|

市場調查報告書

商品編碼

1646800

歐洲的家具市場The Furniture Industry in Europe |

|||||||

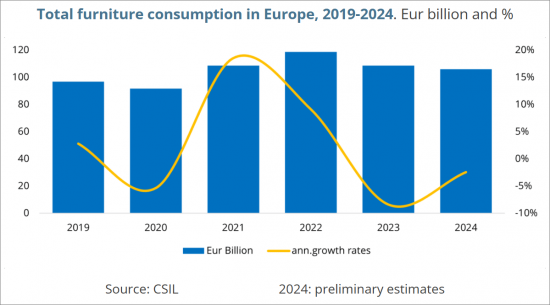

作為世界第2位的家具市場的歐洲的消費額約1,060億歐元以(全球市場的4分之一以上),作為生產,市場規模,世界貿易的極為重要的據點,在全球家具產業中接連佔著重要的地位。

從2023年到2024年儘管是嚴苛的市場環境,這個部門證明那個復甦力,被高度的整合和市場集中支撐,超過大流行前的水準推移著。與以歐洲規模開展事業的大間零售產業連鎖廠商壟斷市場做著,受到著市場內部強的團結力和確立的貿易網路的恩惠。這個結構性的強度,也成為不僅僅支撐市場穩定性,推進域內的進出口大幅度的集中的原動力。同時,歐洲反映國際貿易能放的積極的作用,對全球市場維持著持續性開放性。

預測著2025年的家具需求停滯,中期性慢慢有復甦的徵兆。

本報告提供歐洲的家具市場相關調查,彙整2019年~2024年時的家具生產,消費,進口,出口趨勢,各國排行榜,2025年和2026年的家具市場預測,主要家具製造商簡介等資料。

亮點

目錄(摘要)

摘要整理

歐洲的家具產業

- 全球家具產業上歐洲所扮演的角色

- 歐洲和其他地區。家具的生產,消費,出口,進口

- 歐洲的整合流程

- 國際家具貿易,按家具進口的目的地和原產地的家具出口

- 歐洲的家具生產實際成果

- 主要的家具製造國(義大利,德國,波蘭英國,法國)的說明

- EU家具製造商競爭力的影響因素

- 歐洲的家具競爭系統

- 最近的歐洲的家具製造商策略,M&A

- 歐洲的上場家具製造商最新資料

- 歐洲的前50大廠商:總銷售額排行榜

- 歐洲的家具市場趨勢:2019年~2024年

- 市場資訊來源

- 國內生產,歐盟市場整合,進口流通量

- 貿易收支

- 市場開放度的高漲

- 出口意願

- 歐洲的家具生產的各領域明細

- 家具子區隔趨勢

各國分析

- 市場概況及宏觀經濟趨勢、家俱生產、消費、進口、出口、國家排名、家具市場預測、貿易夥伴、各細分市場的家具消費和生產、製造系統以及主要家具製造商的簡介:

- 奧地利、比利時、保加利亞、克羅埃西亞、賽普勒斯、捷克、丹麥、愛沙尼亞、芬蘭、法國、德國、希臘、匈牙利、愛爾蘭、義大利、拉脫維亞、立陶宛、馬爾他、荷蘭、挪威、波蘭、葡萄牙、羅馬尼亞、斯洛伐克、斯洛維尼亞、西班牙、瑞典、瑞士、英國

超過2400公司的歐洲的家具製造商簡介:

- 活動

- 產品系列

- 銷售額範圍

- 員工數

- 電子郵件地址

- 網站

方法論的註解

Part of the CSIL Country Furniture Outlook Series covering 100 countries at present with CSIL furniture industry insights, "The Furniture Industry in Europe" contains all the main statistics and indicators useful to analyze the furniture sector in Europe and in 30 European countries: Austria, Belgium-Lux, Bulgaria, Croatia, Cyprus, Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Ireland, Italy, Latvia, Lithuania, Malta, the Netherlands, Norway, Poland, Portugal, Romania, Slovakia, Slovenia, Spain, Sweden, Switzerland, the UK.

THE FURNITURE INDUSTRY IN EUROPE: INSIGHTS AND FORECASTS

The first part of this furniture market report goes in-depth into the future perspectives for the European furniture sector with a particular focus on the green and digital transitions shaping the industry.

European Furniture Market: Key Data and Trends

The role of Europe in the global furniture context is analysed with historical series of basic data (furniture production, consumption, and trade 2019-2024), the European furniture production performance and future perspectives, the main factors affecting the competitiveness of manufacturers (labor cost, availability of raw materials and components, investments in technology and machinery, innovations, recycling, sustainability, and circularity), imports penetration, exports orientation, description of the main furniture manufacturing countries.

The European furniture market potential, development insights, and Furniture market trends are analysed through a historical series of furniture consumption data and future perspectives of the furniture sector in Europe, with consumption forecasts for 2025 and 2026.

The Furniture manufacturing system and trends in the development of furniture production by segment (upholstered furniture, kitchen furniture, office furniture, furniture for the bedroom &dining-living room, other furniture) with trends in furniture sub-segments (available data up to 2023).

Top Furniture Manufacturers in Europe

The competitive system in Europe is covered with the recent European furniture manufacturers' strategies, mergers, and acquisitions (M&A).

The competitive system analysis includes figures for the leading 50 European furniture companies (company name, headquarters' country, furniture specialization, total turnover, and the number of employees, share of furniture on total sales) ranked by their turnover.

Financial performance analysis of a selection of publicly listed European furniture manufacturers, including aggregated key annual (2019-2023) figures such as total revenue, EBITDA, total liabilities, total shareholders' equity, and the Debt-to-Equity Ratio, and quarterly (2024) data for total revenue, gross profit, operating expense, operating income, total expense, EBIT and EBITDA, is also provided.

Over 2400 short profiles of furniture manufacturers are also provided, with information on their activity, product portfolio, turnover range, employees range, general email address -when available- and website.

COUNTRY ANALYSIS: FURNITURE INDUSTRY REPORTS FOR 30 EUROPEAN COUNTRIES

For each considered country (Austria, Belgium-Lux, Bulgaria, Croatia, Cyprus, Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Ireland, Italy, Latvia, Lithuania, Malta, the Netherlands, Norway, Poland, Portugal, Romania, Slovakia, Slovenia, Spain, Sweden, Switzerland, the United Kingdom) this study offers a complete report including:

- Market Outline and macroeconomic trends

- Production, consumption, imports, and exports of furniture for the time series 2019-2024

- Comparison with the European furniture sector: country rankings on production, consumption, imports, and exports

- Furniture market forecasts for 2025 and 2026

- Trading partners: the origin of furniture imports and furniture export destination

- Value of furniture consumption and production by segment (upholstered furniture, office furniture, kitchen furniture, Furniture for bedroom, dining-living room * and other furniture)

- Manufacturing system: number of furniture firms, and size

- Short profiles of leading furniture manufacturers

Types of furniture covered: Office furniture, Upholstered furniture, Non-upholstered seats, Kitchen furniture, Bedroom furniture, Dining and living room furniture, and Other Furniture.

* For Bulgaria, Croatia, Estonia, Latvia, Lithuania, Malta, and Slovenia, the furniture consumption and production breakdown by segment is available only by upholstered furniture, office furniture, kitchen furniture, and other furniture.

Selected companies

Among the leading furniture manufacturers mentioned in this study: Aquinos, BRW Black Red White, Cotta Collection, Ekornes, Friul Intagli, Howden Joinery, IKEA, Lifestyle Design, Natuzzi, Nobilia, Nowy Styl, Polipol, Schmidt Groupe, Schuller, Fournier, Steelcase, Welle Holding.

Highlights:

Europe, the world's second-largest furniture market with a consumption value of around EUR 106 billion (over one-quarter of the global market), continues to hold a crucial position in the global furniture industry, acting as a pivotal hub for production, market size, and world trade.

Despite difficult market conditions in 2023-2024, the sector has proven its resilience, staying above pre-pandemic levels, supported by a high level of integration, and market concentration. Dominated by major retail chains and manufacturers operating on a European scale, the market benefits from strong internal cohesion and a well-established trade network. This structural strength not only underpins its stability but also drives the substantial concentration of export and import flows within the region. At the same time, Europe maintains an ongoing openness to global markets, reflecting its proactive role in international trade.

CSIL forecasts stagnant furniture demand in 2025, with signs of a gradual recovery in the medium term.

TABLE OF CONTENTS (ABSTRACT)

EXECUTIVE SUMMARY

- The future perspectives for the European furniture sector

- The global macroeconomic context and furniture market forecasts in Europe

- Green and digital transitions: a hot topic for the European furniture industry

THE EUROPEAN FURNITURE SECTOR

- The Role of Europe in the Global Furniture Context

- Europe and the rest of the world. Furniture production, consumption, exports, imports

- The integration process within Europe

- International furniture trade, furniture exports by destination and origin of furniture imports

- The European furniture production performance

- Description of the main furniture manufacturing countries (Italy, Germany, Poland, The United Kingdom, France)

- Factors affecting the competitiveness of EU furniture producers

- The furniture competitive system in Europe

- Recent European furniture manufacturers' strategies, M&A

- Recent figures of publicly listed European furniture manufacturers

- The TOP 50 European manufacturers. Ranking by total turnover

- European furniture market performance 2019-2024

- Market sources

- National production, EU market integration and import flows

- Trade balance

- The growing degree of market openness

- The export orientation

- European furniture production by segment

- Trends in furniture sub-segments

COUNTRY ANALYSIS

- Market outline and macroeconomic trends, Production, consumption, imports, and exports of furniture, Country rankings, Furniture market forecasts, Trading partners, Furniture consumption and production by segment, Manufacturing system, and short profiles of leading furniture manufacturers for:

- Austria, Belgium, Bulgaria, Croatia, Cyprus, Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Ireland, Italy, Latvia, Lithuania, Malta, Netherlands, Norway, Poland, Portugal, Romania, Slovakia, Slovenia, Spain, Sweden, Switzerland, United Kingdom

SHORT PROFILES OF OVER 2400 EUROPEAN FURNITURE COMPANIES:

- activity

- product portfolio

- turnover range

- employees range

- e-mail address

- website

METHODOLOGICAL NOTES

印度家具業

印度家具業 商務用家具零售市場報告:趨勢、預測和競爭分析(至 2031 年)座椅整理器市場報告:2031 年趨勢、預測與競爭分析

商務用家具零售市場報告:趨勢、預測和競爭分析(至 2031 年)座椅整理器市場報告:2031 年趨勢、預測與競爭分析 家具,全球市場 2025-2029

家具,全球市場 2025-2029 客廳和餐廳市場規模、佔有率及成長分析(按產品類型、材料、分銷管道、最終用戶和地區)—2025-2032 年行業預測

客廳和餐廳市場規模、佔有率及成長分析(按產品類型、材料、分銷管道、最終用戶和地區)—2025-2032 年行業預測 全球高度可調辦公桌市場研究報告 - 產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年

全球高度可調辦公桌市場研究報告 - 產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年 全球 K-12 家具市場(2025-2029)智慧家具市場規模、佔有率和成長分析(按產品、分銷管道、應用和地區)- 2025-2032 年產業預測

全球 K-12 家具市場(2025-2029)智慧家具市場規模、佔有率和成長分析(按產品、分銷管道、應用和地區)- 2025-2032 年產業預測 全球教育家具市場:按材料、產品、應用、分銷管道和地區進行分析,規模、趨勢、COVID-19 的影響以及 2030 年預測

全球教育家具市場:按材料、產品、應用、分銷管道和地區進行分析,規模、趨勢、COVID-19 的影響以及 2030 年預測 全球竹家具市場

全球竹家具市場