|

市場調查報告書

商品編碼

1665037

汽車座椅熱舒適系統市場機會、成長動力、產業趨勢分析與預測 2025 - 2034Automotive Seating Thermal Comfort System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

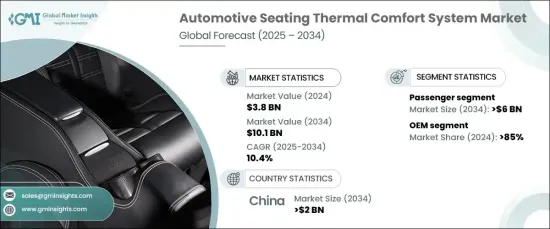

2024 年全球汽車座椅熱舒適系統市場價值為 38 億美元,預計 2025 年至 2034 年期間將以 10.4% 的強勁複合年成長率成長。加熱、通風和冷卻座椅等功能曾經是高階車型的專屬,現在已成為中檔和經濟型汽車的標準配備。隨著駕駛員和乘客越來越重視旅途中的舒適度,汽車製造商正在整合先進的熱系統以滿足這些不斷變化的期望。

對個人化舒適體驗的需求不斷成長,與對創新汽車技術的日益重視一致。汽車製造商正致力於整合智慧感測器和節能系統,以在降低能耗的同時保持最佳舒適度。這些進步不僅提高了使用者滿意度,而且有助於整體車輛的永續性。此外,全球汽車產量的成長、城市化以及長途通勤的日益普及也使市場受益,所有這些都推動了對更舒適座椅解決方案的需求。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 38億美元 |

| 預測值 | 101億美元 |

| 複合年成長率 | 10.4% |

電動和混合動力汽車(EV)的日益普及已成為汽車座椅熱舒適系統市場的另一個關鍵驅動力。與傳統的內燃機汽車不同,電動車沒有引擎產生的廢熱,因此專用的座椅加熱和冷卻系統對於保持車廂舒適度至關重要。為了滿足電動車所需的能源效率標準,製造商正在開發創新的熱技術,以最小的功耗提供卓越的舒適度。這種轉變凸顯了先進座椅解決方案在更廣泛的電動車生態系統中的重要性,因為汽車製造商的目標是在不影響能源效率的情況下提升車艙體驗。

就車輛類型而言,市場分為乘用車和商用車。 2024 年,乘用車佔了 70% 的市場佔有率,預計到 2034 年將創下 60 億美元的市場規模。隨著中檔和高檔乘用車擴大配備加熱和冷卻座椅等功能,該領域預計將在未來幾年保持領先地位。

根據銷售管道,市場分為原始設備製造商(OEM)和售後市場。 2024 年,OEM 憑藉其將熱舒適系統無縫整合到車輛設計中的能力,佔據了 85% 的市場佔有率。與供應商建立牢固的合作夥伴關係使 OEM 能夠以有競爭力的價格提供先進的解決方案,同時確保跨型號的可靠性和相容性。

2024 年,中國佔據汽車座椅熱舒適系統市場的主導地位,佔全球佔有率的 60%,預計到 2034 年將創下 20 億美元的市場規模。隨著中國在電動車生產和普及方面繼續保持領先地位,對先進的熱舒適系統的需求也隨之成長。其強大的供應鏈和具有成本效益的生產能力進一步鞏固了中國在全球市場中的重要地位。

報告內容

第 1 章:方法論與範圍

- 研究設計

- 研究方法

- 資料收集方法

- 基礎估計和計算

- 基準年計算

- 市場估計的主要趨勢

- 預測模型

- 初步研究與驗證

- 主要來源

- 資料探勘來源

- 市場定義

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 供應商概況

- OEM汽車座椅熱舒適系統製造商

- 售後市場供應商

- 經銷商

- 最終用戶

- 利潤率分析

- 定價分析

- 專利格局

- 汽車座椅熱舒適系統的成本明細

- 技術與創新格局

- 重要新聞及舉措

- 監管格局

- 衝擊力

- 成長動力

- 對車輛舒適性和豪華性的需求不斷增加

- 電動和混合動力汽車(EV)的普及率不斷上升

- 溫度控制與能源效率智慧技術的進步

- 擴大新興經濟體的汽車生產

- 產業陷阱與挑戰

- 先進熱舒適系統成本高,限制了其在經濟型車輛的應用

- 售後市場改造熱舒適系統的複雜性與成本

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第 5 章:市場估計與預測:按材料,2021 - 2034 年

- 主要趨勢

- 皮革

- 織物

- 合成材料

- 其他

第6章:市場估計與預測:依工藝,2021 - 2034 年

- 主要趨勢

- 座椅加熱

- 座椅冷卻

- 座椅通風

- 整合系統

第7章:市場估計與預測:依車型,2021 - 2032 年

- 主要趨勢

- 搭乘用車

- 掀背車

- 轎車

- 越野車

- 商用車

- 輕型商用車 (LCV)

- 重型商用車 (HCV)

第 8 章:市場估計與預測:按銷售管道,2021 - 2032 年

- 主要趨勢

- OEM

- 售後市場

第 9 章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 義大利

- 俄羅斯

- 北歐

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳新銀行

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東及非洲

- 阿拉伯聯合大公國

- 南非

- 沙烏地阿拉伯

第10章:公司簡介

- Adient

- BorgWarner

- Brose Fahrzeugteile

- Continental

- Denso

- Faurecia

- Gentherm

- Grammer

- Hyundai Transys

- Johnson Controls International

- Lear

- Magna International

- NHK Spring

- RECARO Automotive

- Rochling

- Tachi-S

- Toyota Boshoku

- TS TECH

- Yanfeng Automotive Interiors

- Zentex Industries

The Global Automotive Seating Thermal Comfort System Market was valued at USD 3.8 billion in 2024 and is forecasted to expand at a robust CAGR of 10.4% from 2025 to 2034. This growth is primarily driven by escalating consumer preferences for comfort and luxury features in modern vehicles. Once exclusive to high-end models, features like heated, ventilated, and cooled seats are now becoming standard in mid-range and economy cars. As drivers and passengers increasingly prioritize enhanced comfort during their journeys, automakers are integrating advanced thermal systems to meet these evolving expectations.

The rising demand for personalized comfort experiences aligns with the growing emphasis on innovative automotive technologies. Automakers are focusing on integrating smart sensors and energy-efficient systems that maintain optimal comfort while reducing energy consumption. These advancements not only enhance user satisfaction but also contribute to overall vehicle sustainability. Additionally, the market benefits from rising global automotive production, urbanization, and the increasing prevalence of long commutes, all of which drive demand for more comfortable seating solutions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.8 Billion |

| Forecast Value | $10.1 Billion |

| CAGR | 10.4% |

The growing popularity of electric and hybrid vehicles (EVs) has emerged as another pivotal driver for the automotive seating thermal comfort system market. Unlike traditional vehicles powered by internal combustion engines, EVs lack engine-generated waste heat, making dedicated seat heating and cooling systems essential for maintaining cabin comfort. To meet the energy efficiency standards required by EVs, manufacturers are developing innovative thermal technologies that deliver superior comfort with minimal power consumption. This shift underscores the importance of advanced seating solutions in the broader EV ecosystem, as automakers aim to enhance cabin experiences without compromising energy efficiency.

In terms of vehicle type, the market is segmented into passenger and commercial vehicles. Passenger vehicles commanded 70% of the market share in 2024 and are expected to generate USD 6 billion by 2034. This dominance is attributed to the high production volumes of passenger cars globally and the rising consumer demand for premium features across various price segments. As mid-range and premium passenger vehicles increasingly include features such as heated and cooled seats, the segment is poised to maintain its leadership in the coming years.

By sales channel, the market is divided into original equipment manufacturer (OEM) and aftermarket segments. In 2024, OEMs captured 85% of the market share, leveraging their ability to seamlessly integrate thermal comfort systems into vehicle designs. Strong partnerships with suppliers allow OEMs to deliver advanced solutions at competitive prices while ensuring reliability and compatibility across models.

China dominated the automotive seating thermal comfort system market in 2024, representing 60% of the global share, and is projected to generate USD 2 billion by 2034. The country's unmatched automotive production capacity and competitive manufacturing infrastructure drive this growth. As China continues to lead in EV production and adoption, the demand for sophisticated thermal comfort systems grows in parallel. Its robust supply chain and cost-effective production capabilities further cement China's position as a pivotal player in the global market.

Report Content

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 OEM Automotive seating thermal comfort system manufacturers

- 3.2.2 Aftermarket providers

- 3.2.3 Distributors

- 3.2.4 End users

- 3.3 Profit margin analysis

- 3.4 Pricing analysis

- 3.5 Patent landscape

- 3.6 Cost Breakdown of automotive seating thermal comfort systems

- 3.7 Technology & innovation landscape

- 3.8 Key news & initiatives

- 3.9 Regulatory landscape

- 3.10 Impact forces

- 3.10.1 Growth drivers

- 3.10.1.1 Increasing demand for comfort and luxury features in vehicles

- 3.10.1.2 Rising adoption of electric and hybrid vehicles (EVs)

- 3.10.1.3 Advancements in smart technologies for temperature control and energy efficiency

- 3.10.1.4 Expanding vehicle production in emerging economies

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 High cost of advanced thermal comfort systems limiting adoption in economy vehicles

- 3.10.2.2 Complexity and cost of retrofitting thermal comfort systems in the aftermarket

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter’s analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Material, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Leather

- 5.3 Fabric

- 5.4 Synthetic materials

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Process, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Seat heating

- 6.3 Seat cooling

- 6.4 Seat ventilation

- 6.5 Integrated systems

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2032 ($Bn)

- 7.1 Key trends

- 7.2 Passenger vehicles

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicles

- 7.3.1 Light commercial vehicles (LCV)

- 7.3.2 Heavy commercial vehicles (HCV)

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2021 - 2032 ($Bn)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Adient

- 10.2 BorgWarner

- 10.3 Brose Fahrzeugteile

- 10.4 Continental

- 10.5 Denso

- 10.6 Faurecia

- 10.7 Gentherm

- 10.8 Grammer

- 10.9 Hyundai Transys

- 10.10 Johnson Controls International

- 10.11 Lear

- 10.12 Magna International

- 10.13 NHK Spring

- 10.14 RECARO Automotive

- 10.15 Rochling

- 10.16 Tachi-S

- 10.17 Toyota Boshoku

- 10.18 TS TECH

- 10.19 Yanfeng Automotive Interiors

- 10.20 Zentex Industries

全球座椅通風市場:市場佔有率和排名、總銷售量和需求預測(2025-2031)

全球座椅通風市場:市場佔有率和排名、總銷售量和需求預測(2025-2031) 全球汽車座椅加熱市場 -市場佔有率和排名、總收入、需求預測(2025-2031 年)

全球汽車座椅加熱市場 -市場佔有率和排名、總收入、需求預測(2025-2031 年) 越野車座椅市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

越野車座椅市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 2025年全球兒童安全座椅及配件市場報告

2025年全球兒童安全座椅及配件市場報告 2025 年至 2029 年全球越野車座椅市場

2025 年至 2029 年全球越野車座椅市場 汽車座椅市場規模、佔有率和成長分析(按裝飾材料、座椅類型、車輛類型和地區)- 2025-2032 年產業預測全球汽車座椅加熱市場:2033 年的機會與策略2025 年全球汽車座椅市場報告汽車座椅加熱器市場-全球產業規模、佔有率、趨勢、機會和預測,按加熱技術、車輛類型、銷售管道、地區和競爭細分,2019-2029F汽車座椅市場 - 全球產業規模、佔有率、趨勢、機會和預測,按材料類型、技術、銷售通路、地區和競爭細分,2019-2029F

汽車座椅市場規模、佔有率和成長分析(按裝飾材料、座椅類型、車輛類型和地區)- 2025-2032 年產業預測全球汽車座椅加熱市場:2033 年的機會與策略2025 年全球汽車座椅市場報告汽車座椅加熱器市場-全球產業規模、佔有率、趨勢、機會和預測,按加熱技術、車輛類型、銷售管道、地區和競爭細分,2019-2029F汽車座椅市場 - 全球產業規模、佔有率、趨勢、機會和預測,按材料類型、技術、銷售通路、地區和競爭細分,2019-2029F