|

市場調查報告書

商品編碼

1667146

分析儀器市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測Analytical Instrumentation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

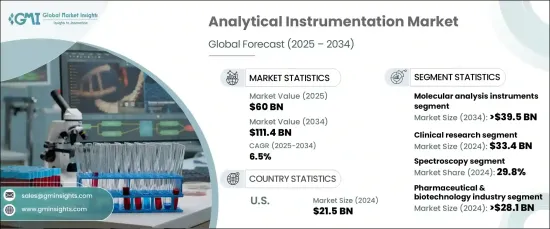

2024 年全球分析儀器市場價值將達到 600 億美元,預計將大幅成長,預計 2025 年至 2034 年的複合年成長率為 6.5%。尤其是製藥和生物技術行業,正在推動這一需求,因為他們優先考慮嚴格的品質控制措施和遵守監管標準。分析儀器在醫療保健領域的應用日益廣泛,再加上材料科學、環境監測和化學分析領域的創新,凸顯了市場在現代工業中的多功能性和重要性。

人們對個人化醫療的興趣日益濃厚,加上慢性病的盛行,刺激了複雜診斷工具的採用。分析儀器在臨床實驗室和診斷中心發揮關鍵作用,能夠提供準確、高效的測試解決方案。此外,各行各業都在增加對研發的投資,以提高產品品質和永續性,進一步推動了這些工具的採用。這些趨勢以及對環保實踐的日益重視,正在推動各行各業將先進的分析解決方案融入其營運中。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 600億美元 |

| 預測值 | 1114億美元 |

| 複合年成長率 | 6.5% |

市場依產品類型分類,包括電化學分析儀器、層析儀器、分子分析儀器、光譜儀器、粒子計數器及分析儀等。其中,分子分析儀器表現突出,預計複合年成長率為 6.9%,到 2034 年將達到 395 億美元。對分子水平分析精度的不斷成長的需求推動了醫療保健和學術研究等各個領域的需求。

按技術分類,市場涵蓋光譜學、色譜學、粒子分析、聚合酶鏈反應和其他方法。 2024 年,光譜學佔了 29.8% 的市場佔有率,價值 179 億美元。光譜技術的廣泛應用歸功於其對化學和分子結構進行無損分析的能力。這些方法廣泛應用於生物技術、製藥和材料科學,支持產品開發和品質保證的創新。

在美國,分析儀器市場在 2024 年創造了 215 億美元的收入,預計到 2034 年將以 6.2% 的複合年成長率成長。藥物開發、臨床試驗和生物標記研究中先進分析工具的使用正在加速。個人化醫療計劃和精準診斷設備的需求進一步推動了臨床和研究領域的市場擴張。

目錄

第 1 章:方法論與範圍

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 技術進步

- 製藥業和政府研究機構的研發支出不斷增加

- 精準醫療應用分析儀器的採用日益增多

- 慢性病盛行率不斷上升

- 產業陷阱與挑戰

- 儀器成本高

- 缺乏熟練的專業人員

- 成長動力

- 成長潛力分析

- 2024 年定價分析

- 監管格局

- 美國

- 歐洲

- 2021 – 2034 年產量分析(單位)

- 全球的

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東及非洲

- 技術格局

- 報銷場景

- 未來市場趨勢

- 差距分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司矩陣分析

- 公司市佔率分析

- 競爭定位矩陣

- 供應商矩陣分析

- 策略儀表板

第 5 章:市場估計與預測:按產品,2021 年至 2034 年

- 主要趨勢

- 分子分析儀器

- 光譜儀器

- 色譜儀器

- 電化學分析儀器

- 粒子計數器和分析儀

- 其他產品

第6章:市場估計與預測:按技術,2021 – 2034 年

- 主要趨勢

- 光譜學

- 色譜法

- 顆粒分析

- 聚合酶連鎖反應

- 其他技術

第 7 章:市場估計與預測:按應用,2021 年至 2034 年

- 主要趨勢

- 臨床研究

- 臨床診斷

第 8 章:市場估計與預測:依最終用途,2021 年至 2034 年

- 主要趨勢

- 製藥及生技產業

- 研究和學術機構

- 診斷中心

- 其他最終用途

第 9 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 波蘭

- 瑞典

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 泰國

- 印尼

- 菲律賓

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 哥倫比亞

- 智利

- 秘魯

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 以色列

- 土耳其

- 伊朗

第10章:公司簡介

- Agilent

- Avantor

- BIO-RAD

- BRUKER

- Danaher

- Eppendorf

- HITACHI

- Illumina

- Malvern Panalytical

- Metrohm

- METTLER TOLEDO

- Revvity (PerkinElmer)

- Roche

- Sartorius

- SHIMADZU

- Thermo Fisher Scientific

- Waters

- ZEISS Group

The Global Analytical Instrumentation Market, valued at USD 60 billion in 2024, is poised for significant growth, with projections indicating a CAGR of 6.5% from 2025 to 2034. This upward trajectory reflects the increasing integration of advanced technologies and the escalating demand for precision and accuracy across industries. Pharmaceutical and biotechnology sectors, in particular, are driving this demand as they prioritize stringent quality control measures and compliance with regulatory standards. The expanding applications of analytical instruments in healthcare, coupled with innovations in materials science, environmental monitoring, and chemical analysis, underscore the market's versatility and importance in modern industries.

Rising interest in personalized medicine, coupled with the prevalence of chronic diseases, has spurred the adoption of sophisticated diagnostic tools. Analytical instruments are playing a pivotal role in clinical laboratories and diagnostic centers, enabling accurate and efficient testing solutions. Additionally, industries are increasingly investing in R&D to enhance product quality and sustainability, further fueling the adoption of these tools. These trends, along with the growing emphasis on eco-friendly practices, are pushing industries to integrate advanced analytical solutions into their operations.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $60 Billion |

| Forecast Value | $111.4 Billion |

| CAGR | 6.5% |

The market is categorized by product types, including electrochemical analysis instruments, chromatography instruments, molecular analysis instruments, spectroscopy instruments, particle counters and analyzers, and others. Among these, molecular analysis instruments stand out with a projected CAGR of 6.9%, expected to reach USD 39.5 billion by 2034. This segment's growth is fueled by the increasing adoption of cutting-edge techniques in research and diagnostics, particularly in genomics and proteomics. The rising need for precision in molecular-level analysis is driving demand across various sectors, including healthcare and academic research.

By technology, the market encompasses spectroscopy, chromatography, particle analysis, polymerase chain reaction, and other methods. Spectroscopy held a significant 29.8% market share in 2024, valued at USD 17.9 billion. The widespread adoption of spectroscopic techniques is attributed to their ability to perform non-destructive analyses of chemical and molecular structures. These methods are extensively used in biotechnology, pharmaceuticals, and materials science, supporting innovations in product development and quality assurance.

In the United States, the analytical instrumentation market generated USD 21.5 billion in revenue in 2024 and is forecast to grow at a CAGR of 6.2% through 2034. This growth is primarily driven by advancements in the pharmaceutical and biotechnology industries. The adoption of advanced analytical tools for drug development, clinical trials, and biomarker research has been accelerating. Personalized medicine initiatives and the need for precise diagnostic devices are further propelling market expansion in both clinical and research domains.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Technological advancements

- 3.2.1.2 Rising R&D spending by pharmaceutical industry & government research organizations

- 3.2.1.3 Increasing adoption of analytical instrumentation for precision medicine applications

- 3.2.1.4 Growing prevalence of chronic diseases

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of instruments

- 3.2.2.2 Lack of skilled professionals

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Pricing analysis, 2024

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 MEA

- 3.5 Regulatory landscape

- 3.5.1 U.S.

- 3.5.2 Europe

- 3.6 Volume analysis, 2021 – 2034 (Units)

- 3.6.1 Global

- 3.6.2 North America

- 3.6.3 Europe

- 3.6.4 Asia Pacific

- 3.6.5 Latin America

- 3.6.6 MEA

- 3.7 Technology landscape

- 3.8 Reimbursement scenario

- 3.9 Future market trends

- 3.10 Gap analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive positioning matrix

- 4.5 Vendor matrix analysis

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Molecular analysis instruments

- 5.3 Spectroscopy instruments

- 5.4 Chromatography instruments

- 5.5 Electrochemical analysis instruments

- 5.6 Particle counters and analyzers

- 5.7 Other products

Chapter 6 Market Estimates and Forecast, By Technology, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Spectroscopy

- 6.3 Chromatography

- 6.4 Particle analysis

- 6.5 Polymerase chain reaction

- 6.6 Other technologies

Chapter 7 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Clinical research

- 7.3 Clinical diagnostics

Chapter 8 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Pharmaceutical & biotechnology industry

- 8.3 Research and academic institutes

- 8.4 Diagnostic centers

- 8.5 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Poland

- 9.3.7 Sweden

- 9.3.8 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Thailand

- 9.4.7 Indonesia

- 9.4.8 Philippines

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Columbia

- 9.5.5 Chile

- 9.5.6 Peru

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

- 9.6.4 Israel

- 9.6.5 Turkey

- 9.6.6 Iran

Chapter 10 Company Profiles

- 10.1 Agilent

- 10.2 Avantor

- 10.3 BIO-RAD

- 10.4 BRUKER

- 10.5 Danaher

- 10.6 Eppendorf

- 10.7 HITACHI

- 10.8 Illumina

- 10.9 Malvern Panalytical

- 10.10 Metrohm

- 10.11 METTLER TOLEDO

- 10.12 Revvity (PerkinElmer)

- 10.13 Roche

- 10.14 Sartorius

- 10.15 SHIMADZU

- 10.16 Thermo Fisher Scientific

- 10.17 Waters

- 10.18 ZEISS Group

催化劑篩檢合成設備市場按產品類型、應用和最終用戶分類 - 全球預測 2025-2030

催化劑篩檢合成設備市場按產品類型、應用和最終用戶分類 - 全球預測 2025-2030 2025年全球燃料特性分析儀市場報告

2025年全球燃料特性分析儀市場報告 分析儀器市場:依產品類型、技術、應用和地區分類2024 年分析儀器全球市場報告分析儀器市場:按產品、技術和應用分類 - 2025-2030 年全球預測過程分析儀市場:按類型、應用和最終用戶產業分類 - 2025-2030 年全球預測食品檢測和分析儀器市場:按產品、技術和應用分類 - 2025-2030 年全球預測

分析儀器市場:依產品類型、技術、應用和地區分類2024 年分析儀器全球市場報告分析儀器市場:按產品、技術和應用分類 - 2025-2030 年全球預測過程分析儀市場:按類型、應用和最終用戶產業分類 - 2025-2030 年全球預測食品檢測和分析儀器市場:按產品、技術和應用分類 - 2025-2030 年全球預測 過程分析設備:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)

過程分析設備:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029) 食品醣類水解酵素的全球市場規模:各產品,各用途,各地區,範圍及預測

食品醣類水解酵素的全球市場規模:各產品,各用途,各地區,範圍及預測 分析儀器:工業市場機會

分析儀器:工業市場機會