|

市場調查報告書

商品編碼

1413700

晶片擴產對美國化學品供應鏈的影響Impact of Chip Expansion on US Chemical Supply-Chain |

||||||

本報告分析了美國半導體製造化學品供應鏈的結構和最新發展,並考慮了近期美國晶片產量增加的趨勢對化學品供應鏈的影響。

主要優點

- 我們提供美國濕式化學品的供需趨勢(數量/收入基礎)、晶圓起始需求以及美國主要晶片代工廠排名等資訊。

- 本報告面向有興趣了解支援晶片製造的美國半導體供應鏈趨勢的任何人,包括業務開發經理、供應鏈經理和金融投資/顧問。

- 單一使用者授權:使用 2FA(雙重認證)為一人提供 techcet.com 的入口網站登入存取權限。使用者可以自由使用購買的報告中的資料進行內部和外部演示,並附有適當的版權聲明。

樣本視圖

目錄

第一章執行摘要

第二章 現狀

- 國內製造業萎縮

- 全球市場佔有率:按國家劃分

- 全球市場趨勢對產業前景的影響

- 材料市場仍然重要

- 美國晶片市場擴張對濕式化學品需求的影響

- 邏輯電路製造對濕化學品的需求增加

- 先進設備帶來的材料增加

- 當前供應商:供應鏈特徵

- 當前供應商:市場排名

- 當前供應商:市場動態

第三章 從預測到現狀的變化

- 已宣布和計劃的鑄造廠擴建:最新信息

- 晶片與科學法 (2022)

- 小費法規定

- 美國新鑄造廠

- 美國鑄造廠/工廠擴建活動

- 美國晶片擴產對產能影響

- 晶片擴容導致濕化學品需求變化

- 濕化學品的需求:給供應商的強烈訊息

第四章 需求、供給與生產能力

- 本報告中使用的術語定義

- 半導體擴張推動材料需求成長

- 預計產能短缺

- 化學品需求預測、製造能力與缺口

- 純度概覽

- 國內晶圓代工廠擴張計畫加速

- 濕化學品需求成長率:依類型

- 化學品需求增加75%

- 濕化學品供需預測

- 硫酸(H2SO)的展望

- 異丙醇(IPA)前景

- 過氧化氫(H2O2)前景

- 鹽酸(HCL)前景

- 氫氧化銨 (NH4OH) 展望

- 氫氟酸(HF)前景

- 磷酸(H3PO4)前景

- 硝酸(HNO3)前景

- 主要供應商概況

第五章 市場調整展望

- 預期市場調整

- 預期行為

- 供應商在美國的工廠擴建活動

- SAMSUNG/TSMC影響力

- 參與者的評論

第六章 進口依賴與挑戰

- 美國對濕化學品進口的依賴

- 導入狀態的變化

- “進口或不進口,這是一個問題。”

第 7 章 包裝與純度

- 不斷變化的包裝要求

- 對超高純度的需求:責任還是機會?

- 化學純度的趨勢

- 提高純度要求

- 運輸管理和需求演變

第八章 TECHCET評估:風險與機會

- TECHCET 評估:一般結果

- TECHCET評估:國際考慮

- TECHCET 評級:供應商擔憂

附錄 A:超高壓化學品製造

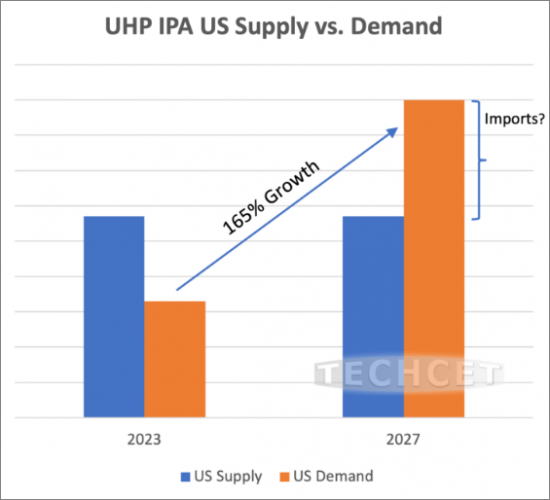

The electronic materials advisory firm providing business and technology information on semiconductor supply chains -- is forecasting a jump in the US domestic share of the semiconductor material market to 13-15% by 2027, as support grows for incoming fab expansions. While this outlook is looking generally positive for the US semiconductor industry, uncertainties with timing expansions have made it difficult for suppliers to plan effectively and CHIPS Act funding does not seem to be helping. In many cases, suppliers are "expansion-ready," and are just awaiting demand signals from chip manufacturers. As a result, much of the incremental US wet chemical capacity is focused on an "import first, build later" strategy, meaning capacity is being used to warehouse, possibly purify, repackage, and distribute imported chemicals, rather than manufacture them domestically. This is the case in regard to IPA, as shown in the graph below. Although the potential growth is high, the timing is uncertain.

TABLE OF CONTENTS

1.0. EXECUTIVE SUMMARY

- 1.1. EXECUTIVE SUMMARY - EXPANSIONS HAVE A MAJOR IMPACT ON WAFER STARTS

- 1.2. EXECUTIVE SUMMARY - CHEMICAL DEMAND GROW ACCELERATES

- 1.3. EXECUTIVE SUMMARY - MATERIALS INCREASES ACROSS THE SPECTRUM

- 1.4. EXECUTIVE SUMMARY - CAPACITY SHORTFALLS EXPECTED

- 1.5. EXECUTIVE SUMMARY - IMPORT DEPENDENCIES

- 1.6. EXECUTIVE SUMMARY - BY CHEMICAL (NO SIGNIFICANT CHANGE FROM 2022)

- 1.7. EXECUTIVE SUMMARY - "IMPORT FIRST, BUILD LATER"

2.0. THE CURRENT STATE OF AFFAIRS

- 2.1. SHRINKING DOMESTIC MANUFACTURING

- 2.2. GLOBAL MARKET SHARE BY COUNTRY

- 2.3. GLOBAL DYNAMICS IMPACT INDUSTRY OUTLOOK

- 2.4. MATERIAL MARKETS REMAIN SIGNIFICANT

- 2.5. IMPACT OF US CHIP EXPANSION ON WET CHEMICAL DEMAND

- 2.6. WET CHEMICAL DEMAND INCREASE LED BY LOGIC MANUFACTURING

- 2.7. ADVANCED DEVICES DRIVE MATERIALS INCREASES

- 2.8. CURRENT SUPPLIERS - SUPPLY CHAIN CHARACTERISTICS

- 2.8.1. CURRENT SUPPLIERS - MARKET RANKINGS

- 2.8.2. CURRENT SUPPLIERS - MARKET DYNAMICS

3.0. THE FORECAST CHANGES TO THE STATUS QUO

- 3.1. ANNOUNCED AND PLANNED FAB EXPANSIONS UPDATE

- 3.2. CHIPS AND SCIENCE ACT OF 2022

- 3.3. CHIPS ACT PROVISIONS

- 3.4. NEW FABS IN THE US

- 3.5. US FAB/PLANT EXPANSION ACTIVITY

- 3.6. US CHIP EXPANSION EFFECT ON CAPACITY

- 3.7. CHIP EXPANSION CHANGES IN WET CHEMICAL DEMAND

- 3.8. WET CHEMICAL DEMAND - A STRONG MESSAGE TO SUPPLIERS

4.0. SUPPLY, DEMAND & CAPACITY

- 4.1. DEFINITIONS OF THE TERMS USED THROUGHOUT THIS REPORT

- 4.2. SEMICONDUCTOR EXPANSION DRIVES MATERIALS DEMAND GROWTH

- 4.3. CAPACITY SHORTFALLS EXPECTED

- 4.4. CHEMICAL DEMAND FORECAST, MANUFACTURING CAPABILITIES & GAP

- 4.5. PURITY OVERVIEW

- 4.6. DOMESTIC FAB EXPANSION PLANS ACCELERATE

- 4.7. DEMAND GROWTH BY WET CHEMICAL TYPE

- 4.8. CHEMICAL VOLUME DEMAND GROWS BY 75%

- 4.9. WET CHEMICAL SUPPLY/DEMAND FORECASTS

- 4.9.1. SULFURIC ACID (H2SO) OUTLOOK

- 4.9.1.1. US IMPORTS OF UHP H2SO4

- 4.9.1.2. H2SO4 US MARKET LANDSCAPE

- 4.9.2. ISOPROPYL ALCOHOL (IPA) OUTLOOK

- 4.9.2.1. US IMPORTS OF UHP IPA

- 4.9.2.2. IPA US MARKET LANDSCAPE

- 4.9.3. HYDROGEN PEROXIDE (H2O2) OUTLOOK

- 4.9.3.1 US IMPORTS OF UHP H2O2

- 4.9.3.2. H2O2 US MARKET LANDSCAPE

- 4.9.4. HYDROCHLORIC ACID (HCL) OUTLOOK

- 4.9.4.1 US IMPORTS OF UHP HCL

- 4.9.4.2. HCL US MARKET LANDSCAPE

- 4.9.5. AMMONIUM HYDROXIDE (NH4OH) OUTLOOK

- 4.9.5.1 US IMPORTS OF UHP NH4OH

- 4.9.5.2. NH4OH US MARKET LANDSCAPE

- 4.9.6. HYDROFLUORIC ACID (HF) OUTLOOK

- 4.9.6.1 US IMPORTS OF UHP HF

- 4.9.6.2. HF US MARKET LANDSCAPE

- 4.9.7. PHOSPHORIC ACID (H3PO4) OUTLOOK

- 4.9.7.1 US IMPORTS OF UHP H3PO4

- 4.9.7.2. H3PO4 US MARKET LANDSCAPE

- 4.9.8. NITRIC ACID (HNO3) OUTLOOK

- 4.9.8.1 US IMPORTS OF UHP HNO3

- 4.9.8.2. HNO3 US MARKET LANDSCAPE

- 4.9.1. SULFURIC ACID (H2SO) OUTLOOK

- 4.10. KEY SUPPLIERS SUMMARY

5.0. ANTICIPATED MARKET ADJUSTMENTS

- 5.1. ANTICIPATED MARKET ADJUSTMENTS

- 5.2. ANTICIPATED ACTIONS

- 5.3. SUPPLIER US PLANT EXPANSION ACTIVITY

- 5.4. THE SAMSUNG/TSMC EFFECT

- 5.5. COMMENTS FROM THE PARTICIPANTS

6.0 DEPENDENCIES & CHALLENGES OF IMPORTS

- 6.1. US DEPENDENCE ON WET CHEMICAL IMPORTS

- 6.2. A CHANGING IMPORT PICTURE

- 6.3. "TO IMPORT OR NOT TO IMPORT, THAT IS THE QUESTION"

7.0 PACKAGING & PURITY

- 7.1. EVOLVING PACKAGING REQUIREMENTS

- 7.2. ULTRA HIGH PURITY DEMANDS - A LIABILITY OR OPPORTUNITY?

- 7.3. CHEMICAL PURITY TRENDS

- 7.3.1. EVER INCREASING PURITY REQUIREMENTS

- 7.4 SHIP TO CONTROL & EVOLVING REQUIREMENTS

8.0 TECHCET'S ASSESSMENT OF RISKS AND OPPORTUNITIES

- 8.1. TECHCET'S ASSESSMENT - GENERAL OBSERVATIONS

- 8.2. TECHCET'S ASSESSMENT - INTERNATIONAL CONSIDERATIONS

- 8.3. TECHCET'S ASSESSMENT - SUPPLIER CONCERNS

APPENDIX A: MANUFACTURING UHP CHEMICALS

FIGURES

- FIGURE 1: 2023 US CHIP FAB CAPACITY - 33.9 M WAFERS (200MM EQUIV.)

- FIGURE 2: 2027 US CHIP FAB CAPACITY - 46.4 M WAFERS (200MM EQUIV.)

- FIGURE 3: US ANNUAL WAFER CAPACITY FORECAST 2023-2027 (200MM EQUIV.)

- FIGURE 4: SEMICONDUCTORS LEAD US EXPORTS

- FIGURE 5: US SEMICONDUCTOR INDUSTRY IS STRONG, DESPITE LIMITED MANUFACTURING PRESENCE. (REVENUES AS A PERCENT OF TOTAL SALES BY HQ LOCATION)

- FIGURE 6: 2022 GLOBAL SEMICONDUCTOR MATERIALS MARKET BY SEGMENT (US$71.7B)

- FIGURE 7: US WET CHEMICAL DEMAND BY CHIP FABRICATOR 2023-2027 (200MM EQUIV. WAFERS)

- FIGURE 8: US WAFER START CAPACITY FOR LOGIC DEVICES BY NODE, 2023-2027 (200MM EQUIV. WAFERS)

- FIGURE 9: US WAFER CAPACITY FOR MEMORY DEVICES BY NODE, 2023-2027 (200MM EQUIV. WAFERS)

- FIGURE 10: SEMICONDUCTOR DEMAND AS A PERCENT OF TOTAL

- FIGURE 11: INVESTMENT IN GLOBAL CHIP EXPANSIONS 2022-2027 ($500 B USD)

- FIGURE 12: US CHIP EXPANSIONS 2023-2027

- FIGURE 13: CHIP EXPANSION EXPECTED TO GROW ANNUAL CAPACITY >35% TO 46.4M (200MM EQUIV.)

- FIGURE 14: WET CHEMICAL DEMAND WILL RISE 75% FROM LEADING CHIP FABS 2023-2027

- FIGURE 15: US WAFER START GROWTH BY DEVICE TYPE AND NODE

- FIGURE 16: US 2023 -- 2027 US WET CHEMICAL DEMAND FORECAST

- FIGURE 17: US H2SO4 SUPPLY VS. DEMAND VOLUME (MKG)

- FIGURE 18: US H2SO4 UHP GRADE -- DEPENDENCE ON IMPORTS

- FIGURE 19: US H2SO4: 71% GROWTH, 11% CAGR

- FIGURE 20: US SUPPLY VS. DEMAND VOLUME (MKG)

- FIGURE 21: US IPA UHP GRADE -- INCREASING DEPENDENCE ON IMPORTS

- FIGURE 22: US IPA VOLUME DEMAND 92% GROWTH 14% CAGR

- FIGURE 23: US H2O2 SUPPLY VS. DEMAND (MKG)

- FIGURE 24: US H2O2 UHP GRADE -- DEPENDENCE ON IMPORTS

- FIGURE 25: US H2O2 US VOLUME DEMAND 80% GROWTH 13% CAGR

- FIGURE 26: US HCL SUPPLY VS. DEMAND (MKG)

- FIGURE 27: US HCL UHP GRADE -- DEPENDENCE ON IMPORTS

- FIGURE 28: US HCI US DEMAND 70% GROWTH 11% CAGR

- FIGURE 29: US NH4OH SUPPLY VS. DEMAND (MKG)

- FIGURE 30 US NH4OH UHP GRADE DEPENDENCE ON IMPORTS

- FIGURE 31: US NH4OH US VOLUME DEMAND 77% GROWTH 12% CAGR

- FIGURE 32: US HF SUPPLY VS. DEMAND (MKG)

- FIGURE 33: US HF UHP GRADEDEPENDENCE ON IMPORTS

- FIGURE 34: US HF VOLUME DEMAND 59% GROWTH, 10% CAGR

- FIGURE 35: US H3PO4 SUPPLY VS. DEMAND (MKG)

- FIGURE 36: US H3PO4 UHP GRADE - DEPENDENCY ON IMPORTS

- FIGURE 37: US H3PO4 US VOLUME DEMAND79% GROWTH, 12% CAGR

- FIGURE 38: US HNO3 SUPPLY VS. DEMAND (MKG)

- FIGURE 39: US HNO3 UHP GRADE - DEPENDENCE ON IMPORTS

- FIGURE 40: US HNO3 US VOLUME DEMAND 33% GROWTH, 6% CAGR

- FIGURE 41: RENDERING OF TSMC'S ARIZONA FACILITY

- FIGURE 42: CHINA TO US OCEAN FREIGHT EXPORT PRICE TRENDS

- FIGURE 43: SHIP TO CONTROL FOR PROCESS CHEMICALS EXAMPLE

TABLES

- TABLE 1: CHEMICAL VOLUME GROWTH 2023-2027

- TABLE 2: US WET CHEMICAL EXCESS/SHORTFALLS EXPECTED

- TABLE 3: DEPENDENCY OF UHP PRODUCTS ON IMPORTS WITHOUT ADDITIONAL DOMESTIC CAPACITY

- TABLE 4: US DOMESTIC TIER I TOP 3 SUPPLIERS BY VOLUME SUPPLIED

- TABLE 5: US FAB RAMP FORECAST (200MM EQUIV.)

- TABLE 6: WET CHEMICALS WITH THE HIGHEST DEMAND GROWTH IN THE US 2027/2023

- TABLE 7: CAPACITY SHORTFALLS EXPECTED (SAME AS TABLE 2)

- TABLE 8: UHP AND IC GRADE SPLIT USED FOR GRAPHS

- TABLE 9: US SEMICONDUCTOR CHEMICAL VOLUME GROWTH 2027/2023

- TABLE 10: SUMMARY OF KEY US SUPPLIERS

- TABLE 11: SUPPLIER US CHEMICAL PLANT EXPANSION ACTIVITY, PAGE 1 OF 3

- TABLE 11: SUPPLIER US CHEMICAL PLANT EXPANSION ACTIVITY, PAGE 2 OF 3

- TABLE 11: SUPPLIER US CHEMICAL PLANT EXPANSION ACTIVITY, PAGE 3 OF 3

- TABLE 12: COMMENTS FROM THE SELECTED PARTICIPANTS

- TABLE 13: 2027 IMPORTS AS A PERCENTAGE OF UHP AND TOTAL DEMAND

- TABLE 14: INCREASING DEPENDENCY OF UHP PRODUCTS ON IMPORTS

- TABLE 15: EVOLVING PACKAGING REQUIREMENTS

- TABLE 16: PURITY REQUIREMENTS

- TABLE 17: COMMENTS FROM THE SELECTED PARTICIPANTS

非接觸IC卡晶片的全球市場:2030年前的預測

非接觸IC卡晶片的全球市場:2030年前的預測 裸晶運輸、搬運、加工和儲存的全球市場預測(截至 2030 年):按產品、應用和地區進行分析

裸晶運輸、搬運、加工和儲存的全球市場預測(截至 2030 年):按產品、應用和地區進行分析 裸晶運輸、裝卸、加工和儲存市場:按產品類型和應用分類的全球預測 - 2025-2030

裸晶運輸、裝卸、加工和儲存市場:按產品類型和應用分類的全球預測 - 2025-2030 多晶片模組市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、垂直產業、地區和競爭細分,2019-2029 年

多晶片模組市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、垂直產業、地區和競爭細分,2019-2029 年 2024 年感測器集線器全球市場報告

2024 年感測器集線器全球市場報告 智慧功率晶片市場報告:2030 年趨勢、預測與競爭分析

智慧功率晶片市場報告:2030 年趨勢、預測與競爭分析 行動半導體市場,按類型、應用和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測

行動半導體市場,按類型、應用和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測 2024-2032 年按產品、應用和地區分類的裸晶片運輸和處理以及加工和儲存市場報告

2024-2032 年按產品、應用和地區分類的裸晶片運輸和處理以及加工和儲存市場報告 可信任運算晶片市場,按組件、按部署類型、按應用、按最終用戶、按國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測

可信任運算晶片市場,按組件、按部署類型、按應用、按最終用戶、按國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測 嵌入式儲存控制晶片市場,按記憶體類型、儲存容量、應用、國家和地區分類 - 2024-2032 年行業分析、市場規模、市場佔有率和預測

嵌入式儲存控制晶片市場,按記憶體類型、儲存容量、應用、國家和地區分類 - 2024-2032 年行業分析、市場規模、市場佔有率和預測