|

市場調查報告書

商品編碼

1665287

太空最後一哩交付市場機會、成長動力、產業趨勢分析和 2025 - 2034 年預測Space Last-Mile Delivery Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

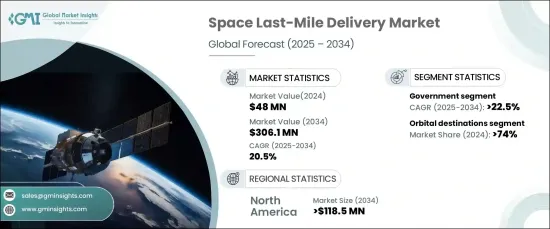

2024 年全球太空最後一哩交付市場價值 4,800 萬美元,並將經歷令人矚目的成長,預計 2025 年至 2034 年的年複合成長率(CAGR) 為 20.5%。軌道轉移飛行器和先進推進系統的創新使得有效載荷的放置和重新定位更加高效,從而使衛星網路、太空探索和商業營運比以往任何時候都更加有效。隨著太空商業化的不斷發展和可重複使用技術的進步,這些服務變得更具成本效益,並可被更廣泛的行業所使用。

太空最後一哩交付市場主要分為兩類:軌道目標和行星或地面目的地。 2024 年,軌道目的地領域佔據了 74% 的市場佔有率,預計未來幾年將實現強勁成長。為了實現全球寬頻覆蓋、地球觀測和通訊服務,衛星星座的持續部署極大地推動了對軌道傳輸解決方案的需求。各組織更加重視實現精確的軌道定位以最佳化衛星性能,並更加依賴最後一哩的運載系統和軌道轉移技術來滿足不斷變化的太空任務需求。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 4800萬美元 |

| 預測值 | 3.061億美元 |

| 複合年成長率 | 20.5% |

就最終用戶而言,市場分為商業和政府部門。政府部門預計將經歷最高的成長,到 2034 年預計複合年成長率為 22.5%。精確軌道定位的需求引發了人們對軌道轉移飛行器和在軌服務能力的更大興趣,這反過來又增強了國家安全並最佳化了衛星網路效率。

預計北美將引領太空最後一英里交付市場,到 2034 年規模將達到 1.185 億美元。用於地球觀測和通訊的衛星星座的持續部署進一步加劇了對先進的在軌物流系統的需求。各公司正專注於開發可重複使用的轉運飛行器和自動運載技術,以增強任務靈活性並降低成本,使太空作業更有效率、經濟實惠。

目錄

第 1 章:方法論與範圍

- 市場範圍和定義

- 基礎估算與計算

- 預測計算

- 資料來源

- 基本的

- 次要

- 付費來源

- 公共資源

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 影響價值鏈的因素

- 利潤率分析

- 中斷

- 未來展望

- 製造商

- 經銷商

- 供應商概況

- 利潤率分析

- 重要新聞及舉措

- 監管格局

- 衝擊力

- 成長動力

- 衛星部署數量不斷增加

- 商業太空企業的興起以及私營部門擴大參與太空探索

- 增加共乘和二次有效載荷發射

- 越來越關注永續性和減少太空垃圾

- 增加政府投資和太空計劃

- 產業陷阱與挑戰

- 開發和營運成本高

- 技術限制和可靠性

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第 5 章:市場估計與預測:按目的地,2021-2034 年

- 主要趨勢

- 軌道目的地

- 低地球軌道(LEO)

- 中地球軌道(MEO)

- 地球靜止軌道(GEO)

- 高地球軌道(GEO 以外)

- 行星/地面目的地

- 月球表面

- 火星表面

- 小行星表面

第6章:市場估計與預測:依交付酬載,2021-2034 年

- 主要趨勢

- 科學設備

- 基礎設施組件

- 太空站模組

- 衛星零件

- 耗材

- 推進劑/燃料

- 其他

第 7 章:市場估計與預測:按交付技術,2021 年至 2034 年

- 主要趨勢

- 自主系統

- 載人送貨

- 混合系統

第 8 章:市場估計與預測:依最終用途,2021 年至 2034 年

- 主要趨勢

- 商業的

- 政府

第 9 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 中東及非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- AAC Clyde Space

- Aliena

- Astro Digital

- D-Orbit

- Exotrail

- Impulse Space

- Momentus Space

- Orbit Fab

- Rocket Lab

- SEOPS (Space Exploration and Orbital Solutions)

- Spaceflight Industries

- SpaceLink

- TransAstra

The Global Space Last-Mile Delivery Market was valued at USD 48 million in 2024 and is set to experience impressive growth, with a projected compound annual growth rate (CAGR) of 20.5% from 2025 to 2034. This growth is being driven by an increasing demand for cutting-edge in-orbit logistics solutions and precise satellite deployment. Innovations in orbital transfer vehicles and advanced propulsion systems enable more efficient payload placement and repositioning, making satellite networks, space exploration, and commercial operations more effective than ever. With the growing commercialization of space and advancements in reusable technologies, these services are becoming more cost-effective and accessible to a broader range of industries.

The space last-mile delivery market is primarily divided into two categories: orbital targets and planetary or surface destinations. The orbital destinations segment held a dominant 74% market share in 2024 and is expected to see robust growth in the coming years. The expanding deployment of satellite constellations for global broadband coverage, Earth observation, and communication services is significantly boosting the demand for orbital delivery solutions. Organizations are placing greater emphasis on achieving precise orbital placement to optimize satellite performance, driving increased reliance on last-mile delivery systems and orbital transfer technologies to meet the evolving needs of space missions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $48 million |

| Forecast Value | $306.1 million |

| CAGR | 20.5% |

In terms of end users, the market is segmented into commercial and government sectors. The government segment is expected to experience the highest growth, with a projected CAGR of 22.5% through 2034. Governments worldwide are ramping up investments in last-mile delivery infrastructure to deploy critical defense satellites for surveillance, communications, and missile detection. The need for exact orbital positioning is fueling greater interest in orbital transfer vehicles and in-orbit servicing capabilities, which in turn enhances national security and optimizes satellite network efficiency.

North America is anticipated to lead the space last-mile delivery market, reaching USD 118.5 million by 2034. The United States is at the forefront of this growth, driven by its technological expertise in space exploration and commercialization. The escalating deployment of satellite constellations for Earth observation and communication is further intensifying the demand for advanced in-orbit logistics systems. Companies are focusing on developing reusable transfer vehicles and autonomous delivery technologies, which enhance mission flexibility and reduce costs, making space operations more efficient and affordable.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Growing number of satellite deployment

- 3.6.1.2 Rise of commercial space ventures and the growing private sector involvement in space exploration

- 3.6.1.3 Increasing ride-sharing and secondary payload launches

- 3.6.1.4 Growing focus on sustainability and mitigating space debris

- 3.6.1.5 Increasing governmental investments and space programs

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High development and operational costs

- 3.6.2.2 Technological limitations and reliability

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Destination, 2021-2034 (USD Million)

- 5.1 Key trends

- 5.2 Orbital destinations

- 5.2.1 Low earth orbit (LEO)

- 5.2.2 Medium earth orbit (MEO)

- 5.2.3 Geostationary orbit (GEO)

- 5.2.4 High earth orbit (Beyond GEO)

- 5.3 Planetary/surface destinations

- 5.3.1 Lunar surface

- 5.3.2 Martian surface

- 5.3.3 Asteroids surface

Chapter 6 Market Estimates & Forecast, By Delivery Payload, 2021-2034 (USD Million)

- 6.1 Key trends

- 6.2 Scientific equipment

- 6.3 Infrastructure components

- 6.3.1 Space station modules

- 6.3.2 Satellite components

- 6.4 Consumables

- 6.5 Propellants/fuel

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Delivery Technology, 2021-2034 (USD Million)

- 7.1 Key trends

- 7.2 Autonomous systems

- 7.3 Manned delivery

- 7.4 Hybrid systems

Chapter 8 Market Estimates & Forecast, By End Use, 2021-2034 (USD Million)

- 8.1 Key trends

- 8.2 Commercial

- 8.3 Government

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AAC Clyde Space

- 10.2 Aliena

- 10.3 Astro Digital

- 10.4 D-Orbit

- 10.5 Exotrail

- 10.6 Impulse Space

- 10.7 Momentus Space

- 10.8 Orbit Fab

- 10.9 Rocket Lab

- 10.10 SEOPS (Space Exploration and Orbital Solutions)

- 10.11 Spaceflight Industries

- 10.12 SpaceLink

- 10.13 TransAstra

2025 年至 2033 年自動駕駛最後一哩配送市場報告(按平台、解決方案、範圍(短程、長程)、應用和地區)

2025 年至 2033 年自動駕駛最後一哩配送市場報告(按平台、解決方案、範圍(短程、長程)、應用和地區) 全球自動駕駛最後一哩配送市場 - 2025 年至 2032 年

全球自動駕駛最後一哩配送市場 - 2025 年至 2032 年 2025年人工智慧賦能的最後一哩配送全球市場報告

2025年人工智慧賦能的最後一哩配送全球市場報告 2025 年首英里和最後一哩配送全球市場報告

2025 年首英里和最後一哩配送全球市場報告 全球最後一哩配送市場:市場規模、市場佔有率、趨勢、行業分析(依服務類型、技術、應用、配送時間和地區)、未來預測(2025-2034年)

全球最後一哩配送市場:市場規模、市場佔有率、趨勢、行業分析(依服務類型、技術、應用、配送時間和地區)、未來預測(2025-2034年) 自動駕駛最後一哩配送市場- 全球產業規模、佔有率、趨勢、機會和預測,按平台(空中配送無人機、地面配送無人機)、按應用、按有效載荷重量、按地區、按競爭進行細分,2020-2030F

自動駕駛最後一哩配送市場- 全球產業規模、佔有率、趨勢、機會和預測,按平台(空中配送無人機、地面配送無人機)、按應用、按有效載荷重量、按地區、按競爭進行細分,2020-2030F 印度最後一哩配送市場評估:依服務類型、技術、應用、配送時間、目的地和地區劃分的機會和預測(2018-2032年)

印度最後一哩配送市場評估:依服務類型、技術、應用、配送時間、目的地和地區劃分的機會和預測(2018-2032年) 2025 年自動駕駛最後一哩配送全球市場報告

2025 年自動駕駛最後一哩配送全球市場報告 全球最後一哩交付軟體市場:產業分析、規模、佔有率、成長、趨勢和預測,2025 年至 2032 年

全球最後一哩交付軟體市場:產業分析、規模、佔有率、成長、趨勢和預測,2025 年至 2032 年 德國最後一哩配送:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

德國最後一哩配送:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)