|

市場調查報告書

商品編碼

1665245

光感測器市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測Light Sensor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

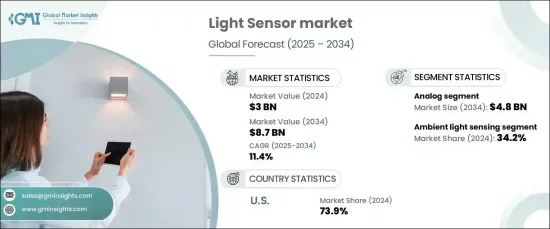

2024 年全球光感測器市場規模達到 30 億美元,預計將經歷大幅成長,預計 2025 年至 2034 年的複合年成長率為 11.4%。這些創新顯著提高了感測器功能,例如更寬的光譜檢測和在各種照明條件下增強的性能。因此,光感測器的應用正在擴展到多個行業,並提供了新的成長機會。

市場按類型細分為環境光感應、接近檢測、RGB 顏色感應、手勢識別和紫外線/紅外線 (IR) 檢測。其中,環境光感應領域在 2024 年佔據市場主導地位,佔有 34.2% 的佔有率。環境光感測器對於測量周圍光強度和調整設備設定以最佳化性能至關重要。這些感測器廣泛應用於電子產品,透過自動調節亮度等級和節省電力,幫助增強使用者體驗、提高能源效率並最佳化設備功能。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 30億美元 |

| 預測值 | 87億美元 |

| 複合年成長率 | 11.4% |

從產量來看,光感測器市場分為類比感測器和數位感測器。預計到 2034 年,類比感測器領域將產生 48 億美元的收入。它們的可靠性和與類比系統的無縫整合使其在環境光檢測、智慧照明和節能系統等應用中特別有益。消費性電子、汽車和工業自動化等產業越來越依賴這些感測器來提高營運效率和性能。

2024年美國光感測器市場佔全球市場佔有率的73.9%。這種主導地位很大程度上歸功於該國強大的技術基礎設施以及消費性電子、汽車和醫療保健等關鍵領域對光感測器的高需求。物聯網設備的日益普及和自主技術的進步進一步促進了對先進光感測器的需求不斷成長。此外,政府對智慧城市計畫和永續基礎設施的支持正在加速光感測器在公共和商業應用中的採用,進一步鞏固了美國作為市場領導者的地位。

目錄

第 1 章:方法論與範圍

- 市場範圍和定義

- 基礎估算與計算

- 預測計算

- 資料來源

- 基本的

- 次要

- 付費來源

- 公共資源

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 影響價值鏈的因素

- 利潤率分析

- 中斷

- 未來展望

- 製造商

- 經銷商

- 供應商概況

- 利潤率分析

- 重要新聞及舉措

- 監管格局

- 衝擊力

- 成長動力

- 光感測技術的技術進步

- 智慧型設備和物聯網應用的普及率不斷提高

- 增加節能解決方案和永續發展重點

- 汽車工業和自動駕駛汽車的成長

- 產業陷阱與挑戰

- 先進光感測技術成本高

- 整合複雜性和相容性問題

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第 5 章:市場估計與預測:按類型,2021 年至 2034 年

- 主要趨勢

- 環境光感應

- 接近探測器

- RGB 顏色感應

- 手勢識別

- 紫外線/紅外線(IR)檢測

第6章:市場估計與預測:依產量,2021-2034 年

- 主要趨勢

- 模擬

- 數位的

第 7 章:市場估計與預測:按技術,2021 年至 2034 年

- 主要趨勢

- 光電二極體

- 光電電晶體

- 電荷耦合元件 (CCD)

- 互補金屬氧化物半導體 (CMOS) 感測器

第 8 章:市場估計與預測:依最終用途,2021 年至 2034 年

- 主要趨勢

- 消費性電子產品

- 智慧型手機

- 電視機

- 平板電腦

- 穿戴式裝置

- 汽車

- 工業的

- 其他

第 9 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 中東及非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- Analog Devices, Inc.

- ams-OSRAM AG

- Broadcom Inc.

- Everlight Electronics Co., Ltd.

- Geospace Technologies Corporation

- Hamamatsu Photonics KK

- Honeywell International Inc.

- Infineon Technologies AG

- Kyocera Corporation

- Lite-On Technology Corporation

- Microchip Technology Incorporated

- NXP Semiconductors NV

- ON Semiconductor Corporation

- OSRAM Opto Semiconductors GmbH

- Panasonic Corporation

- ROHM Semiconductor

- Samsung Electronics Co., Ltd.

- Sharp Corporation

- STMicroelectronics NV

- TDK Corporation

- Texas Instruments Incorporated

- Vishay Intertechnology, Inc.

The Global Light Sensor Market reached USD 3 billion in 2024 and is expected to experience substantial growth, with a projected CAGR of 11.4% from 2025 to 2034. This impressive growth is being driven by rapid advancements in technology, which have led to the creation of highly sensitive, compact, and multi-spectral light sensors. These innovations have significantly improved sensor capabilities, such as broader spectrum detection and enhanced performance under various lighting conditions. As a result, the applications of light sensors are expanding across multiple industries, offering new opportunities for growth.

The market is segmented by type into ambient light sensing, proximity detection, RGB color sensing, gesture recognition, and UV/infrared (IR) detection. Among these, the ambient light sensing segment led the market in 2024, holding a 34.2% share. Ambient light sensors are crucial in measuring the surrounding light intensity and adjusting device settings to optimize performance. These sensors are widely used in electronics, helping to enhance user experience, improve energy efficiency, and optimize device functionality by automatically adjusting brightness levels and conserving power.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3 billion |

| Forecast Value | $8.7 billion |

| CAGR | 11.4% |

In terms of output, the light sensor market is divided into analog and digital sensors. The analog sensor segment is expected to generate USD 4.8 billion in revenue by 2034. Analog light sensors are preferred in applications that require continuous output signals proportional to light intensity, making them ideal for precise and real-time measurements. Their reliability and seamless integration with analog systems make them particularly beneficial in applications such as ambient light detection, smart lighting, and energy-saving systems. Industries like consumer electronics, automotive, and industrial automation are increasingly dependent on these sensors to improve operational efficiency and performance.

In 2024, the U.S. light sensor market accounted for 73.9% of the global market share. This dominance is largely due to the country's strong technological infrastructure and high demand for light sensors in key sectors like consumer electronics, automotive, and healthcare. The growing proliferation of IoT devices and advancements in autonomous technologies further contribute to the rising need for advanced light sensors. Moreover, government support for smart city projects and sustainable infrastructure is accelerating the adoption of light sensors in public and commercial applications, further solidifying the U.S. position as a market leader.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Technological advancements in light sensing technology

- 3.6.1.2 Rising adoption of smart devices and IoT applications

- 3.6.1.3 Increase in energy-efficient solutions and sustainability focus

- 3.6.1.4 Growth in automotive industry and autonomous vehicles

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High cost of advanced light sensing technologies

- 3.6.2.2 Integration complexity and compatibility issues

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021-2034 (USD Billion) (Volume Unit)

- 5.1 Key trends

- 5.2 Ambient light sensing

- 5.3 Proximity detector

- 5.4 RGB color sensing

- 5.5 Gesture recognition

- 5.6 UV/infrared light (IR) detection

Chapter 6 Market Estimates & Forecast, By Output, 2021-2034 (USD Billion) (Volume Unit)

- 6.1 Key trends

- 6.2 Analog

- 6.3 Digital

Chapter 7 Market Estimates & Forecast, By Technology, 2021-2034 (USD Billion) (Volume Unit)

- 7.1 Key trends

- 7.2 Photodiodes

- 7.3 Phototransistors

- 7.4 Charge-Coupled devices (CCDs)

- 7.5 Complementary metal-oxide-semiconductor (CMOS) sensors

Chapter 8 Market Estimates & Forecast, By End Use, 2021-2034 (USD Billion) (Volume Unit)

- 8.1 Key trends

- 8.2 Consumer electronics

- 8.2.1 Smartphones

- 8.2.2 Televisions

- 8.2.3 Tablets

- 8.2.4 Wearables

- 8.3 Automotive

- 8.4 Industrial

- 8.5 Other

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Volume Unit)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Analog Devices, Inc.

- 10.2 ams-OSRAM AG

- 10.3 Broadcom Inc.

- 10.4 Everlight Electronics Co., Ltd.

- 10.5 Geospace Technologies Corporation

- 10.6 Hamamatsu Photonics K.K.

- 10.7 Honeywell International Inc.

- 10.8 Infineon Technologies AG

- 10.9 Kyocera Corporation

- 10.10 Lite-On Technology Corporation

- 10.11 Microchip Technology Incorporated

- 10.12 NXP Semiconductors N.V.

- 10.13 ON Semiconductor Corporation

- 10.14 OSRAM Opto Semiconductors GmbH

- 10.15 Panasonic Corporation

- 10.16 ROHM Semiconductor

- 10.17 Samsung Electronics Co., Ltd.

- 10.18 Sharp Corporation

- 10.19 STMicroelectronics N.V.

- 10.20 TDK Corporation

- 10.21 Texas Instruments Incorporated

- 10.22 Vishay Intertechnology, Inc.

環境光感測器市場-全球產業分析、規模、佔有率、成長、趨勢及預測(2025-2035)

環境光感測器市場-全球產業分析、規模、佔有率、成長、趨勢及預測(2025-2035) 智慧型手機光學感測器市場:未來預測(2025-2030)

智慧型手機光學感測器市場:未來預測(2025-2030) 環境光感測器市場機會、成長動力、產業趨勢分析及 2025-2034 年預測

環境光感測器市場機會、成長動力、產業趨勢分析及 2025-2034 年預測 世界光學感測器 -市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)

世界光學感測器 -市場佔有率分析、產業趨勢/統計、成長預測(2025-2030) 日光感測器市場:按類型、安裝位置、最終應用分類 - 2025-2030 年全球預測

日光感測器市場:按類型、安裝位置、最終應用分類 - 2025-2030 年全球預測 全球環境光感測器市場(2024-2028)光學感測器市場:按整合度、功能、輸出和應用分類 - 2025-2030 年全球預測環境光感測器市場 - 全球產業規模、佔有率、趨勢、機會和預測,按感測器類型、輸出類型、安裝方式、應用、地區和競爭細分,2019-2029F環境光感測器的全球市場2024-2032 年按功能(環境光感應、接近檢測、RGB 顏色感應、手勢識別、紫外線/紅外光檢測)、輸出、整合、最終用途行業和地區分類的光感測器市場報告

全球環境光感測器市場(2024-2028)光學感測器市場:按整合度、功能、輸出和應用分類 - 2025-2030 年全球預測環境光感測器市場 - 全球產業規模、佔有率、趨勢、機會和預測,按感測器類型、輸出類型、安裝方式、應用、地區和競爭細分,2019-2029F環境光感測器的全球市場2024-2032 年按功能(環境光感應、接近檢測、RGB 顏色感應、手勢識別、紫外線/紅外光檢測)、輸出、整合、最終用途行業和地區分類的光感測器市場報告