|

市場調查報告書

商品編碼

1604918

二次電池用黏合劑技術的開發情形及預測(~2035年)<2025> Development Status and Outlook of Binder Technology for Secondary Batteries (~2035) |

||||||

鋰離子電池的特性受電極的影響很大,而優化電極結構是實現優異電池性能的重中之重。目前,不僅鋰離子電池已進入實用階段,研究部門也積極研究和重新審視正負極活性材料。非活性黏合劑不參與電極反應,以較低的重量比(5 wt% 或更低)維持電極的完整性並支持電化學過程。它們與活性材料和導電劑一起,在使電極發揮最佳性能方面發揮重要作用。然而,與其重要性相比,它們卻很少受到關注。

雖然黏合劑只佔電極的一小部分,但它對決定電極的整體性能起著至關重要的作用。它有助於正極和負極中的活性材料和導電劑牢固地黏附在集流體上並提高耐久性。黏合劑必須具備以下特性:(1)在電解質中具有電化學穩定性,(2)具有柔韌性且不溶,以及(3)具有抗氧化腐蝕的能力,尤其是在正極黏合劑的情況下。

因此,需要具有高黏合強度和彈性的功能性黏合劑,以有效地將活性材料和導電劑連接到集流體上,適應體積膨脹,並確保在充放電循環過程中電極結構的穩定性。近年來,隨著對黏合劑篩選和設計的深入了解,重點已從簡單地提供機械穩定性的結構支撐轉移到開發也具有電化學優勢的多功能黏合劑。

近年來,隨著矽基負極材料的應用日益廣泛,研究表明,黏合劑對鋰化反應有顯著的影響,有助於提高電極容量和循環穩定性。因此,我們正在積極開發下一代黏合劑。傳統上,氟樹脂PVDF(聚偏氟乙烯)一直是正極的主要黏合劑,而SBR(丁苯橡膠)或CMC(羧甲基纖維素)一直是負極的主要黏合劑。但由於矽基負極的體積膨脹較大,這些傳統的黏結劑並不適用於矽基材料。

近年來,正極用PTFE(聚四氟乙烯)黏合劑備受關注,負極用PAA(聚丙烯酸)、PI(聚醯亞胺)等水性黏合劑也開始使用。這些水性黏合劑特別適用於利用水溶劑作為電解質的矽基陽極。與傳統黏合劑相比,PAA和PI具有更高的拉伸強度和更強的黏合力,使其更能抵抗矽基負極的體積膨脹。此外,這些黏合劑包覆活性材料並有助於形成穩定的SEI(固體電解質界面)層,從而提高電極的穩定性和循環性能。

PTFE(聚四氟乙烯)是下一代陰極黏合劑,是用於乾電極製程的黏合劑。作為一種具有優異耐化學性和耐熱性的高疏水性材料,預計它將用於乾電極製程和固態電池。

PVDF黏合劑由日本吳羽公司、比利時索爾維公司和法國阿科瑪公司生產,SBR黏合劑由日本瑞翁公司生產,這意味著這些都是高成本材料,並且對海外供應商的依賴程度很高。

韓國Chemtros公司成功實現了正極黏合劑的國產化,韓國Hansol Chemical公司也實現了負極黏合劑的國產化,並向三星SDI和SK On供應。此外,LG化學、錦湖石油化學等也進入了陽極黏合劑供應市場。

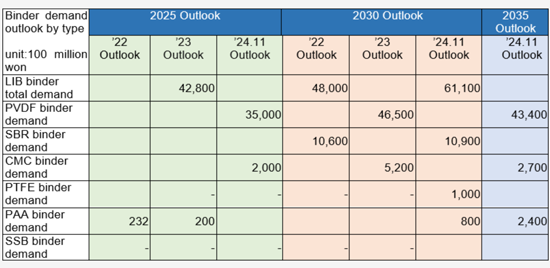

根據SNE Research 2024年11月的全球鋰離子電池黏合劑需求預測,市場預計將從2025年的181.2噸成長到2030年的311.4噸。就價值而言,預計將從2025年的4.4兆韓元增長到2030年的6.11兆韓元。

本報告調查並分析了二次電池黏合劑市場,並根據鋰離子電池市場的前景預測了黏合劑的需求和市場趨勢。

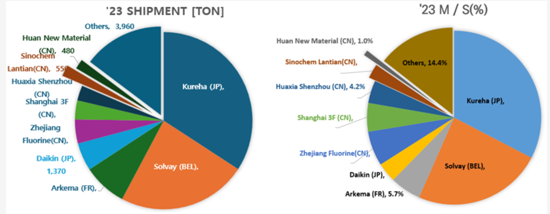

PVDF黏合劑製造商出貨量與市場佔有率(M/S)

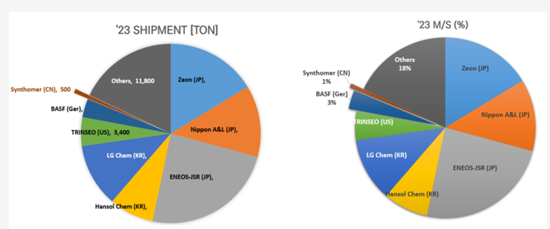

SBR黏合劑製造商出貨量與市場佔有率(M/S)

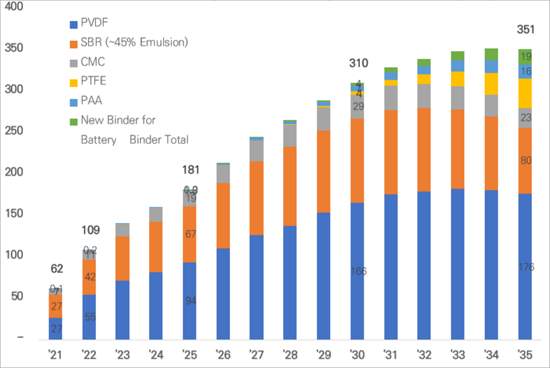

全球LIB用黏合劑(正極+負極)需求的預測(千噸)

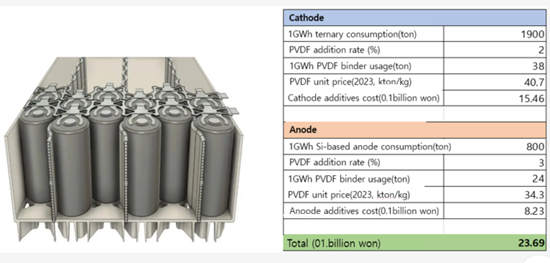

Tesla 4680電池的黏合劑成本分析

- 正極:NCM811,負極:矽基

- 1GWh 電池的 PVDF 陰極黏合劑要求和成本:約。 38噸

- 1GWh 電池的 PAA 陽極黏合劑的要求和成本:約。 24噸

目錄

第1章 黏合劑概要

- 簡介

- 定義、角色、要求

- 類別和類型

- 運作機制

- Binder 失敗機制

- 黏合劑開發的高級策略

- 黏合劑性能評估技術

第2章 黏合劑的類型與研究開發活動

- 正極黏合劑

- 負極黏合劑

- 新一代電池黏合劑 (1)

- 4680 乾式製程黏合劑

- 新一代電池黏合劑 (2)

第3章 黏合劑市場

- 黏合劑市場的整體前景(其他研究人員的前景)

- 全球 PVDF 市場對 LIB 的預測

- 全球電池市場需求展望

- LIB黏合劑的全球需求預測

- 鋰離子電池黏合劑的價格前景

- LIB黏合劑市場規模預測

- 全球主要電池企業對正極黏合劑需求的預測

- 全球陽極黏合劑需求展望:主要電池公司

- 矽基陽極黏合劑市場前景

- 矽基陽極 PAA 黏合劑市場前景

- 全球 LFP 黏合劑需求展望(複合年增長率 12%)

- 特斯拉 4680 電池黏合劑成本分析

- LIB黏合劑製造商的出貨量和M/S

- PVDF 黏合劑製造商的出貨量和 M/S

- SBR 黏合劑製造商的出貨量和 M/S

- CMC黏合劑製造商的出貨量和M/S

第4章 黏合劑製造商情形

- Arkema Group

- BASF SE

- Solvay

- Kureha Corp.

- ZEON Corp.

- JSR Corp.

- Fujian Blue Ocean Co. Ltd (BLUE OCEAN & BLACK STONE)

- Dupont (CMC)

- Ashland Inc.

- MTI Corp.

- TRINSEO

- Xinxiang Jinbang Power Technology Co., Ltd.

- Chongqing Lihong Fine Chemical (CMC Binder Manufacturers)

- Chemtros

- Hansol Chemical

- Kumho Petrochemical

- Daikin Industry

- Nanografi Nano Technology

- Nippon Paper Group

- APV Engineered Coatings LLC

- Sichuan Indigo Materials Science & Technology (INDIGO)

- Guangzhou Songbai Chemical Co (Songbai)

- Nippon A&L Inc.

- Daicel Miraizu Ltd.

- Sinochem Group Co.

- Ube Corp.

- AOT Battery Equipment Technology

- Shanghai Huayi 3F New Materials

- GL Chem

第5章 附錄(參考)(水系正極用黏合劑的成本的分析等)

第6章 參考文獻

The characteristics of LIBs are largely determined by the electrodes, and optimizing the electrode structure is the top priority in order to achieve excellent battery performance. While the active materials of the cathode and anode are being studied and reviewed with much interest not only in currently commercialized LIBs but also in the research field, the inactive binder that does not participate in the electrode reaction maintains the integrity of the electrode with a low weight ratio (less than or equal to 5 wt%) and supports the electrochemical process, and occupies an important position in terms of implementing the performance of the electrode along with the active material and the conductive agent, but it is receiving less attention compared to its importance.

The binder occupies a very small portion of the electrode but plays a crucial role in determining the overall performance of the electrode. It helps active materials and conductive agents in both the cathode and anode adhere firmly to the current collector while enhancing durability. A binder must be (1) electrochemically stable in the electrolyte, (2) possess flexibility and insolubility, and (3) specifically for cathode binders, provide corrosion resistance against oxidation.

Therefore, a functional binder with high bonding strength and elasticity is required to effectively connect the active material and conductive agent to the current collector, accommodate volume expansion, and ensure a stable electrode structure during charge and discharge cycles. Recently, with deeper insights into binder screening and design, research has been shifting its focus from merely serving as a structural support for mechanical stabilization to developing multifunctional binders that also provide electrochemical advantages.

Recently, with the increasing adoption of silicon anode materials, research has shown that binders significantly influence the lithiation reaction, contributing to improved electrode capacity and cycle stability. This has led to active advancements in next-generation binder development. Traditionally, fluoropolymer-based PVDF (Polyvinylidene Fluoride) has been primarily used as a binder for cathodes, while SBR (Styrene-Butadiene Rubber) and CMC (Carboxymethyl Cellulose) have been used for anodes. However, due to the significant volume expansion of silicon anodes, these conventional binders are unsuitable for use with silicon-based materials.

Recently, PTFE (PolyTetraFluoroEthylene) binders have been gaining attention for cathodes, while water-based binders such as PAA (PolyAcrylic Acid) and PI (PolyImide) are increasingly used for anodes. These water-based binders are particularly suitable for silicon anodes, which utilize water-based solvents as electrolytes. Compared to conventional binders, PAA and PI offer higher tensile strength and stronger adhesion, making them more resistant to the volume expansion of silicon anodes. Additionally, these binders encapsulate the active material, helping to form a stable SEI (Solid Electrolyte Interphase) layer, which enhances electrode stability and cycle performance.

The next-generation cathode binder, PTFE (PolyTetraFluoroEthylene), is a binder for dry electrode processes. As a highly hydrophobic material with excellent chemical and thermal resistance, it is expected to gain attention for use in dry electrode processes and solid-state batteries.

PVDF binders are produced by Kureha (Japan), Solvay (Belgium), and Arkema (France), while SBR binders are manufactured by Zeon (Japan), making them high-cost materials with a high reliance on foreign suppliers.

For cathode binders, Chemtros (South Korea) has successfully localized production, while for anode binders, Hansol Chemical (South Korea) has also achieved domestic production and is supplying to Samsung SDI and SK On. Additionally, LG Chem and Kumho Petrochemical are entering the anode binder supply market.

According to SNE Research's global demand forecast for lithium-ion battery binders as of November 2024, the market is expected to grow from 181.2 kton in 2025 to 311.4 kton in 2030. In terms of value, it is projected to increase from KRW 4.4 trillion in 2025 to KRW 6.11 trillion in 2030.

The 2024 edition of the report has been enhanced with a particular focus on solid-state batteries and sodium-ion batteries, which have recently become hot topics. It includes thermal and dispersion properties of binders for these next-generation batteries and provides additional insights into the operational mechanisms and failure mechanisms of binders to improve understanding. Additionally, the report presents a chronological compilation of research on binder design, synthesis, and application in lithium-ion battery electrodes, covering all relevant literature published to date. For those seeking deeper technical details, references to the original papers have been included, allowing for further exploration of the subject.

Based on our lithium-ion battery market outlook, we have projected the demand and market trends for binders. In the appendix, we have included market size estimates and forecasts from external research institutions to help readers gain a comprehensive understanding of the overall market scale. For key binders such as PVDF, SBR, and CMC, the report includes detailed market data from 2021, 2022, and 2023, along with forecasts for 2024, providing a clear view of demand trends over time.

Finally, by compiling the most recent status and key products of binder manufacturers in 2024, this report aims to provide comprehensive insights for researchers and industry professionals. It is expected to contribute significantly to improving battery performance, including energy density, fast-charging capability, and long-term cycle life.

Strong Points of This Report :

- 1. Comprehensive overview and detailed technical content on binders

- 2. Key design and synthesis considerations derived from binder development case studies

- 3. Analysis of binder development trends and case studies for next-generation batteries, including Li-S batteries, solid-state batteries, and sodium-ion batteries (SIBs), in addition to LIBs

- 4. Binder market outlook based on SNE Research's battery forecasts, along with data on the binder market for LFP batteries

- 5. Detailed information on the latest developments and product status of major binder manufacturers

[PVDF Binder Manufacturers' Shipment Volume and Market Share (M/S)]

[SBR Binder Manufacturers' Shipment Volume and Market Share (M/S)]

Global LIB Binder(Cathode + Anode) Demand Forecast (kTon)

[Tesla 4680 Battery Binder Cost Analysis]

- Cathode: NCM811, Anode: Si-based

- PVDF cathode binder requirement and cost for 1 GWh battery: around 38 tons

- PAA anode binder requirement and cost for 1 GWh battery: around 24 tons

Table of Contents

1. Binder Overview

- 1.1. Introduction

- 1.2. Definition, Role, and Requirements

- 1.2.1. Role and Features

- 1.2.1.1. Mechanical Properties

- 1.2.1.1.1. Improvement of Adhesion and Mechanical Strength

- 1.2.1.1.2. Control of Volume Change

- 1.2.1.2. Mitigation of Interface Performance Degradation

- 1.2.1.3. Electrical Properties

- 1.2.1.3.1. Improvement of Electrical Conductivity

- 1.2.1.3.2. Improvement of Ion Conductivity

- 1.2.1.4. Thermal Properties

- 1.2.1.4.1. Improvement of Thermal Stability and Wide Temperature Operation Range

- 1.2.1.5. Dispersion Properties

- 1.2.1.5.1. Improvement of Electrode Homogeneity

- 1.2.1.1. Mechanical Properties

- 1.2.2. Requirements

- 1.2.1. Role and Features

- 1.3. Categories and Types

- 1.3.1. Types

- 1.4. Operation Mechanism

- 1.5. Binder Failure Mechanisms

- 1.6. Advanced Strategies for Binder Development

- 1.6.1. Improvement of Mechanical Bonding Strength

- 1.6.2. Improvement of Chemical Bonding Strength

- 1.6.3. Design of Multifunctional Integrated Binders

- 1.7. Binder Characterization Techniques

- 1.7.1. Evaluation of Binder Distribution and Composition in Cathode

2. Types of Binders and R&D Practices

- 2.1. Binder for Cathodes

- 2.1.1. Non-Aqueous Binders

- 2.1.2. Industry Status of PVDF Cathode Binders

- 2.1.3. Industry Status of (CMC+SBR) Anode Binders

- 2.1.4. Water-based Binders

- 2.1.5. Other Binders

- 2.1.5.1. Conductive Polymer

- 2.1.5.1.1. Polyacrylonitrile(PAN)

- 2.1.5.1. Conductive Polymer

- 2.2. Binders for Anodes

- 2.2.1. Insertable Anode Binder

- 2.2.1.1. Binders for Graphite Electrodes

- 2.2.1.2. Anode Binder for LTO

- 2.2.2. Alloy Anode Binders

- 2.2.2.1. Linear Polymer Binders

- 2.2.2.2. Crosslinked Polymer Binders

- 2.2.2.3. Branched and Extra-Large Polymer Binders

- 2.2.2.4. Conductive Polymer Binders

- 2.2.1. Insertable Anode Binder

- 2.3. Binder for Next-Generation Batteries (1)

- 2.3.1. Binders for Lithium-Sulfur (Li-S) Batteries

- 2.3.2 (4680)Binders for Dry Process

- 2.3.3. Binders for Sodium-Ion Batteries (SIB)

- 2.3.3.1. Development of Binders for SIB

- 2.3.3.2. Conventional Binders

- 2.3.3.2.1. PVDF

- 2.3.3.2.2. PAA

- 2.3.3.2.3. SA(Sodium Alginate)

- 2.3.3.2.4. CMC

- 2.3.3.3. New Binders

- 2.3.3.3.1. Conductive Binders

- 2.3.3.3.2. Cross-linking Binders

- 2.3.3.3.3. Self-healing Binders

- 2.3.3. Binders for Sodium-Ion Batteries (SIB)

- 2.4. Binder for Next-Generation Batteries (2)

- 2.4.1. Binders for Solid Electrolytes

- 2.4.1.1. Overview of All-Solid-State Batteries

- 2.4.1.2. Sulfide-based All-Solid-State Battery Technology

- 2.4.1.3. Manufacturing of All-Solid-State Cells and the Purpose of Binders

- 2.4.1.4. Binder Technology for Cathodes

- 2.4.1.4.1. Binder Technology for Wet Processes

- 2.4.1.4.2. Binder Technology for Dry Processes

- 2.4.1.5. Binder Technology for Electrolyte Layers

- 2.4.1.6. Binder Technology for Anodes

- 2.4.1.6.1. Binder Technology for Graphite-Based Anodes

- 2.4.1.6.2. Next Generation Binder Technology for Anodes

- 2.4.1. Binders for Solid Electrolytes

3. Binder Market

- 3.1. Overall Outlook for the Binders Market(Outlook by Other Researchers)

- 3.2. PVDF Market Outlook for Global LIBs

- 3.2.1. Global Battery Market Demand Outlook

- 3.2.1.1. Global LIB Demand Outlook by Form Factor (GWh, %)

- 3.2.1.2. Global LIB Cathode Material Demand Outlook (GWh, k ton)

- 3.2.1.3. Global LIB Anode Material Demand Outlook (k ton)

- 3.2.2. Global LIB Binder Demand Outlook

- 3.2.3. LIB Binder Price Outlook

- 3.2.4. LIB Binder Market Size Outlook

- 3.2.5. Global Cathode Binder Demand Outlook by Major Battery Companies

- 3.2.6. Global Anode Binder Demand Outlook by Major Battery Companies

- 3.2.7. Market Outlook for Binders for Silicon-based Anodes

- 3.2.8. PAA Binders for Silicon Anode Market Outlook

- 3.2.9. Global LFP Binder Demand Outlook (k ton)(CAGR 12%)

- 3.2.10. Binder cost analysis for 4680 batteries for Tesla

- 3.2.11. Shipments and M/S of LIB Binder Manufacturers

- 3.2.12. Shipments and M/S of PVDF Binder Manufacturers

- 3.2.13. Shipments and M/S of SBR Binder Manufacturers

- 3.2.14. Shipments and M/S of CMC Binder Manufacturers

- 3.2.1. Global Battery Market Demand Outlook

4. Binder Manufacturer Status

- Arkema Group

- BASF SE

- Solvay

- Kureha Corp.

- ZEON Corp.

- JSR Corp.

- Fujian Blue Ocean Co. Ltd (BLUE OCEAN & BLACK STONE)

- Dupont (CMC)

- Ashland Inc.

- MTI Corp.

- TRINSEO

- Xinxiang Jinbang Power Technology Co., Ltd.

- Chongqing Lihong Fine Chemical (CMC Binder Manufacturers)

- Chemtros

- Hansol Chemical

- Kumho Petrochemical

- Daikin Industry

- Nanografi Nano Technology

- Nippon Paper Group

- APV Engineered Coatings LLC

- Sichuan Indigo Materials Science & Technology (INDIGO)

- Guangzhou Songbai Chemical Co (Songbai)

- Nippon A&L Inc.

- Daicel Miraizu Ltd.

- Sinochem Group Co.

- Ube Corp.

- AOT Battery Equipment Technology

- Shanghai Huayi 3F New Materials

- GL Chem

5. Appendix[For reference](Analysis of binder cost for water-based cathodes, etc.)

6. References

2025年全球鋰離子電池黏合劑市場報告

2025年全球鋰離子電池黏合劑市場報告 電池黏合劑市場:按類型、材料、製程、電池類型、應用分類 - 2025-2030 年全球預測鋰電池正極黏合劑市場:按電池類型、材料類型、應用分類 - 2025-2030 年全球預測

電池黏合劑市場:按類型、材料、製程、電池類型、應用分類 - 2025-2030 年全球預測鋰電池正極黏合劑市場:按電池類型、材料類型、應用分類 - 2025-2030 年全球預測 鋰離子電池黏合劑的市場規模、佔有率和趨勢分析報告:按類型、按應用、按材料、按地區和細分市場預測,2024-2030年

鋰離子電池黏合劑的市場規模、佔有率和趨勢分析報告:按類型、按應用、按材料、按地區和細分市場預測,2024-2030年 全球電池黏合劑市場規模研究,按電池類型、材料和區域預測 2022-2032

全球電池黏合劑市場規模研究,按電池類型、材料和區域預測 2022-2032 電池黏合劑市場:依類型、電池類型、材料、應用、行業、地區劃分 - 到2030年的全球預測

電池黏合劑市場:依類型、電池類型、材料、應用、行業、地區劃分 - 到2030年的全球預測 歐洲電池黏合劑市場分析與預測:2022-2031

歐洲電池黏合劑市場分析與預測:2022-2031 亞太電池黏合劑市場(2022-2031):分析與預測

亞太電池黏合劑市場(2022-2031):分析與預測 鋰電池黏合劑HNBR的全球市場(2023年)

鋰電池黏合劑HNBR的全球市場(2023年) 二次電池黏合劑技術發展現況及展望

二次電池黏合劑技術發展現況及展望