: LIST OF COMPANIES AND ORGANIZATIONS

List of Tables

- Table 6.1 Blood Sugar Levels

- Table 7.1 Insulin Pumps: Information on Stage of Development, Launch Year and Type of Pump

- Table 7.2 Insulin Pumps: Information on Degree of Automation, Type of Diabetes Targeted and Type of Dose Administered

- Table 7.3 Insulin Pumps: Information on Reservoir Capacity and Type of Battery

- Table 7.4 Insulin Pumps: Information on Insulin Name, Target Patient Population, Availability of Software / Mobile App, Regulatory Approval Compliance and Price of Pump

- Table 8.1 Insulin Pump Manufacturers in North America: List of Companies Profiled

- Table 8.2 Beta Bionics: Company Overview

- Table 8.3 Beta Bionics: Insulin Pumps Portfolio

- Table 8.4 Beta Bionics: Recent Developments and Future Outlook

- Table 8.5 Insulet: Company Overview

- Table 8.6 Insulet: Insulin Pumps Portfolio

- Table 8.7 Insulet: Recent Developments and Future Outlook

- Table 8.8 MannKind: Company Overview

- Table 8.9 MannKind: Insulin Pumps Portfolio

- Table 8.10 MannKind: Recent Developments and Future Outlook

- Table 8.11 Medtronic: Company Overview

- Table 8.12 Medtronic: Insulin Pumps Portfolio

- Table 8.13 Medtronic: Recent Developments and Future Outlook

- Table 8.14 Tandem Diabetes Care: Company Overview

- Table 8.15 Tandem Diabetes Care: Insulin Pumps Portfolio

- Table 8.16 Tandem Diabetes Care: Recent Developments and Future Outlook

- Table 9.1 Insulin Pump Manufacturers in Europe: List of Companies Profiled

- Table 9.2 CeQur: Company Overview

- Table 9.3 CeQur: Insulin Pumps Portfolio

- Table 9.4 CeQur: Recent Developments and Future Outlook

- Table 9.5 Roche: Company Overview

- Table 9.6 Roche: Insulin Pumps Portfolio

- Table 9.7 Roche: Recent Developments and Future Outlook

- Table 9.8 ViCentra: Company Overview

- Table 9.9 ViCentra: Insulin Pumps Portfolio

- Table 9.10 Terumo: Company Overview

- Table 9.11 Terumo: Insulin Pumps Portfolio

- Table 9.12 Terumo: Recent Developments and Future Outlook

- Table 9.13 Ypsomed: Company Overview

- Table 9.14 Ypsomed Medical: Insulin Pumps Portfolio

- Table 9.15 Ypsomed: Recent Developments and Future Outlook

- Table 10.1 Insulin Pump Manufacturers in Asia Pacific: List of Companies Profiled

- Table 10.2 EOFlow: Company Overview

- Table 10.3 EOFlow: Insulin Pumps Portfolio

- Table 10.4 EOFlow: Recent Developments and Future Outlook

- Table 10.5 Medtrum Technologies: Company Overview

- Table 10.6 Medtrum Technologies: Insulin Pumps Portfolio

- Table 10.7 MicroPort: Company Overview

- Table 10.8 MicroPort: Insulin Pumps Portfolio

- Table 10.9 MicroPort: Recent Developments and Future Outlook

- Table 10.10 MicroTech Medical: Company Overview

- Table 10.11 MicroTech Medical: Insulin Pumps Portfolio

- Table 10.12 SOOIL Development: Company Overview

- Table 10.13 SOOIL Development: Insulin Pumps Portfolio

- Table 10.14 SOOIL Development: Recent Developments and Future Outlook

- Table 11.1 Patent Analysis: Top CPC Sections

- Table 11.2 Patent Analysis: Top CPC Symbols

- Table 11.3 Patent Analysis: Top CPC Codes

- Table 11.4 Patent Analysis: Summary of Benchmarking Analysis

- Table 11.5 Patent Analysis: Categorization based on Weighted Valuation Scores

- Table 11.6 Patent Portfolio: List of Leading Patents (by Highest Relative Valuation)

- Table 11.7 Patent Portfolio: List of Leading Patents (By Number of Citations)

- Table 21.1 Company Snapshot: Mid-sized Company

- Table 22.1 Insulin Pumps: Distribution by Stage of Development

- Table 22.2 Insulin Pumps: Distribution by Launch Year

- Table 22.3 Insulin Pumps: Distribution by Type of Pump

- Table 22.4 Insulin Pumps: Distribution by Degree of Automation

- Table 22.5 Insulin Pumps: Distribution by Type of Diabetes Targeted

- Table 22.6 Insulin Pumps: Distribution by Type of Dose Administered

- Table 22.7 Insulin Pumps: Distribution by Insulin Storage Capacity

- Table 22.8 Insulin Pumps: Distribution by Type of Battery

- Table 22.9 Insulin Pump Manufacturers: Distribution Year of Establishment

- Table 22.10 Insulin Pump Manufacturers: Distribution by Company Size

- Table 22.11 Insulin Pump Manufacturers: Distribution by Location of Headquarters (Region)

- Table 22.12 Insulin Pump Manufacturers: Distribution by Location of Headquarters (Country)

- Table 22.13 Insulin Pump Manufacturers: Distribution by Company Size and Location of Headquarters

- Table 22.14 Insulin Pump Manufacturers: Distribution by Type of Company

- Table 22.15 Most Active Players: Distribution by Number of Devices Manufactured

- Table 22.16 Insulet: Business Segment-wise Revenues and Consolidated Financial Details (USD Million)

- Table 22.17 MannKind: Business Segment-wise Revenues and Consolidated Financial Details (USD Million)

- Table 22.18 Medtronic: Business Segment-wise Revenues and Consolidated Financial Details (USD Billion)

- Table 22.19 Tandem Diabetes Care: Consolidated Financial Details (USD Million)

- Table 22.20 Roche: Business Segment-wise Revenues and Consolidated Financial Details (CHF Billion)

- Table 22.21 Terumo: Consolidated Financial Details (Yen Billion)

- Table 22.22 Ypsomed: Business Segment-wise Revenues and Consolidated Financial Details (CHF Million)

- Table 22.23 MicroPort: Consolidated Financial Details (USD Million)

- Table 22.24 MicroTech Medical: Business Segment-wise Revenues and Consolidated Financial Details (RMB Million)

- Table 22.25 Patent Analysis: Distribution by Type of Patent

- Table 22.26 Patent Analysis: Cumulative Year-wise Trend by Patent Publication Year, Since 2021

- Table 22.27 Patent Analysis: Cumulative Year-wise Trend by Patent Application Year, Since 2005

- Table 22.28 Patent Analysis: Year-wise Distribution of Granted Patents and Patent Applications, Since 2005

- Table 22.29 Patent Analysis: Distribution by Patent Jurisdiction

- Table 22.30 Patent Analysis: Cumulative Year-wise Trend by Type of Applicant

- Table 22.31 Leading Industry Players: Distribution by Number of Patents

- Table 22.32 Leading Non-Industry Players: Distribution by Number of Patents

- Table 22.33 Leading Patent Assignees: Distribution by Number of Patents

- Table 22.34 Patent Analysis: Distribution by Patent Age

- Table 22.35 Insulin Pumps: Patent Valuation

- Table 22.36 Global Insulin Pumps Market, Historical Trends, till-2035 (Million Units Sold, USD Billion)

- Table 22.37 Global Insulin Pumps Market, till 2035: Conservative Scenario (Million Units Sold, USD Billion)

- Table 22.38 Global Insulin Pumps Market, till 2035: Optimistic Scenario (Million Units Sold, USD Billion)

- Table 22.39 Insulin Pumps Market: Distribution by Type of Pump, 2017, Current Year and 2035 (USD Billion)

- Table 22.40 Insulin Pumps Market for Tethered Pumps, till 2035 (Million Units Sold, USD Billion)

- Table 22.41 Insulin Pumps Market for Patch Pumps, till 2035 (Million Units Sold, USD Billion)

- Table 22.42 Insulin Pumps Market: Distribution by Degree of Automation, 2017, Current Year and 2035 (USD Billion)

- Table 22.43 Insulin Pumps Market for Manual Pumps, till 2035 (Million Units Sold, USD Billion)

- Table 22.44 Insulin Pumps Market for Automated / Smart Pumps, till 2035 (Million Units Sold, USD Billion)

- Table 22.45 Insulin Pumps Market: Distribution by Type of Battery, 2017, Current Year and 2035 (USD Billion)

- Table 22.46 Insulin Pumps Market for Replaceable Batteries, till 2035 (Million Units Sold, USD Billion)

- Table 22.47 Insulin Pumps Market for Rechargeable Batteries, till 2035 (Million Units Sold, USD Billion)

- Table 22.48 Insulin Pumps Market: Distribution by Type of Diabetes Targeted, 2017, Current Year and 2035 (USD Billion)

- Table 22.49 Insulin Pumps Market for Type 1 Diabetes, till 2035 (Million Units Sold, USD Billion)

- Table 22.50 Insulin Pumps Market for Type 1 Diabetes in North America, till 2035 (Million Units Sold, USD Billion)

- Table 22.51 Insulin Pumps Market for Type 1 Diabetes in US, till 2035 (Million Units Sold, USD Billion)

- Table 22.52 Insulin Pumps Market for Type 1 Diabetes in Canada, till 2035 (Million Units Sold, USD Billion)

- Table 22.53 Insulin Pumps Market for Type 1 Diabetes in Europe, till 2035 (Million Units Sold, USD Billion)

- Table 22.54 Insulin Pumps Market for Type 1 Diabetes in UK, till 2035 (Million Units Sold, USD Billion)

- Table 22.55 Insulin Pumps Market for Type 1 Diabetes in Germany, till 2035 (Million Units Sold, USD Billion)

- Table 22.56 Insulin Pumps Market for Type 1 Diabetes in Spain, till 2035 (Million Units Sold, USD Billion)

- Table 22.57 Insulin Pumps Market for Type 1 Diabetes in Italy, till 2035 (Million Units Sold, USD Billion)

- Table 22.58 Insulin Pumps Market for Type 1 Diabetes in France, till 2035 (Million Units Sold, USD Billion)

- Table 22.59 Insulin Pumps Market for Type 1 Diabetes in Asia, till 2035 (Million Units Sold, USD Billion)

- Table 22.60 Insulin Pumps Market for Type 1 Diabetes in China, till 2035 (Million Units Sold, USD Billion)

- Table 22.61 Insulin Pumps Market for Type 1 Diabetes in Japan, till 2035 (Million Units Sold, USD Billion)

- Table 22.62 Insulin Pumps Market for Type 1 Diabetes in India, till 2035 (Million Units Sold, USD Billion)

- Table 22.63 Insulin Pumps Market for Type 1 Diabetes in Pakistan, till 2035 (Million Units Sold, USD Billion)

- Table 22.64 Insulin Pumps Market for Type 1 Diabetes in Middle East and North Africa, till 2035 (Million Units Sold, USD Billion)

- Table 22.65 Insulin Pumps Market for Type 1 Diabetes in Israel, till 2035 (Million Units Sold, USD Billion)

- Table 22.66 Insulin Pumps Market for Type 1 Diabetes in Egypt, till 2035 (Million Units Sold, USD Billion)

- Table 22.67 Insulin Pumps Market for Type 1 Diabetes in Saudi Arabia, till 2035 (Million Units Sold, USD Billion)

- Table 22.68 Insulin Pumps Market for Type 1 Diabetes in Latin America, till 2035 (Million Units Sold, USD Billion)

- Table 22.69 Insulin Pumps Market for Type 1 Diabetes in Brazil, till 2035 (Million Units Sold, USD Billion)

- Table 22.70 Insulin Pumps Market for Type 1 Diabetes in Argentina, till 2035 (Million Units Sold, USD Billion)

- Table 22.71 Insulin Pumps Market for Type 1 Diabetes in Mexico, till 2035 (Million Units Sold, USD Billion)

- Table 22.72 Insulin Pumps Market for Type 2 Diabetes, till 2035 (Million Units Sold, USD Billion)

- Table 22.73 Insulin Pumps Market for Type 2 Diabetes in North America, till 2035 (Million Units Sold, USD Billion)

- Table 22.74 Insulin Pumps Market for Type 2 Diabetes in US, till 2035 (Million Units Sold, USD Billion)

- Table 22.75 Insulin Pumps Market for Type 2 Diabetes in Canada, till 2035 (Million Units Sold, USD Billion)

- Table 22.76 Insulin Pumps Market for Type 2 Diabetes in Europe, till 2035 (Million Units Sold, USD Billion)

- Table 22.77 Insulin Pumps Market for Type 2 Diabetes in UK, till 2035 (Million Units Sold, USD Billion)

- Table 22.78 Insulin Pumps Market for Type 2 Diabetes in Germany, till 2035 (Million Units Sold, USD Billion)

- Table 22.79 Insulin Pumps Market for Type 2 Diabetes in Spain, till 2035 (Million Units Sold, USD Billion)

- Table 22.80 Insulin Pumps Market for Type 2 Diabetes in Italy, till 2035 (Million Units Sold, USD Billion)

- Table 22.81 Insulin Pumps Market for Type 2 Diabetes in France, till 2035 (Million Units Sold, USD Billion)

- Table 22.82 Insulin Pumps Market for Type 2 Diabetes in Asia, till 2035 (Million Units Sold, USD Billion)

- Table 22.83 Insulin Pumps Market for Type 2 Diabetes in China, till 2035 (Million Units Sold, USD Billion)

- Table 22.84 Insulin Pumps Market for Type 2 Diabetes in Japan, till 2035 (Million Units Sold, USD Billion)

- Table 22.85 Insulin Pumps Market for Type 2 Diabetes in India, till 2035 (Million Units Sold, USD Billion)

- Table 22.86 Insulin Pumps Market for Type 2 Diabetes in Pakistan, till 2035 (Million Units Sold, USD Billion)

- Table 22.87 Insulin Pumps Market for Type 2 Diabetes in Middle East and North Africa, till 2035 (Million Units Sold, USD Billion)

- Table 22.88 Insulin Pumps Market for Type 2 Diabetes in Israel, till 2035 (Million Units Sold, USD Billion)

- Table 22.89 Insulin Pumps Market for Type 2 Diabetes in Egypt, till 2035 (Million Units Sold, USD Billion)

- Table 22.90 Insulin Pumps Market for Type 2 Diabetes in Saudi Arabia, till 2035 (Million Units Sold, USD Billion)

- Table 22.91 Insulin Pumps Market for Type 2 Diabetes in Latin America, till 2035 (Million Units Sold, USD Billion)

- Table 22.92 Insulin Pumps Market for Type 2 Diabetes in Brazil, till 2035 (Million Units Sold, USD Billion)

- Table 22.93 Insulin Pumps Market for Type 2 Diabetes in Argentina, till 2035 (Million Units Sold, USD Billion)

- Table 22.94 Insulin Pumps Market for Type 2 Diabetes in Mexico, till 2035 (Million Units Sold, USD Billion)

- Table 22.95 Insulin Pumps Market: Distribution by Distribution Channel, 2017, Current Year and 2035 (USD Billion)

- Table 22.96 Insulin Pumps Market for Retail Pharmacies, till 2035 (Million Units Sold, USD Billion)

- Table 22.97 Insulin Pumps Market for Online Pharmacies, till 2035 (Million Units Sold, USD Billion)

- Table 22.98 Insulin Pumps Market for Hospital Pharmacies, till 2035 (Million Units Sold, USD Billion)

- Table 22.99 Insulin Pumps Market for Other Pharmacies, till 2035 (Million Units Sold, USD Billion)

- Table 22.100 Insulin Pumps Market: Distribution by Geography, 2017, Current Year and 2035 (USD Billion)

- Table 22.101 Insulin Pumps Market in North America, till 2035 (Million Units Sold, USD Billion)

- Table 22.102 Insulin Pumps Market in US, till 2035 (Million Units Sold, USD Billion)

- Table 22.103 Insulin Pumps Market in Canada, till 2035 (Million Units Sold, USD Billion)

- Table 22.104 Insulin Pumps Market in Europe, till 2035 (Million Units Sold, USD Billion)

- Table 22.105 Insulin Pumps Market in UK, till 2035 (Million Units Sold, USD Billion)

- Table 22.106 Insulin Pumps Market in Germany, till 2035 (Million Units Sold, USD Billion)

- Table 22.107 Insulin Pumps Market in Spain, till 2035 (Million Units Sold, USD Billion)

- Table 22.108 Insulin Pumps Market in Italy, till 2035 (Million Units Sold, USD Billion)

- Table 22.109 Insulin Pumps Market in France, till 2035 (Million Units Sold, USD Billion)

- Table 22.110 Insulin Pumps Market in Asia, till 2035 (Million Units Sold, USD Billion)

- Table 22.111 Insulin Pumps Market in China, till 2035 (Million Units Sold, USD Billion)

- Table 22.112 Insulin Pumps Market in Japan, till 2035 (Million Units Sold, USD Billion)

- Table 22.113 Insulin Pumps Market in India, till 2035 (Million Units Sold, USD Billion)

- Table 22.114 Insulin Pumps Market in Pakistan, till 2035 (Million Units Sold, USD Billion)

- Table 22.115 Insulin Pumps Market in Middle East and North Africa, till 2035 (Million Units Sold, USD Billion)

- Table 22.116 Insulin Pumps Market in Israel, till 2035 (Million Units Sold, USD Billion)

- Table 22.117 Insulin Pumps Market in Egypt, till 2035 (Million Units Sold, USD Billion)

- Table 22.118 Insulin Pumps Market in Saudi Arabia, till 2035 (Million Units Sold, USD Billion)

- Table 22.119 Insulin Pumps Market in Latin America, till 2035 (Million Units Sold, USD Billion)

- Table 22.120 Insulin Pumps Market in Brazil, till 2035 (Million Units Sold, USD Billion)

- Table 22.121 Insulin Pumps Market in Argentina, till 2035 (Million Units Sold, USD Billion)

- Table 22.122 Insulin Pumps Market in Mexico, till 2035 (Million Units Sold, USD Billion)

List of Figures

- Figure 2.1 Research Methodology: Project Methodology

- Figure 2.2 Research Methodology: Data Sources for Secondary Research

- Figure 3.1 Market Dynamics: Forecast Methodology

- Figure 3.2 Market Dynamics: Key Market Segmentation

- Figure 3.3 Market Dynamics: Robust Quality Control

- Figure 4.1 Lessons Learnt from Past Recessions

- Figure 5.1 Executive Summary: Insulin Pumps Market Landscape

- Figure 5.2 Executive Summary: Patent Analysis

- Figure 5.3 Executive Summary: Market Forecast and Opportunity Analysis

- Figure 6.1 Classification of Diabetes

- Figure 7.1 Insulin Pumps: Distribution by Stage of Development

- Figure 7.2 Insulin Pumps: Distribution by Launch Year

- Figure 7.3 Insulin Pumps: Distribution by Type of Pump

- Figure 7.4 Insulin Pumps: Distribution by Degree of Automation

- Figure 7.5 Insulin Pumps: Distribution by Type of Diabetes Targeted

- Figure 7.6 Insulin Pumps: Distribution by Type of Dose Administered

- Figure 7.7 Insulin Pumps: Distribution by Reservoir Capacity

- Figure 7.8 Insulin Pumps: Distribution by Type of Battery

- Figure 7.9 Insulin Pump Manufacturers: Distribution by Year of Establishment

- Figure 7.10 Insulin Pump Manufacturers: Distribution by Company Size

- Figure 7.11 Insulin Pump Manufacturers: Distribution by Location of Headquarters (Region)

- Figure 7.12 Insulin Pump Manufacturers: Distribution by Location of Headquarters (Country)

- Figure 7.13 Insulin Pump Manufacturers: Distribution by Company Size and Location of Headquarters

- Figure 7.14 Insulin Pump Manufacturers: Distribution by Type of Company

- Figure 7.15 Most Active Players: Distribution by Number of Insulin Pumps Manufactured

- Figure 8.1 Insulet: Business Segment-wise Revenues and Consolidated Financial Details (USD Million)

- Figure 8.2 MannKind: Business Segment-wise Revenues and Consolidated Financial Details (USD Million)

- Figure 8.3 Medtronic: Business Segment-wise Revenues and Consolidated Financial Details (USD Billion)

- Figure 8.4 Tandem Diabetes Care: Consolidated Financial Details (USD Million)

- Figure 9.1 Roche: Business Segment-wise Revenues and Consolidated Financial Details (CHF Billion)

- Figure 9.2 Ypsomed: Business Segment-wise Revenues and Consolidated Financial Details (CHF Million)

- Figure 10.1 MicroPort: Consolidated Financial Details (USD Million)

- Figure 10.2 MicroTech Medical: Business Segment-wise Revenues and Consolidated Financial Details (RMB Million)

- Figure 10.3 Terumo: Consolidated Financial Details (Yen Billion)

- Figure 11.1 Patent Analysis: Distribution by Type of Patent

- Figure 11.2 Patent Analysis: Cumulative Year-wise Trend by Patent Publication Year, Since-2021

- Figure 11.3 Patent Analysis: Cumulative Year-wise Trend by Patent Application Year, Since-2005

- Figure 11.4 Patent Analysis: Year-wise Distribution of Granted Patents, Patent Applications and Other Patents, Since-2021

- Figure 11.5 Patent Analysis: Distribution by Patent Jurisdiction

- Figure 11.6 Patent Analysis: Distribution by CPC Symbols

- Figure 11.7 Patent Analysis: Cumulative Year-wise Trend by Type of Applicant

- Figure 11.8 Leading Industry Players: Distribution by Number of Patents

- Figure 11.9 Leading Non-industry Players: Distribution by Number of Patents

- Figure 11.10 Leading Patent Assignees: Distribution by Number of Patents

- Figure 11.11 Patent Benchmarking Analysis: Distribution of Patent Characteristics (CPC Codes) by Leading Industry Players

- Figure 11.12 Patent Benchmarking Analysis: Distribution of Leading Industry Players by Patent Characteristics (CPC Codes)

- Figure 11.13 Patent Analysis: Distribution by Patent Age

- Figure 11.14 Insulin Pump: Patent Valuation

- Figure 13.1 Global Insulin Pumps Market, till 2035 (Million Units Sold, USD Billion)

- Figure 13.2 Global Insulin Pumps Market, till 2035: Conservative Scenario (Million Units Sold, USD Billion)

- Figure 13.3 Global Insulin Pumps Market, till 2035: Optimistic Scenario (Million Units Sold, USD Billion)

- Figure 14.1 Insulin Pumps Market: Distribution by Type of Pump, 2017, Current Year and 2035 (USD Billion)

- Figure 14.2 Insulin Pumps Market for Tethered Pumps, till 2035 (Million Units Sold, USD Billion)

- Figure 14.3 Insulin Pumps Market for Patch Pumps, till 2035 (Million Units Sold, USD Billion)

- Figure 15.1 Insulin Pumps Market: Distribution by Degree of Automation, 2017, Current Year and 2035 (USD Billion)

- Figure 15.2 Insulin Pumps Market for Manual Pumps, till 2035 (Million Units Sold, USD Billion)

- Figure 15.3 Insulin Pumps Market for Smart / Automated Pumps, till 2035 (Million Units Sold, USD Billion)

- Figure 16.1 Insulin Pumps Market: Distribution by Type of Battery, 2017, Current Year and 2035 (USD Billion)

- Figure 16.2 Insulin Pumps Market for Replaceable Batteries, till 2035 (Million Units Sold, USD Billion)

- Figure 16.3 Insulin Pumps Market for Rechargeable Batteries, till 2035 (Million Units Sold, USD Billion)

- Figure 17.1 Insulin Pumps Market: Distribution by Type of Diabetes Targeted, 2017, Current Year and 2035 (USD Billion)

- Figure 17.2 Insulin Pumps Market for Type 1 Diabetes, till 2035 (Million Units Sold, USD Billion)

- Figure 17.3 Insulin Pumps Market for Type 1 Diabetes in North America, till 2035 (Million Units Sold, USD Billion)

- Figure 17.4 Insulin Pumps Market for Type 1 Diabetes in the US, till 2035 (Million Units Sold, USD Billion)

- Figure 17.5 Insulin Pumps Market for Type 1 Diabetes in Canada, till 2035 (Million Units Sold, USD Billion)

- Figure 17.6 Insulin Pumps Market for Type 1 Diabetes in Europe, till 2035 (Million Units Sold, USD Billion)

- Figure 17.7 Insulin Pumps Market for Type 1 Diabetes in the UK, till 2035 (Million Units Sold, USD Billion)

- Figure 17.8 Insulin Pumps Market for Type 1 Diabetes in Germany, till 2035 (Million Units Sold, USD Billion)

- Figure 17.9 Insulin Pumps Market for Type 1 Diabetes in Spain, till 2035 (Million Units Sold, USD Billion)

- Figure 17.10 Insulin Pumps Market for Type 1 Diabetes in Italy, till 2035 (Million Units Sold, USD Billion)

- Figure 17.11 Insulin Pumps Market for Type 1 Diabetes in France, till 2035 (Million Units Sold, USD Billion)

- Figure 17.12 Insulin Pumps Market for Type 1 Diabetes in Asia, till 2035 (Million Units Sold, USD Billion)

- Figure 17.13 Insulin Pumps Market for Type 1 Diabetes in China, till 2035 (Million Units Sold, USD Billion)

- Figure 17.14 Insulin Pumps Market for Type 1 Diabetes in Japan, till 2035 (Million Units Sold, USD Billion)

- Figure 17.15 Insulin Pumps Market for Type 1 Diabetes in India, till 2035 (Million Units Sold, USD Billion)

- Figure 17.16 Insulin Pumps Market for Type 1 Diabetes in Pakistan, till 2035 (Million Units Sold, USD Billion)

- Figure 17.17 Insulin Pumps Market for Type 1 Diabetes in Middle East and North Africa, till 2035 (Million Units Sold, USD Billion)

- Figure 17.18 Insulin Pumps Market for Type 1 Diabetes in Israel, till 2035 (Million Units Sold, USD Billion)

- Figure 17.19 Insulin Pumps Market for Type 1 Diabetes in Egypt, till 2035 (Million Units Sold, USD Billion)

- Figure 17.20 Insulin Pumps Market for Type 1 Diabetes in Saudi Arabia, till 2035 (Million Units Sold, USD Billion)

- Figure 17.21 Insulin Pumps Market for Type 1 Diabetes in Latin America, till 2035 (Million Units Sold, USD Billion)

- Figure 17.22 Insulin Pumps Market for Type 1 Diabetes in Brazil, till 2035 (Million Units Sold, USD Billion)

- Figure 17.23 Insulin Pumps Market for Type 1 Diabetes in Argentina, till 2035 (Million Units Sold, USD Billion)

- Figure 17.24 Insulin Pumps Market for Type 1 Diabetes in Mexico, till 2035 (Million Units Sold, USD Billion)

- Figure 17.25 Insulin Pumps Market for Type 2 Diabetes, till 2035 (Million Units Sold, USD Billion)

- Figure 17.26 Insulin Pumps Market for Type 2 Diabetes in North America, till 2035 (Million Units Sold, USD Billion)

- Figure 17.27 Insulin Pumps Market for Type 2 Diabetes in the US, till 2035 (Million Units Sold, USD Billion)

- Figure 17.28 Insulin Pumps Market for Type 2 Diabetes in Canada, till 2035 (Million Units Sold, USD Billion)

- Figure 17.29 Insulin Pumps Market for Type 2 Diabetes in Europe, till 2035 (Million Units Sold, USD Billion)

- Figure 17.30 Insulin Pumps Market for Type 2 Diabetes in the UK, till 2035 (Million Units Sold, USD Billion)

- Figure 17.31 Insulin Pumps Market for Type 2 Diabetes in Germany, till 2035 (Million Units Sold, USD Billion)

- Figure 17.32 Insulin Pumps Market for Type 1 Diabetes in Spain, till 2035 (Million Units Sold, USD Billion)

- Figure 17.33 Insulin Pumps Market for Type 2 Diabetes in Italy, till 2035 (Million Units Sold, USD Billion)

- Figure 17.34 Insulin Pumps Market for Type 2 Diabetes in France, till 2035 (Million Units Sold, USD Billion)

- Figure 17.35 Insulin Pumps Market for Type 2 Diabetes in Asia, till 2035 (Million Units Sold, USD Billion)

- Figure 17.36 Insulin Pumps Market for Type 2 Diabetes in China, till 2035 (Million Units Sold, USD Billion)

- Figure 17.37 Insulin Pumps Market for Type 2 Diabetes in Japan, till 2035 (Million Units Sold, USD Billion)

- Figure 17.38 Insulin Pumps Market for Type 2 Diabetes in India, till 2035 (Million Units Sold, USD Billion)

- Figure 17.39 Insulin Pumps Market for Type 2 Diabetes in Pakistan, till 2035 (Million Units Sold, USD Billion)

- Figure 17.40 Insulin Pumps Market for Type 2 Diabetes in Middle East and North Africa, till 2035 (Million Units Sold, USD Billion)

- Figure 17.41 Insulin Pumps Market for Type 2 Diabetes in Israel, till 2035 (Million Units Sold, USD Billion)

- Figure 17.42 Insulin Pumps Market for Type 2 Diabetes in Egypt, till 2035 (Million Units Sold, USD Billion)

- Figure 17.43 Insulin Pumps Market for Type 2 Diabetes in Saudi Arabia, till 2035 (Million Units Sold, USD Billion)

- Figure 17.44 Insulin Pumps Market for Type 2 Diabetes in Latin America, till 2035 (Million Units Sold, USD Billion)

- Figure 17.45 Insulin Pumps Market for Type 2 Diabetes in Brazil, till 2035 (Million Units Sold, USD Billion)

- Figure 17.46 Insulin Pumps Market for Type 2 Diabetes in Argentina, till 2035 (Million Units Sold, USD Billion)

- Figure 17.47 Insulin Pumps Market for Type 2 Diabetes in Mexico, till 2035 (Million Units Sold, USD Billion)

- Figure 18.1 Insulin Pumps Market: Distribution by Distribution Channel, 2017, Current Year and 2035 (USD Billion)

- Figure 18.2 Insulin Pumps Market for Retail Pharmacies, till 2035 (Million Units Sold, USD Billion)

- Figure 18.3 Insulin Pumps Market for Online Pharmacies, till 2035 (Million Units Sold, USD Billion)

- Figure 18.4 Insulin Pumps Market for Hospital Pharmacies, till 2035 (Million Units Sold, USD Billion)

- Figure 18.5 Insulin Pumps Market for Other Pharmacies, till 2035 (Million Units Sold, USD Billion)

- Figure 19.1 Insulin Pumps Market: Distribution by Geography, 2017, Current Year and 2035 (USD Billion)

- Figure 19.2 Insulin Pumps Market in North America, till 2035 (Million Units Sold, USD Billion)

- Figure 19.3 Insulin Pumps Market in the US, till 2035 (Million Units Sold, USD Billion)

- Figure 19.4 Insulin Pumps Market in Canada, till 2035 (Million Units Sold, USD Billion)

- Figure 19.5 Insulin Pumps Market in Europe, till 2035 (Million Units Sold, USD Billion)

- Figure 19.6 Insulin Pumps Market in the UK, till 2035 (Million Units Sold, USD Billion)

- Figure 19.7 Insulin Pumps Market in Germany, till 2035 (Million Units Sold, USD Billion)

- Figure 19.8 Insulin Pumps Market in Spain, till 2035 (Million Units Sold, USD Billion)

- Figure 19.9 Insulin Pumps Market in Italy, till 2035 (Million Units Sold, USD Billion)

- Figure 19.10 Insulin Pumps Market in France, till 2035 (Million Units Sold, USD Billion)

- Figure 19.11 Insulin Pumps Market in Asia, till 2035 (Million Units Sold, USD Billion)

- Figure 19.12 Insulin Pumps Market in China, till 2035 (Million Units Sold, USD Billion)

- Figure 19.13 Insulin Pumps Market in Japan, till 2035 (Million Units Sold, USD Billion)

- Figure 19.14 Insulin Pumps Market in India, till 2035 (Million Units Sold, USD Billion)

- Figure 19.15 Insulin Pumps Market in Pakistan, till 2035 (Million Units Sold, USD Billion)

- Figure 19.16 Insulin Pumps Market in Middle East and North Africa, till 2035 (Million Units Sold, USD Billion)

- Figure 19.17 Insulin Pumps Market in Israel, till 2035 (Million Units Sold, USD Billion)

- Figure 19.18 Insulin Pumps Market in Egypt, till 2035 (Million Units Sold, USD Billion)

- Figure 19.19 Insulin Pumps Market in Saudi Arabia, till 2035 (Million Units Sold, USD Billion)

- Figure 19.20 Insulin Pumps Market in Latin America, till 2035 (Million Units Sold, USD Billion)

- Figure 19.21 Insulin Pumps Market in Brazil, till 2035 (Million Units Sold, USD Billion)

- Figure 19.22 Insulin Pumps Market in Argentina, till 2035 (Million Units Sold, USD Billion)

- Figure 19.23 Insulin Pumps Market in Mexico, till 2035 (Million Units Sold, USD Billion)

- Figure 19.24 Penetration Growth (P-G) Matrix: Geography

- Figure 19.25 Market Movement Analysis: Geography

- Figure 20.1 Concluding Remarks: Insulin Pumps Market Landscape

- Figure 20.2 Concluding Remarks: Patent Analysis

- Figure 20.3 Concluding Remarks: Market Sizing and Opportunity Analysis

全球胰島素幫浦市場 - 2025 至 2033 年

全球胰島素幫浦市場 - 2025 至 2033 年 全球胰島素幫浦市場:市場規模、佔有率、趨勢分析(按類型、產品、配件、最終用途和地區)、細分市場預測(2025-2030 年)

全球胰島素幫浦市場:市場規模、佔有率、趨勢分析(按類型、產品、配件、最終用途和地區)、細分市場預測(2025-2030 年) 按產品類型(胰島素幫浦、胰島素幫浦耗材和配件)、配銷通路(醫院藥房、零售藥房、線上銷售、糖尿病診所/中心等)和地區分類的胰島素幫浦市場報告2025-2033胰島素幫浦市場:按產品、適應症、配件和分銷管道 - 全球預測 2025-2030

按產品類型(胰島素幫浦、胰島素幫浦耗材和配件)、配銷通路(醫院藥房、零售藥房、線上銷售、糖尿病診所/中心等)和地區分類的胰島素幫浦市場報告2025-2033胰島素幫浦市場:按產品、適應症、配件和分銷管道 - 全球預測 2025-2030 胰島素幫浦市場規模、佔有率、成長分析、按產品類型、按配件、按最終用途、按地區 - 行業預測,2024-2031 年

胰島素幫浦市場規模、佔有率、成長分析、按產品類型、按配件、按最終用途、按地區 - 行業預測,2024-2031 年 全球胰島素幫浦市場(2024-2028)

全球胰島素幫浦市場(2024-2028) 胰島素幫浦研發產品線:發展階段、細分市場、地區和國家、監管途徑、主要參與者(2024年版)快速注射器市場:按產品類型、按應用、按最終用戶、按地區

胰島素幫浦研發產品線:發展階段、細分市場、地區和國家、監管途徑、主要參與者(2024年版)快速注射器市場:按產品類型、按應用、按最終用戶、按地區 胰島素幫浦市場:按類型、產品、配件、疾病、年齡層、最終用戶、通路、地區、機會、預測,2017-2031胰島素幫浦市場- 分產品[設備(管式/繫繩式、無管式)、配件(電池、胰島素儲器或藥筒、胰島素套件插入裝置)]、最終用途(家庭護理、醫院和診所) -全球預測,2024 年- 2032 年

胰島素幫浦市場:按類型、產品、配件、疾病、年齡層、最終用戶、通路、地區、機會、預測,2017-2031胰島素幫浦市場- 分產品[設備(管式/繫繩式、無管式)、配件(電池、胰島素儲器或藥筒、胰島素套件插入裝置)]、最終用途(家庭護理、醫院和診所) -全球預測,2024 年- 2032 年