|

市場調查報告書

商品編碼

1666675

軟糖市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測Gummy Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

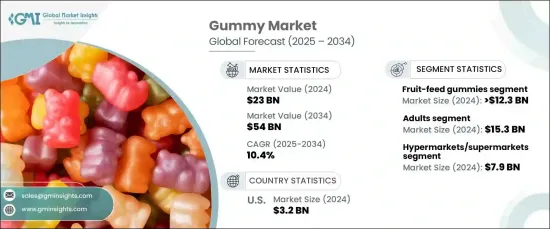

2024 年全球軟糖市場價值為 230 億美元,預計 2025 年至 2034 年期間將以 10.4% 的強勁複合年成長率成長。軟糖因其吸引人的外形、口味以及提供必需營養素的多功能性而成為不同人群的首選。

向天然和有機產品的轉變是市場成長的重要動力。採用真正的水果萃取物製作且不含合成添加劑的水果軟糖特別受到注重健康的消費者的歡迎。這些產品能夠提供維生素、抗氧化劑和其他必需營養素,滿足追求功能性和營養益處的個人的需求。此外,對植物性和清潔標籤產品的需求不斷成長,促進了有機和純素軟糖的採用,符合全球對更健康、無過敏原替代品的趨勢。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 230億美元 |

| 預測值 | 540億美元 |

| 複合年成長率 | 10.4% |

成年人群體正迅速崛起,成為軟糖產品的主要消費群體,標誌著其與兒童的傳統聯繫發生了轉變。越來越多的成年人喜歡用軟糖作為膳食補充劑,包括維生素、益生菌、膠原蛋白和 CBD。與傳統藥片或膠囊相比,軟糖的便利性、口味和易用性推動了這個細分市場的成長。該領域內的熱門類別包括針對美容、免疫和緩解壓力的保健產品,這對製造商來說是一個有利可圖的機會。

大賣場、超市等零售通路在軟糖市場擴張中扮演關鍵角色。這些網點讓消費者可以輕鬆購買到各種各樣的軟糖產品,從糖果到功能性補充劑。這些商店的可見性和便利性使其成為品牌接觸更廣泛受眾的理想平台。此外,折扣和捆綁銷售等促銷活動進一步提高了透過該管道的產品銷售量。

美國仍然是軟糖市場的主導力量,這得益於傳統軟糖和針對特定健康需求的功能性軟糖日益流行的推動。植物性、無糖和有機軟糖的創新正在吸引注重健康的消費者,而電子商務的興起和零售網路的不斷擴大則促進了市場滲透。隨著需求不斷成長,在消費者偏好不斷變化和產品持續創新的推動下,軟糖市場將迎來重大進步。

目錄

第 1 章:方法論與範圍

- 市場範圍和定義

- 基礎估算與計算

- 預測計算

- 資料來源

- 基本的

- 次要

- 付費來源

- 公共資源

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 影響價值鏈的因素

- 利潤率分析

- 中斷

- 未來展望

- 製造商

- 經銷商

- 供應商概況

- 利潤率分析

- 重要新聞及舉措

- 監管格局

- 衝擊力

- 成長動力

- 健康與保健趨勢

- 方便、輕鬆消費

- 產品不斷創新

- 對天然和清潔標籤產品的需求不斷增加

- 產業陷阱與挑戰

- 含糖量問題

- 供應鏈中斷

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第 5 章:市場估計與預測:按類型,2021 年至 2034 年

- 主要趨勢

- 水果軟糖

- CBD/THC 軟糖

- 益生菌軟糖

- 維生素軟糖

- 其他

第6章:市場估計與預測:依人口統計,2021-2034 年

- 主要趨勢

- 孩子們

- 成年人

- 老年人

第 7 章:市場估計與預測:按配銷通路,2021-2034 年

- 主要趨勢

- 大賣場/超市

- 專賣店

- 線上

- 品牌網站

- 電子商務平台

- 其他

第 8 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 中東及非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- Amway Corp.

- Bayer AG

- Catalent, Inc.

- Church & Dwight Co. Inc.

- GSK Plc

- H&H Group

- Haleon Group of Companies

- Nestle SA

- Otsuka Holdings Co., Ltd.

- Procter & Gamble

- Procaps Group

- Unilever PLC (OLLY)

The Global Gummy Market, valued at USD 23 billion in 2024, is projected to grow at a robust CAGR of 10.4% from 2025 to 2034. This remarkable expansion highlights the increasing demand for convenient and enjoyable health and wellness solutions among consumers. Gummies are becoming a preferred choice across demographics due to their appealing format, taste, and versatility in delivering essential nutrients.

The shift toward natural and organic products is a significant growth driver for the market. Fruit-based gummies crafted using real fruit extracts and free from synthetic additives are particularly popular among health-conscious consumers. With their ability to provide vitamins, antioxidants, and other essential nutrients, these products cater to individuals seeking functional and nutritional benefits. Additionally, the rising demand for plant-based and clean-label products is bolstering the adoption of organic and vegan gummies, aligning with global trends for healthier, allergen-free alternatives.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $23 Billion |

| Forecast Value | $54 Billion |

| CAGR | 10.4% |

The adult segment is rapidly emerging as a key consumer base for gummy products, marking a shift from their traditional association with children. Adults increasingly prefer gummies for dietary supplements, including vitamins, probiotics, collagen, and CBD. This segment's growth is fueled by the convenience, taste, and ease of use that gummies offer compared to traditional pills or capsules. Popular categories within this segment include wellness products targeting beauty, immunity, and stress relief, making them a lucrative opportunity for manufacturers.

Retail channels such as hypermarkets and supermarkets are playing a pivotal role in the gummy market's expansion. These outlets provide consumers with easy access to a diverse range of gummy products, from candy to functional supplements. The visibility and convenience of these stores make them an ideal platform for brands to reach a wider audience. Additionally, promotional activities like discounts and bundled offerings further enhance product sales through this channel.

The U.S. remains a dominant force in the gummy market, driven by the growing popularity of both traditional gummies and functional variants designed to address specific health needs. Innovations in plant-based, sugar-free, and organic gummies are attracting health-conscious consumers, while the rise of e-commerce and expanding retail networks contribute to market penetration. As demand continues to grow, the gummy market is poised for significant advancements, driven by evolving consumer preferences and ongoing product innovation.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Health and wellness trends

- 3.6.1.2 Convenience and easy consumption

- 3.6.1.3 Continuous innovation in products

- 3.6.1.4 Increasing demand for natural and clean-label products

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Sugar content concerns

- 3.6.2.2 Supply chain disruptions

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Fruit-feed gummies

- 5.3 CBD/THC gummies

- 5.4 Probiotic gummies

- 5.5 Vitamin gummies

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Demography, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Children

- 6.3 Adults

- 6.4 Seniors

Chapter 7 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Hypermarkets/Supermarkets

- 7.3 Specialty stores

- 7.4 Online

- 7.4.1 Brand websites

- 7.4.2 E-commerce platforms

- 7.5 Others

Chapter 8 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Amway Corp.

- 9.2 Bayer AG

- 9.3 Catalent, Inc.

- 9.4 Church & Dwight Co. Inc.

- 9.5 GSK Plc

- 9.6 H&H Group

- 9.7 Haleon Group of Companies

- 9.8 Nestle SA

- 9.9 Otsuka Holdings Co., Ltd.

- 9.10 Procter & Gamble

- 9.11 Procaps Group

- 9.12 Unilever PLC (OLLY)

軟糖市場 - 全球產業規模、佔有率、趨勢、機會和預測,按產品、成分、最終用途、配銷通路、地區和競爭細分,2020-2030 年

軟糖市場 - 全球產業規模、佔有率、趨勢、機會和預測,按產品、成分、最終用途、配銷通路、地區和競爭細分,2020-2030 年 全球膠原蛋白軟糖市場:產業分析、規模、佔有率、成長、趨勢和預測,2025-2032 年

全球膠原蛋白軟糖市場:產業分析、規模、佔有率、成長、趨勢和預測,2025-2032 年 膠原蛋白軟糖的全球市場 - 全球產業分析,規模,佔有率,成長,趨勢,預測(2032年)

膠原蛋白軟糖的全球市場 - 全球產業分析,規模,佔有率,成長,趨勢,預測(2032年) 軟糖市場 - 成長、未來展望、競爭分析,2025年~2033年軟糖市場、佔有率、規模、趨勢、行業分析報告:按產品、按成分、按最終用途、按分銷渠道、按地區、按細分市場、預測,2024-2032 年全球軟糖市場:按產品類型、最終用戶、地區 - 全球產業分析、規模、佔有率、成長、趨勢、預測(2023-2030)

軟糖市場 - 成長、未來展望、競爭分析,2025年~2033年軟糖市場、佔有率、規模、趨勢、行業分析報告:按產品、按成分、按最終用途、按分銷渠道、按地區、按細分市場、預測,2024-2032 年全球軟糖市場:按產品類型、最終用戶、地區 - 全球產業分析、規模、佔有率、成長、趨勢、預測(2023-2030) 全球軟糖市場 - 2023-2030 年

全球軟糖市場 - 2023-2030 年