|

市場調查報告書

商品編碼

1666908

區域供熱管網市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測District Heating Pipeline Network Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

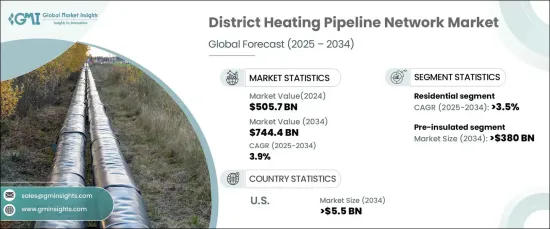

2024 年全球區域供熱管道網路市場價值為 5057 億美元,預計在 2025 年至 2034 年期間將以 3.9% 的複合年成長率穩步成長。區域供熱管道透過減少熱量損失、提高能源節約和符合全球永續發展目標,為現代能源挑戰提供了解決方案。

隨著城市人口的增加和政府實施更嚴格的能源標準,區域供熱解決方案的採用將會加速。這些系統不僅提高了能源效率,而且顯著降低了碳排放,使其成為智慧城市計畫的基石。它們整合生質能能、太陽熱能和地熱能等再生能源的能力凸顯了它們在創造有彈性、環保的基礎設施方面的重要性。此外,經濟效益(降低能源成本和長期運作效率)使區域供熱管道成為全球住宅、商業和工業應用的有吸引力的投資。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 5057億美元 |

| 預測值 | 7444億美元 |

| 複合年成長率 | 3.9% |

隨著永續基礎設施投資的不斷增加,預製絕緣區域供熱管道網路預計到 2034 年將產生 3,800 億美元的收入。這些管道經過精心設計,可承受高溫並具有無與倫比的耐用性,非常適合需要大量供暖的地區。其創新設計最大限度地減少了熱量損失,最佳化了能源消耗,並支持大型城市計畫。隨著開發商優先考慮節能技術,預絕緣管道已成為現代永續供熱系統的代名詞。它們在降低熱效率和降低溫室氣體排放方面發揮作用,使其成為城市實現環境基準的關鍵解決方案。

在住宅領域,到 2034 年,區域供熱管道市場預計將以 3.5% 的速度成長。區域供熱系統為家庭供暖和供應熱水提供了一種無縫且經濟有效的方法,同時減少了對單一加熱裝置的依賴。它們與再生能源的兼容性進一步增強了它們的吸引力,使家庭能夠轉向更綠色的能源選擇。隨著各國政府強調碳中和和能源效率,住宅採用區域供熱系統預計將激增,使其成為未來城市規劃不可或缺的一部分。

在美國,區域供熱管網市場預計到 2034 年將創收 55 億美元。全國各地的城市正在實施先進的區域供熱系統,以滿足能源需求和脫碳目標。預製絕緣管道具有減少熱損失、提高運作效率的能力,已成為城市供熱項目中不可或缺的一部分。隨著各市政當局努力降低溫室氣體排放並將再生能源納入其框架,對尖端供熱解決方案的需求持續上升,使得美國成為區域供熱網路的關鍵市場。

目錄

第 1 章:方法論與範圍

- 市場範圍和定義

- 市場估計和預測參數

- 預測計算

- 資料來源

- 基本的

- 次要

- 有薪資的

- 民眾

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 監管格局

- 產業衝擊力

- 成長動力

- 產業陷阱與挑戰

- 成長潛力分析

- 波特的分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- PESTEL 分析

第4章:競爭格局

- 介紹

- 戰略展望

- 創新與永續發展格局

第5章:市場規模及預測:按管道,2021 – 2034 年

- 主要趨勢

- 預絕緣鋼

- 聚合物

第6章:市場規模及預測:依直徑,2021 – 2034 年

- 主要趨勢

- 20-100 毫米

- 101-300 毫米

- ≥300毫米

第 7 章:市場規模與預測:按應用,2021 – 2034 年

- 主要趨勢

- 住宅

- 商業的

- 工業的

第 8 章:市場規模與預測:按地區,2021 – 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 波蘭

- 瑞典

- 俄羅斯

- 義大利

- 英國

- 芬蘭

- 丹麥

- 亞太地區

- 中國

- 日本

- 韓國

第9章:公司簡介

- Aquatherm

- Brugg Pipes

- CPV

- Golan Plastic Products

- Isoplus

- Ke Kelit

- Logstor

- Mannesmann Line Pipe

- Microflex

- Perma-Pipe

- Pipelife

- Rehau

- Thermaflex

- Uponor

The Global District Heating Pipeline Network Market, valued at USD 505.7 billion in 2024, is set to grow at a steady CAGR of 3.9% between 2025 and 2034. This growth reflects a transformative shift toward sustainable energy technologies and a heightened demand for energy-efficient heating systems. District heating pipelines offer a solution to modern energy challenges by reducing heat loss, improving energy conservation, and aligning with global sustainability goals.

As urban populations expand and governments enforce stricter energy standards, the adoption of district heating solutions is poised to accelerate. These systems not only enhance energy efficiency but also significantly lower carbon emissions, making them a cornerstone of smart city initiatives. Their ability to integrate renewable energy sources such as biomass, solar thermal, and geothermal energy underscores their importance in creating resilient, eco-friendly infrastructure. Furthermore, the economic benefits-reduced energy costs and long-term operational efficiency-make district heating pipelines an attractive investment for residential, commercial, and industrial applications worldwide.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $505.7 Billion |

| Forecast Value | $744.4 Billion |

| CAGR | 3.9% |

The pre-insulated district heating pipeline network is anticipated to generate USD 380 billion by 2034, driven by increasing investments in sustainable infrastructure. These pipelines are engineered to endure high temperatures and deliver unmatched durability, making them ideal for regions with extensive heating requirements. Their innovative design minimizes heat loss, optimizes energy consumption, and supports large-scale urban projects. As developers prioritize energy-efficient technologies, pre-insulated pipelines have become synonymous with modern, sustainable heating systems. Their role in reducing thermal inefficiencies and lowering greenhouse gas emissions positions them as a pivotal solution for cities aiming to achieve environmental benchmarks.

In the residential sector, the district heating pipeline market is projected to grow at a rate of 3.5% through 2034. The rising preference for eco-friendly heating solutions in densely populated urban areas is a key factor propelling this growth. District heating systems provide a seamless and cost-effective method for heating homes and supplying hot water while reducing reliance on individual heating units. Their compatibility with renewable energy sources further enhances their appeal, enabling households to transition toward greener energy options. With governments emphasizing carbon neutrality and energy efficiency, residential adoption of district heating systems is expected to surge, making them an integral part of future urban planning.

In the United States, the district heating pipeline network market is forecasted to generate USD 5.5 billion by 2034. Significant investments in urban development and energy-efficient infrastructure are driving this growth. Cities across the country are implementing advanced district heating systems to meet energy mandates and decarbonization goals. Pre-insulated pipelines, with their ability to reduce thermal losses and improve operational efficiency, are becoming indispensable for urban heating projects. As municipalities strive to lower greenhouse gas emissions and incorporate renewable energy into their frameworks, the demand for cutting-edge heating solutions continues to rise, positioning the US as a pivotal market for district heating networks.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Pipe, 2021 – 2034 (km & USD Billion)

- 5.1 Key trends

- 5.2 Pre-insulated steel

- 5.3 Polymer

Chapter 6 Market Size and Forecast, By Diameter, 2021 – 2034 (km & USD Billion)

- 6.1 Key trends

- 6.2 20-100 mm

- 6.3 101-300 mm

- 6.4 ≥300 mm

Chapter 7 Market Size and Forecast, By Application, 2021 – 2034 (km & USD Billion)

- 7.1 Key trends

- 7.2 Residential

- 7.3 Commercial

- 7.4 Industrial

Chapter 8 Market Size and Forecast, By Region, 2021 – 2034 (km & USD Billion)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 Poland

- 8.3.3 Sweden

- 8.3.4 Russia

- 8.3.5 Italy

- 8.3.6 UK

- 8.3.7 Finland

- 8.3.8 Denmark

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 South Korea

Chapter 9 Company Profiles

- 9.1 Aquatherm

- 9.2 Brugg Pipes

- 9.3 CPV

- 9.4 Golan Plastic Products

- 9.5 Isoplus

- 9.6 Ke Kelit

- 9.7 Logstor

- 9.8 Mannesmann Line Pipe

- 9.9 Microflex

- 9.10 Perma-Pipe

- 9.11 Pipelife

- 9.12 Rehau

- 9.13 Thermaflex

- 9.14 Uponor

區域供熱:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

區域供熱:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 全球區域供熱市場研究報告 - 產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年

全球區域供熱市場研究報告 - 產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年 區域供熱市場,規模,佔有率,趨勢,產業分析報告:各能源來源,各用途,各技術,各地區 - 2025~2034年市場預測

區域供熱市場,規模,佔有率,趨勢,產業分析報告:各能源來源,各用途,各技術,各地區 - 2025~2034年市場預測 2025 年全球區域供熱市場報告歐洲區域供熱 -市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

2025 年全球區域供熱市場報告歐洲區域供熱 -市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 區域供熱市場:按熱源、組件、設備類型和應用分類 - 2025-2030 年全球預測

區域供熱市場:按熱源、組件、設備類型和應用分類 - 2025-2030 年全球預測 全球區域供熱市場(2024-2028)

全球區域供熱市場(2024-2028) 全球熱網市場,2024-2028

全球熱網市場,2024-2028 區域供熱市場規模、佔有率、趨勢分析報告:按熱源、按應用、按工廠類型、按地區、細分市場預測,2024-2030區域供熱市場規模 - 按應用(住宅、商業{學院/大學、辦公大樓、政府/軍事}、工業{化工、煉油廠、造紙})、按來源、按區域展望和預測,2024 - 2032 年

區域供熱市場規模、佔有率、趨勢分析報告:按熱源、按應用、按工廠類型、按地區、細分市場預測,2024-2030區域供熱市場規模 - 按應用(住宅、商業{學院/大學、辦公大樓、政府/軍事}、工業{化工、煉油廠、造紙})、按來源、按區域展望和預測,2024 - 2032 年